Income code in 3-NDFL: decoding

The code for the type of income in 3-NDFL (approved by Order of the Federal Tax Service of Russia dated October 3, 2018 N ММВ-7-11/) is reflected in line 020 of Appendix 1 “Income from sources in the Russian Federation”. The specified two-digit code for the type of income in the 3-NDFL declaration has one of the following meanings:

| Type of income | Code of type of income in 3-NDFL |

| Income from the sale of real estate and shares in it, determined based on the price of the object specified in the agreement on the alienation of property | 01 |

| Income from the sale of real estate and shares in it, determined based on the cadastral value of this object, multiplied by a reduction factor of 0.7 | 02 |

| Income from the sale of other property | 03 |

| Income from transactions with securities | 04 |

| Income from property rental (hire) | 05 |

| Income in cash and in kind received as a gift | 06 |

| Income received on the basis of an employment contract or civil law contract (CLA), from which personal income tax was withheld by the tax agent | 07 |

| Income received on the basis of an employment contract or a civil law contract (CLA), from which personal income tax was not withheld by the tax agent, including partially | 08 |

| Income from equity participation in the activities of organizations (dividends) | 09 |

| Other income | 10 |

Taxpayer identification in the 3-NDFL declaration

The adjustment code for the 3-NDFL declaration means which declaration is submitted to the tax office for the reporting period. The first document is marked “000”, if the declaration is submitted again – “001”, the second corrected version must be numbered “002” and so on. The number is indicated in the appropriate field on the title page.

Also, on the title page of the declaration form, the applicant for a personal income tax refund is required to indicate the adjustment number. This is the very first cell, consisting of three cells, immediately after the document title, which is indicated in bold.

https://www..com/watch?v=aePEQXr-dSc

The adjustment number exists so that tax agents can immediately see what type of return it is, filed by the same individual during the tax period indicated in it.

How to indicate the number

This number usually consists of one digit. First of all, write down the required number, and then put two dashes. You must fill out the cell in which you want to enter the adjustment number as follows:

- 0 – if taxpayers submit a declaration for verification for the first time in the year specified in the document as the tax period;

- 1 – if an individual sends the document for consideration again. This often happens if errors were made when filling out the previous form, and the tax inspector demanded that they be corrected;

- 2 – if the applicant for an income tax refund reissues or simply submits Form 3-NDFL for verification for the third time in a year. This happens when one individual has the right to several deductions at the same time and decides to receive them during one tax period. For example, this could be the registration of compensation for training, for medical services and for the purchase of property.

Code of the country

In the “Country code” field, indicate the code of the state of which the person submitting the declaration is a citizen.

Determine the code yourself using the All-Russian Classifier of Countries of the World (OKSM), approved by Gosstandart Decree of December 14, 2001 529-ST. For Russian citizens, enter the code “643”.

If the person does not have citizenship, indicate the code of the country that issued the identity document.

https://www.youtube.com/watch?v=aePEQXr-dSc

Taxpayer category code

In the “Taxpayer Category Code” field, enter the code in accordance with Appendix No. 1 to the Procedure approved by Order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671. For an individual entrepreneur, enter “720” in this field, for individuals – “760”. Separate codes are provided for notaries, lawyers and heads of peasant (farm) households.

FULL NAME. and personal data

Please indicate your last name, first name and patronymic in full, without abbreviations, as in your passport. Writing in Latin letters is allowed only for foreigners (subclause 6, clause 3.2 of the Procedure approved by order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671).

At the top of each page you fill out, indicate your Taxpayer Identification Number, as well as your last name and initials. The TIN must be filled out if the declaration is submitted by an entrepreneur. Individuals may not fill out this field, in which case they will have to provide passport data (clause 1.10 and subclause 7 of clause 3.2 of the Procedure approved by order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671).

Taxpayer status

In this field you must indicate whether the citizen is a resident or non-resident of the Russian Federation.

If a citizen has been in Russia for more than 183 calendar days over the past 12 months, then he is a resident. In this case, indicate the number 1. If less, enter the number 2. Read the article on how to find out whether an individual is a resident or a non-resident.

Residence

In the “Place of residence of the taxpayer” field, enter the number 1 if you have a residence permit in Russia. If there is no registration, but there is registration at the place of residence, indicate the number 2.

Indicate the postcode, district, city, town, street, house, building and apartment number based on the entry in your passport or certificate of registration of residence. If you do not have a place of residence, please indicate your registered address at your place of residence. Take it from your residence registration certificate.

