When is tax time

In any organization, certain dates are assigned each month when employees receive salaries. Usually, money is given to employees on the following dates - the 5th or 10th.

The Tax Code of the Russian Federation establishes the deadline for transferring income tax to the budget. Thus, personal income tax from wages, in accordance with current regulations, must be received by the treasury no later than the next day after the payment of remuneration for labor. This period is set quite clearly and does not depend on the method of payment of salaries. The following situations are possible:

- The organization transfers the salaries of its employees to bank cards. This means that personal income tax must be paid no later than the next day. The same procedure is relevant in the case of issuing money in person after first withdrawing it from a bank account.

- Salaries are paid from the cash register (daily earnings). The tax must be transferred to the treasury before the end of the next day.

These rules are enshrined in paragraph 6 of Article 226 of the Tax Code of the Russian Federation. They are valid from 2021.

An enterprise accountant may have a question: when to pay personal income tax when dismissing an employee in 2021? After all, the previous rules do not apply if an employee leaves the company on a day other than the day the remuneration is issued. What to do in this case?

EXAMPLE

All employees receive their salary on the 5th of every month. One of the employees left the company on May 29.

When should he be paid? What about personal income tax upon dismissal in this case? Will the employee have to wait until June 5 or will the money be paid earlier? To resolve these issues, you must be guided by the letter of the Ministry of Finance No. 03-04-06/4831 dated February 21, 2013. More on this later.

Payment of personal income tax upon dismissal in 2021

Not a day without instructions × Not a day without instructions 2021 did not make any significant changes to the transfer of personal income tax upon dismissal of an employee. However, it is necessary to remember some important nuances.

June 21, 2021 Author: Batsezheva Zarema Termination of labor relations between an employee and an employer can be initiated on the grounds provided for in Art. 77 Labor Code of the Russian Federation. In this article, we will consider possible types of mutual settlements with an employee upon dismissal and the features of transferring personal income tax (hereinafter referred to as tax). When making payments to an employee in connection with the end of an employment relationship, pay attention to a number of features:

- use of vacation in advance.

- the availability of vacation days and the employee’s choice of compensation for unused days;

- the availability of vacation days and the provision of vacation to an employee with the subsequent termination of an employment contract with him;

General rule

In 2021, the situation with personal income tax deductions is as follows. Based on Article 226 of the Tax Code of the Russian Federation, the employer is obliged to transfer personal income tax upon dismissal no later than the day following the payment of wages. At the same time, they do not take into account the methods used by the employer to transfer wages to employees. Even in the case of a non-cash transfer to a plastic card, the period is the same.

We also invite you to read the article: “Dismissal “without working two weeks”: possible or not.”

RULE

In 2021, transfer personal income tax from payments upon dismissal no later than the next day after payment to the employee (clause 6 of article 226 of the Tax Code of the Russian Federation).

Let's sum it up

Salaries, some types of severance pay, as well as compensation upon dismissal are subject to personal income tax in the general manner. Tax deductions are applied in accordance with the Tax Code of the Russian Federation. There are no exceptions for dismissal payments.

The deadline for paying personal income tax upon dismissal is the day following the day of transfer of final settlement payments, that is, the day following the date of termination of the employment agreement. If this date falls on a weekend or holiday, then complete the calculation on the first working day (clauses 6-7 of Article 6.1 of the Tax Code of the Russian Federation).

This is important to know: How to fire an external part-time worker at the initiative of the employer

When should a fired person be paid?

If an employee has expressed a desire to leave the organization and has written a corresponding statement addressed to the manager, then all due amounts must be paid to him on the day of dismissal. In particular, this applies to:

- remuneration for the number of days worked;

- bonus payments;

- debts to the employee.

The salary issued on the day of dismissal must consist of all amounts due to the employee. That is, the organization must pay the employee in full and have no debts to him. This rule is enshrined in the Labor Code of the Russian Federation (Article 140).

Failure to comply with this procedure for making the final salary payment in the event of an employee's departure may result in liability for the employer. Among other things, delays in wages can even result in criminal punishment for the company’s management.

If the employee did not come to the employer on the day of dismissal to receive the payments due and his work book, then he will have to be paid a salary later. This must be done on the day the employee reports.

The Labor Code also establishes the possibility of making the payment of the last salary not on the day the employee arrives, but on the next day after that. You can push back the deadlines if the accountant needs to recalculate the amounts due (for example, if an employee gets sick, the final payment amount changes, since it is calculated taking into account the number of sick days). An additional day in this case will allow the calculations to be made in a new way, after which the money will be issued to the resigning employee.

Everything is now clear regarding payment of wages in the event of dismissal. But how is personal income tax paid upon dismissal in 2021 on a day that does not coincide with the salary?

For more information about this, see the article: “What are the deadlines for paying salaries upon dismissal.”

