Who is the tax agent for personal income tax?

The following persons are recognized as tax agents for personal income tax (clause 1 of Article 226 of the Tax Code of the Russian Federation):

- Russian organizations;

- individual entrepreneurs;

- notaries and lawyers engaged in private practice or having law offices;

- separate divisions of foreign companies.

The tax base for personal income tax is payments to taxpayers at the expense of a tax agent (clause 9 of Article 226 of the Tax Code of the Russian Federation, letters of the Federal Tax Service of the Russian Federation dated 02/06/2017 No. GD-4-8/ [email protected] , Ministry of Finance dated 12/15/2017 No. 03-04 -06/84250).

If a company hires personnel under an employee supply agreement, then the functions of a tax agent for personal income tax remain with the executing organization, since it is the organization that makes direct payments to individuals under employment contracts (letter of the Ministry of Finance of Russia dated November 6, 2008 No. 03-03-06/8/618 ).

Individuals who are not registered as individual entrepreneurs who make payments in favor of individuals who are employees are not recognized as tax agents. In this case, recipients of funds must independently calculate and pay personal income tax (letter of the Ministry of Finance of Russia dated July 13, 2010 No. 03-04-05/3-390).

The list of income subject to personal income tax is presented in Art. 208 Tax Code of the Russian Federation.

Read more about the features of calculating and withholding income tax in the article “Calculation of personal income tax (personal income tax): procedure and formula.”

Tax agent when paying dividends

A Russian organization acts as a tax agent for income tax if it pays dividends to a Russian or foreign company.

One of the features of recognizing a Russian organization-issuer as a tax agent is how dividends are paid. If they are paid directly through the issuer, he is obliged to calculate, withhold and transfer the tax amount to the budget. If dividends are paid through certain intermediaries (for example, through depositories), in this case the obligation to act as a tax agent for income tax in accordance with Russian legislation rests with the specified intermediary.

Separately, we should talk about those business entities that apply special tax regimes in their activities. For such organizations, the obligation to act as a tax agent remains, even despite the fact that they are not payers of income tax.

It should also be noted that when organizations receiving dividends apply special tax regimes, the income tax agent remains obligated to pay tax. Thus, if the recipient of dividends uses the simplified tax system or the unified agricultural tax system, the dividends for him will be income subject to income tax in accordance with the provisions of clause 3 of Art. 346.1 and paragraph 2 of Art. 346.11 Tax Code of the Russian Federation.

This rule also applies to organizations using UTII. For them, the dividends received will be income not related to activities that, according to Russian legislation, are subject to UTII, therefore, in this case, it is also necessary to pay income tax on such income. The corresponding clarifications are contained in the letter of the Ministry of Finance of Russia dated May 16, 2005 No. 03-03-02-04/1/121.

However, there are exceptions to this rule. The obligation to calculate and pay tax if organizations receiving dividends apply special tax regimes does not arise for the tax agent in the following cases:

- when paying dividends on shares or shares in them owned by the state or municipality (opinion of the Ministry of Finance of Russia, reflected in letter dated August 30, 2012 No. 03-03-06/4/91);

- when paying dividends to mutual investment funds, the management of which is transferred to management companies (the position of specialists from the Ministry of Finance of Russia, reflected in letter dated November 13, 2010 No. 03-03-06/1/717);

- when paying dividends on shares owned by Vnesheconombank (clarifications of the Ministry of Finance of Russia, set out in letter dated February 22, 2008 No. 03-03-06/2/17).

Interesting information about tax agents can be gleaned from the articles “Features of calculating dividends for calculating income tax” and “Capitalization of interest does not relieve the agent of the obligation to pay income tax”.

Responsibilities of a tax agent – Article 230 of the Tax Code of the Russian Federation

Tax legislation establishes what a personal income tax agent must do. Article number 230 of the Tax Code of the Russian Federation contains a small but comprehensive list from which the responsibilities of a tax agent for personal income tax are visible:

- calculate tax on payments to individuals;

- withhold tax;

- transfer tax amounts to the budget;

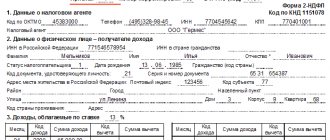

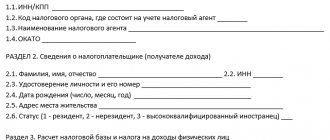

- within the prescribed period, report on the calculated, withheld and transferred to the budget income tax in forms 2-NDFL and 6-NDFL.

