The concept of leasing appeared in our country relatively recently. This is a kind of form of lending to an enterprise when it purchases fixed assets. Leasing objects can be: equipment, structures, enterprises, transport, etc. In essence, leasing is a long-term lease of property with subsequent acquisition of ownership. Our company provides implementation and maintenance services for 1C software products. If you have any questions about working with the system, contact him, we will be happy to help you.

Depreciation in leasing

Although equipment purchased on lease is not the property of the organization, it still must be registered and depreciated accordingly. Depreciation is calculated using the document “Depreciation and depreciation of fixed assets” in the fixed assets and intangible assets menu. You can also calculate it automatically if you use the “Month Closing” assistant.

Fig. 15 Closing the month

In conclusion, it is important to pay attention to the fact that for leasing transactions there is a difference between accounting and tax accounting, since in the latter leasing expenses are taken into account minus tax depreciation. The 1C 8.3 program will automatically calculate depreciation and leasing expenses, and also reflect the difference between accounting and tax accounting. To do this, in 1C 8.3 it is necessary to correctly draw up the accounting policy of the enterprise.

If, in addition to leasing accounting, you regularly have questions about working with 1C programs, contact our specialists. We will be happy to advise you and also select the optimal tariffs for 1C subscription services, focusing on your individual tasks.

Leasing accounting for the lessee in 1C 8.3

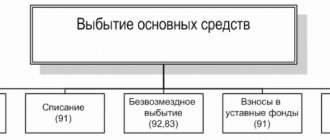

Accounting for leasing in the program is presented in the diagram below. When using the scheme, pay attention to where leased property is taken into account before its redemption.

Let's look at leasing accounting in 1C 8.3 in more detail using an example.

An organization for furniture production leased a membrane-vacuum press from FORTEX LLC for 18 months. The equipment is recorded on the recipient's balance sheet before it is redeemed. The amount of equipment under the contract is RUB 1,267,200. including VAT 20%. It was determined taking into account lease payments of 1,036,800 rubles. and redemption price 230,400 rubles.

July 01, 2021 The membrane-vacuum press was capitalized according to the transfer documents. On the same day the equipment was put into operation.

SPI at the time of transfer of property is 4 years.

The book value of the equipment indicated in the certificate is RUB 816,000.

On January 11, 2021, the equipment was purchased and ownership was transferred.

Payment of leasing payment - posting in 1C 8.3

Calculation of lease payment

When you receive an invoice for a lease payment, enter the document Receipt (act, invoice) . To do this, go to the section Purchases - Receipts (acts, invoices) and select Receipts - Leasing services .

All remaining payments are processed in the same way.

Attention! If the redemption value is reflected as part of the lease payments, but is not allocated as a separate amount, it is not safe to accept it as an expense before purchasing the operating system. Disputes with tax authorities are possible.

Postings

The amount of the lease payment will be reflected only in mutual settlements. In accounting, leasing payments are included in the cost of fixed assets and are repaid by depreciation. In NU - recognized on the last day of the month in the Month Closing .

Acceptance of VAT for deduction on lease payments

Payment for leasing - postings in 1C 8.3

The transfer of leasing payments, including the redemption value, is formalized as a regular payment to the supplier using the document Write-off from the current account .

Attention! If the redemption price is paid together with leasing payments, do not reflect it in expenses, but count it as an advance payment in account 60.02.

Postings

Entry into leasing in 1C 8.3

Capitalization of the leased asset

Enter the document Acceptance of leasing . To do this, go to the section OS and intangible assets .

Fill it out according to the transfer documents. The settlement account and VAT will be set automatically; changing them is not recommended.

In the Total the total amount under the contract should be formed, check it.

By default, subaccounts of account 76.07 “Rent payments” are used.

Postings

Reflection on the balance sheet of equipment accepted for leasing

In the same section, enter the document Acceptance for accounting of fixed assets.

Specify the method of receipt - Under a leasing agreement , then fill in the name of the counterparty and its agreement. By selecting these settings, you will be able to specify the Initial cost of equipment in NU from the lessor’s book value, and leasing payments will be determined automatically for this equipment.

The remaining fields are filled in as standard.

Next, determine whether depreciation is required.

Costs of leasing payments are reflected as part of other (indirect) expenses in NU, so for them select an article whose type of expense Other expenses .

Postings

The difference between the cost in BU and NU will be reflected in Dt 01.K: this is the part of the cost that is not depreciated in NU.

Account Dt 01.K is closed when the costs of leasing payments are recognized. The account will be closed completely upon redemption of the leased property.

Leasing is a nightmare for almost every accountant. Why "almost"? Because they say that the new features of the 1C: Accounting program, ed. 3 allow you to use documents to reflect the following operations: receipts of fixed assets for leasing and its acceptance for accounting, reflection of leasing payments and write-off of VAT on them, subsequent repurchase of this property.

Accounting for property on the lessee's balance sheet is considered the most difficult. In my article I will try to figure out this tricky accounting in the program and perhaps this will be another reason to switch to the 3rd edition of accounting. Let's start with the fact that version 3 of the program added subaccounts 76 to the chart of accounts to account for rental transactions and VAT on them. Already good! This is not in the previous edition, and I suspect that it is unlikely to happen.

