What payments are due upon dismissal?

On the last day of work, as a general rule, regardless of the reason for the employee’s dismissal, he must be paid:

- all due wages on the day of dismissal,

- compensation for missed vacation days.

When terminating an employment contract due to staff reduction, liquidation of an organization, often when terminating an employment contract by agreement of the parties, in addition to the above payments, the quitter is paid severance pay. In addition, if an employee is laid off, he is entitled to retained earnings for the duration of his employment.

Compensation payments upon dismissal

According to current legislation, the procedure for leaving a job is preceded by the employee filing an application as a notification to the manager 2 weeks before he leaves the organization. The specialist has an obligation to work 14 calendar days for the director to find a new employee. This rule applies if he does not belong to a preferential category of the population. The next step is to issue a dismissal order, in which the person signs, which is considered to be his familiarization with the issued document. The contract with the employee is terminated. On the last day, a work book with the corresponding entry is issued and payments are calculated.

Mandatory ones include:

- wages due to the employee for the days he worked during the last month;

- compensation for unused vacation days (if he was on vacation for 28 calendar days, this payment is not provided).

Calculation and accrual upon dismissal is carried out by the accounting department, the amount depends on the number of days worked and the average salary.

For example, a citizen has a monthly income of 50 thousand rubles. The employee wrote a letter of resignation on April 5, taking into account 14 days of work, his last working day is considered to be the 18th. Thus, during the month, the citizen performed his official duties for 14 shifts out of 22. Dividing the salary by the number of days worked, we get the accrued salary in the amount of 35 thousand 700 rubles.

To determine the amount of compensation for unused vacation, the accountant needs to know how much the average earnings of the dismissed person are for the last 12 months of work. It is calculated using the formula: the amount received by the employee during 1 year / 12 months / 29.3 (average number of calendar days in a month). To obtain the payment amount, average earnings per day * number of vacation days. For example, 50 thousand rubles / 12 / 29.3, we get 1706. 1706 * 28 days of rest = 47781 - compensation for unused vacation.

Compensation for unused vacation

Every year, the employer is obliged to provide an employee with leave of 28 calendar days while maintaining average earnings (Article 114 of the Labor Code of the Russian Federation). If at the time of dismissal the vacation has not been taken off completely, these days must be compensated (Article 127 of the Labor Code of the Russian Federation). If vacation is provided in advance, then the amount previously paid for excessive vacation days is withheld from the employee. Whether compensation upon dismissal is subject to insurance contributions is regulated by Article 422 of the Tax Code of the Russian Federation. In paragraphs Clause 2, paragraph 1 of this article states that compensation for vacation pay cannot be excluded from the object of taxation with insurance contributions.

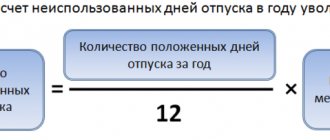

For each month worked in full, an employee is entitled to 2.33 calendar days of vacation. Moreover, if in the last month of work an employee worked more than 15 days, then he is considered fully worked and is included in the calculation. If less, then the month is excluded from the calculation.

| Limited Liability Company "Pion" ORDER dated 02/05/2020 No. 111 On payment of compensation for unused vacation upon dismissal In connection with the dismissal of manager Semenov Semen Semenovich on 02/06/2020, in accordance with order No. 110 of 02/05/2020 and guided by Article 127 of the Labor Code of the Russian Federation, I ORDER:

General Director A.V. Voronov |

The amount of compensation for vacation unused on the last day of work is calculated using the formula:

The average daily income is determined similarly to the calculation of vacation pay (clause 10 of the procedure approved by government decree No. 922 of December 24, 2007).

How is vacation compensation paid?

To receive “vacation” compensation, the reasons for terminating the employment contract are not important, this is exactly what Rostrud indicated in its letter dated July 2, 2009 No. 1917-6-1. If, at the time of dismissal, an employee has not taken time off not only from his main annual 28-day leave, but also from additional (for example, during irregular working hours, when working in harmful and dangerous conditions, or for work in the Far North), then compensation is paid to him for such a vacation too.

