Who has the right to claim compensation?

If the employer is an insurer and during the month paid temporary disability benefits and other social payments to employees, he has the right to request the return of sick leave from the Social Insurance Fund in 2021 or reduce the amount of the monthly contribution to VNiM by the amount of paid benefits from the fund (Part 2 of Article 4.6 255 -FZ of December 29, 2006, clause 2 of Article 431 of the Tax Code of the Russian Federation).

If the amount of the listed social benefits is greater than the insurance premiums calculated for the month, then the procedure for compensation for sick leave from the Social Insurance Fund in 2021 is as follows:

- Apply the excess balance toward the next month's payment.

- Write an application to the territorial department of the fund for monetary compensation of the difference.

The application is sent according to the form from letter No. 02-09-11/04-03-27029 (approved by order No. 951n dated 12/04/2009). The following must be attached to the application:

- certificate-calculation;

- breakdown of expenses;

- supporting documents.

More information on how to fill out an application for a refund: “Instructions: fill out an application to the Social Insurance Fund for reimbursement of benefits.”

How to get money back for sick leave from the Social Insurance Fund in 2021

- debt of the Social Insurance Fund to the employer regarding insurance contributions, as of the beginning and end date of the period;

- accrued insurance premiums for the entire period and three months payable;

- additional insurance charges;

- expenses that do not need to be taken into account in calculations;

- funds that have already been reimbursed by the fund during the reporting period;

- refunded overpaid contributions to the Social Insurance Fund;

- the amount that was spent on compulsory social insurance during the reporting period and within three months;

- funds contributed as insurance premiums;

- written off debt of the policyholder.

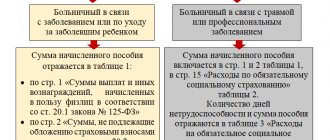

The calculation certificate has not changed. All information was previously recorded in the first table 4-FSS. Now the legislative decision has been made to allocate a separate document for these purposes.

Features for pilot project participants

Participants in the pilot project submit documents for payment of social benefits directly to the Social Insurance Fund. Policyholders fill out the necessary documentation from Order No. 578 dated November 24, 2017 (Appendix No. 1 to the Order). The application and certificate of incapacity for work are transferred to the territorial department of the fund, and the territorial department makes all payments independently. As a result, compensation for sick leave for pregnancy and childbirth from the Social Insurance Fund is not required - the policyholder does not incur expenses for social benefits.

Application for Reimbursement of Expenses Under the FSS What is the Kbk for the return of funds

Having considered the issue, we came to the following conclusion: Receipt of compensation from the Federal Social Insurance Fund of the Russian Federation regarding expenses incurred for medical examinations can be reflected in accounting as a “income” transaction - using account 2,209,30,000. Receipt of funds to the personal account of a budgetary institution at the same time reflected as an increase in off-balance sheet account 17 indicating the article of the analytical group of the subtype of budget income 130 and article 130 of the KOSGU.

