Justified overspending

Overspending can be considered justified if the following conditions are met:

- the employee spent money on completing a task assigned by the organization (as a rule, it is indicated in the manager’s order to issue money on account);

- The employee presented documents confirming the existence of overspending (for example, cash receipts).

If one of the specified conditions is not met, the employee may not be reimbursed. These are the requirements of the instructions approved by Resolution of the State Statistics Committee of Russia dated August 1, 2001 No. 55.

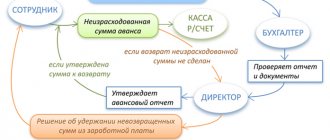

Compensation for overspending from the cash register

The amounts that the employee spent in excess of those received on the report, give him from the cash register. To do this, fill out a cash receipt order form No. KO-2. Indicate the number and date of this document in the line of the advance report “Overexpenditure issued by cash order.” This is provided for in the instructions approved by Resolution of the State Statistics Committee of Russia dated August 1, 2001 No. 55.

Situation: is it possible to make an entry about compensation for overexpenditure (details of the cash receipt order for which the payment was made) of accountable amounts in the employee’s advance report after its approval?

Yes, you can.

The period during which an organization must compensate an employee for overspending is not limited by law. Therefore, you can make an entry about debt repayment in the advance report even after its approval. The instructions approved by Resolution of the State Statistics Committee of Russia dated August 1, 2001 No. 55 do not contain a prohibition in this regard.

Situation: is it possible to reimburse an employee for overexpenditure of accountable amounts during his vacation?

Yes, you can.

There is no need to wait until the employee returns from vacation. Current legislation does not prohibit paying overages to an employee during the period when he is on vacation (Article 22 of the Labor Code of the Russian Federation, instructions approved by Resolution of the State Statistics Committee of Russia dated August 1, 2001 No. 55).

Therefore, if necessary, the organization has the right to reimburse the employee for overexpenditure while he is on vacation.

Situation: is it possible to reimburse an employee for overexpenditure of accountable amounts after the employee returns from vacation? The employee submitted an advance report and went on vacation the next day.

Yes, you can.

After the accountant has checked the expense report, it must be approved by the manager. The period during which the manager approves the expense report is not limited by law. He can do this a few days after the employee has submitted the report to the accounting department. The accounting department should pay the employee only after the manager approves the advance report. Therefore, the organization has the right to reimburse the overexpenditure of accountable amounts after the employee returns from vacation. This conclusion can be drawn from the instructions approved by Resolution of the State Statistics Committee of Russia dated August 1, 2001 No. 55.

When issuing money from the cash register to compensate for the overspent amount, make the following entry:

Debit 71 Credit 50

– the employee is reimbursed for expenses exceeding the amount previously issued on account.

An example of compensation to an employee for expenses in excess of the amounts issued to him on account

Secretary of Alpha LLC E.V. Ivanova purchased stationery for the organization. On March 31, she was given 2,000 rubles for these purposes. But she spent 2100 rubles. For this amount, she submitted supporting documents to the accounting department (sales and cash receipts, where VAT in the amount of 320 rubles was allocated), there is no invoice.

On April 1, the head of Alpha approved Ivanova’s advance report.

On April 3, the Alpha cashier gave Ivanova an overexpenditure in the amount of 100 rubles. (2100 rub. – 2000 rub.).

Alpha's accountant reflected these transactions as follows.

March 31:

Debit 71 Credit 50 – 2000 rub. – money was issued against Ivanova’s report.

April 1:

Debit 10 Credit 71 – 1780 rub. (RUB 2,100 – RUB 320) – stationery purchased by the employee was received;

Debit 19 Credit 71 – 320 rub. – VAT on purchased stationery is taken into account;

Debit 91-2 Credit 19 – 320 rub. – VAT is written off at the expense of the organization’s own funds.

April 3:

Debit 71 Credit 50 – 100 rub. – the employee was compensated for expenses in excess of the amounts given to her on account.