In the "Region" field, enter the region code. It can be determined using Appendix 3 to the Procedure approved by Order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671.

Such rules are established by subclause 9 of clause 3.2 of the Procedure approved by order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671.

The field “Residence address outside the territory of the Russian Federation” is filled in only by non-residents.

The country of citizenship of the person filing the declaration is indicated in code form on the title page. The list is contained in the All-Russian Classifier of Countries of the World. The most popular country code for the 3-NDFL tax return is “643” - Russian Federation.

Tax authority number

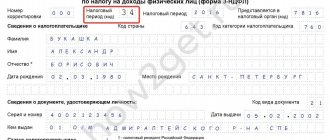

In 3-NDFL, the tax period (code) is the period of time for which you are reporting. Each time period is indicated by a digital value, depending on the period for which the declaration is submitted and indicated on the title page.

| 21 | First quarter |

| 31 | Half year |

| 33 | Nine month |

| 34 | Year |

In the “Submitted to the tax authority” field, enter the 4-digit number of the inspectorate to which the reporting is submitted. The first two digits are the region number, and the last two are the inspection code. You can find out the tax service branch number on the website of the Federal Tax Service.

Contact phone number

Write your contact phone number in full, including the city code. This can be either a landline or a mobile number. The telephone number should not contain spaces or dashes, but you can use brackets and a sign to indicate the code (subclause 11, clause 3.2 of the Procedure approved by order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671).

Sheet A

Start filling out the total indicators from sheet A, which indicates income received from sources in Russia. At the same time, do not indicate income from entrepreneurial and legal activities, as well as from private practice, on sheet A; such income is reflected on sheet B.

Fill out the indicators on sheet A separately for each source of income payment and for each tax rate. For income under an employment or civil contract, take it from the certificate in form 2-NDFL.

On line 010, indicate the tax rate at which the income was taxed.

On line 020, indicate the code of the type of income. These codes are given in Appendix 4 to the Procedure approved by Order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671. For example, for income under an employment contract (in other words, wages), enter the code “06”.

On line 030, indicate the TIN of the organization that paid the income. When receiving income from an entrepreneur, enter his TIN.

On line 040, indicate the checkpoint of the organization that paid the income. If you receive income from an entrepreneur, put dashes.

On line 050, indicate OKTMO of the organization from which the income was received.

On line 060, indicate the name of the organization that paid the income. If you received income from an individual, then enter his last name, first name, patronymic and Taxpayer Identification Number (if any).

On line 070, reflect the amount of income received in the year for which you are filling out the declaration.

On line 080, indicate the amount of income on which you need to pay tax (tax base).

On line 090, reflect the amount of calculated tax. You will get it by multiplying the tax base (line 080) by the tax rate indicated above in line 010.

If all sources of income do not fit on one page, then fill out as many sheets A as you need (clause 6.2 of the Procedure approved by Order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671).

Sheet B

On Sheet B, reflect income received from sources outside of Russia. Only citizens who are tax residents of Russia need to fill out this sheet.

If you received income that is taxed at different rates, then fill out several sheets B. That is, on one sheet indicate income that is taxed at the same rate.

If all sources of income payment that are taxed at the same rate do not fit on one page, then fill out as many sheets B as you need. In this case, reflect the final results only on the last page.

On line 010, indicate the digital code of the country from which the income was received, according to OKSM.

On line 020, indicate the name of the organization that paid the income. When filling out this line, you can use letters of the Latin alphabet.

On line 030, indicate the currency code according to the All-Russian Currency Classifier.

On line 031, indicate the type of income code:

- 1 - profit of a controlled foreign company;

On line 040, indicate the date of receipt of income. Enter the date in numbers: day, month, year in the format DDMMYYYY.

On line 050, indicate the foreign currency exchange rate to the ruble established by the Bank of Russia on the date of receipt of income.

On line 060, indicate the amount of income in foreign currency.

On line 070, indicate the amount of income converted to rubles.

On line 080, indicate the tax payment date.

On line 090, indicate the foreign currency to ruble exchange rate established by the Bank of Russia on the date of tax payment.

On line 100, indicate the amount of tax paid in a foreign country in foreign currency. The basis is a document confirming income received and payment of tax outside Russia.

On line 110, indicate the amount of tax paid in a foreign country, converted to rubles.

On line 120, indicate the amount of tax calculated in Russia at the appropriate rate.

On line 130, indicate the amount of tax to be credited in Russia. It is equal to the indicator of line 110, but cannot exceed the tax amount:

- reflected on line 120.

Such rules are established in Chapter VII of the Procedure, approved by order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671.

