Report 6 personal income tax, when and how to submit

Personal income tax is a tax on personal income, which is withheld from such income as::

- When selling your property if it was owned for less than the required period

- When renting out your own property

- Winnings from the lottery or various competitions

- From salary

No tax is paid on:

- If a close relative gave or inherited any property

Even if a company is an intermediary, for example, it hires employees to work in another company, it will be considered a tax agent and is obliged to remit personal income tax on wages.

Report 6 Personal Income Tax is submitted by legal entities and individual entrepreneurs who have employees who receive wages. This report form is compiled quarterly on an accrual basis and submitted electronically in the month following the reporting month no later than the last day.

Important! If the report submission date falls on a weekend, it is submitted on the first working day.

The report itself consists of a title page and two sections.

- The first section reflects the amounts as a cumulative total of generalized indicators

- The second section contains the dates and amounts when the income was actually received and transferred, as well as the tax itself was paid

It is worth remembering that if an enterprise has separate divisions that have their own checkpoint, this type of report is submitted for each separate division separately, each to its own district where the structural division is registered.

What does the line show?

Line 060 of the calculation indicates the number of employees who received income subject to personal income tax (usually a rate of 13%) in the period under review. Moreover, this indicator is not adjusted in the event of re-hiring or dismissal of individuals. Filling out is carried out on the basis of information from the tax accounting register.

Also see “Tax register for 6-NDFL”.

A similar requirement is provided for when cooperation has repeatedly taken place on the basis of a civil law agreement.

Instructions for filling in general terms

- Cells must be filled in from left to right according to generally accepted rules;

- Cells that cannot be filled in are crossed out

- If you provide a report on paper, each section is printed on a separate sheet; double-sided printing is prohibited in this case

- For manual filling, you can use black, purple or blue ink;

- If the report is submitted on a computer, you must use Courier New font with a height of 16 - 18 points.

6-NDFL: filling out lines

When preparing Form 6-NDFL, questions may arise regarding filling out individual lines of the Calculation of the amounts of personal income tax calculated and withheld by the tax agent (approved by Order of the Federal Tax Service dated October 14, 2015 No. ММВ-7-11 / [email protected] ). We will tell you how to correctly fill out each of the lines of Section 1 “Generalized indicators” and Section 2 “Dates and amounts of actual income received and withheld personal income tax” in our consultation.

Line 010

Line 010 “Tax rate, %” indicates the personal income tax rate at which the tax agent assessed the income of individuals in the reporting period. Accordingly, how many tax rates were applied during the period of compilation of the Calculation, so much will be Section 1 in form 6-NDFL. In this case, lines 020-050 are filled in with a cumulative total in relation to a specific rate reflected on line 010.

Line 020

Line 020 “Amount of accrued income” indicates the amount of accrued income on an accrual basis from the beginning of the year, taxed at a certain personal income tax rate.

Line 025

Line 025 “Including the amount of accrued income in the form of dividends” must be completed if the tax agent paid dividends to individuals during the reporting period.

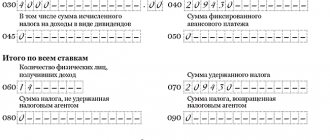

Line 030

Line 030 “Amount of tax deductions” reflects the amount of tax deductions that were provided to individuals in the reporting period. The list of tax deductions for line 030 can be found in Order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/ [email protected] . The amount of tax deductions reduces the income subject to tax. Moreover, if for any individual the amount of deductions exceeds the income accrued to him, the deduction will be reflected only in the amount of income.

Line 040

On line 040 “Amount of calculated tax” you need to show the amount of personal income tax calculated from income from line 020, which was reduced by tax deductions on line 030.

Line 045

If the tax agent reflected dividends on line 025, then separately on line 045 “Including the amount of calculated tax on income in the form of dividends” you must indicate the amount of personal income tax on these dividends.

Line 050

If a tax agent employs “patent” foreigners who independently pay personal income tax, line 050 “Amount of fixed advance payment” will show the amount of fixed payments they have made for personal income tax, by which the tax agent reduces the tax on their income.