It is important to perform all the above operations correctly and within the time limit established in the Tax Code of the Russian Federation. ConsultantPlus experts explained in detail how to do this. Full trial access to K+ is available for free. This ready-made solution will help you correctly calculate personal income tax, this material will tell you about the procedure for withholding personal income tax, and this instruction will introduce you to the nuances of transferring personal income tax to the budget.

To fulfill his duties, a tax agent must be able to withhold tax. Payment of tax amounts must be made exclusively on payments to individuals. A tax agent has no right to pay taxes from his own funds. It is also prohibited to include clauses on the payment of tax amounts at the expense of the tax agent for personal income tax in the terms of an employment or civil contract (clause 9 of Article 226 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of Russia dated July 11, 2017 No. 03-04-06/43981, dated August 30 .2012 No. 03-04-06/9-263). It is also impossible to shift the payment of personal income tax from the agent to the taxpayer himself.

However, the Supreme Court believes that it is impossible to punish a taxpayer for early payment of income tax (see resolution No. 305-KG17-15396 dated December 21, 2017).

The Ministry of Finance allowed the overpayment of personal income tax to be counted against future payments for this tax, but with restrictions. Read more here.

Also, starting from 2021, the tax agent has the right to pay personal income tax from his own funds in the case where the tax was additionally assessed during the audit. See here for details.

What are the responsibilities?

The list of what tax agents are required to do is given in paragraphs 3 of Article 24 of the Tax Code of the Russian Federation. These include:

- timely and correct calculation and withholding of fiscal fees from funds paid to the taxpayer;

- transfer of withheld amounts to the budget of the Russian Federation within the time limits established by law;

- notification to the Federal Tax Service about the impossibility of withholding tax;

- submission of reports necessary for control to the Federal Tax Service;

- accounting of calculated, withheld and transferred taxes for each taxpayer;

- ensuring the safety of documents necessary to verify the correctness of calculation and deduction of fiscal payments.

Also, the Tax Code of the Russian Federation may provide for other obligations for certain types of taxes. For example, not only the Federal Tax Service must be notified about the impossibility of withholding personal income tax, but also the taxpayer himself.

Responsibility of the tax agent – penalties and fines for non-payment

The duties of the tax agent for personal income tax regarding the transfer of tax amounts may not be fulfilled or partially fulfilled. Such situations often arise if the income is paid in kind or represents a material benefit received by an individual.

Read about the duties of a tax agent when paying an employee income in kind in the material “Did the individual receive income in kind? Perform the duties of a tax agent .

Here it is necessary to deduct money payments due to the person himself or to a third party on behalf of the recipient of the income. The amount of withholding corresponds to the amount of the payment arrears and the newly accrued tax, if any (paragraph 2, paragraph 4, article 226 of the Tax Code of the Russian Federation).

If payments to the debtor under personal income tax will no longer be made or the amount of payments is not enough to cover the debt, the tax agent for personal income tax is obliged to notify the tax authorities and the taxpayer about this. This should be done before March 1 after the end of the tax period (subclause 2, clause 3, article 24, clause 5, article 226 of the Tax Code of the Russian Federation). Sending a message relieves the agent of the obligation to withhold personal income tax amounts from this person. The obligation to pay tax will arise on the taxpayer himself upon receipt of a tax notice from the Federal Tax Service.

It is also noted that if the tax agent did not report the impossibility of withholding personal income tax to either the tax service or the taxpayer or did not lose such an opportunity, then penalties may be assessed on the amount of arrears to the personal income tax agent based on the results of an on-site tax audit (letter from the Federal Tax Service of Russia dated November 22, 2013 No. BS-4-11/20951 and No. SA-4-7/16692 dated August 22, 2014). A message about the impossibility of withholding tax must be sent even if the deadline for its submission is missed (letter of the Federal Tax Service of Russia dated July 16, 2012 No. ED-4-3 / [email protected] ). To submit the message, form 2-NDFL with sign 2 is used.

For a life hack from the specialists of our website, see the material “[LIFE HACK] Checking whether you need to submit a 2-NDFL with sign 2.”

In addition to penalties, tax authorities have the right to impose a fine for non-payment of personal income tax by a tax agent.

For more information about the responsibility of this category of taxpayers and when a fine is imposed for non-payment of personal income tax by a tax agent, read the article “What liability is provided for non-payment of personal income tax”.

