Home — Civil procedural law — How is leased property depreciated after its redemption in 2021

Let's consider the accelerated depreciation formula: AMu = AM*AMC, where AMu denotes the rate of accelerated depreciation AM denotes the rate of depreciation, which is calculated in accordance with the validity period of the contract AMC denotes the accelerated depreciation coefficient, which can vary from 1 to 3 Application of the accelerated depreciation coefficient when leasing a car is also considered a significant advantage of the transaction, which lessees willingly take advantage of. It is also acceptable that this opportunity applies to all categories of clients (legal entities and individuals, as well as entrepreneurs). Some companies on their official websites provide a convenient opportunity to use an online calculator that will help you quickly calculate the amount of payments at different coefficients, as well as estimate the residual value of the upcoming purchase of the vehicle.

Features of depreciation during leasing

Info

Calculation and accrual are carried out by the party on whose balance sheet the car or work equipment is located. The maximum coefficient is 3. If the contract term is from 1 to 5 years, it is considered short-term, which is the reason for imposing a restriction - depreciation is not calculated. When applying the usual coefficient, the depreciation rate must be multiplied by the appropriate indicator.

It is set in the numerical range from one to three, multiplication by a fractional value is allowed, for example, 1.5. Formula for calculation: AMu = AM*KUA The following values are substituted:

- AMu – established rate of depreciation with acceleration;

- AM is the norm, which is calculated based on the total duration of the leasing agreement;

- AMC – coefficient.

Redemption value of leased property (transactions)

In accounting, the initial cost is defined as the sum of all payments under the leasing agreement excluding VAT. But in tax accounting, a completely different rule applies: the initial cost is equal to the amount of the lessor’s expenses for the acquisition of the leased asset <p. .In addition, in tax accounting, leased property is taken into account differently in different periods.1. During the period of validity of the leasing agreement - as a leased item. Expenses for tax accounting purposes include monthly depreciation of the leased asset and the part of the lease payment that exceeds the amount of accrued depreciation. Thus, the residual value of the leased property on the date of its redemption in tax accounting does not matter. You can simply forget about it. After all, everything that you paid to the lessor as current payments, you have already recognized as expenses.2.

Payment of redemption price

Payments for the redemption of leased property should not be included in expenses until the transfer of ownership. They are not subject to the procedure for accounting for leasing payments for the temporary use of property.

Reflect settlements for the redemption of leased property in the debit of account 60 (76) by opening a subaccount for it “Settlements for the redemption of the leased asset.” When payment of the redemption price is provided at the end of the contract, reflect this operation in accounting as follows:

Debit 60 (76) subaccount “Calculations for the redemption of the leased asset” Credit 51 (50...) – the redemption price of the leased asset has been paid.

If you transfer the redemption value during the term of the contract, then apply these amounts to advances. Do this until ownership of the leased asset passes from the lessor to your organization. For convenience, use a separate subaccount “Calculations for advances issued” to account 60 (76):

Debit 60 (76) subaccount “Settlements for advances issued” Credit 51 - an advance is transferred towards the redemption value of property received on lease.

Don't forget to reflect VAT on the advance:

Debit 19 Credit 76 subaccount “Calculations for VAT on advances issued” - VAT paid as part of the advance is taken into account;

Debit 68 subaccount “Calculations for VAT” Credit 19 – submitted for deduction of input VAT upon receipt of an advance invoice.

And at the moment of transfer of ownership, make the following entries:

Debit 60 (76) subaccount “Calculations for the redemption of the leased asset” Debit 60 (76) subaccount “Calculations for advances issued” - the advance is credited to repay the redemption value of the leased asset;

Debit 19 Credit 68 subaccount “Calculations for VAT” – VAT previously claimed for deduction from advances has been restored;

Debit 76 subaccount “Calculations for VAT on advances issued” Credit 19 – the restored amount of VAT is written off.

This procedure follows from the provisions of paragraph 1 of Article 19 of the Law of October 29, 1998 No. 164-FZ, articles 624 and 625 of the Civil Code of the Russian Federation, paragraphs 3, 16 PBU 10/99 and the Instructions for the chart of accounts (accounts 19, 50, 51, 60, 68, 76).

The order in which the transfer of ownership of a leased asset is reflected in accounting depends on whose balance sheet this object was on during the term of the agreement: the lessor or the lessee.

Is it possible to change the depreciation method after purchasing the leased property?