Line 060

Line 060 “Number of individuals who received income” shows the total number of individuals who received income from the tax agent in the reporting period. Moreover, if a tax agent fired and rehired the same person during the year, it will be shown on line 060 only once.

Line 070

On line 070 “Amount of tax withheld” you need to reflect the amount of personal income tax withheld by the tax agent.

Line 080

Line 080 “Amount of tax not withheld by the tax agent” will be filled in if the tax agent has declared it impossible to withhold the tax (clause 5 of Article 226, clause 14 of Article 226.1 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service dated July 19, 2016 No. BS- 4-11/ [email protected] ). For example, a tax agent gave a person income in kind, but could not withhold personal income tax, because The taxpayer had no income in cash.

Line 090

On line 090 “Amount of tax returned by the tax agent” you need to show the amount that the tax agent returned to the personal income tax payer (Letter of the Federal Tax Service dated July 18, 2016 No. BS-4-11 / [email protected] ).

Line 100

Line 100 “Date of actual receipt of income” of Section 2 is filled out in accordance with Art. 223 Tax Code of the Russian Federation. So, for example, the date of receipt of income in the form of wages will be the last day of the month for which this income was accrued, and for income in the form of material benefits received from savings on interest when receiving borrowed funds - the last day of each month during the term , for which borrowed funds were provided.

Line 110

Line 110 “Date of tax withholding” indicates the date of actual payment of income, because tax agents are required to withhold the calculated amount of personal income tax directly from the taxpayer’s income upon their actual payment (paragraph 1, clause 4, article 226 of the Tax Code of the Russian Federation). In the case of issuing income in kind, as well as when receiving income in the form of material benefits, the tax agent must withhold personal income tax at the expense of any income paid in cash (paragraph 2, paragraph 4, article 226 of the Tax Code of the Russian Federation).

Line 120

Line 120 “Tax transfer deadline” indicates the date no later than which the personal income tax amount must be transferred to the budget. And this is the day following the day of payment of income (paragraph 1, clause 6, article 226 of the Tax Code of the Russian Federation). An exception applies to temporary disability benefits and vacation pay: personal income tax from them is transferred no later than the last day of the month in which such payments were made (paragraph 2, clause 6, article 226 of the Tax Code of the Russian Federation). In this case, on line 120 you only need to indicate a working day. This means that if the day following the day of payment of income, or the last day of the month (for vacation pay and sick leave) is a day off, then the following working day is indicated as the deadline for tax transfer (Clause 7, Article 6.1 of the Tax Code of the Russian Federation, Letter Federal Tax Service dated May 16, 2016 No. BS-4-11/ [email protected] ).

You can read more about filling out lines 100-120 of Calculation 6-NDFL in our separate consultation.

Line 130

Line 130 “Amount of income actually received” shows the total amount of income of individuals (including personal income tax) received on the date indicated on line 100.

Line 140

Line 140 “Amount of tax withheld” reflects the amount of tax withheld on the date indicated on line 110.

Please note that lines 100-140 are filled in in total for all personal income tax rates applied in the reporting period. Moreover, if the dates of actual receipt of income, tax withholding and the deadline for transferring personal income tax (lines 100-120) coincide in relation to different incomes, then such income and the amount of tax withheld on them in lines 130-140 are reflected in a collapsed manner.

Section 1, line 060 to fill out

To fill out the first section of 6NDFL at different rates, for example, foreign citizens worked for an employer whose tax rate is 30%, then lines 010-050 must be filled out for each rate separately. Income is summed up for all people, at this rate.

| Line, numbering | What is indicated |

| 010 | We set the tax rate that was used to calculate the tax |

| 020-050 | Based on the applied rate, these lines are filled in |

| 020-050 | Based on the applied rate, these lines are filled in. Line 020 real amount of accrued income, wages or other income received |

| 030 | This reflects the amount of tax deductions based on the number of children. In order for the accountant to give these deductions, you must provide the child’s birth certificate or a certificate from the educational institution stating that he is a full-time student. |

| 040 | Amount of calculated tax |

| 050 | The amount by which the tax agent reduces the calculated personal income tax |

| 060 | Number of employees who received income |

| 070 | Amount of tax withheld by the tax agent |

| 080 | The amount of tax that for any reason was not withheld by the agent |

| 090 | Tax refund to an individual |

Important! Line 060 tells us how many people received income in this quarter, and if in the same reporting period an employee quit and started working again, he is counted as one employee.

