In 2021, all employers are faced with major changes to their current reporting practices.

If until this moment they reported on pension contributions to the Pension Fund, on contributions in case of temporary disability and injuries - to the Social Insurance Fund, and on accrued and paid taxes - to the Federal Tax Service, now all powers to administer contributions have been transferred to the Tax Inspectorate (except for contributions "for injuries"). In connection with this, Order No. ММВ-7-11/551 of the Federal Tax Service of 2016 approved a unified reporting form RSV-1. Dear readers! To solve your specific problem, call the hotline or visit the website. It's free.

8 (800) 350-31-84

According to the new rules, all employers, regardless of their form of ownership, rent it out: these can be either individual entrepreneurs with employees or legal entities.

Conditions for filling out reports

RSV-1 reporting is required to be submitted to the Tax Inspectorate by all legal entities and individuals who use hired labor in their work and are payers of insurance premiums. The form and reporting procedure for RSV-1 were approved by Order of the Federal Tax Service of 2021 No. ММВ-7-11/ [email protected]

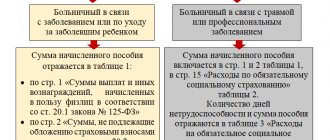

Part of the benefits for temporary disability on sick leave is paid by the employer from his own funds, the other part is compensated by the Social Insurance Fund.

If the amount of accrued benefits turns out to be less than the amount of benefits paid, then the employer has the right to receive compensation to his current account. In this case, the receipt of such compensation must be reflected in the RSV-1 reporting form.

Thus, the conditions for filling out RSV-1 reporting are as follows: the employer has the status of a legal entity or individual entrepreneur, he employs employees under an employment contract, or he engages persons for certain operations under a civil contract, he is a payer of insurance premiums.

Sv-experience: sample of filling out reports

The policyholder writes down the TIN only if he has information about it. Also, the middle name is not written if it is missing. The compiled document is endorsed by the head of the organization or individual entrepreneur.

His position must be indicated and his signature deciphered. Signing of the report by a representative is not allowed. The date of compilation is entered next to it in the format “DD.MM.YYYY”. Stamped upon availability. The policyholder must submit the completed reports himself. Methods for submitting SZV-M: advantages and disadvantages The policyholder is required to submit an electronic version of the report if he employs more than 25 people.

If the number of employees is less than 25 people, the report is submitted on paper. Depending on this, an acceptable method of delivery and delivery of SZV-M is selected.

- home

- For individual entrepreneurs

Deciphering the semantics of the letters “SZV-M” The letter combination “SZV-M” does not have a specific legalized decoding. It is generally accepted that this is a symbol for the type of unified reporting on which the policyholder reports to the Pension Fund. The symbol is reflected in the appropriate instructions for filling out the form. Actually, the document itself is referred to as “Information about the insured persons.”

The “SZV-M” characteristic is determined by the letter designation and code established by the standard. Based on this, we can distinguish the following interpretation of the letters in this combination:

- “B” means that the report data is transferred to the Pension Fund, i.e.

they are “incoming”. By the way, the encoding of documents coming from the fund contains “I”. - “M” - displays the reporting period, i.e.

Thus, these definitions are not identical. If the first is strictly tied to the full name of the object and can be guessed by its meaning, then the second is not at all connected with the name of the object to which it relates, and may not be decipherable without a special key document.

What is the meaning of the abbreviation SZV-M? In thematic Internet communities there are heated debates about what the decoding of the SZV-M form is. The most common options:

- information on earnings (remuneration) submitted monthly;

- information about the insured (incoming), submitted monthly, with explanations of the abbreviation:

- “B” - incoming information (submitted to the Pension Fund); the letter “I” is used to encode documents originating from the Pension Fund;

- “M” - indicates the frequency of reporting,

i.e.

How to fill out the RSV form correctly

The RSV-1 calculation contains information that is the basis for the calculation and payment of insurance premiums from the 1st quarter of 2017. One of the sections of the report is devoted to insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity.

It consists of a title page and three sections indicating contributions for pension, medical and social insurance of employees, as well as personalized information.

In the RSV-1 form, it is necessary to fill out only those sections in which the employer has something to transfer. For example, if an employer does not have contributions with additional tariffs, then he does not fill it out and submit it to the inspectorate.

