13.08.2019

0

926

4 min.

There are several reasons why you need a 2nd personal income tax certificate upon dismissal. It may be required for submission to government agencies and banking organizations, and may also be needed at a new job. Usually it is included in the package of documents requested by social institutions that award various types of benefits from the state. The basis for issuance is a simple requirement, and the place is the organization where the citizen worked for a certain period of time. He cannot refuse this request; in these cases, he has the right to involve regulatory authorities. Particular attention is paid to the proper execution of the certificate in accordance with accepted standards.

What certificates can you take when leaving your job?

A dismissed employee has the right to request from his employer any certificate related to his work activity, both during the period of work and after dismissal.

The basis for termination of an employment contract does not have any impact on the list of certificates issued - it can be either the employee’s own desire or any other reason (for example, the employer’s initiative, agreement of the parties).

List of certificates that an employee has the right to request at the place of former work upon dismissal:

- Salary information for the last 2 years of work. For registration, standard form 182-N is used. This data will be required to calculate sick leave benefits at your next place of employment.

- An indicator of average earnings used to determine unemployment benefits for it. Information on the average salary for the central labor center is compiled for the last 3 months.

- Certificate 2-NDFL about income. It reflects information about income tax paid on the earnings of a particular citizen and personal income tax deductions provided to him.

- Certificates drawn up according to the forms SZV-STAZH, SZV-M, as well as SPV-2, issued when an employee retires, and calculation of insurance premiums (section 3).

If necessary, the outgoing employee has the right to request other certificates, as well as copies of official papers (for example, a copy of management’s order to terminate the employment relationship).

Applications for certificates can be found in this article.

Registration rules and issuance procedure

The form for filling out a certificate of income for an individual is established by order of the Federal Tax Service dated October 30, 2015. The form is filled out according to strict rules that cannot be changed at the discretion of the employer or employee.

The document has a certain procedure for filling out:

- the contents of the document indicate only those payments that are subject to tax deductions. The date of issue and period must be indicated at the top of the form;

- Next comes the column called “Data about the tax agent.” It contains information about the employer, the full name of the organization and all details;

- then the form contains information about the employee: Full name. in full, employee citizenship, status, passport details, place of residence and registration;

- Below is information about the employee’s income separately for each month of the period. In addition to the amount, the income code is indicated;

- after the income, data on various deductions is written down, and below is the total amount of the tax deduction;

- withheld tax is displayed only in rubles, without kopecks. Amounts containing kopecks are rounded according to general rules: if less than 50 kopecks, then it is not taken into account, if more than 50 kopecks, then it is rounded up to the nearest ruble;

- the declaration does not indicate tax-free payments, for example: severance pay, payments related to maternity leave and childbirth, compensation for layoffs, payments for physical or moral harm.

The 2-NDFL certificate is issued no later than three working days from the date of submission of the application in writing by the dismissed employee. If requested at the time of dismissal, the certificate must be issued on the same day.

When applying orally, the issuance deadlines will be more blurred; it all depends on the employer. A written appeal can be written in any form, but be sure to indicate the request itself and the period.

You can send it by mail electronically or carry it yourself; you must register it. Issuance of a certificate of income upon request is free of charge.

A sample certificate of income upon dismissal is available.

Is the employer obliged to issue them himself?

When an employee quits, his employer returns his work book and finally pays him off. These procedures are carried out directly on the day of dismissal of a working citizen.

If on the day of termination of the employment relationship the employee does not pick up the work book, the employer must send him a notice of the need to receive it.

If a departing employee requires any paperwork related to his employment, he must contact his employer with the appropriate written request. The head of the organization is obliged to satisfy the request by providing the applicant with certified copies of the necessary documents.

These rules are clearly stated in Part 4 of Art. 84.1 of the Labor Code of the Russian Federation, which regulates the general procedure for compliance with formal procedures when dismissing an employee.

It is mandatory that the management of the organization issues the following official documents relating to work activities to the outgoing employee:

- The work record of this citizen.

- Certificate drawn up in form 182-N. It is used to determine the appropriate hospital benefits intended for an individual and reflects information about his earnings (income received) for the previous 2 years.