Lines 060-090 in the first section are filled in with a cumulative total, taking into account previous quarters.

Line 060 in 6-NDFL - is it filled out on an accrual basis or not?

The periods for submitting the 6-NDFL calculation are:

- first quarter,

- half a year

- 9 months,

- year.

It is for these periods that Section 1 is filled out. Since the half-year includes data from the first quarter, and the year includes data from the first quarter, half-year and 9 months, it can be understood that all indicators in this section are entered incrementally from one presentation period to another. Hence the conclusion: line 060, like other lines of section 1, is filled in with a cumulative total from the beginning of the year.

Section 2 includes data only from the last quarter included in the reporting period. Information for other quarters cannot be included in it. That is, in the report submitted for 9 months of 2019, section 2 will include information for July, August, and September of the corresponding year.

For information on how to fill out other lines of form 6-NDFL, read the materials:

- “Line 140 in form 6-NDFL - accrued or payment”;

- “Filling out line 030 in form 6-NDFL, what is included there”;

- “Line 080 in form 6-NDFL when filled out”;

- “Filling out line 070 in form 6-NDFL, what is included there”;

- “When line 090 is filled out in form 6-NDFL”;

- “Filling out line 040 in form 6-NDFL, what is included there”;

- “Filling out line 020 in form 6-NDFL, what is included there.”

Section 2 of report 6 personal income tax

In this section it is necessary to reflect by date:

- When did the employee actually receive income;

- The date of personal income tax withholding from him;

- deadlines for transferring personal income tax;

- the amount of income actually received;

- amount of personal income tax withheld.

| Line | Decoding |

| 100 line | Date of actual receipt of income |

| 110 | When should tax be withheld? |

| 120 | Date of personal income tax transfer |

| 130 | Amount of income |

| 140 | Withholding tax |

Important! If two individuals have the same dates for the actual transfer, withholding and calculation of tax, then they are formed into one amount in the report in blocks 100-140.

On line 100, you must indicate the specific date of receipt of income; for wages, it is considered the last day of the month for which this income was received.

Sick leave is reflected on the date when the money is paid.

Please note that in the calculation for the 1st quarter you may encounter December wages, which were paid in January 2021, as well as March wages, which will be paid in April 2021. In this case, the December salary is reflected only in section 2 of the Calculation, and the March salary - only in section 1. In section 2, the salary for March, paid in April, will be shown only in the report for the half-year of 2021.

Formation of line 060

Line 060 is in section 1 of the report. In addition to the general principles of formation outlined above, the following nuances should be taken into account:

- Line 060 contains general information about the number of those who received taxable payments from the enterprise. Based on the territorial principle of filling, if in the past period an individual worked and received money in several structural divisions of one enterprise and these divisions are recognized as separate, such a person will be included in the report for all divisions.

- In the case where one individual counterparty received income from one enterprise (division) under several different contracts, for the purposes of generating a report on line 060, such an individual is considered as 1 person.

- In a situation where the same individual counterparty received income from one enterprise at several personal income tax rates, for the purposes of filling out line 060 such an individual is considered as 1 person.

- If events in one tax period developed in such a way that an individual was first fired and then rehired at the same enterprise (in the same division), the information in line 060 in 6-NDFL for this individual does not change.

Example

According to the results of the 1st quarter of 20XX, 20 people were indicated in the 6-NDFL of Cafe-1 LLC on line 060. In May, a separate division “Cafe-1/2” began operating, where 4 employees transferred from “Cafe-1” and 6 more new employees were hired. Payment of salaries to those working in “Cafe-1/2” is made directly to “Cafe-1/2” from the proceeds. 2 employees of Cafe-1 quit in May, while 1 of them took a job at Cafe-1 again in June. In connection with the expansion of the business, Cafe-1 also hired 3 new employees in May-June. What will the 6-NDFL report look like for the 1st half of 20XX (considering line 060)?