But a fine can be avoided if:

1. 6-NDFL was submitted to the Federal Tax Service without delay;

2. The amount of personal income tax is correctly indicated in the form (without underestimation);

3. The tax and penalties are paid before the tax authorities find out about the non-payment.

Such rules are in force from January 28, 2019 and apply to legal relations that arose before this date. We talked about the details here.

Also find out about the innovations when imposing fines on tax agents in 2021.

Tax agents: their rights and obligations

A tax agent pays taxes for other persons, and not for himself, and he has exactly the same rights as a taxpayer, unless tax legislation provides otherwise (Article 24 of the Tax Code of the Russian Federation).

The rights of tax agents are ensured in accordance with Art. 21 and 22 of the Tax Code of the Russian Federation, according to which they, in particular, can:

- receive information from the Federal Tax Service Inspectorate about taxes, fees, current regulations on taxation, tax reporting forms, etc., and from the Ministry of Finance of the Russian Federation and regional authorities - clarifications on emerging issues of application of tax legislation,

- take advantage of tax benefits if available,

- receive a deferment, installment plan, investment tax credit, if there are grounds for this,

- timely receive credit/refund of overpayments on taxes (penalties, fines),

- carry out reconciliation with tax authorities, receive reconciliation reports from the Federal Tax Service,

- provide explanations to the Federal Tax Service on accrued/paid taxes, as well as on tax audit reports,

- be personally present during an on-site tax audit, receive copies of audit reports and decisions of tax authorities, tax requirements and notifications,

- not to comply with unlawful demands of tax authorities, and also to appeal acts of the Federal Tax Service.

The main responsibilities assigned to tax agents of the Tax Code of the Russian Federation are the correct and timely calculation, withholding and transfer of tax for the taxpayer. In addition, the tax agent is obliged (Article 24 of the Tax Code of the Russian Federation):

- inform the Federal Tax Service Inspectorate in writing about the amount of tax debt of the taxpayer that cannot be withheld from him - this must be done within a month,

- keep records for each taxpayer of income accrued and paid to him, taxes withheld from him,

- submit documents to tax authorities that allow you to control the correctness of tax calculations,

- keep documents required for the calculation, withholding, and transfer of taxes for at least 4 years.

The above list is not exhaustive, since everyone who is a tax agent is also subject to other requirements stipulated by tax legislation: the duties of tax agents for VAT reporting are provided for in clause 5 of Art. 174 of the Tax Code of the Russian Federation, features of personal income tax withholding by agents - Art. 226 of the Tax Code of the Russian Federation, etc.

KBK for transferring tax amounts

In 2020-2021, the following personal income tax codes are in effect (orders of the Ministry of Finance of Russia dated November 29, 2019 No. 207n, dated June 8, 2020 No. 99n):

- 182 1 0100 110 - code for transferring personal income tax on income paid by a tax agent to a taxpayer. The exception is income received in accordance with Art. 227, 227.1, 228 Tax Code of the Russian Federation.

- 182 1 0100 110 - code for transferring personal income tax received by an individual - an individual entrepreneur, a notary or lawyer or a person carrying out other business activities under Art. 227 Tax Code of the Russian Federation.

- 182 1 0100 110 - transfer of tax on personal income received under Art. 228 Tax Code of the Russian Federation.

- 182 1 0100 110 - code for transferring tax on the income of foreign citizens carrying out activities in accordance with the patent. The personal income tax payment in this case is a fixed advance payment and is made on the basis of Art. 227.1 Tax Code of the Russian Federation.

The nuances of paying personal income tax can be found in the section “Time limits and procedures for paying personal income tax.”

Income tax

An organization becomes a tax agent for this tax if it pays:

- dividends from another organization;

- interest on state (municipal) securities to other organizations;

- income of a foreign organization from the sale or rental of real estate on the territory of the Russian Federation, from international transportation. A Russian organization has this obligation if the recipient of the income does not have a representative office in the Russian Federation.

The company must notify the Federal Tax Service about the paid income and withheld tax by submitting:

- income tax return - when paying dividends or interest to a Russian organization;

- tax calculation (Order of the Federal Tax Service dated March 2, 2016 No. ММВ-7-3/ [email protected] ) - when paying income to a foreign organization.

How to make a refund of overpaid personal income tax by a tax agent?

If a tax agent overpaid personal income tax, then he, in fact, reduced the income of an individual by such action. The injured employee has the right to apply to the employer for a refund of the overpaid amount of tax. Tax legislation in paragraph 7 of Art. 78 of the Tax Code of the Russian Federation determines that the statute of limitations for such cases is 3 years, during which a statement can be written.