Unused vacation is compensated when an employee is transferred from one organization to another, as well as when he is hired for another position in the same place of work, but through dismissal (Article 77 of the Labor Code of the Russian Federation).

The number of vacations that an employee has accumulated is not limited - he must receive compensation for all unused days, since the law does not limit the period for using vacation (Article 127 of the Labor Code of the Russian Federation).

The employee must be given compensation for vacation along with his salary, bonus and other payments due to him on the last day of work.

Please note that “vacation” compensation is not always associated with dismissal: an employee may ask to replace additional leave exceeding the standard 28 days with monetary compensation. This replacement does not apply to regular vacation (Part 1 of Article 126 of the Labor Code of the Russian Federation).

Vacation compensation is not due to those employees who quit after working less than 15 days, as well as those working under GPC contracts (Article 11 of the Labor Code of the Russian Federation, letter of Rostrud dated 06/08/2007 No. 1920-6).

Insurance premiums and personal income tax

The procedure for levying insurance premiums and personal income tax depends on the type of payment in the final settlement. Compensation for unused vacation is subject to insurance contributions and personal income tax in full (clause 2, clause 1, article 422 and clause 3, article 217 of the Tax Code of the Russian Federation). And other types of compensation upon dismissal will be subject to contributions depending on their size. If the amount of payments, including severance pay and average monthly earnings, does not exceed the amount of the three-month average salary of the resigning employee, then they are exempt from insurance contributions and personal income tax in full (clause 2, clause 1, article 422 of the Tax Code of the Russian Federation). From the amount of compensation payments to a former employee that exceeds three times the amount of wages, it is necessary to calculate and pay insurance contributions to the budget, and personal income tax must be withheld from them.

IMPORTANT!

Severance pay, retained income during employment, and other compensation upon dismissal are taxed if their total amount exceeds three times the employee’s average monthly earnings. And vacation compensation upon dismissal is always subject to insurance contributions and personal income tax.

Leave compensation upon dismissal, insurance premiums

Info

Online cash register: who can take the time to buy a cash register Individual business representatives may not use online cash register until 07/01/2019. However, for the application of this deferment there are a number of conditions (tax regime, type of activity, presence/absence of employees).

So who has the right to work without a cash register until the middle of next year? < … Home → Accounting consultations → Insurance premiums Current as of: July 7, 2021 Many employees have unused vacation days at the time of dismissal. Under such circumstances, an employee can write an application for leave with subsequent dismissal (provided that he is not fired for guilty actions) or receive compensation for unused leave (Article 127 of the Labor Code of the Russian Federation, clause 28 of the Rules, approved by the People's Commissariat of Labor of the USSR on April 30, 1930 No. 169). Let's assume the employee has chosen compensation upon dismissal.

Severance pay and retained earnings during employment

If the employment contract is terminated due to staff reduction, the employer is obliged to pay severance pay in the amount of average monthly earnings (Article 178 of the Labor Code of the Russian Federation). By agreement of the parties, the amount of severance pay is limited to the financial capabilities of the employer. In this case, the payment procedure is prescribed in a collective or employment agreement and is specified in the agreement between the employee and the employer. Also, an employee dismissed due to layoffs retains his average earnings for the duration of his employment, but not more than two months. The calculation of retained income also includes severance pay. In exceptional cases, earnings are retained for another month if the right to it is confirmed by the employment service.

The calculation of severance pay and retained earnings during layoffs is similar:

The number of working days during the payment period is determined according to the organization’s work schedule. The calculation begins on the working day following the dismissal. For example, if an employee quit on June 25, 2020, then severance pay is paid to him for the period from June 26, 2020 to July 25, 2020. Saved earnings for the second month will be calculated for the period from 07/26/2020 to 08/25/2020.

The average daily earnings are calculated based on payments for the last 12 months preceding the month of dismissal, in accordance with paragraph 4 of Resolution No. 922. The calculator for calculating leave compensation upon dismissal will help you not make mistakes in the calculations.