After the employer submits a report on contributions to the Federal Tax Service, the inspectorate transmits it to the territorial division of the Social Insurance Fund (Appendix 2-4 to Section 1 with information on accrued contributions and benefits). Therefore, the employer should take into account that the figures calculated for contributions and those transferred to the Social Insurance Fund to receive compensation must be the same.

Sample of filling out RSV with sick leave in 2021

The report must be submitted for each quarter, even if no activity was carried out and no salaries were accrued. What is included in the DAM Calculation of insurance premiums includes a fairly large number of sheets, which, however, are required to be filled out by not all companies. The DAM contains several sheets that must be filled out by all employers, while other sheets are used only as needed.

How to indicate compensation from the Social Insurance Fund in 2021 when filling out the RSV

Before sending to the tax office, the form will be tested by all Federal Tax Service verification programs. Try it for free: Payers of mandatory insurance premiums, that is, policyholders, are companies and their separate divisions, individual entrepreneurs, heads of peasant farms:

The amounts of employer expenses reimbursed by the territorial bodies of the Social Insurance Fund for the payment of insurance coverage for compulsory social insurance in case of temporary disability and in connection with maternity are indicated in line 080 “Reimbursed by the Social Insurance Fund for expenses for the payment of insurance coverage” of Appendix No. 2 to Section 1 of the RSV (clause 11.14 of the Procedure, approved by Order of the Federal Tax Service dated October 10, 2021 No. ММВ-7-11/ [email protected] ).

Based on the results of the reporting or billing period, it may turn out that the amount of expenses incurred by the policyholder for the payment of benefits at the expense of the Social Insurance Fund exceeded the total amount of accrued insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity. The difference that arises can either be offset against upcoming social insurance payments, or reimbursed by the territorial body of the Social Insurance Fund (clause 9 of Article 431 of the Tax Code of the Russian Federation). Where is compensation from the Social Insurance Fund reflected in the RSV?

We recommend reading: VPD for Military Personnel in 2021 in the Southern District

The procedure for filling out the DAM when receiving compensation from the Social Insurance Fund 2021

- “1” - “amount of insurance premiums payable to the budget”, if the amount calculated according to the above formula is ≥0;

“2” - “the amount of excess of expenses incurred by the payer for the payment of insurance coverage over the calculated insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity”, if the amount is according to the formula for the 1st half of 2021.

- the number of insured persons to whom income was paid;

- the amount of income paid for the half-year each month of the second quarter, broken down;

- payments for which insurance premiums were not calculated (the list can be found in Article 422 of the Tax Code of the Russian Federation);

- income within the limit.

How to reflect sick leave in RSV-1

According to the procedure for filling out the reporting form RSV-1, the amounts of insurance premiums for insurance in connection with temporary disability and maternity are prescribed in Appendix 2 to Section 1.

Line 060 displays accrued contributions from the beginning of the year on an accrual basis , including for the reporting period (quarter) with a monthly breakdown. Line 070 records benefits that have been accrued since the beginning of the year on an accrual basis, including for the reporting period (quarter) with a monthly breakdown.

According to clause 11.14 of the Procedure, line 080 indicates the amount of compensation from the Social Insurance Fund in the column that corresponds to the month of receipt of the actual compensation. For example, if expenses are compensated by the fund in April, then this is displayed in the column for the first month of the 2nd quarter.

Line 090 of Appendix No. 2 indicates the amount calculated using the following formula : accrued contributions minus expenses for the payment of temporary disability benefits plus the amount of compensation received from the Social Insurance Fund for the reporting period.

According to the above calculations, either a negative or a positive value can be obtained. The employer should take into account that if the difference is negative, then he does not need to put a minus in front of the number.

The sign of the resulting difference is indicated using the numbers 1 or 2. If the value is set to “1”, this indicates that the contributions are more than the costs of insurance compensation for workers, “2” - the employer’s costs are more than the accrued contributions. Accordingly, if the value according to the formula for line 090 is negative, then the number “2” is entered.

If the amount is positive, this means that the employer must make an additional payment to the budget; if it is negative, then he will be reimbursed from the budget.

If the employer remains in debt, then he fills out one of the lines: 110, 111, 112, 113. When he has an overpayment, then fill out lines 120, 121, 122, 128. At the same time, these lines are not filled in: that is, the employer can or must budget, or overpay into it.