An example of filing a declaration in form 3-NDFL when receiving dividends from sources outside of Russia

A.S. Kondratiev (resident) on October 15, 2015 received dividends in the amount of $625 from a foreign organization HOLDING LIMITED, which is located in the United States.

When paying dividends, the foreign organization simultaneously withheld tax on them at a rate of 10 percent in accordance with the Treaty between the Russian Federation and the United States of America for the avoidance of double taxation and the prevention of tax evasion with respect to taxes on income and capital of June 17, 1992.

The Bank of Russia exchange rate for the US dollar on the date of payment of dividends and taxes was 40.5304 rubles/USD (conditionally).

In Russia in 2015, such income was subject to personal income tax at a rate of 9 percent (clause 4 of article 224 of the Tax Code of the Russian Federation). No later than April 30, 2021, Kondratyev must submit a declaration in form 3-NDFL to the tax office of his place of residence (subclause 3, clause 1, article 228, clause 1, article 229 of the Tax Code of the Russian Federation).

The organization where Kondratiev works withheld the entire amount of personal income tax from his salary and transferred it to the budget in full. Therefore, he decided not to indicate this income in the form of salary in the declaration. This right is given to him by paragraph 4 of Article 229 of the Tax Code of the Russian Federation.

Source: https://rfposuda.ru/kody-kategoriy-nalogoplatelshchika-3-ndfl-2021-rasshifrovka/

Code of type of income from sources outside the Russian Federation

In addition to taxable income received from sources in Russia, individuals must declare taxable income received from sources located outside the Russian Federation. Such income is reflected in 3-NDFL in Appendix 2 “Income from sources outside the Russian Federation, taxed at the rate of__%”.

The code for the type of income data must be indicated in line 031 of Appendix 2. This code can take the following values:

| Type of income | Code of type of income in 3-NDFL |

| Income in the form of the amount of profit of a controlled foreign company | 21 |

| Dividends | 22 |

| Interest | 23 |

| Royalty | 24 |

| Income from alienation of property | 25 |

| Income from the alienation of shares and similar rights, more than 50% of the value of which is represented by real estate located in another state | 26 |

| Income from the provision of independent personal services (professional services or other activities of an independent nature) | 27 |

| Income from employment (salaries and other similar remuneration) | 28 |

| Directors' fees and other similar payments received as a member of the board of directors or any other governing body of the company | 29 |

| Income from personal activities as a theater, film, radio or television artist, musician or athlete | 30 |

| Income from public service | 31 |

| Other income | 32 |

Read also

03.03.2017

Directory

Appendix No. 1 to the Procedure for filling out the tax return form for personal income tax (form 3-NDFL), approved by order of the Federal Tax Service of December 24, 2014 No. ММВ-7-11/ [email protected]

(as amended by Order of the Federal Tax Service of Russia dated November 25, 2015 N ММВ-7-11/ [email protected] )

Directory “Taxpayer Category Codes”

| 720 | an individual registered as an individual entrepreneur |

| 730 | a notary engaged in private practice, and other persons engaged in private practice in accordance with the procedure established by current legislation |

| 740 | lawyer who established a law office |

| 750 | arbitration manager |

| 760 | another individual declaring income in accordance with Articles 227.1 and 228 of the Code, as well as for the purpose of obtaining tax deductions in accordance with Articles 218-221 of the Code or for another purpose |

| 770 | an individual registered as an individual entrepreneur and who is the head of a peasant (farm) enterprise |

Appendix No. 6 Directory “Codes of persons claiming property tax deductions”

Assistance in filling out tax returns 3-NDFL

Detailed information can be obtained by calling (495) 764-04-31, 210-82-31

Source: https://nalog7.ru/instr2014-17

Taxpayer category code 760

Another code to be filled out in the certificate indicates the category of the individual paying the tax. There are six such categories in total, and every taxpayer filling out 3-NDFL can include himself in them.

The table below shows the characteristics of a taxpayer with their corresponding numeric code:

Related terms

- How to fill out the 3-NDFL declaration - instructions, sample filling

- 3 Personal income tax in 2021 - sample of filling out a declaration

- How to submit a 3rd personal income tax return through State Services

- Certificate 2-NDFL - what is it and why is it needed?

- Income codes in personal income tax certificate 2 in 2021

- How to fill out a 2-NDFL certificate - sample and procedure

14:16 23.08.2019

Credit cardCertificatesInstallment plansDepositsLoansCurrent accountMicroloansBanksBenefitsSalariesMortgage

show all