Deadlines for submitting an advance report to the accounting department by the accountable person

Attention

A note indicating acceptance of the report is made in the appropriate column of the document. When issuing an overexpenditure, the report indicates the date of preparation and the number of the cash order. The report must contain a transcript of the signature of the cashier and chief accountant.

If employees of an enterprise use funds received from the cash register, they must submit a report. Based on this document, the company’s accounting department writes off money for operating or administrative expenses. Essence After three days from the date of return from a business trip, the employee must report on the funds received and spent.

To do this, an advance report of the accountable person is drawn up, and documents confirming the expenditure of funds are attached to it: travel tickets, hotel bills, etc. The form of the form is approved by the manager. Unused amounts are handed over to the cashier using a receipt order. If the employee does not have enough issued funds, then the overexpenditure is also compensated from the cash register, but according to an expense order.

- According to sub. 1 clause 8 art. 23 of the Tax Code of the Russian Federation, documents related to accounting or tax accounting, on the basis of which the tax base for calculating taxes to the budget is formed, must be stored for 4 years. These documents also include advance reports.

- In accordance with paragraph 4 of Art. 283 of the Tax Code of the Russian Federation, documents confirming the loss incurred are stored for the entire period during which the resulting loss is carried forward to future periods and reduces the tax base of the current tax period.

- In Art. 29 of Law No. 402-FZ for primary accounting documentation, which includes, in particular, advance reports, a storage period established by the rules of state archiving is provided, but not less than 5 years.

In paragraph 362 of the List of standard management archival documents generated in the process of activities of state bodies, local governments and organizations, indicating storage periods, approved. By order of the Ministry of Culture of Russia dated August 25, 2010 No. 558, a storage period of 5 years was established for advance reports.

Thus, the minimum storage period for advance reports is 5 years, the maximum is determined by the duration of the transfer of the loss (if received) to the future.

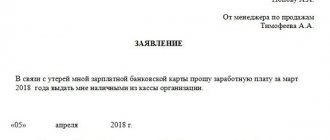

Compensation for overspending on a salary card

Situation: is it possible to reimburse an employee for overspending of accountable amounts to the same bank card to which his salary is transferred?

The legislation does not contain a clear answer to this question.

The advance report form provides for only one form of compensation for overspent accountable amounts - cash. The same opinion was expressed by the Bank of Russia in letter dated December 18, 2006 No. 36-3/2408.

At the same time, in letter dated December 24, 2008 No. 14-27/513, when commenting on settlements for business trips, the Bank of Russia indicated that the issue of the possibility of using bank cards for settlements on accountable amounts does not fall within its competence. The previously issued letter was not canceled. Therefore, the organization must independently decide whether to be guided by this letter or not.

Some arbitration courts do not deny the possibility of reimbursement of overspending to an employee’s bank card. For example, in resolution dated February 11, 2008 No. A52-174/2007, the Federal Antimonopoly Service of the North-Western District indicated that the organization lawfully transferred accountable funds to the employee’s “salary” account. And the employee, in turn, subsequently lawfully returned the unused accountable amounts from his bank account. These transactions were confirmed by the manager’s order (it recorded the possibility of issuing accountable amounts to employees by transferring them to bank cards), an employee’s advance report, a cash receipt order (on the basis of which the balance of the unused advance was returned to the organization), invoices, cash register checks , receipts.

To avoid unnecessary disputes with regulatory agencies, whenever possible, make all payments for accountable amounts through the cash desk. However, in any case, there is no responsibility for reimbursing the employee for overspending of accountable amounts to the same bank card to which his salary is transferred. The number of cash violations (violations of the procedure for working with cash and conducting cash transactions) does not include compensation for overspending of accountable amounts on a salary card (Article 15.1 of the Code of Administrative Offenses of the Russian Federation).

What is the procedure for reimbursement of an advance report?

