Report form 6-NDFL must be filled out on new sample forms approved for use on March 26, 2021 (Order of the Federal Tax Service of the Russian Federation No. ММВ-7-11/18 dated January 17, 2021). It must be borne in mind that the report for the 1st quarter is a report for the first three months of the year, including indicators on the income of individuals for this particular period (January February, March). The declaration for the 1st quarter is submitted to the Federal Tax Service no later than April 30 of the current year.

Report 6-NDFL, in addition to the Title Page, contains:

- Section 1 reflects general indicators for the first quarter of 2021: indicates the total amount of personal income tax withheld from the income of individuals for 3 months;

- Section 2 contains information about the dates and amounts of tax withheld for the first quarter, since the tax office will refer to these indicators for violations, if any.

Calculation form 6-NDFL for the 1st quarter of 2021

The composition of the new form has not changed at all - it consists of a title page and two parts:

- Section 1 – generalized indicators of income, accrued, withheld and paid tax,

- Section 2 – dates of payments and amounts of income and tax withheld from them.

We described in detail what changes have occurred in the new 6-NDFL form for the 1st quarter of 2021 in our recent publication. The introduced innovations concern mainly the successors of reorganized and liquidated legal entities, having changed the title page and practically not affecting the main sections of the form.

To fill out the Calculation, you can download the new 6-NDFL form (Q1 2018) from the above link.

Let us remind you that Calculation 6-NDFL for the 1st quarter of 2021 should be submitted to the Federal Tax Service no later than 05/03/2018. The due date has been postponed from 04/30/2018 due to non-working holidays.

No payments: what to do with 6-NDFL

To answer this question, let's change the conditions of the example:

Due to the seasonal nature of the activities of Investstroyproekt LLC, no income was paid to individuals in the 1st quarter of 2021. They decided not to issue a zero calculation in form 6-NDFL.

This article will tell you about zero 6-personal income tax.

The director of Investstroyproekt LLC (in order to avoid sanctions from the tax authorities for failure to submit 6-NDFL) sent a letter to the controllers:

“Explanations on Form 6-NDFL

for the 1st quarter of 2021

Investstroyproekt LLC reports that during the 1st quarter of 2020 it did not conduct business activities and did not pay wages.

In such a situation, Investstroyproekt LLC is not recognized as a tax agent for personal income tax and is not obliged to submit 6-personal income tax calculations (Articles 226 and 230 of the Tax Code of the Russian Federation).”

The director signed the notice, putting it on the company's letterhead (containing all the necessary details) and indicating on it the name and number of the inspection (to which the payment should be received).

Rules for filling out 6-NDFL for the 1st quarter

The procedure for filling out the new Calculation 6-NDFL is contained in Appendix No. 2 to the order of the Federal Tax Service of the Russian Federation dated October 14, 2015 No. ММВ-7-11/450 (as amended on January 17, 2018).

The general rules for filling out 6-NDFL for the 1st quarter of 2021 require filling it out separately for each OKTMO. If, when filling out sections of the form, there is not enough space on one page for all indicators, the required number of pages is drawn up. All Calculation sheets are numbered in order.

When preparing the “paper” 6-NDFL for the 1st quarter of 2021, you cannot print the form on both sides of the sheet, staple the pages and use a proofreader to correct errors. Should only be printed in black, purple or blue.

If there are no total indicators, “0” is indicated in the line; dashes are placed in empty text fields.

Previously, we have already reviewed the new Calculation form, including filling out its title page: please note that in 6-NDFL for the 1st quarter of 2021 (see sample at the end of the article), code “21” is indicated in the “Submission period” field, and the tax period - “2018”.

The indicators in lines 010-050 of section 1 are filled in for each tax rate separately, incrementally from the beginning of the year. Lines 060-090 are filled out only on the first sheet of section 1, summed for all bets.

For section 2, the procedure for filling out 6-NDFL for the 1st quarter of 2021 is different: this section contains indicators related to the last quarter of the period. Thus, section 2 of the Calculation for the 1st quarter contains the indicators of the 1st quarter, the calculation for the half year contains the indicators of the 2nd quarter, etc.

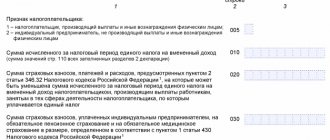

Completing Section 1

A correctly completed report will avoid misunderstandings with tax inspectors.