The main benefit is that at the end of the contract the leased asset can be purchased at a minimum cost. Increasing coefficient The increasing coefficient is the value due to which the amount of payments under the contract increases. It should be used in order to shorten the repayment period of the debt under the transaction and redeem the car sooner.

When calculating the coefficient, it should be taken into account that if the car or equipment was registered on the balance sheet of the leasing recipient, then this indicator will correspond to the current tax rate for a specific vehicle. Russian legislation contains an indication that the party to the transaction that is the balance holder has the right to apply a special increasing coefficient of 1-3.

Features of re-registration of a car after leasing payment

Re-registration of a car after leasing is possible if the client has paid its full cost to the leasing company, taking into account the percentage increase in price. In this case, the contract must contain a clause providing for the possibility of purchasing the car after the end of the lease period.

Also read: Financial leasing: types, subject and terms of the contract + essence and leasing scheme using a specific example

If the car is on the balance sheet of a leasing company, then in order to transfer it into the ownership of the borrower it is necessary to draw up a purchase and sale agreement. The agreement usually specifies the minimum residual value of the vehicle at which the borrower can purchase the property. After the transaction is concluded, the lessee becomes the full owner and can re-register the car.

To do this, you must obtain all documents confirming the transfer of ownership. The package of documents will be more extensive than when registering a car after a regular purchase.

Additionally, you will need a transfer act signed by the parties to the transaction and a letter for the traffic police about the re-registration of the car as the property of your company.

Accounting and depreciation of leased property in practice

Important

However, when assessing income tax savings, it should be taken into account that the initial cost of property both when leasing and when purchasing fixed assets directly is the same and the total amount attributed to costs by calculating depreciation of fixed assets will also be the same both with accelerated depreciation and and with the usual scheme for calculating depreciation charges. The only difference is that with the accelerated depreciation method this will happen faster. But at the end of the leasing transaction, if the leased property is completely written off, depreciation on it will no longer be included in expenses, and with the usual depreciation calculation, fixed assets will be depreciated, reducing the income tax base.

When applying the accelerated depreciation method, it is necessary to control the total amount of expenses and the financial result of the company.

Redemption of leased property: acceptance for accounting

Term The period for calculating depreciation on leased property does not exceed the duration of the transaction. Even if the leasing agreement was terminated early, the lessor undertakes to restore depreciation, because the vehicle is on its balance sheet. This is regulated by Federal Law. Such a resolution insures lessees against possible risks and unfair financial fraud of leasing companies. Since groups 1-3 of leased property are not subject to depreciation, the period may exceed a five-year period. Thus, depreciation is especially beneficial for legal entities and private entrepreneurs who have rented special equipment or trucks. Acceleration of depreciation is possible from any period of the leasing agreement, but the important thing is that it is the coefficient that is taken into account.

Depreciation when leasing a car

Increasing the volume of depreciation deductions helps to achieve a reduction in the tax rate on the lessee's profit. But such a privilege can only be used at the time the contract is valid. Thus, the primary price of a car differs slightly from the cost of a vehicle purchased directly.

There will be no special differences with accelerated depreciation. If this method is used, control the financial activities of the enterprise and its expenses. Otherwise, accrued amounts of accelerated depreciation may lead to increased costs and ultimately serious losses.

Another advantage of accelerated depreciation is that at the end of the leasing transaction, the residual value of the vehicle will be more accessible to the buyer, because it will be significantly reduced due to monthly deposits. Moreover, this coefficient has a controlled value and is fixed by agreement. Accelerated depreciation helps reduce the residual value of a leased car and is calculated using a formula that we will discuss below. Financiers explain to their clients the essence of depreciation as follows: it is the acceleration of payments for leasing and redemption of a vehicle through the use of a special coefficient that increases cash contributions. Accelerated depreciation during leasing It is this type of depreciation that is considered by clients to be the most profitable aspect of leasing, which indicates that leasing is a more flexible financial transaction than a car loan.

Re-registration of a car from an individual entrepreneur to an individual

To re-register a leased vehicle from an individual entrepreneur to an individual, you will not need to enter into an additional agreement. In the process of re-registration of a car, income that is subject to taxation does not arise. During the subsequent sale of the car, an individual will not be able to take advantage of the property tax deduction. And transport tax is paid by a private individual, regardless of who the car is registered to.

This procedure is enshrined at the legislative level with some differences and features depending on the region where the transaction is carried out.

