Individual entrepreneurs in their activities are faced with the need to fill out various documents. Most of them - certificates, declarations, reports - are sent to the tax office. Almost all documentation is filled out on the basis of confirmed data, however, there are several forms based on information received from an individual entrepreneur.

Declaration 4-NDFL

An individual entrepreneur submits a 4-NDFL declaration based on assumptions about the amount of income in the next calendar year. In certain cases, the document is required to be submitted to the tax office. The submission procedure is in most cases voluntary, but many entrepreneurs are wondering whether 4-NDFL must be submitted to the Federal Tax Service. During the existence of the enterprise, the individual entrepreneur must send a document to the tax office at least once.

The information provided by the taxpayer is used by inspectors to calculate the amount of advances that will need to be paid over the next year. Tax payments on income received and payments on calculated advances differ from each other.

Submission deadlines and penalties for late reporting

A businessman submits a declaration once, within 5 working days after receiving revenue for 30 days, indicating the amount of funds actually earned for this period, multiplied by 12 months.

If there is a sudden increase or decrease in profit by more than 50%, the 4-NDFL report is submitted again within the 3-NDFL filing deadline (together with the 3-NDFL declaration). According to paragraph 1 of Art. 126 of the Tax Code of the Russian Federation, penalties for late submission of a report to the local inspectorate are low compared to violation of deadlines for filing other reports. The fine will be 200 rubles. However, according to Art. 119 of the Tax Code of the Russian Federation, the fine for late submission of a report is calculated based on the total amount of tax, and since it (the amount) is not indicated in KND 1151021, a fine is unlikely.

Declaration 4-NDFL: who submits it?

This is one of the most pressing issues affecting individual entrepreneurs who have just started their activities. So, who submits 3-NDFL/4-NDFL declarations? The form is filled out in the following cases:

- In the case of receiving the first income from an enterprise, that is, when registering an individual entrepreneur, a 4-NDFL declaration is filled out.

- Who should surrender - entrepreneurs whose income has decreased by 50% at the end of the calendar year.

- Entrepreneurs whose income increased by 50% over the past calendar year.

The legislation of the Russian Federation clearly defines the rules for filing the 4-NDFL declaration - who submits the report and within what time frame. The established rules are not subject to changes or other interpretations.

Brief summary

Declaration 4-NDFL is an accompanying tax report. It is necessary for calculating advance contributions for personal income tax. Entrepreneurs are required to submit the form when starting a business, switching to OSNO from another regime, or a sudden change in revenue. In other cases, the Russian Ministry of Finance ordered the tax service to use the 3-NDFL declarations previously submitted by the payer for calculations.

The form, submission procedure and deadlines for providing information are strictly regulated. Violation of the rules faces a fine of 200 rubles.

Due dates

The legislation establishes certain time frames within which all forms must be submitted, including the 4-NDFL declaration 2016. Those who submit the declaration - namely individual entrepreneurs - must draw up the document within a certain time frame; As a rule, there are no difficulties with this. The report is provided within the following deadlines:

- The completed form for new entrepreneurs is submitted within five days of the month following the month in which the first profit was received.

- Existing individual entrepreneurs file a declaration after an increase or decrease in profits. This usually happens at the beginning of the next tax period.

Deadlines for submitting 4-NDFL in 2021

A specific number has not been established here, because an individual entrepreneur can receive his first income on any day - it depends. The deadline is calculated as follows: the form must be submitted within 5 days after a month has passed from the date of the first income.

It’s a little confusing, so here’s an example: individual entrepreneurs began using OSNO from the beginning of 2021. His first income came on January 21. We add a month and five more days (working days!) to this date - we get the deadline until February 28.

Important! There is also such a point: The estimated income that the individual entrepreneur puts in the declaration is calculated on the basis of the first income actually received and the economic considerations of the businessman. But during the year the situation can change dramatically, and this figure can change either up or down. If this change is serious (we focus on 50%), then it is better to submit an updated declaration.

In principle, it is not necessary to take it, but it is advisable. For example, it is in your best interests to do this if your income has changed downward, the tax office will recalculate your advance payments, and you will not overpay them all year.

The difference between 4-NDFL and 3-NDFL

- The 3-NDFL declaration is drawn up on the basis of income already received for the past calendar year, while the 4-NDFL is drawn up on the basis of estimated income.

- Taxation standards are taken as the basis for filling out 3-NDFL. Its completion is mandatory for those citizens who received a certain income on which tax was not paid: for example, the amount from the sale or rental of real estate.