- Documentary confirmation of pension contributions and other insurance contributions made in favor of a specific employee.

- Certificate 2-NDFL, which shows the income paid to this person, as well as the amount of income tax withheld and transferred from this income.

The employer prepares and issues other documentation requested by the dismissed citizen within 3 days, counted from the date of submission of the relevant request (it is submitted in writing). This requirement is clearly stated in Part 1 of Art. 62 of the Labor Code of the Russian Federation, which regulates the issuance to an employee of papers relating to his work activity.

Form 182n for calculating sick leave benefits

The certificate, which is issued in standard form 182n, contains information about the income received by employees for the previous two-year period before dismissal.

Such data is taken into account to calculate benefits payable to a citizen in connection with his temporary disability (that is, on sick leave), as well as in connection with maternity (maternity leave). The information indicated in this certificate allows you to calculate the average salary of a person, which, in turn, is needed to determine the amount of the benefit.

As you know, the amount of sick leave benefits is determined based on income received in the last two years preceding the year in which this citizen fell ill. It is necessary to ensure that the relevant data is available, since there is a possibility that the employee will need it at the new place of employment. After all, he may get sick or, alternatively, go on maternity leave.

If the worker does not submit 182n to his new employer before handing over the certificate of incapacity for work, the sick leave benefit will be calculated for him according to the minimum wage, that is, it will be minimal. Such a settlement could result in a significant loss of money owed.

That is why the employee must ensure that this certificate is available in a timely manner. If the employer did not independently issue Form 182n for some reason, you need to request it yourself.

The current form 182 is contained in Appendix No. 1 to Order of the Ministry of Labor of Russia No. 182n dated April 30, 2003, as last amended as of January 9, 2017. This form can be downloaded for free from the link below in Word format.

.

2-NDFL on employee income

Form 2-NDFL reflects information about the employee’s taxable income, personal income tax amounts withheld from him and issued income tax deductions for a specific reporting year.

A working citizen will need this form if he will receive deductions through a new employer (if there are appropriate grounds) or directly through a division of the tax department.

If a citizen applies for this deduction, the actually transferred tax amount, which is indicated in the 2-NDFL certificate, will be legally returned to the applicant citizen.

If the employer himself does not issue 2-NDFL upon dismissal, then in order to receive it, the resigning employee submits an appropriate application to him.

The current 2-NDFL form is approved by Order of the Federal Tax Service of Russia No. ММВ-7-11/ [email protected] dated 10/02/2018. This download form is presented below.

.

Is SZV-STAZH needed?

It should be noted that the SZV-STAZH documentary template has been used since 2017. This form contains information about the insurance premiums actually paid for a specific employee.

Upon dismissal, SZV-STAZH is issued to the employee directly on the agreed day of departure. You do not need to make a special request to receive this paper.

If the employer does not issue such a certificate, he may be held accountable (company management is punishable by a fine).

The current SZV-STAZH form is approved by the Resolution of the Board of the Pension Fund of the Russian Federation dated December 6, 2018 No. 507p, you can download it below for free in xls format.

.

What to do if they don’t give you documents?

The resigning citizen must receive a paycheck (all due payments), a work book and additional papers related to work on the day of his dismissal from his place of work. The date of such disposal is always determined in advance.

Some documentation is provided to the departing employee without the requirement to submit a written application. To obtain some certificates (papers), an individual still has to make the necessary request in writing, addressing it directly to the management of the organization.

One way or another, the employer’s refusal to issue mandatory documents and satisfy the request of a resigning employee to provide additional certificates is considered unlawful.

If management does not issue certificates upon dismissal, you will have to answer according to the law if the retiring employee, whose rights have been infringed, wishes to implement the appropriate procedure:

- The applicant prepares a written request to receive the required papers and addresses it to the company management. Such a paper can be drawn up in two copies by submitting it through the director’s office. In this case, the applicant’s copy must bear the secretary’s acceptance mark. Another way is to send this request by mail, that is, by registered mail (the sender is notified that this letter has been sent to the addressee).