Rationale for the conclusion: In accordance with Art. Art. 212, 213 of the Labor Code of the Russian Federation, medical examinations are the responsibility of the employer and are carried out by him at his own expense (not at the expense of employees). At the same time, in accordance with paragraphs. “e” clause 3 of the Rules, approved by order of the Ministry of Labor and Social Protection of Russia dated December 10, 2021 N 580n (hereinafter referred to as the Rules), the insurer’s expenses are subject to financial support from the amounts of insurance contributions for compulsory social insurance against industrial accidents and occupational diseases to conduct mandatory periodic medical examinations (examinations) of workers engaged in work with harmful and (or) dangerous production factors. The specifics of reimbursement of the insurer's expenses for preventive measures to reduce industrial injuries and occupational diseases of workers in the constituent entities of the Russian Federation participating in the implementation of the pilot project are set out in Resolution of the Government of the Russian Federation dated April 21, 2021 N 294 (hereinafter referred to as Regulation N 294). Payment for preventive measures is carried out by the policyholder at his own expense, followed by reimbursement from the budget of the Social Insurance Fund of the Russian Federation (hereinafter - FSS RF) for expenses incurred by the policyholder within the amount agreed with the territorial body of the FSS for these purposes (clause 3 of Regulations No. 294). In this case, expenses actually incurred by the policyholder, but not confirmed by documents on the intended use of funds, are not subject to reimbursement (clause 5 of Regulation No. 294). Conducting medical examinations is the responsibility of the employer and does not apply to the expenditure obligations of the Federal Social Insurance Fund of the Russian Federation. The decision to reimburse a budgetary institution for expenses incurred (part of the expenses incurred) by the FSS of the Russian Federation is made by the territorial body of the FSS in the prescribed manner, provided that the employer complies with the established conditions. Accordingly, reimbursement of expenses incurred is an independent fact of economic life, carried out as part of a new business transaction and from another person (not from the counterparty to whom the payment was made, but from the Federal Social Insurance Fund of the Russian Federation). In this connection, in our opinion, the receipt of compensation for part of the expenses incurred for medical examinations into the personal account of a budgetary institution must be reflected in accounting as a “income” transaction. Based on the economic meaning, such an operation can be reflected in accounting under the article of the analytical group of subtype of budget income 130 “Revenue from the provision of paid services (work) and compensation of costs” (hereinafter referred to as AnKVD) and article 130 “Revenue from the provision of paid services (work)” KOSGU as compensation for the costs of state (municipal) institutions using the balance sheet account 0 209 30 000 “Calculations for compensation of costs” (clause 4.1.1, clause 4.1 of section II, clause 3 of section V of the Instructions approved by order of the Ministry of Finance of Russia dated 01.07. 2021 N 65n, paragraphs 220, 221 of the Instruction approved by order of the Ministry of Finance of Russia dated December 1, 2021 N 157n, hereinafter referred to as Instruction No. 157n, paragraph 107 of the Instruction approved by order of the Ministry of Finance of Russia dated December 16, 2021 N 174n, hereinafter referred to as Instruction N 174n). All income legally received as part of activities with subsidies goes to the independent disposal of budgetary institutions (clause 3 of Article 298 of the Civil Code of the Russian Federation). The ability to independently dispose of the funds received is the basis for accounting for a “profitable” transaction within the framework of activity “2”. At the same time, specialists from authorized bodies directly indicate that within the framework of type of financial support “4” only income transactions can be taken into account in the amount of: - subsidy received for completing the task; — return of receivables from previous years generated during the period of the institution’s activities as recipients of budget funds. Accordingly, the receipt of reimbursement of expenses incurred from the Social Insurance Fund should be reflected in accounting under KFO “2”. In the future, the institution can dispose of these funds at its own discretion, including directing them to fulfill obligations related to the implementation of municipal tasks. The document that determines the directions for the use of subsidy funds by a budgetary institution to fulfill a municipal task is the plan of financial and economic activities of the institution (hereinafter referred to as the FCD Plan). The general requirements for drawing up the FCD Plan are established by Order of the Ministry of Finance of Russia dated July 28, 2021 N 81n (hereinafter referred to as Requirements N 81n). At the same time, the municipal budgetary institution draws up a FCD Plan in accordance with Requirements No. 81n in the manner determined by the body exercising the functions and powers of the founder in relation to the institution (hereinafter referred to as the Founder). The founder has the right to establish the specifics of drawing up and approving the FCD Plan for individual institutions (clause 2 of Requirements No. 81n). The possibility of making changes to the FCD Plan is provided for in clause 19 of Requirements No. 81n. In this case, the decision to make changes to the FCD Plan is made by the head of the institution, and the FCD Plan, taking into account the changes, is approved by the head of the institution, unless otherwise established by the Founder (clauses 19, 22 of Requirements No. 81n). Accordingly, in the situation under consideration, it is necessary to make appropriate changes to the planned income assignments approved by the FHD Plan. This will be reflected in accounting in accordance with paragraph 171 of Instruction No. 174n. Thus, in the situation under consideration, the following correspondence accounts can be reflected in the accounting of a budgetary institution: 1. Debit 4,506 10,226 Credit 4,502 11,226 - obligations were accepted under the contract for medical examinations; 2. Debit 4,401 20,226 (4,109 XX 226) Credit 4,302 26,730 - reflects the accrual of debt for payment for services for medical examinations; 3. Debit 4,502 11,226 Credit 4,502 12,226—acceptance of monetary obligations is reflected; 4. Debit 4,302 26,830 Credit 4,201 11,610, at the same time an increase in off-balance sheet account 18 (244 KVR, 226 KOSGU) is reflected - payment for services for medical examinations is reflected; 5. Debit 2,209 30,560 Credit 2,401 10,130 - reflects the accrual of income based on the decision made by the territorial body of the Federal Social Insurance Fund of the Russian Federation; 6. Debit 2,507 10,130 Credit 2,504 10,130 - reflects changes to the FCD Plan in the amount of funds received from the Federal Social Insurance Fund of the Russian Federation as part of financial support for preventive measures; 7. Debit 2,201 11,510 Credit 2,209 30,660, at the same time an increase in off-balance sheet account 17 (130 AnKVD, 130 KOSGU) is reflected - the receipt of funds from the Federal Social Insurance Fund of the Russian Federation to the personal account of a budgetary institution is reflected; 8. Debit 2,508 10,130 Credit 2,507 10,130 - reflects the receipt of income from the provision of paid services for the current financial year.