Leave compensation upon dismissal is subject to insurance contributions

- Themes:

- Labor compensation

See how to calculate and pay compensation for unused vacation in 2021, how to determine the number of days to be compensated, as well as what income code to indicate in the 2-NDFL certificate. applications to replace vacation with monetary compensation When an employer is obliged to pay compensation Compensation is paid for each month of work. If an employee has worked for more than half a month, he is paid compensation as for a full month. Therefore, even if an employee worked only 1 month or more than half a month, he is entitled to payment of compensation for unused vacation upon dismissal in 2021. EXAMPLE 1 Ivanov I.A. hired on June 1, 2021, dismissed on June 20, 2021 at his own request. The employee worked more than half a month.

Insurance premium deductions

In 2021, deductions of insurance premiums (IC) are carried out in accordance with Chapter. 34 Tax Code of the Russian Federation. Control over the accuracy of accruals, transfers and reporting is carried out by the Federal Tax Service.

Contributions for injury prevention are made to the Social Insurance Fund account. Transfer of contributions to the budget for the billing (monthly) period is carried out simultaneously for all amounts accrued for the enterprise.

When calculating contributions for a dismissed employee, previously accrued benefits are taken into account on an accrual basis. Summing up income from the beginning of the calendar year makes it possible to determine whether the maximum base value has been reached for individual contributions.

Limits that determine contribution rates are established for contributions to compulsory pension and social insurance (OPS and OSS). The limits are recalculated annually.

The amount of contributions paid to the Social Insurance Fund for the prevention of injuries and occupational diseases is determined by the main type of activity of the enterprise. There is no limit on the amount of income received by the employee by the date of dismissal for deductions. The tax period established for calculating contributions is a calendar year.

Calculation of taxes when issuing compensation payments for vacation upon dismissal

According to Article 223 of the Tax Code of the Russian Federation, all tax fees transferred to the budget must be paid not at the end of the working month, as when calculating salary, but on the day of transfer of compensation for leave upon dismissal. In this case, the date of receipt of the worker’s income will be considered the day:

- transferring funds to the bank to his account;

- payment of income upon dismissal from the employing organization's cash desk;

- receiving money at the cash desk of a banking institution from the employer’s account according to a payment order.

Based on all of the above, the employing organization must pay taxes and contributions on the day the compensation is paid.

When issuing compensation payments to a former employee for a vacation not taken, the employer is required to pay taxes no later than the day following the day of dismissal.

Calculation of insurance premiums for compensation of unused vacation

Compensation for unused vacation is not exempt from the calculation of insurance contributions to the Pension Fund and the Social Insurance Fund (currently all these contributions are collected by the Tax Inspectorate). These payments must be made from the employer’s funds and cannot reduce the amount of compensation.

Contributions from compensation are deducted for pension, social and health insurance, as well as for “injury”. Contribution rates depend on the applicable tax regime, the availability of benefits from the employer and the type of activity. In general, 22% is allocated to pension insurance, 5.1% to medical insurance, 2.9% to social insurance, and from 0.2 to 8.5% to injuries.

When determining the amount of insurance premiums, the employer must take into account the limits established for the current year. If the employee’s income exceeds 1,021,000 rubles, then the pension insurance rate is reduced to 10%. The limit for social insurance, beyond which contributions are not paid, is 815 thousand rubles.

Insurance premiums are transferred within the standard time frame: before the 15th day of the month following the billing month.

As for personal income tax, vacation compensation, unlike severance pay, is subject to contributions in full. Personal income tax is charged at a standard rate of 13%. In this case, the employer performs the functions of a tax agent: he withholds and transfers the withheld tax to the budget. Personal income tax is translated in accordance with clause 3 of Art. 217 Tax Code of the Russian Federation.

For example, if the amount of vacation compensation was 25 thousand rubles, then the employee will receive 21,750 rubles. minus personal income tax (25000-25000*13%).