Payment of personal income tax by individual entrepreneurs for 2021

Author: Danchenko S.P. , expert of the information and reference system "Ayudar Info"

Question:

Expert opinion

Lebedev Sergey Fedorovich

Practitioner lawyer with 7 years of experience. Specialization: civil law. Extensive experience in defense in court.

Is an individual entrepreneur applying the general taxation regime required to submit Form 4-NDFL in 2021?

Answer:

The procedure for calculating and paying personal income tax by individual entrepreneurs applying the general taxation regime is established by Art. 227 Tax Code of the Russian Federation.

For many years, the norm provided for in paragraph 7 of Art. 227 of the Tax Code of the Russian Federation, according to which, if during the year individual entrepreneurs received income from business activities or from private practice, taxpayers were required to submit a tax return reflecting the amount of expected income from this activity in the current tax period in the tax period authority within five days after the expiration of a month from the date of occurrence of such income. In this case, the amount of estimated income was determined by the taxpayer.

The tax return form on the estimated income of an individual (form 4-NDFL) was approved by Order of the Federal Tax Service of Russia dated December 27, 2010 No. ММВ-7-3/ [email protected]

Thus, the above norms of the Tax Code of the Russian Federation directly established the right of the taxpayer to independently determine the amount of expected income for calculating advance payments for personal income tax. At the same time, the taxpayer had the right to determine the amount of estimated income in the amount of estimated income from business activities, taking into account the estimated expenses for conducting activities (which are a professional deduction for personal income tax).

According to paragraph 8 of Art. 227 of the Tax Code of the Russian Federation, the calculation of the amount of advance payments was made by the tax authority on the basis of the amount of estimated income reflected in the tax return in Form 4-NDFL, or the amount of income actually received from these types of activities for the previous tax period, taking into account tax deductions provided for in Art. 218 and 221 of the Tax Code of the Russian Federation.

This was the case back in 2021.

On 01/01/2020, the changes introduced by Federal Law dated 04/15/2019 No. 63-FZ in clauses 7 and 8 of Art. came into force. 227 of the Tax Code of the Russian Federation: individual entrepreneurs based on the results of the first quarter, half a year, nine months calculate the amount of advance payments based on the tax rate, actual income received, professional and standard tax deductions, as well as taking into account previously calculated amounts of advance payments.

This means the following:

1) there is no longer a need to submit a tax return in form 4-NDFL;

2) now the amount of advance payments is calculated not by the tax authorities, but by the individual entrepreneur himself;

3) the amount of advance payments for personal income tax must be calculated quarterly - based on the results of the first quarter, half a year, nine months;

4) when calculating advance payments, you can take into account professional and standard tax deductions for personal income tax, as well as the amount of advance payments;

5) advance payments for personal income tax should be calculated not from estimated income, but from actual income.

Since the concept of “estimated income” was not defined in the Tax Code of the Russian Federation, this allowed individual entrepreneurs to underestimate the amount of the advance payment for personal income tax. Now this will not be possible, since the amount of advance payments for personal income tax must be calculated from the actual income received.

This is important to know: Can a child be fired if a child is disabled?

It can be assumed that the corresponding changes will be made to the tax return in form 3-NDFL, in which individual entrepreneurs will indicate all the necessary data for calculating advance payments. Based on this information, tax authorities will charge penalties in case of underpayment of advance payments.

Please note that in the current tax return in Form 3-NDFL, individual entrepreneurs indicate only the amount of advance payments actually paid (based on payment documents) on line 070 of Appendix 3 of the declaration. When calculating personal income tax for 2021, individual entrepreneurs will need to indicate the accrued amounts of advance payments somewhere in the 3-NDFL form, which will require changes to the 3-NDFL form.

Question:

In what order should an individual entrepreneur make advance payments for personal income tax in 2021?

Answer:

The usual procedure for paying personal income tax for individual entrepreneurs in 2021 was as follows (clauses 9 and 10 of Article 227 of the Tax Code of the Russian Federation).

Advance payments were paid by the taxpayer on the basis of tax notices:

for January – June – no later than July 15 of the current year in the amount of 1/2 of the annual amount of advance payments;

for July - September - no later than October 15 of the current year in the amount of 1/4 of the annual amount of advance payments;

for October - December - no later than January 15 of the following year in the amount of 1/4 of the annual amount of advance payments.

In addition, in the event of a significant (more than 50%) increase or decrease in income during the tax period, the taxpayer was required to submit a new tax return in Form 4-NDFL indicating the amount of estimated income from activities for the current year. In this case, the tax authority recalculated the amounts of advance payments for the current year based on unfulfilled payment deadlines. The recalculation of advance payment amounts was carried out by the tax authority no later than five days from the date of receipt of the new tax return.

