When it is impossible to conclude a GPC agreement

It is not always illegal to enter into such a contract. Officials provided specific conditions. If the employer violates them, the labor inspectorate will impose a substantial fine. A budgetary institution does not have the right to conclude a PPPC if:

- The position in which the contract worker works is provided for in the staffing table of the government agency.

- The internal labor regulations apply to the mercenary. For example, such an employee works during working hours that are established for core personnel.

- Work is carried out in a specially created workplace. For example, a doctor in a medical facility.

If at least one of the conditions is met, then enter into an employment contract. There are no exceptions. In 2021, taxes and contributions under the GPC agreement will be collected without fail.

What fees should I pay?

Insurance coverage for payments under DHPC is calculated according to the usual rules, but with reservations. The base for insurance premiums when renewing a GPC agreement is determined depending on the type of insurance premium. Here are the contributions employers are required to pay under the GPC:

- Compulsory pension insurance, or compulsory pension insurance, is calculated in full. The tariff for insurance premiums for compulsory health insurance is determined in accordance with the tariff applied by the institution in relation to payments under employment contracts.

- Compulsory health insurance, or compulsory medical insurance, is charged in full at the rate applied by the organization.

- Contributions to pay for temporary disability and in connection with maternity, or VNIM, are not charged. According to paragraphs. 2 p. 3 art. 422 of the Tax Code of the Russian Federation, payments under PGPC are non-taxable in terms of insurance for temporary disability and in connection with maternity.

- Insurance against accidents and occupational diseases, or accidents and illnesses, is accrued only if such an obligation is expressly stated in the terms of a civil contract.

Peculiarities of taxation of fees for compulsory medical insurance and compulsory medical insurance of contract agreements

Sometimes, by agreement between the contractor and the customer, in addition to direct remuneration for labor, payment to the contractor under the GPC is provided for reimbursement of expenses incurred by him related to the fulfillment of obligations. These may be costs for tools, raw materials, materials, and even travel to the place of work - everything that the contract itself provides for; There is no need to pay contributions for these amounts, as stated in paragraphs. 2 clause 1 of article 422 of the Tax Code of the Russian Federation. But personal income tax is still withheld from these amounts.

Moreover, all expenses of this kind must be supported by documents. This is necessary so that when conducting an audit, organizations do not charge additional insurance premiums for these amounts paid in favor of an individual.

Legal documents

- Article 779 of the Civil Code of the Russian Federation

- Article 702 of the Civil Code of the Russian Federation

- Article 1288 of the Civil Code of the Russian Federation

- Article 226 of the Tax Code of the Russian Federation

- Article 420 of the Tax Code of the Russian Federation

- Article 422 of the Tax Code of the Russian Federation

- Federal Law of July 24, 1998 No. 125-FZ

- Article 422 of the Tax Code of the Russian Federation

Calculation example

Payment will be made based on the results of the provision of services. There are no advance payments. There are no contributions for injuries under the terms of the agreement.

The institution pays insurance coverage at generally established rates.

Let's calculate what fees and taxes for civil partnership with an individual the organization will have to pay:

Contributions such as VNiM, NS and PZ are not charged.

The article is devoted to taxes and contributions under the GPC agreement in 2021. It describes in detail what exactly needs to be paid, in what volume, and who exactly should do it.

If you need a specific specialist to do a certain job for you, you can hire him. And for this it is not always necessary to conclude an employment contract. In some cases, a civil law agreement will be optimal. It is also called a GPC agreement.

This agreement differs from an employment agreement in that the parties to it are not the employer and the employee. It is regulated by the Civil Code of the Russian Federation (Article 420), and not by the Labor Code of the Russian Federation. The essence of the contract comes down to the performance by one person of a second volume of work or the provision of specific services for a monetary reward.

In this regard, the question arises: are taxes paid under a civil partnership agreement? Yes, there are no exceptions in this regard in the legislation. Therefore, the relevant issues need to be dealt with.

What it is

A civil law agreement (CLA) is an agreement between a legal entity and an individual to carry out specific work or solve problems of a certain kind. In this case, the legal entity is the customer, and the individual is the hired contractor.

Obligations under the contract terminate after the end of its term or upon completion of the work. As a rule, payment is made for the results of the work, unless the contract provides otherwise.

Work under a GPC agreement is considered one-time, and the employee is not included in the number of full-time employees. The main feature of the agreement is that it is regulated by the Civil Code of the Russian Federation, and not the labor code.

The GPA is concluded only if certain conditions are met:

- The work is temporary.

- The legal entity does not provide tools for carrying out work and does not create working conditions.