- Declaration 3-NDFL is drawn up for an individual to receive property or social tax deductions.

In some cases, declarations in forms 3-NDFL and 4-NDFL are compared with each other - for example, when it is not possible to calculate an advance based on the information provided in 4-NDFL.

What is it and who rents it?

Until 2021, individual entrepreneurs had to submit a declaration in form 4-NDFL on the general taxation system after receiving their first income in the year (from the moment the application of the OSN began or the transition to it).

In 4-NDFL, the entrepreneur indicated the estimated income for the year that he planned to receive (minus expenses). Based on this information, the Federal Tax Service calculated and sent payment slips to individual entrepreneurs for the payment of quarterly advance payments for personal income tax.

It was necessary to resubmit 4-NDFL if the income received during the year differed significantly (by more than 50%) from that indicated in the previously submitted declaration. This was necessary for accurate calculation (adjustment) of advances payable.

At the end of the year, entrepreneurs on OSNO must submit a 3-NDFL declaration.

Procedure for filling out the declaration

To register 4-NDFL, there is a form established by law in which all the necessary data is entered. The declaration form is very simple, filling it out should not cause problems. To avoid errors when filling out, it is advisable to study samples of the completed form in advance - they are usually placed on the appropriate stands at the tax office.

The 4-NDFL declaration is drawn up according to standard rules:

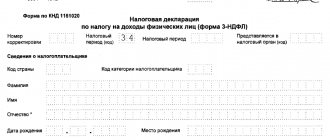

- The TIN number is indicated at the top of the form.

- The adjustment number is entered at the top of the 4-NDFL form. Who submits the declaration for the first time, Fr.

- Tax period is the date after which the individual entrepreneur plans to receive the specified income.

- The tax service department number is indicated in the “provided to the tax authority” field.

- OKTMO code.

When filling out a declaration, an individual entrepreneur indicates his personal information, passport data and the amount of income that is planned to be received by the next tax period. The amount is calculated by the entrepreneur independently without providing third-party documents confirming the likelihood of receiving it.

New self-employed entrepreneurs can calculate their likely income based on the revenue received in the first month of operation.

For those individual entrepreneurs who have been working for a long time, it is advised to calculate the estimated income based on the amount indicated in the 3-NDFL report for the past tax period. This method is one of the most popular and widespread. The form indicates a smaller amount if the entrepreneur believes that the company’s income will decrease next year, and vice versa: if the income is expected to increase, it is recommended to include a larger amount in the declaration.

In addition, when filling out the declaration, it is advisable to take into account the following features:

- The tax inspector calculates advance payments only if the amount indicated in the declaration is one and a half times more or less than the amount given in form 3-NDFL.

- Calculation of advance payments based on actual income for the previous tax period is carried out if the difference between the indicators indicated in the 3-NDFL and 4-NDFL declarations is 50% up or down.

How to draw up and submit a declaration in form 4-NDFL

A declaration of estimated income in Form 4-NDFL is needed so that the tax office can determine the advance payments for personal income tax for the entrepreneur, which he must pay during the year. Until an entrepreneur has started his activities and received his first income, he is not required to submit a declaration in Form 4-NDFL.

The 4-NDFL declaration form and the procedure for filling it out were approved by order of the Federal Tax Service of Russia dated December 27, 2010 No. ММВ-7-3/768.

Who should take it?

All entrepreneurs using the general taxation system must submit a declaration of expected income in Form 4-NDFL. For newly registered entrepreneurs, such an obligation appears from the moment they receive their first income; other entrepreneurs must submit a declaration in Form 4-NDFL annually. This follows from paragraphs 1 and 7 of Article 227 of the Tax Code of the Russian Federation and letters of the Federal Tax Service of Russia dated November 14, 2006 No. 04-2-02/685, dated May 30, 2005 No. 04-2-03/72.

If an entrepreneur uses a simplified tax regime or a patent, there is no need to submit a declaration in form 4-NDFL, since this declaration is submitted only by personal income tax payers (clauses 1 and 7 of Article 227, clause 3 of Article 346.11 of the Tax Code of the Russian Federation). Accordingly, if an entrepreneur combines a patent and the general taxation system, submit a declaration in Form 4-NDFL for activities on the general taxation system.