We recommend reading: Veteran of Combat Operations in Chechnya There will be a Pension Increase in April 2021

Limitations on Refunds

Compensation is limited to minimum and maximum values. The minimum and maximum are calculated for each individual employee for the two years preceding the insured event. The accountant determines the average earnings for these periods, taking into account the marginal base:

- for 2021 - 912,000 rubles;

- for 2021 - 865,000 rubles;

- for 2021 - 815,000 rubles.

The maximum payment in 2020 is paid within the range of 1,680,000 rubles (865,000 + 815,000). And for one day of illness they compensate no more than 2,301.37 rubles. (1,680,000 : 730 days).

The minimum amount is calculated similarly, for two years. But the value is determined by the minimum wage: Minimum wage x 24 months: 730 days. In 2021, the low for one day is 398.79. They will not pay less than this amount.

What documents are needed

Order No. 951n specifies how to reimburse sick leave from the Social Insurance Fund in 2020:

- Determine the amount to be reimbursed and fill out the calculation forms.

- To write an application.

- Submit the package with documents for reimbursement to the fund.

The list of accompanying documentation is given in Order No. 951n and the methodological recommendations of the fund. We collected everything in one table:

| Benefit | Necessary documents to the Social Insurance Fund for reimbursement of sick leave in 2020 (and other insurance payments) |

| For temporary disability |

|

| For pregnancy and childbirth | And these are the documents for returning sick leave from the Social Insurance Fund in 2021 for pregnancy and childbirth:

|

| At the birth of a child |

|

| Child care up to 1.5 years old |

|

| For burial |

|

The procedure for reimbursement of social expenses from the Social Insurance Fund

The regulations for reimbursement of insurance amounts from the Social Insurance Fund of the Russian Federation were approved by order of the Ministry of Health and Social Development dated December 4, 2009 No. 951n. Since 2021, changes have been made to the regulations regarding the list of documents (Order of the Ministry of Labor of the Russian Federation dated October 28, 2016 No. 585n).

Now the package of documents depends on the period for which the expenses were incurred that the businessman wants to reimburse. However, the changes did not affect the entire list.

Regardless of the period, the employer must provide:

- Statement.

- Copies of supporting documents: sick leave certificates, birth certificates of children, etc.

If we are talking about “old” expenses incurred before 2021, then the businessman must, in addition to the above documents, provide an interim report in Form 4-FSS.

If the insured events occurred after 01/01/2017, then you must provide a certificate of calculation.

The reason for the changes is that since 2021, insurance premiums, which pay for sick leave and maternity benefits, have come under the control of tax officials. Therefore, in the “standard” form 4-FSS, which the fund receives, there is no more information about these payments. Consequently, there is no point in submitting an interim calculation in the 4-FSS format.

The recommended form of the new calculation certificate is attached to the letter of the Federal Social Insurance Fund of the Russian Federation dated December 7, 2016 No. 02-09-11/04-03-27029. An application form is also attached to this letter.

The timing of reimbursement depends on whether the fund department decides to verify the documents provided:

- In the absence of verification - 10 days from the date of provision of the complete package (clause 3, article 4.6 of the law of December 29, 2006 No. 255-FZ).

- When conducting a desk audit, the refund period may take up to 3 months (Clause 2, Article 26.15 of Law No. 125-FZ of July 24, 1998).

- An on-site inspection is shorter - in general, its period is no more than 2 months, plus 10 days to make a decision (Articles 26.16, 26.20 of Law No. 125-FZ).

Document verification deadlines

Instructions on how to return sick leave from the Social Insurance Fund in 2021:

- calculate funds for refund;

- fill out the application, certificate and transcript;

- submit papers to the fund;

- wait for the test results;

- receive funds.

The documentation is checked within 10 days (Part 3 of Article 4.6 255-FZ). If a specialist has questions about the calculations, he has the right to organize a desk audit (Part 4, Article 4.6 255-FZ). In this case, the money will come only after a positive control result and not earlier than in 2-3 months.

Form 23-FSS

In cases where legal entities or individual entrepreneurs do not require the return of excessively transferred funds, employees of extra-budgetary funds can, at their discretion, independently decide to credit such amounts to the transfer of future contributions or to pay off existing debts and fines with them.

If the application arrived in a timely manner and the facts indicated in it are true, then the return of funds must occur within a month after its receipt by the employees of the extra-budgetary fund with which the incident happened. At the same time, if the fund violates its obligations and is overdue for the return of funds, then by writing a corresponding statement, for each day of delay, you can demand interest in the amount of 1/300 of the refinancing rate (if representatives of the organization refuse to pay voluntarily, you can safely go to court ).

We recommend reading: The return of goods of inadequate quality is not reflected in the Profit Declaration Why