Previous article: Reporting to an employee’s card from a current account. Next article: Postings on the advance report. Commercial enterprises are often faced with the need to make cash payments.

According to labor legislation, when used by an employee with the consent of the employer, the employee is compensated for expenses associated with the use of assets. In a situation where an employee used his personal money to pay for services or purchase goods, but did not receive an advance for this, the boss compensates for the expenses incurred by him. Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem, contact a consultant:. The report on the use of funds allocated for a business trip or under the report refers to consolidated accounting papers. These papers show the actions that are recorded in the primary papers and, accordingly, with Art. They summarize the indicators of the initial securities, giving the probability of reducing the number of accounts in the accounts. The initial documents include travel tickets, bills for accommodation during a business trip, invoices, etc. An advance report is drawn up in a situation where an employee was given funds in advance to purchase something for the needs of the organization. Funds must be issued on the basis of an expenditure cash order, which is written in the presence of a statement from the accountable person, confirmed by the boss.

Compensation of employee's personal money

An employee can purchase necessary goods (work, services) for the organization at his own expense. In this case, an advance report need not be drawn up, since this document is required to be drawn up only by those employees to whom the organization’s money was issued (clause 6.3 of Bank of Russia Directive No. 3210-U dated March 11, 2014).

To reimburse personal expenses, the employee must write an application and attach documents confirming the purchase (cash receipts, invoices, strict reporting forms, travel documents, etc.).

Submission deadlines

The deadlines for submitting advance reports are set by a local act of the boss. The law does not contain strict restrictions on this matter, but the deadlines must be reasonable.

The deadline for submitting an advance report is determined depending on the purpose for which the accountable funds were issued:

- For travel expenses. If cash is issued against the report - until the end of the fifth banking day, which follows the day on which the employee completed his business trip. If payments were made after they were withdrawn from the card - before the end of the third banking day, which follows the day the employee completed his business trip.

- To execute a production and economic order before the end of the fifth banking day, which follows the day on which the employee completed the execution of the order.

If the organization’s cash desk does not have the required amount, the parties can agree to pay the funds in installments. At the same time, the boss must remember that for unfulfilled obligations on time, the employee may be entitled to compensation for damages.

Personal income tax and insurance premiums

Regardless of the taxation system applied, money paid to an accountable person, provided there are supporting documents, is not taxed:

- Personal income tax (Article 209 of the Tax Code of the Russian Federation);

- contributions for compulsory pension (social, medical) insurance (Part 1, Article 7 of Law No. 212-FZ of July 24, 2009);

- contributions for insurance against accidents and occupational diseases (clause 1 of article 20.1 of the Law of July 24, 1998 No. 125-FZ).

The fact is that the amounts reimbursed to the accountable person are not remuneration for a completed task, but compensation for expenses incurred by him. These amounts were paid to the employee not as wages. In addition, they do not bring economic benefits (income) to the employee (Article 41 of the Tax Code of the Russian Federation).

Results

When organizing accounting for such non-standard transactions, their materiality should also be taken into account. If the organization has had a couple of cases of purchasing, for example, stationery without receiving an advance and the amount spent is insignificant, it is worth considering whether the cost of the accountant’s time to organize the document flow for these operations is equivalent to the amount of the possible error

If, on the contrary, such operations are a feature of the company’s activities or their amount is significant, then you should adhere to all the design recommendations given in our article. We would also like to note that it is better for employees to avoid making purchases for the needs of the organization with their own funds, so that there are no disagreements regarding the approval or disapproval of expenses by management, as well as for confidence during tax audits.

Tags: asset, accountant, personnel, loan, tax, order, expense, storage period for expense reports

OSNO, simplified tax system and UTII

Money paid to an employee in order to reimburse overexpended accountable amounts will be included in expenses when calculating income tax and single tax when simplifying the difference between income and expenses. To do this, it is necessary to confirm their economic feasibility (clause 1 of article 252, clause 2 of article 346.16 of the Tax Code of the Russian Federation). The procedure for accounting for these expenses depends on what the employee paid. For example, entertainment expenses incurred during a business trip can be taken into account within the normal limits. Expenses when purchasing materials and fixed assets are taken into account in a special manner.

