Classification and components of the turnover sheet

The elements of accounting are system of accounts and double entry.

Definition 1

A system of accounts is a certain way of grouping economic values that reflect the current state and changes in assets and liabilities, as well as business processes and their results in digital terms.

There are separate accounts for each group of funds and their sources, business processes and results of activities. On a certain account, the initial balance of the object to be accounted for and its subsequent changes determined by business transactions are recorded.

Definition 2

For the operational management of the results of the enterprise’s economic activities, as well as checking the recording of all operations on synthetic and analytical accounts and summarizing data for the reporting period, turnover sheets are drawn up. The turnover sheet is a table that reflects the balance and turnover of accounting accounts. Turnover statements are also called balance sheets . This is due to the fact that they are compiled on the basis of account data on turnover for the period and account balances at the beginning and end of the period.

The balance sheet is compiled on the basis of the journal of business transactions and the initial balance sheet.

The turnover sheet is a table in which a separate line is allocated for each account.

Finished works on a similar topic

- Coursework Turning statements 480 RUR.

- Abstract Turning statements 280 rub.

- Test work Turnover sheets 250 rub.

Receive completed work or specialist advice on your educational project Find out the cost

There are three types of turnover sheets :

- on synthetic accounts, which includes all accounts,

- for analytical accounts, which is maintained separately for each account,

- chess (blind), reflecting exclusively account turnover.

What is a balance sheet

In accounting, all transactions are documented by postings. For example, an accountant will formalize the purchase and payment of materials for 10,000 rubles as follows:

| Dt | CT | Sum | Description |

| 10 "Materials" | 60 “Settlements with suppliers” | 10,000 rub. | Materials purchased from supplier |

| 60 “Settlements with suppliers” | 51 “Current account” | 10,000 rub. | Money for raw materials was transferred to the supplier |

The larger the company, the more entries the accountant creates. Only the purchase of materials can be reflected several times a day. But there are also salary payments, loan payments, equipment purchases, leasing, and so on. If you ask an accountant how much raw materials were purchased, he will not go to look at all the accounting records for Dt10 Kt60, but will immediately open the SALT.

The balance sheet is an accounting register. Turnover accumulates all information on accounts: their balances and turnover for the period. In addition, it can be used to control the correctness and completeness of information reflection.

For example, a good accountant will always create an OCB before drawing up a balance sheet, because he knows the golden rule “debit is always equal to credit.” This means that the debit balance is always equal to the credit balance, also for turnover. If this rule is not followed, then there is an error in the accounting.

One more example. The accountant has generated the turnover and sees an increase in the debit of account 60.02 “Calculations for advances issued.” This means that the company paid money to suppliers, but there was no movement on loan 60.02, which means the counterparty did not ship the goods or provide the service. There are several options for the development of events:

- it is really an advance for future delivery;

- the counterparty shipped the goods a long time ago, which means someone forgot to hand over the documents to the accounting department.

SALT can be compiled for a separate account or for all at once, it depends on the purpose of use. The only drawback of the turnover is that it is difficult to read without knowledge of the chart of accounts and accounting entries. Let's try to imagine one day in the life of a company in the form of OCB.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

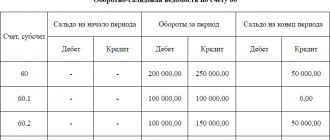

Turnover sheet for synthetic accounts

The turnover sheet for synthetic accounts has the following components (Fig. 1):

- account name;

- opening balance of debit or credit;

- turnover for the month by debit and/or credit;

- balance at the end of the period by debit or credit.

In such a statement, all synthetic accounts that are used in the economic activities of the enterprise are reflected in ascending order.

The total of the turnover sheet for synthetic accounts should be represented by three equalities:

- the balance at the beginning of the reporting period on the debit side of the accounts is equal to the balance on the credit side of the accounts;

- the turnover for the period in the debit of accounts is equal to the turnover in the credit of accounts;

- the debit balance at the end of the reporting period is equal to the credit balance of the accounts.

Three pairs of total columns of the turnover sheet for synthetic accounting accounts contain debit and credit totals equal to each other. This is because the first two columns contain the asset and liability amounts of the balance sheet at the beginning of the month, and the second two include transactions for the period recorded through double entry. The third pair of columns is essentially a new balance.

Need advice from a teacher in this subject area? Ask a question to the teacher and get an answer in 15 minutes! Ask a Question

Note 1

Please note that in the columns “Balance at the beginning of the month” and “Balance at the end of the month” only one amount can always be entered. By debit if the account is active or by credit if the account is passive.

Picture 1.

We can say that the turnover sheet for synthetic accounting accounts is a summary of turnover and balances for all synthetic accounts, which is intended to control accounts, draw up a new balance and allows you to determine the status and changes in funds as a result of economic activity. The equality of the totals of all three pairs of columns of the turnover sheet for synthetic accounts indicates that the double entry method in accounting was applied correctly.