From January 1, 2021, Federal Law dated April 15, 2019 No. 63-FZ, clauses 9 and 10 of Art. 227 of the Tax Code of the Russian Federation were declared invalid, and clause 8 of Art. 227 of the Tax Code of the Russian Federation is presented in a new edition, according to which advance payments based on the results of the first quarter, half year, nine months are paid no later than the 25th day of the first month following, respectively, the first quarter, half year, nine months of the tax period.

Thus, from 2021, the procedure for paying personal income tax by individual entrepreneurs will change dramatically:

the tax authorities do not issue any notices, the individual entrepreneur himself calculates the amount of the advance payment (see above);

The deadlines for paying personal income tax have changed.

Taking into account the amendments made, in 2021 individual entrepreneurs must pay personal income tax on time (including postponements) no later than:

01/15/2020 – last advance payment for 2021;

04/27/2020 – advance payment for the first quarter of 2021;

07/15/2020 – annual payment for 2021;

07/27/2020 – advance payment for the first half of 2021;

10/26/2020 – advance payment for nine months of 2021.

Since the deadline for payment of personal income tax established by clause 4 of Art. 228 of the Tax Code of the Russian Federation has not changed, the tax for 2021 will need to be paid no later than July 15 of the year following the expired tax period, that is, no later than 07/15/2021.

When to transfer taxes from a fired person?

In the absence of force majeure circumstances, the employee receives his salary on the day of his dismissal. If he came for the work book later than the established deadline, then the salary is paid no later than the next day. But what should an accountant do with taxes? When does he need to deduct personal income tax when dismissing any of his employees in 2021?

To understand this situation, you need to carefully study the mentioned letter from the Russian Ministry of Finance. It provides key clarifications regarding timing.

Difficulties arise from the fact that employees most often quit without working for a month. In this case, the employer must pay income on the day of dismissal, which is enshrined in paragraph 2 of Article 223 of the Tax Code of the Russian Federation. But personal income tax on dismissal payments by agreement of the parties (and any other reasons) should be transferred maximum the next day after the day the last salary was issued. This is also the last day of work.

Payment of personal income tax upon dismissal: deadlines and procedure for filling out reports

The employer is required to submit two reports to the Federal Tax Service regarding income paid to individuals and withheld income tax:

- 2-NDFL certificates: submitted once a year no later than April 1 of the year following the reporting year;

- Form 6-NDFL: submitted quarterly no later than the last day of the month following the reporting quarters, and at the end of the year - no later than April 1 of the following year.

The reports include only those payments to the resigning employee that are taxable.

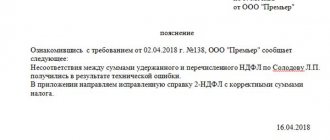

In the 2-NDFL certificate, income is reflected monthly, indicating the codes established by Order of the Federal Tax Service dated September 10, 2015 No. ММВ-7-11/ [email protected] . Until 01/01/2018, all amounts paid in the final settlement were reflected using one code 2000. Any compensation upon dismissal was also reflected under it; The personal income tax code 2021 for these payments has new meanings introduced by the Order of the Federal Tax Service dated October 24, 2017 No. ММВ-7-11/ [email protected] :

- 2013 - compensation for unused vacation,

- 2014 - taxable amount of severance pay exceeding three months' earnings.

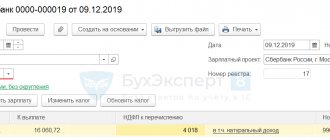

In 6-NDFL, payments of the final settlement, tax amounts calculated and withheld from it should be reflected in the quarter of dismissal. There is a peculiarity if the tax payment date falls on the next quarter. For example, an employee quit and received the final payment on June 30, then the tax must be transferred no later than July 1. In this case, the accrued final calculation and the withheld amount of personal income tax in section 1 of the report will be reflected in the second quarter. Payments must be reflected in section 2 of the report in the third quarter. Such clarifications are given by the Ministry of Finance in Letter dated November 2, 2016 No. BS-4-11/ [email protected]

Transfer deadlines

In order not to violate the law and transfer personal income tax to the budget on time, you need to be guided by the deadlines shown in the table:

| The procedure for issuing salaries | On what day should personal income tax be transferred? |

| To an employee’s bank plastic card (according to the salary project) | At the same time when the salary is transferred to the card or the next day |

| In hand cash, previously withdrawn from the organization’s bank account | At the same time when funds are withdrawn from the account or on the next day |

| In hand from the cash register or from the proceeds received during the day | At the time of payment or the next day |

The letter from the Ministry of Finance explains that the established deadlines for transferring taxes to the treasury apply not only to the wages themselves, but also to all other money due to the employee.

It turns out that along with the salary tax, personal income tax must be deducted from benefits and compensation for unspent vacation. If such payments are made simultaneously, the tax from them must also be transferred to the budget together.

Read also

26.04.2018