If there is a discrepancy between the data from the DAM report and the financial statements, accountants often have questions about whether the form has been filled out correctly. Typically, a discrepancy arises between the actual state of affairs and the figure indicated in column “090”.

For example, if the Fund has already reimbursed the employer for expenses, and when filling out the reporting form it turned out that the company owes the Social Insurance Fund a larger amount than in reality (after all, reimbursed expenses are added to accrued contributions), then there is no error in this. The employer will have to pay only accrued contributions to the budget , and not the amount from the final line 110 or 90 of the DAM report.

If the costs of temporary disability benefits were taken into account by the employer last year, and the employer received compensation in the current year, then the report is also filled out in the standard manner.

In the above formula, it does not matter for what period the employer received compensation; it is taken into account in the month of actual receipt. This position is confirmed by the explanatory letter of the Federal Tax Service No. BS-4-11 / [email protected] dated 2021. A similar conclusion can be drawn based on the analysis of Art. 34 of the Tax Code, which provides for the offset of expenses for temporary disability and maternity benefits against upcoming payments.

Most accounting programs today are configured to automatically check all ratios and prevent you from filling out lines incorrectly. But if the employer fills out the reports independently, then the control ratio is given in the Federal Tax Service Letter of 2021 No. GD-4-11 / [email protected]

Sample document: an example of filling out the RSV with sick leave can be found here.

Also, the employer can always find out whether taxes have been paid correctly by ordering a reconciliation of calculations from the Federal Tax Service. If the accounting data matches the reconciliation results, then there is nothing to worry about.

New reporting forms for personalized accounting

S. E. Nesterov Magazine “Payment: Accounting and Taxation” No. 8/2010

On June 21, 2010, the draft Resolution of the Board of the Pension Fund “On Amendments to the Resolution of the Board of the Pension Fund of the Russian Federation dated July 31, 2006 No. 192p” was posted on the official website of the Pension Fund. At the same time, the closing date for receiving expert opinions from independent experts was determined - June 29, 2010. In this article we will talk about what the new forms look like and what to pay attention to when filling out personalized accounting information. It should be noted that at the time of publication of the material in the journal, the new forms had not been officially approved, despite the fact that there was very little time left for submitting reports - until August 1.

As part of the reporting on personalized accounting, the following forms must be submitted to the Pension Fund:

– SZV-6-1 “Information on accrued and paid insurance contributions for compulsory pension insurance and the insurance period of the insured person” (submitted if in the reporting period it is necessary to indicate leave without pay, and (or) receipt of temporary disability benefits, and (or) the work of the insured person with the need to fill in the details “Territorial working conditions (code)”, “Special working conditions (code)”, “Calculation of the insurance period”, “Conditions for the early assignment of a labor pension”) (see page 39 );

– SZV-6-2 “Register of information on accrued and paid insurance contributions for compulsory pension insurance and the insurance experience of insured persons” (formed for insured persons who do not have special features of accounting for their experience in the reporting period) (see page 40);

– ADV-6-3 “Inventory of documents on accrued and paid insurance premiums and the insurance experience of insured persons, transferred by the policyholder to the Pension Fund of the Russian Federation” (submitted by the insured (employer) as part of a bundle of incoming initial (corrective, canceling) documents containing information on accrued and paid insurance premiums for compulsory pension insurance and the insurance period of the insured person, submitted starting from 2010) (see page 41);

– ADV-6-2 “Inventory of information transmitted by the policyholder to the Pension Fund of the Russian Federation” (contains data in general on the policyholder and accompanies packs of documents and registers of incoming initial and corrective (cancelling) information ADV-6-3, SZV-6-1, SZV- 6-2) (see page 42). Individual information for assigning a pension must be submitted in the SPV-1 form. A pack of SPV-1 must be accompanied by an inventory in the form ADV-6-3.

It should be noted that the forms SZV-6-1, SZV-6-2, ADV-6-3, ADV-6-2 replaced the usual forms SZV-4-1, SZV-4-2, ADV-6-1 , ADV-11.

The main difference between the new forms is that they must indicate not only the accrued amount of insurance premiums of the insured person, but also the amount paid in the reporting period.