- The agreement establishes the deadline for completing the work and its result, without agreeing on the labor process.

Unlike work under an employment contract, an employee under the GPA independently determines the work schedule and the necessary funds. At the same time, he is responsible for the results of the work performed and compliance with deadlines. Social guarantees are not provided by the employer.

Who deals with payments under the GPC agreement

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

It is very important to understand who pays taxes under the GPC agreement. In fact, everything here is quite simple and depends on with whom exactly such an agreement is drawn up:

- if we are talking about an individual, then in this case the customer company acts as a tax agent. That is, she will have to deal with the payments;

- if the executor means an individual entrepreneur, then the individual entrepreneur must pay everything for himself.

The issue of calculating taxes on GPC should be resolved as early as possible. This way you will definitely avoid claims from the tax authorities.

What taxes and fees do you need to pay?

So, you have figured out that in this case you cannot get rid of taxes. Now you need to understand what exactly to pay. That is, you need to understand what taxes the GPC is subject to in 2021. We are talking about the following:

- Personal income tax (personal income tax) – 13% of income if we are talking about an individual. An individual also has the right to use standard tax deductions, but they will only apply to the period during which such an agreement was in effect;

- insurance premiums - only contributions to the Compulsory Medical Insurance Fund and the Pension Fund will be mandatory. Everything else is determined by the text of the contract. Insurance premiums are as follows:

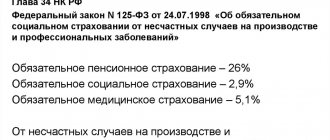

- to the Pension Fund or the Pension Fund – 22%;

- in the Compulsory Medical Insurance Fund – health insurance, the rate will be 5.1%.

Please note that if the customer has the right to apply reduced rates, then he has the right to use it in the described case. That is, this right also applies to payments under GPC.

Also, when deciding what taxes and contributions to pay under the GPC agreement, you need to take into account the Social Insurance Fund or social insurance. And this has its moments.

Thus, contributions are not made for disability or maternity benefits. But there may well be premiums for insurance against injury or occupational disease if they are provided for in the text of the agreement.

Contract agreement with an individual: taxation of insurance premiums in 2020–2021

If an organization has entered into a contract with an individual, then taxation of insurance premiums in 2019–2020 will not differ from taxation in previous years.

Thus, under contract agreements with an individual, contributions for compulsory pension insurance are charged (clause 1, article 7 of the law “On compulsory pension insurance in the Russian Federation” dated December 15, 2001 No. 167-FZ, clause 1, article 420 of the Tax Code of the Russian Federation).

In addition, contributions for compulsory medical insurance are charged (Article 10 of the Law “On Compulsory Medical Insurance in the Russian Federation” dated November 29, 2010 No. 326-FZ, paragraph 1 of Article 420 of the Tax Code of the Russian Federation).

In the Ready-made solution from ConsultantPlus, you can find out how to calculate insurance premiums for certain situations, for example, under a car rental agreement; for remuneration to members of the board of directors. If you do not have access to the K+ system, get a trial online access for free.

Payments under a work contract are not subject to contributions for compulsory insurance in case of temporary disability and maternity (subclause 2, clause 3, article 422 of the Tax Code of the Russian Federation).

Contributions for insurance against occupational diseases and occupational accidents under civil contracts are accrued only if this is provided for by the terms of the agreement (Clause 1, Article 5 of the Law “On Compulsory Social Insurance against Occupational Accidents and Occupational Diseases” dated July 24. 1998 No. 125-FZ).

All details on how to calculate insurance premiums to the Federal Social Insurance Fund of the Russian Federation for injuries for payments under civil contracts are given in the Ready-made solution from ConsultantPlus. Study the material by getting trial access to the K+ system for free.

How to reduce taxes and contributions under a GPC agreement

The issue of tax optimization worries many today. And he did not ignore civil contracts. It should be taken into account that there is a possibility of reducing payments if the customer belongs to a preferential group. Then such a person can use the reduced tariffs legally.

It is also very important to correctly formulate the terms of the contract. That is, so that it is possible to correctly establish without any problems the amount that the customer owes for work and materials. The more specific you are, the fewer problems you will have with the tax authorities later.

When carrying out any activity that involves making a profit, you need to deal with taxes and fees. This will help you not to encounter unpleasant questions from the Federal Tax Service of the Russian Federation later. And the GPC agreement is no exception.

In addition to the permanent staff enrolled in the enterprise, the employer may attract additional workers on a temporary basis to provide certain services. In this case, the relationship between the parties is regulated by a civil contract.