After receiving a written request from the employee, the tax agent writes a statement to his Federal Tax Service and attaches documents that can confirm the fact of the overpayment. The tax authorities will make a decision within 10 days and inform the employer about it. The tax agent is given the right to choose one of two ways to repay the debt:

- Offset the overpayment against future personal income tax payments.

- Transfer the identified amount of overpayment to the taxpayer's account.

If it is not possible to return the tax through the employer, the taxpayer has the right to apply for a tax refund directly to the Federal Tax Service. How to draw up an application for a personal income tax refund in this case, see our article.

Tax agents. Tax agent violations

Vitaly Semenikhin,

Head of the Semenikhin Expert Bureau Tax agents occupy a special place in tax obligations, performing control and accumulating functions, as well as being a connecting link between the taxpayer and the state in cases specified by law.

For failure to fulfill (improper performance) of his duties, the tax agent is liable in accordance with the legislation of the Russian Federation. Read about the violations committed by tax agents and the liability provided for them in the material presented. Tax agents in accordance with clause 1 of Art. 24 of the Tax Code of the Russian Federation recognizes persons who, in accordance with the Tax Code of the Russian Federation, are entrusted with the duties of calculating, withholding from the taxpayer and transferring taxes to the budget system of the Russian Federation. Before we talk about violations committed by tax agents, we should talk about the responsibilities assigned to them by Russian legislation.

Responsibilities of a tax agent

Responsibilities of tax agents defined in paragraph 3 of Art.

24 of the Tax Code of the Russian Federation are as follows. 1. Correctly and timely calculate, withhold from funds paid to taxpayers, and transfer taxes to the budget system of the Russian Federation to the appropriate accounts of the Federal Treasury. Note that the tax agent is obliged to calculate the amount of tax correctly and timely when paying income to the taxpayer in any form.

But the obligation to withhold and transfer the amount of tax to the budget arises from the tax agent only if the income is paid to the taxpayer in cash. If there is another form of payment of income, then it is clear that the tax agent is not able to withhold the amount of tax.

2. Notify in writing the tax authority at the place of your registration about the impossibility of withholding tax and the amount of the taxpayer’s debt within one month from the day the tax agent became aware of such circumstances.

As stated in the Letter of the Federal Tax Service dated August 22, 2014 No. SA-4-7/16692, the impossibility of withholding tax arises, for example, in the case of payment of income in kind or the occurrence of income in the form of a material benefit.

In such a situation, the tax agent is obliged to notify the tax authorities at his place of registration in writing about the impossibility of withholding tax and about the amount of the taxpayer’s debt.

Moreover, the law allows the tax agent only a month for such actions from the day he became aware that the tax amount cannot be withheld.

The fact that the tax agent is obliged to calculate the amount of tax payable by the taxpayer and inform the tax authority about the impossibility of withholding the tax and the amount of debt of the taxpayer in the case where no cash payments were made to the taxpayer in a given tax period and withholding the amount of tax turned out to be impossible is also noted. clause 1 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57 “On some issues arising when arbitration courts apply part one of the Tax Code of the Russian Federation” (hereinafter referred to as the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation No. 57).

Tax agents for personal income tax (hereinafter - personal income tax), taking into account the priority of special rules over general ones, should be guided in the general case by paragraph 5 of Art. 226 of the Tax Code of the Russian Federation, which states that if it is impossible to withhold the calculated amount of tax from the taxpayer during a tax period, the tax agent is obliged, no later than March 1 of the year following the expired tax period in which the relevant circumstances arose, to notify the taxpayer and the tax authority in writing at the place of its registration about the impossibility of withholding tax, the amount of income from which tax was not withheld, and the amount of tax not withheld.

It should also be borne in mind that if, before the end of the tax period, a tax agent pays any money to the taxpayer, then he is obliged to withhold tax from it, taking into account amounts not previously withheld.

After the end of the tax period in which the tax agent pays income, for example, to an individual, and a written message from the tax agent to the taxpayer and the tax authority at the place of registration about the impossibility of withholding personal income tax, the obligation to pay is assigned to the individual, and the tax agent’s obligation to withhold the corresponding amounts of tax stops.

The official form of notifying tax authorities about the impossibility of withholding tax from a taxpayer has today been approved only for tax agents for personal income tax.