Table No. 1. The order of filling out the lines in Section 1.

| Line | Information displayed in line |

| 010 | The tax rate is indicated |

| 020 | The amount of accrued income for all employees of the enterprise is reflected at the appropriate tax rate. In this line, in addition to the basic income of individuals, partially taxable income is indicated in the total amount of accruals. |

| 025 | Income in the form of dividends is shown. |

| 030 | In this cell 6-NDFL for the 1st quarter of 2021 reflects the amount of tax deductions, for example, for partially taxable types of income of individuals (material assistance, gifts, etc.). The amount specified in this cell cannot exceed the amount specified in cell 020 (control ratio). |

| 040 | The amount of tax calculated on employee income. Checked by the control ratio: (page 020 – page 030) * page 010. |

| 045 | This cell calculates the amount of tax liability for accrued dividends. |

| 050 | 6-NDFL for 1 sq. 2021, which expires on April 2, 2018, line 050 shows the amount of permanent advance payments offset by the enterprise against the tax liability calculated from the receipts of foreign entities performing their duties on the patent. Reference ratio: page 050 ≤ page 040. |

| 060 | The number of employees at the enterprise who received taxable income in the current reporting period (1st quarter) is indicated. |

| 070 | 6-NDFL for 1 sq. 2021, can be found on our website, in this cell it states the amount of tax liability withheld from income. Reference ratio: page 070 ≤ page 040. |

| 080 | The amount of tax liability for some reason not withheld in the current period. |

| 090 | The amount of tax liability returned to individuals is recorded (Article 231 of the Tax Code of the Russian Federation). |

Example of filling out 6-NDFL - 1st quarter of 2021.

At Voskhod LLC, employees were paid the following amounts:

- 01/09/2018 salary for December 2021 – RUB 332,000.00. (of which 43,160 rubles were withheld personal income tax);

- 02/09/2018 salary for January – 330,000.50 rubles. and bonus – 120,000.00 rubles. (personal income tax - 58,500 rubles);

- On February 12, 2018, the employee was paid financial assistance related to the birth of a child - RUB 40,000.00. (maternity assistance for a child up to 50,000 rubles is not subject to tax);

- 03/07/2018 salary for February - 318,000.00 rubles, sick leave was paid along with the salary - 10,230.60 rubles. (personal income tax 42,670 rubles);

- On March 15, 2018, the employee received a gift from the company for his anniversary worth RUB 6,000.00. (personal income tax - 260 rubles);

- 04/09/2018 salary for March – 320,000.00 rubles. (Personal income tax - 41,600 rubles).

What will be the filling out of 6-NDFL for the 1st quarter of 2021?

Section 1

Line 010 - personal income tax rate 13%.

Line 020 will include all of the listed income amounts except:

- salaries for December - it should have been reflected in line 020 of the Calculation for 2021, since the date of actual receipt of income is December 31, 2017;

- financial assistance for a child - since it does not exceed the permissible non-taxable limit, there is no need to reflect it in 6-NDFL (letter of the Federal Tax Service of the Russian Federation dated 01.08.2016 No. BS-4-11/13984).

Read more about filling out line 020 in this article.

Line 030 includes a tax deduction - 4000.00 rubles. This is the tax-free portion of the value of the gift. The rest is 2000.00 rubles. (6000.00 – 4000.00) is taxed at a rate of 13%. If the value of the gift was no more than 4,000 rubles, it would not be present at all in lines 020 and 030 of form 6-NDFL for the 1st quarter of 2021.

On line 040 we indicate the accrued tax: multiply the difference between lines 020 and 030 by 13%. The amount of personal income tax calculated in the 1st quarter is RUB 143,030.

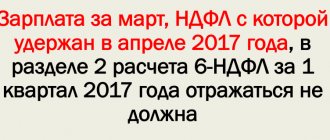

The withheld tax on line 070 includes all amounts, incl. from December wages, but personal income tax from March wages is not reflected in the 6-NDFL report for the 1st quarter of 2021, since it was withheld in April and will be included in the calculation for the half year of 2021. You can read about filling out line 070 in this article.

Section 2

In 6-NDFL for the 1st quarter of 2021, the example of which we are considering, you should fill out several blocks of lines 100 – 140, grouping the indicators by the dates of actual receipt of income (Article 223 of the Tax Code of the Russian Federation), withholding personal income tax and the deadline for its transfer to the budget (Article 226 Tax Code of the Russian Federation).