The turnover sheet is the main document when drawing up a balance sheet. The final balance on the debit side of the accounts in the turnover sheet is data for the asset side of the balance sheet, and the final balance on the credit side of the accounts is transferred to the liability side of the balance sheet. The main advantage of the balance sheet is one register for all accounts.

Turnover statements for synthetic and analytical accounts, their construction and purpose.

Home Favorites Random article Educational New additions Feedback FAQ⇐ PreviousPage 5 of 5

Turnover sheets serve to summarize current accounting data.

The turnover sheet for synthetic accounting accounts is a summary of turnover and balances for all synthetic accounts, intended for checking accounts, drawing up a new balance sheet and general familiarization with the status and changes in the assets and liabilities of the organization.

Turnover sheet for synthetic accounts

compiled on the basis of synthetic monthly accounts.

The main feature of a correctly compiled turnover sheet is the presence of three pairs of equalities (equal totals):

The first pair is the equality of the total balances (balances) at the beginning of the month for the debit and credit of accounts. This equality is due to the fact that these balances are indicated in the balance sheet at the beginning of the reporting period: debit balances (balances) on accounts are reflected in assets, and credit balances are reflected in liabilities of the balance sheet (on active accounts the property of the enterprise is reflected according to its functional role, and on passive accounts - also property, but according to the sources of its formation).

The second pair of equalities is the equality of the totals of turnover in the debit and credit of accounts . This equality follows from the use of double entry of business transactions in the accounts (i.e., a business transaction is reflected in the debit of one and the credit of another account in the same amount).

The third pair of totals of the turnover sheet represents the equality of the totals of balances (balances) of the debit and credit accounts at the end of the month , which is due to the equalities of the first and second pairs of totals. These balances represent the balance at the beginning of the next reporting period.

Thus, the turnover sheet is compiled to summarize the data from synthetic accounts and mutually verify the correctness of the entries on them.

Turnover statements for analytical accounting accounts are a method of summarizing analytical accounting data, united by one synthetic account, and are intended to obtain information on the management of an organization and to verify the correctness of accounting records.

of turnover sheets for analytical accounts - turnover sheets for settlement accounts and for accounts for reflecting material assets.

Current statements for analytical accounts have control and operational significance, since according to the data of these statements, control is carried out over balances, receipts and expenditures of material assets, as well as over the state of settlements

.

Considering the issue of determining the final balance on the accounting accounts, we noted that the balance on the active-passive account is displayed after drawing up the turnover sheets for the accounts of settlement relations (the turnover sheet of analytical accounting). It should be noted that the final final balance from the turnover sheet for analytical accounts to the active-passive account is transferred and recorded as the final balance of the active-passive settlement account. After which this remainder is checked.

In order to check the final credit balance on an active-passive account, you should : add the initial credit balance to the amount of the final debit balance, add the credit turnover and subtract the initial debit balance and subtract the debit turnover

.

To check the correctness of the resulting final debit balance, you must : add the initial debit balance to the final credit balance, add the debit turnover and subtract the initial credit balance and subtract the credit turnover.

The chess turnover sheet is a summary of the turnover of the accounts, which serves to disclose their contents and verify the correctness of the correspondence of the accounts

.

In a checkerboard turnover sheet, as in a regular one, the totals of debit turnover for all accounts must be equal to credit turnover for these accounts. The same totals must be obtained after calculating the amounts in the last (total) column and the last (total) line of the statement and recorded once at their intersection.

The positive thing about drawing up a chess turnover sheet is that with their help you can quickly get a clear picture of the progress of the production process in the organization; the visibility of the correspondence of accounts allows you to see all the changes that have occurred in the state of the organization’s property and the sources of its formation. The advantage of the chess recording principle is a one-time reflection of transactions, eliminating duplication and reducing the complexity of the accounting process. But along with the positive aspects, this statement also has a number of disadvantages. So, if, when compiling correspondence of accounts, another account is mistakenly indicated, but which can still participate in correspondence with this account, then this error in it is practically very difficult to detect. It is determined by reconciling account records with data from primary accounting documents, which limits the widespread use of this statement in accounting.

Exemplary buildings for testing

Topic 1. The essence of accounting and its role in the information system and economic management.

1.What stages does business accounting consist of:

2. Economic accounting is...

3.Collecting information on the progress of business processes begins with:

4.Measurers used in accounting:

5.Measurements used to quantify the cost of time and labor for manufacturing products:

6. A general indicator that allows you to combine heterogeneous accounting objects and express them in one meter is the meter:

7. To quantitatively characterize economic processes and means in physical terms, a meter is used:

8. The main regulatory document governing the organization of accounting:

9. Management functions in the organization are implemented using information received in the system:

10.Accounting used to study the quantitative and qualitative aspects of mass socio-economic, demographic phenomena and processes:

11.Management accounting refers to the type of accounting:

12.Tax accounting refers to the type of accounting:

13. Distinctive features that determine the priority of accounting over other types of accounting are:

Topic 2 Subject and method of accounting

14.What sources are borrowed?