Starting with the submission of information on the income of individuals and amounts of personal income tax for the tax period of 2018, Order of the Federal Tax Service of Russia dated 02.10.2018 No. ММВ-7-11/ [email protected] “On approval of the form of information on the income of individuals and amounts” personal income tax, the procedure for filling out and the format of its submission in electronic form, as well as the procedure for submitting to the tax authorities information about the income of individuals and the amounts of personal income tax and messages about the impossibility of withholding tax, about the amounts of income from which is not withheld tax, and the amount of unwithheld personal income tax.”

Paragraph 2 of the said document establishes that the message about the impossibility of withholding tax, the amount of income from which tax was not withheld, and the amount of unwithheld personal income tax in accordance with paragraph 5 of Art. 226 of the Tax Code of the Russian Federation is submitted according to the Form of information on the income of individuals and amounts of personal income tax “Certificate of income and amounts of tax of an individual” (Form 2-NDFL) in accordance with Appendix No. 1 to Order MMV-7-11/ [email protected]

3. Keep records of accrued and paid income to taxpayers, calculated, withheld and transferred taxes to the budget system of the Russian Federation.

Accounting must be organized in such a way as to ensure the receipt of information for each taxpayer (Resolution of the Federal Antimonopoly Service of the East Siberian District dated 09/02/2003 in case No. A33-20070/02-С3-Ф02-2713/03-С1).

4. Submit to the tax authority at the place of your registration the documents necessary to exercise control over the correctness of calculation, withholding and transfer of taxes (resolutions of the Federal Antimonopoly Service of the Volga-Vyatka District dated 02.05.2012 in case No. A28-5002/2011, dated 28.11.2011 in case No. A29-2853/2011; Resolution of the Federal Antimonopoly Service of the Central District dated August 28, 2006 in case No. A35-9977/05-C18).

For example, if an organization is a tax agent for corporate income tax, it, according to clause 4 of Art. 310 of the Tax Code of the Russian Federation based on the results of the reporting (tax) period within the time limits established for the submission of tax calculations Art. 289 of the Tax Code of the Russian Federation, provides information on the amounts paid to foreign organizations of income and taxes withheld for the past reporting (tax) period to the tax authority at its location.

The tax calculation form on the amounts paid to foreign organizations for income and taxes withheld, the procedure for filling it out, as well as the format for submitting the tax calculation in electronic form were approved by Order of the Federal Tax Service of Russia dated March 2, 2016 No. MMV-7-3/ [email protected]

5. For four years, ensure the safety of documents necessary for the calculation, withholding and transfer of taxes.

6. Perform other duties provided for by the Tax Code of the Russian Federation. For example, personal income tax tax agents are required to inform taxpayers about the facts of excessive tax withholding and the amounts of excessively withheld personal income tax (clause 1 of Article 231 of the Tax Code of the Russian Federation). Moreover, the law allows the tax agent for personal income tax to take such actions only ten days from the date of discovery of such a fact.

Tax Agent Responsibility

For non-fulfillment or improper fulfillment of the duties assigned to him, the tax agent is liable in accordance with the legislation of the Russian Federation (clause 5 of Article 24 of the Tax Code of the Russian Federation).

Types of tax offenses and liability for their commission are provided for in Chapters 16 and 18 of Part One of the Tax Code of the Russian Federation.

At the same time, Chapter 16 directly defines the types of tax offenses and responsibility for their commission, and Chapter 18 defines the types of violations by the bank of obligations provided for by the legislation on taxes and fees, and responsibility for their commission.

A tax offense is an unlawful act (in violation of the legislation on taxes and fees) (action or inaction), in particular, of a tax agent, for which the Tax Code of the Russian Federation establishes liability (Article 106 of the Tax Code of the Russian Federation).

A person is considered innocent of committing a tax offense until his guilt is proven in the manner prescribed by federal law. A person held accountable is not required to prove his innocence of committing a tax offense. The responsibility for proving the circumstances indicating the fact of a tax offense and the guilt of the person in committing it rests with the tax authorities.

Irremovable doubts about the guilt of a person held accountable are interpreted in favor of this person (Clause 6 of Article 108 of the Tax Code of the Russian Federation).

In addition, when considering a case on the collection of sanctions for a tax offense, it is necessary to take into account the circumstances mitigating or aggravating liability provided for by the provisions of Art. 112 of the Tax Code of the Russian Federation.

Clause 1 of Art. 111 of the Tax Code of the Russian Federation provides a list of circumstances that exclude a person’s guilt in committing a tax offense, but this list is not exhaustive.

According to paragraphs. 4 clause 1 of this article, the court or tax authority considering the case may accept other circumstances not specified in the list of circumstances excluding guilt, as indicated in the Letter of the Federal Tax Service dated 08/09/2016 No. GD-4-11/14515 “On the Tax Service” responsibility of tax agents."