- If the employer does not respond adequately within three days, the applicant can send a corresponding complaint to the competent authority - the labor inspectorate or the prosecutor's office. Alternatively, you can transfer this complaint to both government agencies at once. The paper can be delivered in person, by mail or online.

- The complaint is considered by the regulatory government agency within 30 days, counted from the date of its receipt.

- After considering the complaint, government agencies will conduct a proper investigation. The employer will be brought to appropriate administrative liability (if his guilt is officially established and confirmed).

What is reflected in the 2-NDFL certificate

The certificate must include the amounts paid to the dismissed person, starting from January 1 to the date of termination of the contract with him. At the same time, it reflects only those payments from which personal income tax was withheld.

Income that is not subject to this tax is not included in the certificate. Among them:

- severance pay upon dismissal (but not more than 3 times monthly earnings);

- state benefits for pregnancy, childbirth, child support;

- compensation for harm caused;

- a number of others (according to the Tax Code of the Russian Federation, Article 217, paragraph 1).

2-NDFL certificates are signed by the manager or other authorized representative of the employer and issued to the applicant immediately upon dismissal or no later than 3 days from the date of application.

conclusions

Having officially terminated the employment relationship, the employee has the right to receive a settlement (payments), a work book and additional documentation related to the work. All this must be provided to the retiring citizen by his employer.

Some papers are issued to the departing employee without fail (by default), and some certificates are provided upon written request within 3 days.

One way or another, the employer cannot refuse the employee to satisfy his legal requirement. If a request is not fulfilled in a timely manner, the employee has the right to complain.

When to submit 2-NDFL for a fired person to the tax office?

A certificate of income of a dismissed employee is submitted to the tax office along with other certificates issued at the end of the year.

A certificate submitted to the Federal Tax Service about a dismissed employee must have the same number that was assigned to it when issued to the employee on the last working day. The date is also saved.

Deadline for submitting certificates to the tax office:

- 01.04 next year - for all employee income;

- 01.03 next year - for income for which no deduction was made.

Obligation of the employer to issue documents to the employee

Issuing a certificate upon dismissal is not the right, but the obligation of the employer without reminders from the individual. persons about this need. If the certificate is not issued on time, this is done after the employee applies in a short time. This norm is enshrined in Article 62 of the Labor Code.

Upon dismissal of an individual The employer provides a certificate only upon oral request from the employee, who clarifies for what period he needs the calculation. However, if it is provided on time, it is better to support the request with an application for extradition.

The company acts as a tax agent who makes monthly payments to individuals. persons - employees of the organization for the payment of earnings, in addition, accrue, withhold and transfer personal income tax to the treasury.

What income code is used in 2nd personal income tax when renting a car?

In practice, situations are not uncommon when, upon dismissal, the 2nd personal income tax report from the last place is not issued on time due to the formation of a debt to the employee, as well as when errors are discovered in the company’s accounting.

After a written application from the employee, the 2nd personal income tax report is issued no later than three days, only if, if this deadline is violated, the individual. the person will contact the labor inspectorate.

The number of report copies is not regulated. If necessary, after dismissal, the employee makes a written request to the head of the company to issue several forms, and he does not have the right to refuse.

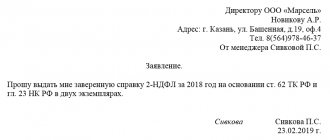

How to make an application to receive personal income tax certificate 2

Example of registration of 2-NDFL upon dismissal

At the top of the form, fill out the introductory title part, which contains the following information sequentially:

- The year for which the paper is being prepared - in the example under consideration, this is the year the employee was dismissed;

- Certificate number and day of issue - these details are stored on the copy of 2-NDFL that will be transferred to the tax office next year;

- Sign – takes one value: “1” – if filling is made in relation to an individual who received income from which personal income tax was withheld; “2” – if tax is not withheld in full from a certain part of the employee’s income;

- Correction number - the serial number of making corrections to the current form is entered with a number; if 2-NDFL is generated for the first time, then “00” is entered in the field;

- Tax code where the certificate will be submitted at the end of the current year.