The SZV-6-1 form is similar to the SZV-4-1 form, the SZV-6-2 form is similar to the SZV-4-2 form. The difference is that in forms SZV-6-1 and SZV-6-2 there is no column to indicate the number of days of leave without pay and temporary disability. Now these periods should be reflected in the SZV-6-1 form as a separate line indicating the dates (from which to which) and the corresponding code in the column “Calculation of insurance experience/Additional information”:

– VRNETRUD – period of temporary incapacity for work;

– ADMINISTR – leave without pay. Particular attention should be paid to working in territorial conditions. Previously, for employees who worked in the regions of the Far North and localities equivalent to them (or in other special territorial conditions), and who had one period of service, it was possible to submit information on the form SZV-4-2, indicating in the accompanying inventory ADV-6- 1 corresponding detail “Territorial conditions” (RKS, ISS and additionally details for radioactive contamination zones). In the new reporting forms, it is necessary to create a separate pack of SZV-6-1. In addition, according to territorial conditions, in addition to the details, it is required to indicate when working in part-time mode the share of the rate (in the electronic file for this it is proposed to use the “Coefficient” parameter, which was used in old forms for some time to indicate the regional coefficient), and when working in the mode part-time work week – reflect periods of work based on actual time worked. Another difference that should be noted is that the new reporting provides that, due to the emergence of new tariffs, an organization may have more than one category code of the insured person. Let us recall that from 2002 to 2009, the HP or CX codes were used for all employees. Now the classifier of codes for categories of insured persons contains the following positions:

– NR – general category of workers;

– Farmers – employees of agricultural producers (in accordance with the criteria of Article 346.2 of the Tax Code of the Russian Federation), organizations of folk arts and crafts and family (tribal) communities of indigenous peoples of the North, applying a reduced tariff in accordance with clause 1, part 2 of art. 57 and paragraph 1, part 1, art. 58 of Federal Law No. 212-FZ (valid until December 31, 2014);

– OZOI – employees of employers who have the status of residents of technology-innovative SEZs and make payments to individuals working in the territory of the technology-innovation SEZ; workers - disabled people of groups I, II, III, etc. (reduced tariff in accordance with clause 2, part 2, article 57 and clause 2, 4, part 1, article 58 of Federal Law No. 212-FZ is valid until 31.12 .2014);

– Unified Agricultural Tax – employees of organizations and individual entrepreneurs on Unified Agricultural Tax, applying a reduced tariff in accordance with clause 3, part 2 of Art. 57 and paragraph 3, part 1, art. 58 of Federal Law No. 212-FZ (until December 31, 2014);

– USEN – employees of organizations and individual entrepreneurs on the simplified tax system and special regime in the form of UTII (clause 2, part 2, article 57 of Federal Law No. 212-FZ);

– FL – indicated for payers of insurance premiums who do not make payments to individuals (for example, individual entrepreneurs without employees). The need to use different codes arises if an organization uses several tariffs for calculating insurance premiums. Please note that when submitting a report on insurance premiums for the first quarter of 2010, organizations applying different insurance premium rates filled out not only section 2, but also section 3 in the RSV-1 form, or filled out two tables in section 2. For employees, when filling out individual information, you must use the category code of the insured person corresponding to the tariff. Moreover, one insured person may have two forms of information with different codes in the reporting period, for example, if his disability was removed during the reporting period.

Please note: Information with different codes must be formatted in different packs.

Form ADV-6-3 (similar to form ADV-6-1) is attached to the package of documents of form SZV-6-1, but it is not attached to SZV-6-2. Form ADV-6-2 contains amounts for the entire organization and is similar to form ADV-11. However, the content of the new form is different: it lists by name all the bundles of information submitted to the Pension Fund of the Russian Federation, indicating the number of insured persons and the amounts of accrued and paid insurance premiums in the bundle. The total amounts for all packages must coincide with the amounts of accrued and paid insurance premiums indicated for the corresponding period in the RSV-1 form.

Question: How can I determine the total amount of contributions paid? For what period should transfers be indicated: until June 30 or until July 15?

Resolution of the Board of the Pension Fund of the Russian Federation dated July 31, 2006 No. 192p stipulates that the forms of documents for individual (personalized) accounting in the compulsory pension insurance system must indicate the amount of paid insurance contributions for the insurance part and the funded part of the labor pension for the last three months (for 2010 - six months) of the reporting period. When presenting information for the reporting period (1st half of the year) of 2010 (from 01/01/2010 to 06/30/2010), the “Paid” indicator includes the amount of insurance premiums paid for 2010 to 06/30/2010. In this case, the total amount of insurance premiums for all insured persons of the organization, indicated in individual information, must be equal to the amount entered in line 140 of the RSV-1 calculation.