When to take it

In the legislation, the exact deadline for submitting the declaration in form 4-NDFL is directly stated for newly registered entrepreneurs. They must submit a declaration in form 4-NDFL to the inspectorate within five working days after a month has passed from the date of receipt of the first income (clause 7 of article 227 of the Tax Code of the Russian Federation).

An example of determining the deadline for submitting a declaration in Form 4-NDFL for a newly registered entrepreneur

A.A. Ivanov was registered as an entrepreneur on January 13, 2015.

The first income from business activities was received on April 25, 2015. The one-month period expires on May 25, 2015 (Clause 5, Article 6.1 of the Tax Code of the Russian Federation). Within five working days after this date, Ivanov must submit a declaration. Thus, the deadline for submitting a declaration in form 4-NDFL to the tax office is May 27, 2015.

For entrepreneurs who have been operating for more than a year, the legislation does not specify deadlines for submitting a declaration. The Federal Tax Service of Russia recommends submitting a declaration in form 4-NDFL simultaneously with a declaration of income in form 3-NDFL for the year (letter of the Federal Tax Service of Russia dated November 14, 2006 No. 04-2-02/685). That is, until April 30 of the year following the reporting year.

Responsibility for failure to submit a declaration

Situation: can the tax office fine an entrepreneur if he filed a declaration late or did not file a declaration in Form 4-NDFL at all?

Answer: no, it cannot.

As a general rule, late filing of a tax return is an offense for which Article 119 of the Tax Code of the Russian Federation provides for liability in the form of a fine. The amount of the fine is calculated as a percentage of the unpaid amount of tax that must be paid (additionally) according to the declaration. However, if the declaration in form 4-NDFL is not submitted on time, this sanction does not apply. After all, an entrepreneur, submitting such a declaration, declares in it the amount of expected income, and not the tax to be paid or additionally paid to the budget. Therefore, there is no basis for calculating a fine in this situation, and bringing the entrepreneur to justice under Article 119 of the Tax Code of the Russian Federation is impossible.

The legality of this approach is confirmed by letters of the Federal Tax Service of Russia dated November 14, 2006 No. 04-2-02/685, dated May 30, 2005 No. 04-2-03/72, as well as arbitration practice (see, for example, the resolution of the FAS Moscow District dated May 18, 2004 No. KA-A41/2951-04).

How to calculate estimated income

To fill out a declaration in Form 4-NDFL, you must first calculate your estimated annual income. The entrepreneur decides independently how to calculate income. This is stated in paragraph 8 of Article 227 of the Tax Code of the Russian Federation.

In practice, an entrepreneur who has just started operating usually determines the amount of expected income for the year based on the revenue received during the first month of work.

An example of calculating the estimated income of a recently registered entrepreneur for filling out a declaration in form 4-NDFL

A.A. Ivanov was registered as an entrepreneur on January 17, 2015.

He received his first income from business activities on April 25, 2015. In total, Ivanov earned 110,000 rubles in April. (less expenses).

Based on this amount, the accountant calculated the estimated income for 2015, which amounted to RUB 990,000. (RUB 110,000 × 9 months).

For entrepreneurs who have been operating for more than a year, the actual income from the declaration in Form 3-NDFL for the previous year is usually indicated as the estimated income. But this is an optional rule. For example, if an entrepreneur is sure that his income this year will drop significantly, then in the declaration on Form 4-NDFL it is worth indicating a smaller amount. Then the advance payments that will need to be paid throughout the year will also decrease.

You just need to take this into account. The inspector will charge advance payments based on income from the 4-NDFL declaration only if the amount in it is at least 1.5 times more or less than the actual income according to the 3-NDFL declaration. If the difference in income between these declarations is less than 50 percent, advance payments will be calculated based on the 3-NDFL declaration for the previous year.

This conclusion can be drawn based on the letter of the Ministry of Finance of Russia dated April 1, 2008 No. 03-04-07-01/47.

Filling procedure

The declaration in form 4-NDFL has one page. Fill it out according to the rules common to all tax returns.

TIN

At the top of the form, indicate the entrepreneur’s TIN. Take it from the notice of registration as an entrepreneur, issued by the Federal Tax Service of Russia upon registration.

Correction number

If an entrepreneur submits a regular (first) declaration this year, enter “0—” in the “Adjustment number” field.

If an entrepreneur clarifies the income declared in a previously filed declaration, indicate the serial number of the adjustment (for example, “1—” if this is the first clarification, “2—” for the second clarification, etc.).

Taxable period

In the “Tax period” field, indicate the year for which the declaration is being submitted (i.e., the year in which the entrepreneur will receive the declared estimated income).