The proposed material examines how insurance premiums are withheld under a GPC agreement in 2021, taking into account legal norms and general principles of taxation in the Russian Federation.

- Peculiarities of civil law contracts (GPC)

- Are GPC agreements subject to insurance premiums in 2021?

- What insurance premiums are charged under GPC agreements?

- Amounts of contributions under GPC agreements

- How can you reduce the base for insurance premiums?

- Features of payment of insurance premiums under GPC agreements

- Deadlines for payment of contributions from the GPC agreement

- How reporting is generated when paying fees under a GPC agreement

- 2-NDFL

- 6-NDFL

- Payment document for insurance premiums

- Video on the topic of the article

Remuneration under the contract

The contract must indicate the specific amount that the customer is willing to pay for the work performed.

In most cases, the contractor's work is paid only after the final delivery of its results. However, the contract may also provide for advance payment for the results of the work.

Based on the results of the provision of services, the contractor draws up a delivery and acceptance certificate, which is drawn up as an appendix to the contract. This act is the basis for payment for services rendered.

note

If the customer refuses to pay for the work performed without good reason, the contractor has the right not to deliver the results of the work until he receives everything that is due to him (Article 359 of the Civil Code of the Russian Federation).

If the customer is not satisfied with the result of the work, a fine can be collected from the contractor. The amount of the fine is also stipulated in the contract.

You can terminate the contract at any time. In this case, you do not need to pay the contractor the entire amount specified in the contract. You only need to pay the part that is commensurate with the work performed.

Peculiarities of civil law contracts (GPC)

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

A civil contract is an agreement concluded by an employer with an employee, without the latter being included in the staff of the enterprise, to perform certain work.

The GPC agreement has the following features:

- performing pre-agreed work or providing a service, without taking into account corporate rules and the need to comply with labor regulations at the enterprise;

- determining the deadlines for the fulfillment of obligations by the involved employee;

- setting prices by mutual agreement.

A GPC agreement differs from an employment agreement:

- the fact that the hired employee is not included in the staffing table with a permanent contract;

- no need to provide a workplace.

In this case, the agreement is temporary and does not imply the assignment of wages. Piece remuneration is expected if the work is completed in accordance with the requirements and on time.

Are GPC agreements subject to insurance premiums in 2021?

The question of whether insurance premiums are charged under civil law agreements interests many.

The legal basis for the procedure for withholding insurance premiums under GPC agreements is determined by the provisions of the current Civil and Tax Codes of the Russian Federation.

The provisions of the listed standards require mandatory payment of contributions for pension and health insurance within the framework of the taxable amount accepted as the calculation base for a civil contract.

Insurance contributions to the Social Insurance Fund are not subject to payment. An exception applies to injury deductions, the manner of withholding of which may be determined by the terms of the agreement entered into by the parties.

A similar legal procedure is provided for when concluding contract agreements with individuals. This rule must be observed, regardless of the tax system under which the company operates.

The specified legal conditions apply to insurance premiums for the employment of individuals under contract with these employees for the following purposes:

- to perform this or that work;

- when providing services;

- for copyright orders;

- when transferring copyrights to use products.

Note! Insurance premiums cannot be deducted from compensation payments that reimburse the employee for the costs incurred by him in connection with the fulfillment of the terms of the contract.

These accrued amounts are not taken into account in the calculation base and are not subject to insurance premiums, since they are not related to making a profit, but are aimed at compensating for damage suffered by an individual.

When payments under contract agreements are not subject to contributions

There are cases when remuneration under contract agreements is not subject to insurance premiums:

- If the service is provided by an individual entrepreneur. In this case, he makes contributions to the budget for himself

- If the work is performed by a foreigner or stateless person temporarily staying in Russia

- If students work at a university as part of a student team under a contract agreement

- If funds were received under a lease agreement

- In real estate transactions

- If you have received loans or borrowings

Based on this, you can reduce the amount of payments to the budget. To do this, you need to draw up contracts that specify both the service and, for example, the sale of goods. That is, if the contractor sets up the Internet and at the same time sold a modem to the customer, then you only need to pay fees for the activity of setting up the Internet.

It is worth following the drafting of the contract very carefully. The Social Insurance Fund very often tries to see in such contracts signs of labor, with all the ensuing consequences. Therefore, in the contract, all conditions must be verified and there should not even be a hint of labor relations.

What insurance premiums are charged under GPC agreements?

Taking into account the legal framework provided for by law, within the amount payable under the terms of the GPC agreement, the employer is obliged to pay the following insurance premiums:

- according to the compulsory medical insurance system;

- for pension insurance.