In this regard, the issue of bringing a person to tax liability should be considered taking into account established factual circumstances, including circumstances mitigating liability, excluding holding a person liable and excluding the person’s guilt in committing a tax offense, provided for by the provisions of Chapter 15 of the Tax Code of the Russian Federation in the manner established by the Tax Code of the Russian Federation .

One of the main responsibilities of a tax agent is to correctly and timely calculate, withhold from funds paid to taxpayers, and transfer taxes to the budget system of the Russian Federation to the appropriate accounts of the Federal Treasury.

For example, a tax agent for personal income tax in accordance with clause 4 of Art. 226 of the Tax Code of the Russian Federation is obliged to withhold the calculated amount of tax directly from the taxpayer’s income upon actual payment.

The tax agent is obliged to transfer the amount of calculated and withheld tax no later than the day following the day the income is paid to the taxpayer.

When paying a taxpayer income in the form of temporary disability benefits (including benefits for caring for a sick child) and in the form of vacation pay, the tax agent is obliged to transfer the amounts of calculated and withheld tax no later than the last day of the month in which such payments were made (clause 6 of Art. 226 of the Tax Code of the Russian Federation).

For unlawful non-withholding and (or) non-transfer (incomplete withholding and (or) transfer) within the period established by the Tax Code of the Russian Federation of the amount of personal income tax subject to withholding and transfer by the tax agent, in Art. 123 of the Tax Code of the Russian Federation establishes liability in the form of a fine in the amount of 20% of the amount subject to withholding and (or) transfer.

At the same time, the Tax Code of the Russian Federation does not provide for the release of a tax agent from liability depending on the period of unlawful failure to fulfill the established obligation to withhold and transfer the amount of tax to the budget system of the Russian Federation, as indicated in letters of the Ministry of Finance of Russia dated April 4, 2017 No. 03-02-08/19755 , dated October 13, 2016 No. 03-02-08/59771.

Paragraph 21 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation No. 57 states that the offense under Art. 123 of the Tax Code of the Russian Federation, can be imputed to the tax agent only in the case where he had the opportunity to withhold and transfer the appropriate amount, bearing in mind that the withholding is carried out from funds paid to the taxpayer.

Article 123 of the Tax Code of the Russian Federation has been supplemented with a new clause 2, according to which the tax agent is released from liability under the said article if the following conditions are simultaneously met:

• the tax calculation (tax calculation) is submitted to the tax authority within the prescribed period; • in the tax calculation (tax calculation) there are no facts of non-reflection or incomplete reflection of information and (or) errors leading to an understatement of the amount of tax to be transferred to the budget system of the Russian Federation; • the tax agent independently transferred to the budget system of the Russian Federation the amount of tax not transferred on time, and the corresponding penalties until the moment when he became aware of the discovery by the tax authority of the fact of untimely transfer of the tax amount or of the appointment of an on-site tax audit for such tax for the corresponding tax period .

Corresponding changes in Art. 123 of the Tax Code of the Russian Federation was introduced by subparagraph “b” of paragraph 4 of Art. 1 of Federal Law No. 546-FZ of December 27, 2018 “On Amendments to Part One of the Tax Code of the Russian Federation” and are valid from January 28, 2019. The basis for bringing a person to justice for violating the legislation on taxes and fees is the establishment of the fact of the commission of this violation by a decision of the tax authority that has entered into force (clause 3 of Article 108 of the Tax Code of the Russian Federation).

If there is at least one mitigating circumstance, the amount of the fine must be reduced by no less than two times compared to the amount established by the relevant article of the Tax Code of the Russian Federation (Clause 3 of Article 114 of the Tax Code of the Russian Federation), as specialists from the Ministry of Finance of Russia recalled in a Letter dated 16.02. .2015 No. 03-02-07/1/6889.

For late fulfillment of tax payment obligations, penalties are charged.

Let us recall that a penalty is recognized as the amount of money established by this article, which the taxpayer must pay in the event of paying the due amounts of taxes later than the deadlines established by the legislation on taxes and fees (clause 1 of Article 75 of the Tax Code of the Russian Federation).

From 01/01/2019, a penalty will be charged, unless otherwise provided by Art. 75 of the Tax Code of the Russian Federation and Chapters 25 and 26.1 of the Tax Code of the Russian Federation, for each calendar day of delay in fulfilling the obligation to pay tax, starting from the day following the tax payment established by the legislation on taxes and fees until the day of fulfillment of the obligation to pay it, inclusive.