How is leased property depreciated after its redemption in 2018?

It is obvious that when using accelerated depreciation of fixed assets, their residual value will decrease much faster than when calculating depreciation using the usual method. In addition, the complete write-off of fixed assets when using accelerated depreciation with a coefficient, for example, 3, is carried out three times faster. All this allows you to significantly reduce the amount and period of payment of property tax when using the accelerated depreciation method. Using the method of accelerated depreciation of fixed assets allows you to reduce the taxable base for income tax by increasing the amount of depreciation deductions for the leased asset. This effect is achieved during the period of validity of the leasing transaction.

Attention

Depending on whether the equipment or vehicle is on the balance sheet of the lessor or the recipient, a coefficient of no more than 3 may be accrued. However, according to tax legislation, its accrual is not allowed for property belonging to depreciation groups 1-3.

- Funds used in scientific and technical activities can also be purchased by the company under a leasing agreement. For them, the maximum indicator is 3.

- An increasing factor (IC) can be applied to equipment used in agricultural activities - in poultry farms, greenhouse plants.

There is no need to make changes in accounting policies if PC is used when calculating depreciation on fixed assets of an enterprise. How to calculate Features of calculating depreciation are described in Russian legislation, namely, in the Federal Law “On Leasing”, as well as in the Tax Code of the Russian Federation.

The equipment will be fully depreciated over the leasing period of 36 months. In this example of calculating accelerated depreciation, you can also take the useful life of the equipment to be equal to, for example, 80 months. In this case, the monthly depreciation rate will be 1.25%, the depreciation rate using an increasing factor of 2.22 - 2.775%.

The equipment will also be completely written off within 36 months. The use of the accelerated depreciation method has its own characteristics and nuances. Our company’s specialists will help you understand the choice of the optimal scheme for using the accelerated depreciation mechanism.

In the Tax Code, Article 256, goods subject to depreciation are recognized as:

- any type of movable property;

- results obtained in the process of mental activity;

- objects that have been recognized as the intellectual property of the lessee.

There is no specific division into categories in depreciation, but when concluding an agreement, the parties must decide among themselves who will register the leased item. This can be done by the end user or the leasing company. Depreciation is an excellent opportunity for an individual entrepreneur to increase his income due to the fact that he is exempt from paying tax on the transaction.

Another obvious advantage is that when purchasing a car on lease, you do not need to take out an insurance policy such as compulsory motor liability insurance, which also allows you not to invest additional funds.

Accounting for leasing when reflecting property on the balance sheet of the lessor or lessee

On the lessor's balance sheet

The most common situation is the reflection of the leased asset on the balance sheet of the leasing company. If the leasing agreement provides for the reflection of the leased asset on the lessor’s balance sheet, the lessee reflects the leased property on off-balance sheet account 001 “Leased fixed assets”.

The accrual of leasing payments is reflected in the credit of account 76 “Settlements with various debtors and creditors” in correspondence with cost accounts: usually account 20.

Postings upon receipt of the leased asset:

Dt 001

— the leased asset is accepted for accounting at cost excluding VAT;

Postings for current lease payments:

Dt 60 - Kt 51

— the advance payment under the leasing agreement has been paid;

Dt 76 - Kt 68

— VAT deduction from the advance payment amount;

The lessee has the right to deduct VAT from the entire advance payment amount at once.

An advance payment under a leasing agreement can be charged to expenses in the first month or over several months (depending on the structure of the payment schedule).

Moreover, if the advance is offset during the entire leasing term or for several months, the lessee is obliged to restore the amount of VAT every month from the advance offset in the current month.

Dt 68 - Kt 76

— VAT has been restored on part of the leasing payment to offset the advance payment.

Dt 20 - Kt 76

— the leasing payment has been accrued for the entire amount, including the advance payment.

Dt 19 - Kt 76

— VAT is charged on the lease payment for the entire amount, including offset of the advance payment.

Dt 68 - Kt 19

— VAT has been submitted to the budget on the amount of the leasing payment.

Dt 76 - Kt 51

— leasing payments are listed.

Postings for the redemption of the leased asset

If there is a buyout price in the leasing agreement (this amount is not included in the leasing payment schedule, for example, let’s take it equal to 1,180 rubles including VAT), the following entries are made in accounting:

Dt 08 - Kt 76

—reflects the costs of repurchasing the leased asset upon transfer of ownership to the lessee (purchase price).