15. The debt of the Orsha supply base is characterized by:

16. Debt to the accountable person based on the results of a business trip refers to the following type of debt:

17. The elements of the accounting method include:

18. The set of primary information carriers is called:

19. The method of checking the actual availability of property and liabilities by comparison with accounting data as of a certain date is:

20. The method by which an organization’s property receives monetary value is called:

21. The cost per unit of production is determined using:

22. Which of the following is not an element of accounting method?

23. The assets of the organization are divided into the following groups:

24. Based on their composition and functional role in economic activity, the organization’s assets are divided into groups:

25. The organization’s funds according to the sources of education are divided into:

Topic 3. Balance sheet

26. Based on the balance sheet data, you can analyze:

27.Part of the balance sheet is called:

28. Continue the sentence: “The total assets of the balance sheet are equal to the total liabilities...”

29.The balance sheet asset total should:

30. The asset balance sheet contains the following sections:

31. Intangible assets are reflected in the balance sheet:

32. “Additional capital” - article:

33. The following sections are reflected in the liabilities side of the balance sheet:

34.Operations of the first type of changes in the balance sheet currency:

35. Operation: “Due to a short-term bank loan, the debt to the Orsha supply base for supplied materials was repaid” - refers to the type of balance sheet change:

36.By the method of cleaning, balances are distinguished:

37.By the time of compilation, balances are divided into:

⇐ Previous5

Turnover sheet for analytical accounts

Figure 2.

Turnover statements for analytical accounting accounts represent a summary of turnover and balances for all analytical accounting accounts opened to a specific synthetic account (Fig. 2). To identify technical errors in the accounts, the results of the turnover sheets for analytical accounting accounts are compared with the data of the corresponding synthetic account in the turnover sheet for synthetic accounts. The total amounts of turnover in the analytical accounting accounts must be equal to the total amounts in the synthetic account.

If records of business transactions in analytical accounts were reflected in monetary terms, then the total form of the statement is used. If the records of business transactions on analytical accounting accounts were reflected using natural and monetary or labor and monetary values, then the quantitative-total form of the statement is used.

What does the turnover sheet look like?

Externally, this report looks like a table that consistently displays information on all accounts used, indicating monthly turnover, opening and closing balances. Each account is assigned an independent line, according to the columns of which the distribution of indicators is carried out. Read also the article: → “Form INV-26. Inventory results record sheet: sample.OB consists of the following columns:

- Line sequence number;

- Account number and name;

- Balance at the beginning of the month with distribution by debit and credit;

- Monthly turnover;

- Balance at the end of the month with distribution by debit and credit.

Information to be filled out is taken from the accounts used by the company to reflect the cost indicators of transactions performed. The ending balance indicated in the OB for each account is obtained as a result of the following arithmetic operations:

- For active accounts – Initial balance for Deb. + Monthly turnover according to Deb. – Monthly turnover on Credit, the result obtained must correspond to the final balance of the account;

- For passive accounts – Initial balance for Credit. + Monthly turnover on Credit. – Monthly turnover according to Deb..

Based on the completed OB for the month, general results for each column are summed up. The results obtained allow us to identify errors, as well as establish the place where they were made.

The company's accounting policy establishes the forms of turnover sheets that will be used in the preparation of monthly reports. If desired, it is possible to use chess statements, which show only monthly turnover of accounts without beginning and ending balances. The organization has the right to independently decide on the form of the statement that will be the most convenient and visual. The choice is subject to enshrinement in the company's policy.

Chess turnover sheet

The chess turnover sheet summarizes the data on turnover on the accounts and reveals their content. It serves to check the correctness of invoice correspondence. The chess sheet clearly shows the correspondence of accounts, i.e. it is easy to trace where the values came from and where they were sent. The sum of the debit turnovers of all accounts in the checkerboard turnover sheet is equal to the sum of the credit turnovers, which is achieved through the principle of double entry in the accounts.

Note 2

Today there is no need to fill out balance sheets manually. This process is automated and implemented in accounting software products. But understanding the principle of drawing up a turnover sheet and the ability to analyze the data reflected in it help to quickly respond to management requests and track errors when entering primary data.

Do you need to select material for your study work? Ask a question to the teacher and get an answer in 15 minutes! Ask a Question

Turnover statements of synthetic and analytical accounts

The main way to summarize information in accounting is the turnover sheets. The turnover sheet contains three pairs of equal totals:

1 pair – equality of initial balances, due to the equality of assets and liabilities of the balance sheet;

2 pair – equality of turnover is due to double entry, i.e. each amount is recorded on the accounts twice;

3 pair – the equality of the final balances is due to the first two equalities and the equality of the assets and liabilities of the balance sheet.

The revolving (balance) statement for synthetic accounts is called in practice the revolving balance sheet, because it contains almost all of its indicators.

The turnover sheet for analytical accounts is maintained in quantitative and total terms and has the following form:

| № | Name | Quantity | Price | Opening balance | Revolutions | Final balance | |||

| Quantity | Sum | Quantity | Sum | Quantity | Sum | ||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Total: | X | X | X | X | X | ||||