The calculation of the single tax under simplified income and the calculation of UTII does not affect the reimbursement of overspent accountable amounts to the employee, since organizations using these special regimes do not take into account any expenses at all (clause 1 of Article 346.14, clause 1 of Article 346.29 of the Tax Code of the Russian Federation).

Situation: is it possible to take into account when calculating income tax the cost of goods (work, services) purchased through an employee before the organization compensated him for the overexpenditure of the amounts issued for reporting for this operation?

The answer to this question depends on what accounting method the organization uses when calculating income taxes.

If an organization calculates income tax using the accrual method, then the moment of compensation to an employee for overexpenditure to recognize costs for purchased goods (work, services) is not important. Recognize expenses during the period in which they are incurred. This is directly stated in paragraph 1 of Article 272 of the Tax Code of the Russian Federation.

If an organization calculates income tax using the cash method, then expenses are considered incurred only after they are actually paid. Payment for goods (work, services) is recognized as the termination of a counter-obligation by the purchaser to the seller, which is directly related to the delivery of goods (work, services). This is stated in paragraph 3 of Article 273 of the Tax Code of the Russian Federation. Article 273 of the Tax Code of the Russian Federation does not establish any specifics in the case of purchasing goods (work, services) through an employee (representative) of an organization. When the accountable pays for goods (work, services), the debt to the seller is repaid. However, as employees of the Ministry of Finance of Russia explain, until the overexpenditure is reimbursed to the accountant, it cannot be assumed that these expenses were paid by the acquiring organization (clause 1 of Article 252 of the Tax Code of the Russian Federation). The organization will have actual expenses only after compensation for overexpenditures. Therefore, in order to recognize expenses in tax accounting, it is necessary that the organization fully reimburse the employee for the overexpenditure.

An example of compensation to an employee for expenses in excess of the amounts issued to him on account. The organization applies a general taxation system. Income tax is calculated using the cash method

Secretary of Alpha LLC E.V. Ivanova purchased stationery for the organization. On March 24, she was given 2,800 rubles for these purposes, but she spent more. Ivanova submitted to the accounting department an invoice, a cash receipt, a receipt slip and an invoice for the amount of 3,000 rubles. (including VAT - 458 rubles).

On March 26, the head of Alpha approved Ivanova’s advance report. On the same day, the purchased stationery was transferred to household needs. On March 31, the organization’s cashier gave Ivanova 200 rubles. (3000 rubles - 2800 rubles), which the employee spent in excess of the money received on the report.

The Alpha accountant reflected these transactions as follows.

March 24:

Debit 71 Credit 50 – 2800 rub. – money was issued against Ivanova’s report.

26 March:

Debit 10 Credit 71 – 2542 rub. (3000 rubles – 458 rubles) – stationery purchased by the employee was received;

Debit 19 Credit 71 – 458 rub. – VAT on purchased stationery is taken into account;

Debit 68 subaccount “Calculations for VAT” Credit 19 – 458 rub. – VAT paid to suppliers is claimed for deduction.

March 31:

Debit 71 Credit 50 – 200 rub. – the employee was compensated for expenses in excess of the amounts given to him on account.

Expenses for the purchase of stationery when calculating income tax in the amount of 2542 rubles. Alpha's accountant took into account in March.

Situation: is it possible for an organization to take into account in expenses the cost of goods (work, services) purchased through an employee in a simplified manner, before he was compensated for the overexpenditure of the amounts issued for reporting for this operation?

No you can not.