If the employee received income in the current year from which tax was not withheld, then 2-NDFL with sign “2” is filled in for such payments, as well as 2-NDFL with sign “1” for taxable income. That is, for one person in such a situation, 2 certificates will be issued with different meanings in the “sign” field.

Registration of sections 2-NDFL

| Field or section name | Information to be filled in | |

| Section 1 | Details of the employer organization making payments. The employer acts as a tax agent for the worker, withholding tax from his income and transferring it to the budget. If payments were made by a separate division, then the details of this division must be indicated. Details include:

| |

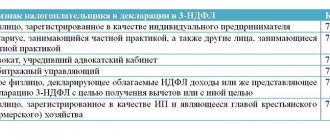

| Section 2 | TIN | The section provides the details of the dismissed employee in respect of whom the certificate is being drawn up. If the individual is a foreign citizen, then it is necessary to indicate the taxpayer code not only in the Russian Federation, but also in the state of which the employee has citizenship. |

| Full name | Taken from the passport. If there is no middle name, the field is not filled in. | |

| Status | A digital code that determines the status of an individual. Taken from section 4 of the Procedure for filling out 2-NDFL. Tax residents (that is, persons who have been in the Russian Federation for at least 183 days over the last year) indicate code “1”. | |

| Citizenship | Indicated as the code of the country of which the individual is a citizen. This code can be viewed in OKSM. For Russian citizens, 643 are paid. | |

| Document code | The digital code of the document that confirms the employee’s identity. For Russian citizens, such a document is a passport, for which it is marked “21”. | |

| Address | Fill in the elements of the address where the dismissed employee lives. | |

| Section 3 | Bid | The tax rate at which income is taxed. If several such rates were used, then fill out one 2-NDFL certificate, which will include as many sections 3-5 as the rates were used. The standard rate applied to salaries is 13%. Rates of 15, 30 or 35% may also apply. |

| Income | Details are given by month; if in any month of the current year income was not paid, then 0 is entered. Months are indicated by numbers in chronological order, starting with “1” and ending with the month of registration of dismissal. For each type of income paid in a particular month, the corresponding code is indicated. Codes approved by Order of the Federal Tax Service MMV-7-11/ [email protected] from 10.09.15. For each month, the income that was actually received by the employee in that month is shown. In particular, the salary is considered to be actually received on the last day of the month for which it was accrued. Vacation compensation paid upon dismissal is included in taxable income. For salaries, code 2000 is indicated; for compensation upon dismissal, code 4800. | |

| Deductions | Deductions are provided for each type of income. This includes professional deductions, as well as amounts not subject to income tax under Article 217. There is no need to show standard, social and property deductions in the 3rd section; a separate 4th section is devoted to them. For each deduction taken into account as part of income, it is necessary to indicate the corresponding code, which is also taken from Order MMV-7-11/ [email protected] | |

| Section 4 | The required deductions of standard, social and property types are shown. They are provided only to residents of the Russian Federation in relation to income taxed at a rate of 13%. For all other persons, as well as income taxed at other rates, zeros are entered in the lines of this section. For each deduction, the amount and the corresponding code designation are indicated. If an employee is entitled to a social or property benefit, then it is necessary to indicate the details of the tax notice confirming the right to this type of deduction. The employee must provide the notice to the employer along with an application for the specified type of deduction. | |

| Section 5 | Total income | Taken from section 3 at the time of preparation of the certificate from the beginning of the year. |

| The tax base | Determined taking into account the total amount of income and required deductions. | |

| Tax calculated | The rate specified in the 3rd section is multiplied by the base from the 5th section. | |

| Tax withheld | A tax that has been subtracted from the amount of income to be paid. | |

| Tax transferred | Actually transferred to the personal income tax budget. | |

| Tax not withheld | The amount is shown if tax is not withheld by the employer on part of the income. | |

If severance pay is paid upon dismissal, it is not necessary to show it in the income section, since it is not subject to taxation within the limits of three monthly earnings.

If the employer’s internal local documentation provides for an increased amount of severance pay, then in part of the excess over the amount established by law, personal income tax should be withheld and the amount of the excess should be shown in the 3rd section of the certificate.