Dt 19 - Kt 76

— VAT is charged on the redemption of the leased asset at the redemption price.

Dt 68 - Kt 19

- submitted VAT to the budget.

Dt 76 - Kt 51

— the amount of redemption of the leased asset has been paid.

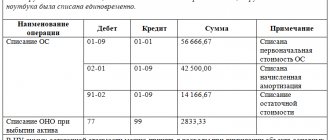

Dt 01 - Kt 08

— the leased asset is accepted for accounting as part of its own fixed assets if the cost of the leased asset upon redemption is more than 40 thousand rubles.

Dt 20 – Kt 08

— the cost of acquiring the leased asset is written off as expenses (when the repurchase is carried out at a conditional or formal price of 1000 or 100 rubles).

On the lessee's balance sheet

The reflection of the leased asset on the lessee's balance sheet has not been fully regulated, and therefore has several accounting methods with their own characteristics.

The disadvantages of some accounting methods are the fact that there is no possibility of accounting for changes in the leasing transaction; the disadvantages of other methods are, for example, the need to customize accounting information systems. However, some accounting methods are still associated with tax risks. Let us highlight the main methodological problems of accounting for leasing operations for the lessee when accounting for property (the leased asset) on its balance sheet.

1) The initial cost of the property on the lessee’s balance sheet differs from the initial cost of the property on the lessor’s balance sheet (the difference is 20-50% depending on the terms of the leasing agreement). This means that the lessee’s property tax will be 20-50% higher than it would be if recorded on the lessor’s balance sheet. 122

2) The initial cost of the lessee's property varies significantly in its value according to accounting and tax records.

3) If the leasing agreement does not specify the useful life of the leased asset and the depreciation method, then they may differ significantly from the lessor, as the main parameters for calculating lease payments, from the lessee, as the actually accepted depreciation conditions under the leasing agreement. This leads to great difficulties in interrupting and terminating the transaction.

4) In accounting, the lessee attributes only depreciation to expenses, usually using the straight-line method of accrual. If the schedule of lease payments is uneven, then an excess of depreciation occurs over lease payments.

5) If the transaction is interrupted, the lessee has difficulties with recording the disposal of property. This applies to both accounting and tax accounting.

6) The tax burden for property tax is significantly higher than when accounting for property on the balance sheet of a leasing company.

If, under the terms of the leasing agreement, the leased property is taken into account on the balance sheet of the lessee, then its value (clause 8 of the Instructions for reflecting transactions under a leasing agreement in accounting, approved by order of the Ministry of Finance of the Russian Federation dated February 17, 1997 No. 15) is reflected in the debit of account 08 “Investments in non-current assets" in correspondence with account 76 "Settlements with various debtors and creditors" without VAT In accordance with the generally accepted accounting methodology, the initial cost of the leased asset includes all amounts that the lessee will pay to the lessor, that is, the initial cost of the fixed asset is equal to the amount of the leased asset payments (clause 8 of PBU 6/01).

The Tax Code of the Russian Federation does not define the procedure for determining by the lessee the initial cost of the leased asset on the balance sheet of the lessee and the leased asset included by him in the depreciable property. The procedure for forming the initial cost of the leased asset, defined in paragraph 1 of Art. 257 of the Tax Code of the Russian Federation takes into account only the lessor's expenses associated with the acquisition of the leased asset, which implies the formation of the initial cost of the leased asset from the lessor and does not take into account the situation when the leased asset is taken into account on the balance sheet of the lessee. From this rule and the absence of special rules regarding the determination of the initial cost of the leased asset by the lessee at the time the property is accepted on the balance sheet, it follows that the lessee also accepts the leased asset for tax accounting in the amount of the lessor's expenses associated with the acquisition of the leased asset. Thus, for tax accounting purposes, the lessee must have data on the initial cost of the leased asset provided by the lessor. The amount of the lessor's expenses for the acquisition of the leased asset must be confirmed by documents provided by the lessor when transferring the leased asset to the balance of the lessee. Such documents are: Certificate of transfer of property for leasing and Certificate of acceptance and transfer of fixed assets OS-1.

For more detailed information on reflecting the leased asset in accounting, read the attached reference material prepared by the Leasing Territory agency. The book “Accounting for Leasing Operations” covers in detail the issues of organizing primary documentation for both the lessee and the lessor, examines the features of accounting for the leased asset depending on the balance sheet holder, and reveals the differences between accounting for leasing under RAS and IFRS.