So, the first fact of economic activity is the receipt of the leased object, and to reflect this there is a document called “Receipt of leasing” and is located in the section OS and intangible assets:

We create a new document in which we must indicate the full cost of the fixed asset under the contract. The settlement account, accounting account and VAT account are inserted into the document automatically:

By the way, pay attention to the account 08.04.1. Two new subaccounts have appeared in the chart of accounts:

Happy owners of the ITS PROF subscription, having read the description of these subaccounts on the ITS portal, are unlikely to understand anything, just like me. Why? Yes, because it turns out that both accounts are designed to account for the costs of purchasing fixed assets that require installation. Perhaps there was an error in the description of these accounts; the names of the accounts give us hope. But at the same time I had a question: what about the score 07? It seems like it has always been used to reflect the receipt of equipment requiring installation. Anyway. Our task is to consider what the program does and how it does it. If you are not satisfied with the fact that when you selected an item from the “Equipment (fixed assets)” group, the account 08.04.1 was inserted into the document, then you can change the accounting account for the item from this folder. You can read how to do this here I apologize for the lyrical digression from the topic of our conversation. So, we have created the document “Receipt of leasing”. Since we are dealing with leased property, this means that ownership of it does not pass to us and there is no invoice for this transaction. Let's analyze the postings this document makes:

Mmm, what can I say. Everything seems to be correct. The price of the received property is reflected on account 08 and deferred VAT is generated. True, what confuses me in the debit of account 08.04.1 is the empty second subaccount. If you select account 08.04 in the document (the old fashioned way), then all three sub-accounts are filled in in the postings. Something again, some kind of hack. Well, or maybe this is how it should be, but the secret meaning of what is happening is not yet clear to me. Let's continue. The next stage is the commissioning of the leased property. Here we need to use the document “Acceptance for accounting of fixed assets” that has been familiar to us for a long time, but with some clarifications on how to fill it out. So, there is nothing new or unusual in filling out the header of the document, but on the first tab “Non-current asset” you need to correctly select the method of receipt: Under a leasing agreement.

The “Fixed Assets” tab also does not contain anything unexpected. Here we substitute our main means.

Go to the “Accounting” tab. Everything here is familiar, except for the accounting account and the depreciation account. They are entered automatically, depending on the method of receipt on the “Non-current asset” tab:

By the way, this is a happy opportunity to learn about new accounts in the chart of accounts:

Go to the “Tax Accounting” tab. Here it is IMPORTANT to correctly indicate the initial cost of the leased property. For tax accounting purposes, we must indicate the amount of the lessor's expenses.

Let's analyze the entries made by this document:

These are the interesting notes this document made. In accounting account 01.03, the cost of the leased object is reflected in full, and in tax accounting - only the lessor's expenses. The part of the cost of fixed assets that is not depreciable in tax accounting is accounted for in account 01.K. Now let's move on to calculating monthly lease payments. They are accrued in the program using the document “Receipt (Act, Invoice)”, type of operation “Leasing Services”

When generating a document, the program automatically enters settlement accounts and accounting accounts. When making payments in foreign currency or in monetary units. they can be changed to 76.27.2, 76.37.2, 76.27.1 or 76.37.1 respectively. Also, do not forget to register an invoice in this document for deduction of VAT.

As a result, the document made the following entries: the lease payment was accrued, the amount of incoming VAT was reflected and the amount of deferred VAT was written off:

Calculation of depreciation and acceptance of leasing payments to NU are routine operations that are performed automatically at the end of the month:

These routine operations make the following entries: - depreciation amounts are accepted as expenses

— leasing payments are accepted as expenses in NU for the amount of the difference between the receipt of lease payments and depreciation accrued in NU:

You can also generate a calculation certificate recognizing expenses on leased fixed assets:

A certificate can be generated for both accounting and tax accounting. To do this, use the “Show settings” button:

And put the switch in the position we need:

At the end of the contract period, it is necessary to reflect in the program the transfer of ownership of the leased property. To do this, we will use a special document: “Repurchase of the leased asset”

In this document we fill in information about the leased asset and its redemption value:

On the “Accounting” tab, accounts for lease obligations and own fixed assets are automatically entered:

On the “Tax Accounting” tab, we indicate options for including the redemption value as expenses. By default, the “Calculate depreciation” option is always set. When you check the appropriate box, the program automatically calculates the remaining useful life of the OS:

We make several entries in this document: transfers the leased asset to its own fixed assets, transfers accumulated depreciation to account 02.01 and closes the remaining lease obligations and VAT on them, reflects the presented VAT:

Well, that’s actually all that concerns the registration of fixed asset leasing operations in the 1C: Accounting program, ed. 3. I think that this significant advantage of the new version of the program over the previous ones will make you think about switching to it. If you still have any questions, then join our groups on social networks, call our consultation line, ask questions and get answers from our specialists.

| Head of care service Budanova Victoria |

Social buttons for Joomla

Redemption of the leased asset in 1C 8.3

Go to the section Fixed assets and intangible assets, enter the document Redemption of leased items .

Check the purchase price, it will be automatically filled with the balance under the leasing agreement.

The accounting accounts in the accounting system, which already accounts for your own fixed assets and its depreciation, will be filled in automatically; change them if necessary.

In NU, select the need to calculate depreciation if the redemption value is more than 100,000 rubles. Or set up expense recognition analytics if it is less than RUB 100,000.

Check that the SPI is filled out correctly, i.e. with the remaining SPI in NU.

At the bottom of the document form, register the invoice details for the redemption of the leased property and accept the input VAT for deduction.

Postings

Depreciation in accounting for the month of repurchase of fixed assets is accrued in the document Repurchase of leased items . And it continues to accrue further at the end of the month.

Depreciation in NU for the month of repurchase of fixed assets is not accrued. And it begins to be recognized from the next month after the redemption.

Generate the report Balance sheet for account 01.01 and check the initial cost of the accepted fixed asset.

- in the accounting system - the amount under the leasing agreement without VAT, formed upon receipt of the leased property.

- in NU - the redemption value of the OS excluding VAT.

Depreciation calculation

Perform month end closing.

We looked at the leasing accounting scheme in 1C.