Current legal norms exempt the employer from paying insurance premiums related to maternity and temporary loss of ability to work, the recipient of which is the Social Insurance Fund. The parties have the right to separately stipulate the procedure for withholding insurance premiums for injuries (in connection with accidents or occupational diseases), providing for or eliminating the need for these payments.

When determining the tax base, it is important to take into account that the legal norms of relations between the parties under a GPC agreement are regulated not by the Labor Code, but by the Civil Code, and that the involved employee is not part of the company’s staff.

The payment provided for the performance of work under the GPC agreement is necessarily included in the personal income tax base. In this situation, the customer acts as a tax agent, and therefore is obliged to calculate, withhold and transfer the tax to the state treasury.

It is necessary to take into account the peculiarity that such a role does not apply to the customer if we are talking about attracting an individual entrepreneur who will pay the tax himself, based on his own profit.

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

At the same time, the legal norms of the legislation in the Tax Code of the Russian Federation do not detail how to prove that payment under the GPC agreement was made to the entrepreneur.

The personal income tax rate for payments under the GPC agreement is 13 percent, as for any other type of income. An individual is given the right to use the possibility of a standard tax deduction, but within the validity period of the GPC agreement.

The reporting of an enterprise as a tax agent must be submitted no later than the beginning of April in the year following the reporting year. In addition to the annual report, these documents, with increasing indicators, should be submitted every quarter, half year and nine months.

In the 2-NDFL report, which is a standard form for providing information to the tax department, this type of income is indicated by code 2010. The recording date of the specified income is noted on the day the money is paid to the employee.

There is no need to specify personal income tax payment in the agreement itself, since here the parties take into account the requirements of legal regulations.

Considering that payments under GPC agreements are among those that are subject to the calculation of insurance premiums, reporting documentation on these deductions must be submitted by the 30th day of the month following the reporting month.

Since payments under these agreements are not subject to insurance premiums for temporary loss of ability to work and maternity, the specified employee is not included in the number of persons for whom contributions are paid.

The parties must agree in the concluded GPC agreement on the need for the employer to pay contributions for injuries. If such deductions are made, the employee will be protected in the event of injury. Otherwise, he is not covered by the possibility of receiving payments from the Social Insurance Fund in the event of an accident or occupational illness.

If such conditions are provided for in the contract, the relevant data should be reflected in the 4-FSS report. Otherwise, the information is not entered there.

Features of paying taxes and contributions for advance payments

In the event that the GPC agreement provides for the payment of an advance to the contractor, insurance premiums must also be charged on it. There are certain nuances regarding personal income tax.

Accrual and payment of personal income tax

The transfer of tax to the budget for full-time employees and third parties when concluding a GPC agreement is significantly different. If the performer does not work for the company, then personal income tax should be withheld at the time of transfer of the advance. This requirement is established by the Tax Code of the Russian Federation, and the Ministry of Finance of the Russian Federation has repeatedly pointed out to it in its letters and clarifications. The regulatory authorities note that advances paid are fully included in the income of the contractor in the period in which the payment was made. The moment of completion of the work and signing of the acceptance certificate does not affect this in any way. If there is an employment relationship with the contractor and he is entrusted with performing certain work in the GPC agreement, personal income tax is withheld on the last day of the month. This is due to the fact that the employee’s main income is salary, and tax is withheld from it on the last day of the period, as required by the Tax Code of the Russian Federation. There may be cases when an organization cannot perform the functions of a tax agent. In such a situation, she is obliged no later than a month after the end of the year to notify the executor under the GPC agreement and the supervisory authority. This fact is reported using Form 2 of the personal income tax.

Calculation and payment of insurance premiums

In accordance with the norms of the Civil Code of the Russian Federation, the form of payment under a civil process agreement can be any: installments, prepayment, payment in full upon completion of work, and so on. The Tax Code of the Russian Federation does not provide any nuances regarding the inclusion of remuneration amounts in the base for calculating contributions. Consequently, the organization, in the case of paying an advance to the contractor, is obliged to charge insurance premiums for this amount. The calculation of the amount of contributions to be paid is made on the last day of the month when the remuneration was accrued. If the contractor returns the advance amount, the company will have an overpayment of insurance premiums, which should be reflected in the declarations. This will reduce the next payment.

Amounts of contributions under GPC agreements

The tariff rates for those items of social insurance contributions that the employer is subject to under these agreements are no different from similar deductions in any other situations.

In accordance with Art. 425 of the Tax Code of the Russian Federation, the legal framework of the legislation requires the withholding of such insurance premiums:

- within the framework of mandatory pension payments - 22 percent of the limit specified by law, with an addition of 10 percent of the excess of this amount;

- for compulsory health insurance – 5.1 percent, regardless of the amount of deductions.