The amount of penalties accrued on arrears cannot exceed the amount of this arrears (clause 3 of article 75 of the Tax Code of the Russian Federation).

Penalties are not accrued on the amount of arrears that the taxpayer (a member of a consolidated group of taxpayers against whom measures were taken to force the collection of taxes) could not repay due to the fact that by decision of the tax authority a seizure of the taxpayer’s property was imposed or by a court decision security bonds were taken measures in the form of suspension of transactions on the accounts of a taxpayer (a member of a consolidated group of taxpayers against whom measures have been taken to forcibly collect taxes) in a bank, seizure of funds or property of a taxpayer (member of a consolidated group of taxpayers).

In this case, penalties are not accrued for the entire period of validity of these circumstances. Filing an application for a deferment (installment plan) or an investment tax credit does not suspend the accrual of penalties on the amount of tax payable.

In the Letter of the Ministry of Finance of Russia dated April 29, 2013 No. 03-02-08/30, with reference to the Resolution of the Constitutional Court of the Russian Federation dated December 17, 1996 No. 20-P, it is noted that failure to pay taxes on time must be compensated by paying off the debt on the tax liability with full compensation for damages, incurred by the state as a result of late payment of taxes.

Therefore, to the amount of the tax itself (arrears) not paid on time, the legislator has the right to add an additional payment - a penalty as compensation for losses to the state treasury as a result of shortfalls in receiving tax amounts on time in the event of a delay in tax payment.

The penalty for each calendar day of delay in fulfilling the obligation to pay tax is determined as a percentage of the unpaid amount of tax (clause 4 of Article 75 of the Tax Code of the Russian Federation). The interest rate of the penalty is assumed to be equal for organizations: • for delay in fulfilling the obligation to pay tax for a period of up to 30 calendar days (inclusive) - in the amount of 1/300 of the refinancing rate of the Central Bank of the Russian Federation in force at that time; • for delay in fulfilling the obligation to pay tax for a period of more than 30 calendar days - in the amount of 1/300 of the refinancing rate of the Central Bank of the Russian Federation, valid for the period up to 30 calendar days (inclusive) of such delay, and 1/150 of the refinancing rate of the Central Bank of the Russian Federation, valid for the period starting from the 31st calendar day of such delay.

Let us recall that this procedure for calculating penalties was introduced by Federal Law No. 401-FZ of November 30, 2016 “On amendments to parts one and two of the Tax Code of the Russian Federation and certain legislative acts of the Russian Federation” and applies to arrears arising from October 1, 2017.

Penalties are paid simultaneously with the payment of tax amounts or after payment of such amounts in full (clause 5 of Article 75 of the Tax Code of the Russian Federation).

Penalties can be collected forcibly from the taxpayer’s funds (precious metals) in bank accounts, as well as from other property of the taxpayer in the manner provided for in Art. Art. 46 - 48 of the Tax Code of the Russian Federation (clause 6 of Article 75 of the Tax Code of the Russian Federation).

Note that in this case, penalties can be collected if the tax authority has timely taken measures to force the collection of the amount of the corresponding tax, as stated in paragraph 57 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation No. 57.

In this case, penalties are accrued on the day of actual repayment of the arrears.

The above rules based on clause 7 of Art. 75 of the Tax Code of the Russian Federation also applies to tax agents.

If a tax agent for personal income tax pays the due amounts of taxes later than the deadlines established by the legislation on taxes and fees, penalties are accrued to the tax agent for the organization as a whole, taking into account the date of receipt of income for each individual and the deadlines for withholding personal income tax for each individual, on as stated in the Letter of the Federal Tax Service dated December 29, 2012 No. AS-4-2/22690.

Another responsibility of the tax agent is, as we said, keeping records of accrued and paid income to taxpayers, calculated, withheld and transferred taxes to the budget system of the Russian Federation for each taxpayer.

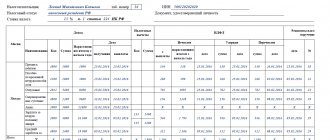

For example, for personal income tax, the forms of tax accounting registers and the procedure for reflecting in them analytical data of tax accounting, data from primary accounting documents are developed by the tax agent independently and must contain information that allows identifying the taxpayer, the type of income paid to the taxpayer and tax deductions provided, as well as expenses and amounts reducing the tax base, in accordance with codes approved by the federal executive body authorized for control and supervision in the field of taxes and fees, the amount of income and the date of their payment, taxpayer status, dates of withholding and transfer of tax to the budget system of the Russian Federation, details of the corresponding payment document (Clause 1 of Article 230 of the Tax Code of the Russian Federation).