- There will be 2 6-NDFL reports - for “Cafe-1” and “Cafe-1/2”.

See details here: “6-NDFL: there must be a separate calculation for each division.”

- Line 060 “Cafe-1” will indicate 20 + 3 = 23 people (4 employees who transferred to “Cafe-1/2” in May received their salaries for January-April back in “Cafe-1”, so they are included in the calculation ; 1 employee who quit in May also received wages for January-April and the May calculation; 1 employee who quit and returned does not affect the calculation).

- Line 060 “Cafe-1/2” will indicate 4 + 6 = 10 people (4 who transferred from “Cafe-1” and received salaries in May and June and 6 new ones who arrived in May).

Responsibility for failure to submit 6NDFL to the tax office

There is no need to submit a blank personal income tax form if the legal entity did not accrue or pay income during this period.

If there was at least one payment, be it sick leave, vacation pay, which led to the fact of transferring personal income tax, the report must be submitted in any case.

The fines for failure to submit 6NDFL on time are not large, but still.

If the violation is for the first time and up to a month has passed, then the fine will be 1000 rubles, if longer, then another 1000. A fine of 300-500 rubles may be imposed on the director.

Important! If personal income tax is not paid on time, the tax office has the right to block the taxpayer’s current accounts and impose penalties. The bank will receive a notification that the required amount has been blocked; now, as a rule, not the entire account is blocked, but only within the limits of what needs to be paid.

For untimely transfer of tax to the budget, for failure to pay penalties, for failure to submit reports, the tax agent is held accountable and penalties may be imposed on him. Depending on the violation, the following types of punishment are provided:

| Violation | Amount of fine |

| For one tax period | 10,000 rubles |

| More than one period | 20 000 |

| Understatement of tax | 20% of the underpaid amount, but not less than 40,000 |

Important! For more serious violations regarding non-payment, the employer may be held administratively liable, as well as suspended from his position for a certain time.

How to fill

The procedure for completing line 060 is regulated by Tax Service Order No. ММВ-7-11/450. It is located in the calculation part of the first section of 6-NDFL. The cumulative total of the number of individuals who received income is actually relevant for line 060.

When receipts to a taxpayer in a reporting period are taxed at different rates, each contribution is reflected separately in the appropriate part of the calculation. However, according to line 060, an individual appears once: on the first page, regardless of the number of attached sheets. The corresponding number is entered in this column, and the remaining cells are left empty.

Also see “Filling out Section 1 in 6-NDFL”.

EXAMPLE submits personal income tax reports for 9 months of 2016. At the same time, according to line 060 for the first quarter. 13 employees were announced. Of them:

- 6 people are permanent employees;

- 3 people were fired in July;

- 4 people were hired in September, among them one was rehired.

How to reflect in 6-NDFL the number of individuals for whom information must be submitted?

Solution The calculation does not take into account an employee who was fired and rehired. Therefore, the number of people that needs to be shown in the reporting will be:

Tax reporting 6-NDFL with the number of individuals must be submitted to the tax office in a timely manner. If deadlines are violated or data on the number of employees is incorrectly filled out, inspectors may raise questions. Therefore, be careful when filling out line 060.

Read also

05.09.2016

6-NDFL: filling out lines

When preparing Form 6-NDFL, questions may arise regarding filling out individual lines of the Calculation of the amounts of personal income tax calculated and withheld by the tax agent (approved by Order of the Federal Tax Service dated October 14, 2015 No. ММВ-7-11 / [email protected] ). We will tell you how to correctly fill out each of the lines of Section 1 “Generalized indicators” and Section 2 “Dates and amounts of actual income received and withheld personal income tax” in our consultation.

Line 010

Line 010 “Tax rate, %” indicates the personal income tax rate at which the tax agent assessed the income of individuals in the reporting period. Accordingly, how many tax rates were applied during the period of compilation of the Calculation, so much will be Section 1 in form 6-NDFL. In this case, lines 020-050 are filled in with a cumulative total in relation to a specific rate reflected on line 010.