Submitted to the tax authority

In the “Submitted to the tax authority” field, enter the code of the tax office where the entrepreneur is registered. This code can be found in the notice of registration as an entrepreneur, issued upon registration.

Also, the code of the Federal Tax Service of Russia can be determined by the registration address of the entrepreneur using the Internet service on the website of the Federal Tax Service of Russia.

Taxpayer category code

In the “Taxpayer Category Code” field, write “720”. This means that the declaration is submitted by an individual entrepreneur (appendix to the Procedure approved by order of the Federal Tax Service of Russia dated December 27, 2010 No. ММВ-7-3/768).

OKTMO code

In the “OKTMO code” field, indicate the code of the territory in which the entrepreneur is registered. This code can be found in the notification of registration with Rosstat. If the entrepreneur did not receive a notification from Rosstat, the code can be determined independently using the order of Rosstandart dated June 14, 2013 No. 159-st.

If the OKTMO code contains less than 11 characters, then put dashes in the cells on the right that remain empty.

Full name and phone number

Please indicate the full last name, first name and patronymic of the entrepreneur, without abbreviations, as in your passport.

If an entrepreneur has foreign citizenship, his name and surname can be written in Latin letters (clause 2.2.7 of the Procedure approved by Order of the Federal Tax Service of Russia dated December 27, 2010 No. ММВ-7-3/768).

Write your contact phone number in full, including the city code. This can be either a landline or a mobile number. The telephone number should not contain spaces or dashes, but you can use brackets and the + sign to indicate the country code (clause 2.2.8 of the Procedure approved by Order of the Federal Tax Service of Russia dated December 27, 2010 No. ММВ-7-3/768).

Estimated income amount

Indicate the amount of expected income in line 010 in full rubles without spaces, dashes or other signs (clause 2.2.9 of the Procedure approved by Order of the Federal Tax Service of Russia dated December 27, 2010 No. ММВ-7-3/768).

An example of filling out a declaration in form 4-NDFL

A.A. Ivanov was registered as an entrepreneur on January 10, 2015.

On February 3, 2015, Ivanov began receiving income from business activities. In February 2015, income amounted to 110,000 rubles. (less expenses).

The entrepreneur's accountant calculated the estimated income for the year as follows: 110,000 rubles. × 11 months = 1,210,000 rub.

The accountant indicated this amount in the declaration on Form 4-NDFL for 2015.

How to pass

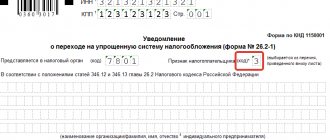

The tax return can be submitted to the inspectorate:

- on paper in person or through a representative; - on paper by post; — electronically through a specialized telecom operator or directly through the Internet service of the Federal Tax Service of Russia.

Updated declaration

If during the year an entrepreneur realizes that actual income will be more than 1.5 times less or more than that indicated in the initial 4-NDFL declaration, he is obliged to submit an updated declaration in the same form (clause 10 of Article 227 of the Tax Code of the Russian Federation).

An example of an entrepreneur submitting an updated declaration in form 4-NDFL

At the beginning of the year, entrepreneur A.A. Ivanov stated an estimated income of 2,000,000 rubles. For the first three months of the year, his actual income was only 180,000 rubles. (less expenses). At the same time, Ivanov believes that such an income level of 60,000 rubles. per month (RUB 180,000: 3 months) will remain throughout the year.

In this case, the estimated income at the end of the year will be 720,000 rubles. This is more than 1.5 times less than the initially stated amount. Therefore, Ivanov must submit an updated declaration in form 4-NDFL.

Advice: it is beneficial for an entrepreneur to submit clarifications with a smaller amount, as this will reduce the advance payments that the tax office will calculate on the basis of the clarified 4-NDFL declaration.

Fill out the updated declaration in form 4-NDFL in the same order as the initial declaration. Only in the “Adjustment number” field put the serial number of the clarification (for example, “1—” if this is the first clarified declaration).

The deadline for submitting an updated declaration is not established by law. However, it is worth taking into account that the inspection recalculates the advance payment within five working days after receiving the updated declaration (clause 10 of article 227, clause 6 of article 6.1 of the Tax Code of the Russian Federation). In this case, the inspectorate sends notifications for advance payments 30 working days before the date of payment (paragraph 2, paragraph 2, article 52, paragraph 6, article 6.1 of the Tax Code of the Russian Federation). Therefore, in order for the new advance payment to be calculated based on the adjusted income, the declaration must be received by the inspectorate 35 working days before the date of its payment.