The absence of tax accounting registers is the basis for bringing the tax agent to liability under Art. 120 Tax Code of the Russian Federation.

Results

The employer has tax agent responsibilities in relation to income tax on payments to employees.

The employer must timely calculate, withhold and transfer personal income tax to the budget, as well as report to the budget on income tax amounts. Failure of a tax agent to fulfill his duties is a reason for a fine from regulatory authorities. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Responsibility and punishment

Accordingly, if a person with the status of “agent” does not fulfill his duties assigned by current legislation, then liability will inevitably arise. Crimes and offenses in the economic sphere under consideration imply two types of liability: tax and criminal. In the first case, certain penalties are provided for, established in accordance with Chapter 16 of the Tax Code of the Russian Federation. For example, this is Article 126.1 – provision of documents containing false information to authorized bodies. For committing such an offense, a fine of 500 rubles is imposed for each document that is false. Article 123 of the Tax Code of the Russian Federation is a failure to comply with the established deadlines for withholding and transferring payments, committed in an unlawful manner. The perpetrator is subject to a fine of 20% of the amount not withheld.

Criminal liability

The mere recognition of an act in the form of a criminal offense indicates the seriousness and significance, as well as the social danger of this act, and, consequently, the severity of the punishment will be an order of magnitude higher than the above sanctions regulated by the provisions of the Tax Code of the Russian Federation. It should be immediately noted that the disposition of Article 199.1, which will be discussed below, contains such a mandatory feature as a large or especially large amount of money involved in the case. In accordance with the legislator's note, a large amount is calculated as the amount of taxes and fees for a three-year financial period of 5,000,000 rubles, if the unpaid amount accounts for more than 25% of the mentioned 5,000,000 rubles, or if the amount exceeds 15,000,000 rubles. And especially large amounts are considered amounts of funds calculated in the amounts of 15,000,000 rubles, 50% and 45,000,000 rubles.

Taking into account all of the above, you should refer to the provisions of Article 199.1 of the Criminal Code of the Russian Federation:

- Failure to fulfill, in personal interests, the duties of a tax agent to calculate, withhold or transfer taxes and (or) fees subject to calculation, withholding from the taxpayer and transfer to the appropriate budget in accordance with the legislation of the Russian Federation on taxes and fees, committed on a large scale, is punishable by a fine of in the amount of one hundred thousand to three hundred thousand rubles or in the amount of wages or other income of the convicted person for a period of one to two years, or forced labor for a period of up to two years with deprivation of the right to hold certain positions or engage in certain activities for a period of up to three years, or without it, or by arrest for a term of up to six months, or by imprisonment for a term of up to two years with or without deprivation of the right to hold certain positions or engage in certain activities for a term of up to three years.

- The same act, committed on an especially large scale, is punishable by a fine in the amount of two hundred thousand to five hundred thousand rubles or in the amount of wages or other income of the convicted person for a period of two to five years, or by forced labor for a term of up to five years with deprivation of the right to occupy certain positions or engage in certain activities for a term of up to three years or without it, or imprisonment for a term of up to six years with deprivation of the right to hold certain positions or engage in certain activities for a term of up to three years or without it.

As can be seen from Part 1, another mandatory condition for qualifying failure to fulfill the duties of a tax agent as a crime is the requirement that the motivational component for the guilty person be in the form of personal interests. This interest is manifested in the desire/desire to receive some kind of personal benefit, for example, career advancement, receiving a mutual favor, the necessary recommendation, etc.

It is important that personal interest cannot be put on a par with selfish motives, since the first implies personal and intangible benefits, and in the second case we mean some form of theft of funds by withdrawing a certain amount in one’s favor. The importance of this difference lies in the fact that if there are no personal interests in the act, the crime in question will not be formed, and the presence of self-interest in the actions will entail additional qualifications.

Separately, it should be noted the severity of the possible punishment provided for in Article 199.1 of the Criminal Code of the Russian Federation, namely:

- fines from 100,000 to 500,000 rubles;

- forced labor for 2 and 5 years, respectively, with a possible official and active ban for up to 3 years;

- arrest for 6 months;

- imprisonment for 2 years or 6 years with a similar prohibition.

Of course, the severity of the penalty directly depends on the amount of money that was not paid in full by the tax agent.