On lines 100 and 130, respectively, we will reflect the dates of receipt and the amount of salaries and bonuses from which personal income tax was withheld in the 1st quarter of 2018 (the date of actual receipt is the last day of the month for which it was accrued). We take into account that income in line 130 is not reduced by tax and deductions from line 030 of form 6-NDFL for the 1st quarter of 2021 (examples of filling out line 130 can be found in this article):

- 12/31/2017 – 332,000.00 (December salary);

- 01/31/2018 – 450,000.00 (January salary);

- 02/28/2018 –318,000.00 (salary for February).

Personal income tax is withheld from the March salary in April, so it will be included in Section 2 of the Half-Year Calculation, and is not reflected in Form 6-NDFL for the 1st quarter (see, for example, letter of the Federal Tax Service of the Russian Federation dated October 24, 2016 No. BS-4-11/20126 ).

Separately, in lines 100 and 130 we will show the sick leave and the cost of the gift by the date of their payment:

- 03/07/2018 – 10,230.60 (read more about reflecting sick leave in 6-NDFL here);

- 03/15/2018 – 6,000.00 (we indicate the full cost of the gift, despite the non-taxable deduction).

In our example, the day of tax withholding for all types of income is the day of their payment. This date is reflected in line 110, and in line 140 - the amount of personal income tax withheld from the corresponding income on line 130.

Line 120 of form 6-NDFL for the 1st quarter of 2021. – deadline for transferring withheld tax to the budget. In the example, the deadline for tax on all payments is the next day after they are transferred, except for sick leave - the deadline for it will be the last day of the month of payment (Article 226 of the Tax Code of the Russian Federation). If the payment deadline coincides with a non-working day, the next working day following it is indicated.

Deadline

As a general rule, 6-NDFL reports must be submitted to the tax office no later than the last day of the month following the reporting period (Article 230 of the Tax Code of the Russian Federation). If the deadline for submitting form 6-NDFL falls on a weekend or non-working holiday, then the calculation is submitted on the next working day (clause 7, article 6.1 of the Tax Code of the Russian Federation).

April 30, 2021 is Monday. However, 04/30/2018 is a day off due to the transfer to this date of the day off from Saturday 04/28/2018 (Government Decree No. 1250 dated 10/14/2017). The next working day after 04/30/2018 will be 05/03/2018. Therefore, 05/03/2018 (Thursday) is the deadline for submitting 6-NDFL for the 1st quarter of 2021.

How to fill out the calculation on form 6-NDFL for the first quarter of 2021?

Answer:

The calculation of the amounts of personal income tax calculated and withheld by the tax agent for the first quarter of 2021 is filled out according to the form approved by Order of the Federal Tax Service of Russia dated October 14, 2015 N ММВ-7-11/ [email protected] “On approval of the form for calculating tax amounts on the income of individuals calculated and withheld by a tax agent (Form 6-NDFL), the procedure for filling it out and submitting it, as well as the format for presenting the calculation of the amounts of personal income tax calculated and withheld by a tax agent in electronic form.”

In Sect. 1 of the calculation in Form 6-NDFL reflects the amounts of income accrued by the tax agent to individuals for the reporting period, as well as the amount of tax calculated and withheld from such income. In Sect. 2 calculations in form 6-NDFL for the first quarter of 2021 reflect those transactions that were made in January - March 2021.

Rationale:

Tax agents are required to submit to the tax authority at the place of their registration a document containing information on the income of individuals for the expired tax period and the amounts of tax calculated, withheld and transferred to the budget system of the Russian Federation, and the calculation in accordance with Form 6-NDFL, including for I quarter 2018, no later than May 3, 2021. Tax agents - Russian organizations with separate divisions, submit calculations in form 6-NDFL in respect of employees of these separate divisions to the tax authority at the place of registration of such separate divisions, as well as in respect of individuals persons who received income under civil law contracts to the tax authority at the place of registration of the separate divisions that entered into such contracts. In the line “KPP” of the calculation in form 6-NDFL for organizations, the KPP of a separate division of the organization is indicated (clause 2 of Article 230 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of Russia for Moscow dated December 29, 2017 N 13-11 / [email protected] ) .

Form 6-NDFL, the procedure for its completion and submission, as well as the format for submitting the calculation in electronic form are approved by Order of the Federal Tax Service of Russia N ММВ-7-11 / [email protected] (hereinafter referred to as the Procedure).

The calculation according to Form 6-NDFL is filled out on the reporting date, respectively, for the first quarter as of March 31 (Letter of the Federal Tax Service of Russia for Moscow dated July 3, 2017 N 13-11/099595). In the “Submission period (code)” field on the title page, you must indicate “21” (Appendix No. 1 to the Procedure).