Question: What amount for employees should be reflected in the “Paid” column of the SZV-6-2 form? How to calculate the premiums paid for each insured person if the organization transfers the contributions in one payment?

Employees have equal rights to the contributions paid for them, therefore the amount paid must be divided in proportion to the accrued amounts among all employees. The calculation of the amounts paid for each insured person is carried out using the payment coefficient, which is calculated as the ratio of the amount paid in the reporting period for the organization as a whole to the amount accrued for the organization as a whole. Since the amount to be transferred must be rounded to the nearest whole ruble, there may be inconsistencies with the accrual amounts, which are made in kopecks. When admitted to the Pension Fund of Russia, such a discrepancy will be considered an error. In this regard, the kopecks resulting from rounding will have to be added by one of the employees.

Let us note that today there are no regulatory documents regulating personal accounting of insurance premiums paid by an organization. You can refer to the Decree of the Government of the Russian Federation dated June 12, 2002 No. 407, which states that the received amounts of current payments for insurance premiums, as well as payments for insurance premiums for past periods, are distributed to individual personal accounts of insured persons in proportion to the amounts of accrued insurance premiums. This resolution approved the forms of individual information.

Question: During the reporting period, the employee had leave without pay, and he belonged to two categories (general taxation system and UTII). How to correctly reflect leave without pay in the SZV-6-1 form? What category code of insured persons should he be assigned to?

Vacation without pay must be reflected in form SZV-6-1 both according to the general taxation system (code NR) and according to UTII (code USEN).

Question: How does the organization’s report (general taxation system) reflect information about disabled people for whom reduced insurance premium rates are applied?

In the form SZV-6-1 (or SZV-6-2 - depending on length of service) for disabled people working on the general taxation system, you should use the insured person category code OZOI and the amount of contributions calculated at a reduced rate. For all other employees, the insured person category code HP is used.

Question: Which category code of insured persons should be used for disabled people working under the simplified tax system or special regime in the form of UTII: OZOI or USEN?

If sections 3 and 4.1 are completed in the RSV-1 form, then the OZOI code must be used. If tariff code 05 is indicated in the RSV-1 (when applying the simplified tax system or paying UTII), sections 3 and 4.1 of the said form are not filled out and the code will be the same as for all employees - USEN.

Question: When filling out form SZV-6-1, is it necessary to break down the length of service of employees who are granted additional unpaid days of rest for working on weekends?

If work on a day off is paid and, therefore, insurance premiums are calculated on the payment amount, then there is no need to show an additional unpaid day of rest, since it is provided in exchange for a worked day off. It is mandatory to highlight leave without pay as a separate line in the length of service in the case of special working conditions or if there are grounds for early assignment of a pension. Question: What should I do if a dismissed employee brought a certificate of incapacity for work within 30 days after dismissal?

In this situation, it is necessary to fill out form SZV-6-1. In this case, the period of temporary disability must be highlighted as a separate line indicating the code VRNETRUD in the column “Calculation of length of service/Additional information”. The end date of the last line of service must correspond to the date of dismissal.

Question: How to reflect data on individuals working under contract agreements in reporting forms?

When filling out the SZV-6-2 form, in the “Work period” column, you should reflect the dates of the contract. If there were several contracts, then for this individual it is necessary to fill in the lines for the number of concluded contracts, indicating the validity dates of these contracts in the column “Work period”.

Question: Are there any special features when filling out reporting forms if an enterprise operates on a shortened work week?

In the absence of the need to calculate preferential length of service and the presence of accrued insurance contributions, it does not matter whether the working week was full or shortened. If for employees it is not required to reflect information in the columns “Territorial conditions”, “Special working conditions”, “Calculation of length of service” or “Conditions for early assignment of a pension”, when filling out the SZV-6-2 form, the period from 01.01 is indicated. 2010 to 06/30/2010 or the period with the dates of hiring and dismissal of employees.

Question: How can I include in the report employees who were on sick leave while the organization was operating on reduced working hours?

For such employees, when filling out the SZV-6-1 form, the period of temporary disability must be highlighted as a separate line indicating the code VRNETRUD in the column “Calculation of insurance length/Additional information”.