For example, in order for the inspectorate to indicate the adjusted amount in the notification for payment of the advance payment, which is due on October 15, 2015, the updated declaration must be submitted no later than August 27, 2015.

How to submit a 4-NDFL declaration

A 4-NDFL declaration can be submitted to the Federal Tax Service in one of three ways:

- By an individual entrepreneur personally or through a representative in paper form in two copies. One of them remains with the individual entrepreneur, the second is transferred to the tax office.

- Via mail with a description of the attachment. The entrepreneur has a receipt and an inventory of the investment in his hands. The date of submission of the declaration will be considered the date indicated on the receipt.

- In electronic form through EDF operators or the official website of the Federal Tax Service of Russia.

If the declaration is submitted by an individual entrepreneur through a representative, then a notarized power of attorney is issued to the latter.

Some tax office branches, when submitting a declaration in paper form, require its equivalent in electronic form indicating a barcode. The Tax Code of the Russian Federation does not specify such requirements, however, the inspector may refuse to accept documents for this reason. You can always appeal a refusal to a higher authority of the Federal Tax Service.

Draft order to abolish 4-NDFL

And now, news for those who must fill out form 4-NDFL.

A draft document on the cancellation of the order of the Federal Tax Service, which approved the 4-NDFL declaration, has been published on the federal portal.

How will we calculate tax after the abolition of 4-NDFL?

According to the rules prescribed in the new edition of paragraphs 7 and 8 of Art. 227 of the Tax Code of the Russian Federation, for those working at OSNO it will be necessary to independently calculate advance payments based on the results of the quarter, half a year and nine months. Advance payments will be calculated based on:

- tax rates;

- actual income received;

- professional and standard tax deductions;

- previously calculated advance payments.

The deadlines for making advance payments are April 25, July 25 and October 25.

This is a new edition of clauses 7 and 8 of Art. 227 of the Tax Code of the Russian Federation, and clauses 9 and 10 lost force (clause 7 of Article 1 of the Law of April 15, 2019 No. 63-FZ was introduced).

Sanctions for failure to submit a declaration

Individual entrepreneurs are obliged by the Tax Code and the Federal Law of the Russian Federation to submit a declaration in form 4-NDFL within the time limits established by law to the local tax inspectorate. Despite the exact deadlines for delivery, violators do not face any liability in the form of penalties. This is explained by the fact that business entities in this reporting form do not indicate data on the income received during the tax period and tax liabilities, since only probable values of income are entered into Form 4-NDFL. In this regard, the maximum fine for an individual entrepreneur who has not submitted a declaration or has overdue the deadline for submitting it is 200 rubles.

The form is submitted within five days after the end of the month in which the individual entrepreneur received income from his activities. The declaration indicates the income expected to be received for the subsequent tax period. The amount of income and, accordingly, probable tax is calculated by the individual entrepreneur independently based on the efficiency of his business.

Form 4-NDFL from 2021: form

The 4-NDFL report is a one-page document that reflects the following information:

- TIN of the entrepreneur;

- Correction number (primary – 0, clarifying the order of the number series – 1, 2, etc.);

- Federal Tax Service code at the place of residence of the individual entrepreneur;

- The period for which the planned income is reflected;

- Payer code – the category to which it belongs. For example, the code for individual entrepreneurs is 720, for private practitioners - 730, for lawyers who have established their own office - 740;

- OKTMO code, i.e. the code of the territory where the entrepreneur operates;

- Full name of the entrepreneur;

- His phone number;

- The amount of expected income for the year;

- If supporting documents are available, fill in the field for the number of application sheets;

- Confirmation of the accuracy of the information is carried out in the section located in the lower right corner of the form. When submitting a declaration by the taxpayer himself, code 1 is entered in the designated field, the full name lines are not filled in, the filing date is indicated and the form is signed by the individual entrepreneur. When certifying the authenticity of information, the businessman’s representative enters code 2, his full last name, first name and patronymic are recorded in the full name field, and below is the name of the document giving him the authority to represent the payer. If the representative of the declarant is an enterprise, then the full name field reflects the full name of the representative for whom the power of attorney is issued, and in the line “Name of organization” the name of the company is recorded and certified by its seal and signature of the authorized representative.

Read also: New form 4-NDFL – 2019