At the same time, by Order of the Federal Tax Service of Russia dated January 17, 2018 N ММВ-7-11/ [email protected] certain changes were made to the calculation form, the Procedure, as well as the format for presenting the calculation in electronic form, related to the entry into force of the provisions of clause 01/01/2018. 5 tbsp. 230 of the Tax Code of the Russian Federation in terms of imposing on the legal successor of a reorganized (reorganized) organization the obligation to submit a payment in form 6-NDFL for the reorganized (reorganized) organization in the event of failure to submit reports by such an organization until the completion of its reorganization.

In Sect. 1 of the calculation in Form 6-NDFL indicates the sums of accrued income, calculated and withheld tax, aggregated for all individuals, on an accrual basis from the beginning of the tax period at the appropriate tax rate (clause 3.1 of the Procedure).

Accordingly, the calculation in form 6-NDFL for the first quarter of 2021 reflects the amount of income accrued by the tax agent to individuals for the reporting period (the date of receipt of which for tax purposes of income of individuals, according to Article 223 of the Tax Code of the Russian Federation, refers to this reporting period ) (Letter of the Federal Tax Service of Russia dated January 25, 2017 N BS-4-11/ [email protected] ), as well as the amount of tax calculated and withheld from such income.

In this regard, income, the date of receipt of which according to Art. 223 of the Tax Code of the Russian Federation applies to other reporting periods (for example, wages for December 2021, paid in January 2021), as well as personal income tax calculated from wages in section. 1 calculations in form 6-NDFL (lines 020, 040) for the first quarter of 2021 are not reflected (clause 2 of article 223, clause 3 of article 226 of the Tax Code of the Russian Federation). According to line 070 section. 1 calculation in form 6-NDFL for the first quarter of 2021 reflects the amount of personal income tax withheld when paying income in the first quarter of 2021 (clause 4 of article 226 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of Russia dated December 5, 2016 N BS-4-11 / [email protected] , dated November 29, 2016 N BS-4-11/ [email protected] ).

In Sect. 2 calculations in form 6-NDFL for the corresponding reporting period reflect those transactions that were made over the last three months of this period.

If a tax agent performs an operation in one presentation period and completes it in another period, then this operation is reflected in the presentation period in which it is completed. In this case, the operation is considered completed in the submission period, in which the deadline for transferring tax occurs in accordance with clause 6 of Art. 226 and paragraph 9 of Art. 226.1 of the Tax Code of the Russian Federation (question 3 of the Letter of the Federal Tax Service of Russia dated July 21, 2017 N BS-4-11/ [email protected] ).

So, in Sect. 2 calculations in form 6-NDFL, submitted for the first quarter of 2021, lines 100 - 140 reflect wages accrued for December 2021, paid in January 2021, the date of withholding tax from wages, the amount of tax withheld, as well as the deadline for transferring the tax to the budget.

Information provided by the reference and legal system "ConsultantPlus".

Completing Section 2

Section 2 of the report is intended to display the dates and amounts of accrued and paid income to individuals, as well as the dates and amounts of calculated, withheld and transferred tax liability.

Table No. 2. The order of filling out the lines in Section 2.

| Line | Information reflected in rows |

| 100 | Date of actual income received by individuals. If this is the wages of individuals, then the date will always be the last day of the accrual month, regardless of whether this day falls on a weekend or holiday. |

| 110 | The day of tax withholding, it corresponds to the day of actual payment of wages. |

| 120 | The deadline for personal income tax payment. If vacation or sick pay are reflected according to 6-NDFL for the 1st quarter of 2021, then the date will correspond to the last day of the month of their actual payment. All other types of receipts – the coming day after the day of actual payment of cash amounts. |

| 130 | The amount of income paid to employees. Note that different types of income at the same tax rate can be entered in one line of the block, but provided that all three dates coincide. This rule also applies to personal income tax withheld from them (p. 140). |

| 140 | The amount of tax paid to the budget. |

The same income of individuals is entered into cell 130 as in cell 020 of Section 1. The advance payment is not shown separately here, since the tax on these amounts is not calculated separately; personal income tax is withheld on the day of actual salary payment.

Similar articles

- 6 personal income tax for the 3rd quarter of 2017

- Declaration 6-NDFL in 2018

- Deadline for submitting 2-NDFL (with sign 2) for 2021

- Filling out 6-NDFL for the 1st quarter of 2018

- New form 6-NDFL from 2021