When calculating a single tax under simplification, an organization has the right to recognize expenses only after they are actually paid. Payment for goods (work, services) is recognized as the termination of a counter-obligation by the purchaser to the seller, which is directly related to the delivery of goods (work, services). This is stated in paragraph 2 of Article 346.17 of the Tax Code of the Russian Federation. Article 346.17 of the Tax Code of the Russian Federation does not establish any specifics in the case of purchasing goods (work, services) through an employee (representative) of an organization. When the accountable pays for goods (work, services), the debt to the seller is repaid. However, until the overexpenditure is reimbursed to the accountable, it cannot be assumed that these expenses were paid by the acquiring organization (clause 2 of article 346.16, clause 1 of article 252 of the Tax Code of the Russian Federation). The organization will have actual expenses only after compensation for overexpenditures. Therefore, when calculating a single tax under simplification, in order to recognize expenses, it is necessary that the organization fully reimburse the employee for the overexpenditure. A similar point of view is reflected in the letter of the Ministry of Finance of Russia dated January 17, 2012 No. 03-11-11/4.

An example of compensation to an employee for expenses in excess of the amounts issued to him on account. The organization applies simplification. The organization pays a single tax on the difference between income and expenses

Alpha LLC applies a simplified tax system; it pays a single tax on the difference between income and expenses.

Secretary E.V. Ivanova purchased stationery for the organization (paper, staplers, pens, etc.). She was given 2,000 rubles for these purposes, but she spent 3,000 rubles. (including VAT - 458 rubles).

On February 11, the head of Alpha approved Ivanova’s advance report in the amount of 3,000 rubles.

On February 13, Ivanova was compensated in the amount of 1,000 rubles. (3000 rubles - 2000 rubles), which she spent in excess of the money given to her on account.

When calculating the single tax (on the difference between income and expenses) for the first quarter, the Alpha accountant included 3,000 rubles in expenses.

How to process reimbursement of expenses to an employee and avoid tax risks

The organization must have a general policy regarding the possibility of employees making such purchases. This may be an order that specifies the persons or positions who can make purchases on behalf of the organization. Or you can include such a clause in the accounting policy, personnel policy or cash circulation policy. These same internal acts can also describe the rules of document flow for the situation that is the topic of the article. The organization sets these rules independently. Below we will give some recommendations that may help when choosing to process an operation for reimbursement of expenses to an employee without reporting.

Since when purchasing goods at his own expense for work purposes, the employee can be said to act on behalf of the organization, then in accordance with paragraph 1 of Art. 183 of the Civil Code of the Russian Federation, it is necessary to draw up documents that will confirm that the organization has approved such a transaction. Such documents may be:

- An employee's application for reimbursement of expenses approved by the manager.

- A report on the funds spent with documents for purchase and payment attached to it (sales receipt, delivery note, invoice, etc.).

- An order on behalf of the manager to reimburse the employee’s expenses.

The organization must develop templates for these documents on its own (Clause 4, Article 9 of Law No. 402-FZ).

Also, a good way to avoid tax authorities’ quibbles regarding input VAT and recognition of income tax expenses may be to additionally issue powers of attorney for a number of employees to make sudden purchases on behalf of the organization. For expensive purchases, it is worth making sure that the seller, on the basis of a power of attorney, issues primary documents in the name of the organization, and not the employee.

However, most often employees make spontaneous purchases for work needs for small amounts. This could be stationery, some consumables for household needs, payment for small household services. Therefore, tax risks in these cases are most often insignificant. In order not to provoke questions from the tax authorities, you should avoid such situations and take care of issuing funds to employees on account in advance.

In addition, the employee himself may come under the attention of inspectors, because they may want to recognize compensation for expenses as income of an individual. However, this is illegal, since the employee does not have any economic benefit when performing such an operation

Letter of the Ministry of Finance of the Russian Federation dated 04/08/2010 No. 03-04-06/3-65 confirms the fact that compensation for money that an employee spent for the needs of the organization does not entail the emergence of a tax base for personal income tax.

For questions that interest tax authorities when checking settlements with accountable persons, read the article “Tax audit of settlements with accountable persons (nuances)”.