Line 020

Line 020 “Amount of accrued income” indicates the amount of accrued income on an accrual basis from the beginning of the year, taxed at a certain personal income tax rate.

Line 025

Line 025 “Including the amount of accrued income in the form of dividends” must be completed if the tax agent paid dividends to individuals during the reporting period.

Line 030

Line 030 “Amount of tax deductions” reflects the amount of tax deductions that were provided to individuals in the reporting period. The list of tax deductions for line 030 can be found in Order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/ [email protected] . The amount of tax deductions reduces the income subject to tax. Moreover, if for any individual the amount of deductions exceeds the income accrued to him, the deduction will be reflected only in the amount of income.

Line 040

On line 040 “Amount of calculated tax” you need to show the amount of personal income tax calculated from income from line 020, which was reduced by tax deductions on line 030.

Line 045

If the tax agent reflected dividends on line 025, then separately on line 045 “Including the amount of calculated tax on income in the form of dividends” you must indicate the amount of personal income tax on these dividends.

Line 050

If a tax agent employs “patent” foreigners who independently pay personal income tax, line 050 “Amount of fixed advance payment” will show the amount of fixed payments they have made for personal income tax, by which the tax agent reduces the tax on their income.

Line 060

Line 060 “Number of individuals who received income” shows the total number of individuals who received income from the tax agent in the reporting period. Moreover, if a tax agent fired and rehired the same person during the year, it will be shown on line 060 only once.

Line 070

On line 070 “Amount of tax withheld” you need to reflect the amount of personal income tax withheld by the tax agent.

Line 080

Line 080 “Amount of tax not withheld by the tax agent” will be filled in if the tax agent has declared it impossible to withhold the tax (clause 5 of Article 226, clause 14 of Article 226.1 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service dated July 19, 2016 No. BS- 4-11/ [email protected] ). For example, a tax agent gave a person income in kind, but could not withhold personal income tax, because The taxpayer had no income in cash.

Line 090

On line 090 “Amount of tax returned by the tax agent” you need to show the amount that the tax agent returned to the personal income tax payer (Letter of the Federal Tax Service dated July 18, 2016 No. BS-4-11 / [email protected] ).

Line 100

Line 100 “Date of actual receipt of income” of Section 2 is filled out in accordance with Art. 223 Tax Code of the Russian Federation. So, for example, the date of receipt of income in the form of wages will be the last day of the month for which this income was accrued, and for income in the form of material benefits received from savings on interest when receiving borrowed funds - the last day of each month during the term , for which borrowed funds were provided.

Line 110

Line 110 “Date of tax withholding” indicates the date of actual payment of income, because tax agents are required to withhold the calculated amount of personal income tax directly from the taxpayer’s income upon their actual payment (paragraph 1, clause 4, article 226 of the Tax Code of the Russian Federation). In the case of issuing income in kind, as well as when receiving income in the form of material benefits, the tax agent must withhold personal income tax at the expense of any income paid in cash (paragraph 2, paragraph 4, article 226 of the Tax Code of the Russian Federation).

Line 120

Line 120 “Tax transfer deadline” indicates the date no later than which the personal income tax amount must be transferred to the budget. And this is the day following the day of payment of income (paragraph 1, clause 6, article 226 of the Tax Code of the Russian Federation). An exception applies to temporary disability benefits and vacation pay: personal income tax from them is transferred no later than the last day of the month in which such payments were made (paragraph 2, clause 6, article 226 of the Tax Code of the Russian Federation). In this case, on line 120 you only need to indicate a working day. This means that if the day following the day of payment of income, or the last day of the month (for vacation pay and sick leave) is a day off, then the following working day is indicated as the deadline for tax transfer (Clause 7, Article 6.1 of the Tax Code of the Russian Federation, Letter Federal Tax Service dated May 16, 2016 No. BS-4-11/ [email protected] ).

You can read more about filling out lines 100-120 of Calculation 6-NDFL in our separate consultation.

Line 130

Line 130 “Amount of income actually received” shows the total amount of income of individuals (including personal income tax) received on the date indicated on line 100.