Question: Is it necessary to submit personalized accounting information if the organization has only a director, who is the only founder, with whom an employment contract was not concluded and to whom wages were not paid?

Individual information with dashes is not submitted to the Pension Fund. Since wages were not accrued, therefore, insurance premiums were not accrued or paid. Consequently, there is nothing to reflect on the personal account of the insured person. Let us remind you that you can submit form RSV-1 with dashes.

Question: How do I fill out a report for an employee fired in 2009 who was awarded a bonus based on the year’s performance in 2010?

For a dismissed employee, you must fill out form SZV-6-2, in which you should indicate only the amounts of accrued and paid insurance premiums, while the column “Period of work” does not need to be filled out, since in 2010 such an employee does not have work experience.

Question: How will periods of temporary disability be reflected in the new reporting?

Let us remind you that previously, when submitting personal information, it was necessary to indicate the total number of days on sick leave. In the new forms, a special code is introduced to reflect information about periods of temporary disability. For an employee who was on sick leave during the reporting period, fill out form SZV-6-1, which indicates the period (from dd.mm.yyyy to dd.mm.yyyy) of sick leave and enters it in the column “Calculation of insurance length/Additional information” code VRNETRUD.

Question? Is it possible to submit the report for the first quarter of 2010 before August 2, since July 31 is a day off? Federal Law No. 213-FZ stipulates that policyholders for the first reporting period of 2010 (half-year) provide information provided for by the Federal Law “On individual (personalized) registration in the compulsory pension insurance system” before August 1, 2010, for the second reporting period of 2010 year (calendar year) – until February 1, 2011. The law does not clearly state the transfer of the reporting deadline from a weekend to the first working day, as is done, for example, in Federal Law No. 212-FZ for the RSV-1 form. To avoid disagreements with regulatory authorities, we recommend submitting the report before August 1. New reporting forms >>

Fresh materials

- Clarification on 4 FSS When it is necessary to adjust 4-FSS The calculation presented in the FSS in form 4-FSS does not need adjustments if...

- Social tax 2021 Tax accrualIn accounting, the amounts of advance tax payments are reflected in the credit of account 69 (68)…

- Tax planning Tax planning in an organization Tax planning can significantly affect the formation of the financial results of an organization,…

- Why do they buy gold? Selling gold competently is a process that will require you to spend some free time. It will be necessary to find out...

DAM for the 2nd quarter of 2021

It contains information about all contributions, except for injuries. Before sending the ERSV to the tax office, check payments from section 1 with income in 6-NDFL. During a desk inspection, inspectors will do the same.

Calculation of insurance premiums for the 1st quarter of 2021: form and sample filling

We will describe in detail how to do this in an example. In the final line 090 of Appendix 2, you must indicate the amount calculated using the following formula: This reflects the difference between accrued contributions and expenses for payment of benefits plus the amount of compensation from the Social Insurance Fund for the reporting period. Calculating the difference can result in either a negative or a positive number.

- on line 080 - the amount of compensation received from the Federal Social Insurance Fund of Russia (clause 11.14 of the Procedure);

- on line 070 - the amount of expenses incurred by the company for the payment of insurance coverage (clause 11.13 of the Procedure);

- on line 090 - the result of reducing the amount of insurance premiums for the costs of paying insurance coverage.

- on line 060 - the amount of accrued insurance premiums (clause 11.12 of the Procedure);

Thus, you need to show in Appendix 2 (section XI of Appendix No. 2 to the Order of the Federal Tax Service dated 10.10.2016 No. ММВ-7-11/[email protected]): - on line 060 - accrued contributions from the beginning of the year, for the reporting period from monthly breakdown for the last quarter; - on line 070 - accrued benefits from the beginning of the year, for the reporting period with a monthly breakdown for the last quarter;

Sample zero calculation for insurance premiums 2020

The form and reporting procedure for RSV-1 were approved by Order of the Federal Tax Service of 2016 No. Opinion of a lawyer Dmitry Ivanov Legal Support Center This article talks about standard ways to resolve the issue, but each case is unique. If you want to find out how to solve your particular problem, call:

1. Title page. Here you must indicate the TIN, KPP and the full name of the organization - the payer of insurance premiums or full name. IP. We pay special attention to the reporting period code. In the reporting for the 3rd quarter of 2021, we indicate the code “33”. You should also write down the reporting year and the code of the tax authority to which the report was sent.