The procedure for calculating insurance premiums is easier to understand using a specific example.

Taking into account the tariffs established by legal norms, the amount of contributions will be:

If the employer resorts to reduced tariffs, the specified limit on contributions to the Pension Fund does not apply.

Reduced tariffs may be assigned in situations where similar conditions apply to full-time personnel. This possibility is provided for certain categories of employees, the list of which is quite limited and approved by law.

With a reduced tariff, the amount of contributions can be reduced to 15 percent.

It’s more complicated with legal regulations regarding additional tariffs. An increase in contributions is expected if the work offered to the employee under a civil process agreement involves an increased degree of harmfulness or danger and corresponds to certain professions that fall under a similar list.

In this case, contributions increase in accordance with the amounts provided for by law.

Contributions to pension insurance and healthcare

Pension provision and receiving free medical care are important moments in people's lives.

For this reason, it is stipulated that payments under contract agreements must be transferred to the amount of contributions to the budget.

Contribution rates are 22% for pension insurance and 5.1% for health insurance. As you can see, the contribution rates are no different from those applied by employers to their employees working under employment contracts.

How can you reduce the base for insurance premiums?

When calculating the base for insurance premiums, you should adhere to certain limits that provide for the appointment of additional payments.

The following limits are established for pension insurance (depending on the year, in thousands of rubles):

- 2019 – 1 150;

- 2020 – 1 292.

In practice, organizations resort to various tricks to comply with legal regulations and reduce the size of the tax base. Instead of a regular GPC agreement, a mixed agreement may be concluded that has features of both types of documents.

For example, hiring a citizen to sell products may involve, in addition to these responsibilities, installation and configuration of equipment.

Considering that contributions are not paid under lease agreements and in relation to purchase and sale, there is no need to highlight services as a separate item. In this case, the tax base will be uniform.

Expert opinion

Semenov Alexander Vladimirovich

Legal consultant with 10 years of experience. Specializes in the field of civil law. Member of the Bar Association.

But if you indicate that the subject of the contract involves the involvement of a specialist not in the profession, but, for example, to sell a dress, insurance premiums will not be withheld.

Features of payment of insurance premiums under GPC agreements

As follows from the above-described features of the taxation of payments under GPC agreements with insurance premiums, the following points must be taken into account:

- deductions can be withheld solely from agreements for the performance of work or provision of services, or for the transfer of intellectual property rights;

- GPC agreements on property transactions (purchase and sale or lease) concluded with volunteers or involving the provision of services outside the Russian Federation are excluded from the list subject to withholding of contributions;

- Only payments to the Pension Fund and Compulsory Medical Insurance are withheld;

- contributions for injuries are deducted if such a condition is provided for in the contract;

- When assigning deductions, standard tariff rates are applied, with the use of general established limits, increased or reduced tariffs.

There are no other differences in the deduction of insurance premiums under GPC agreements. If the legal situation does not imply insurance payments, this is not reflected in the reporting documentation.

Contributions to funds under a civil contract

Under GPC contracts, insurance premiums are paid only in the “pension” part and for compulsory medical insurance. For performers under construction contracts and other civil and industrial contracts, insurance in case of maternity and disability is not provided (Clause 2, Part 3, Article 9 of Law No. 212-FZ). Insurance premiums to the Social Insurance Fund for industrial accidents and occupational diseases are also not accrued on GPC contracts. But, if the terms of the contract directly indicate the customer’s obligation to pay contributions for “injuries,” then these contributions should be paid (Part 1, Article 20.1 of Law No. 125-FZ of July 24, 1998).

Otherwise, insurance premiums under a civil contract are calculated similarly to an employment contract, at the following rates:

- 22% - pension contributions,

- 5.1% - contributions for health insurance.

If the customer has the right to apply reduced rates, then he will apply them to payments under GPC agreements.

Please note that when assessing contributions for a civil contract, it is necessary to exclude from the taxable base compensation for the contractor’s expenses for materials, tools, etc. – these costs are not subject to insurance premiums (Clause 2, Part 1, Article 9 of Law No. 212-FZ).

When concluding a GPC agreement instead of an employment contract, you need to be very careful about its content so that the inspection authorities do not reclassify it as a labor agreement. If such an agreement is challenged by the Social Insurance Fund, and it is recognized as regulating labor relations, then contributions will be accrued for the entire amount of payment under the GPC agreement, and not only contributions in case of disability, but also for “injuries”.