Who should I give it to and what is it?

A report on the average number of employees (ASH) must be submitted by all organizations and individual entrepreneurs (regardless of the chosen taxation system) that had employees in the calendar year.

Newly created organizations (not individual entrepreneurs) need to submit the CHR report twice: once after creation, and the second time at the end of the year.

Individual entrepreneurs without employees, starting from January 1, 2014, do not need

.

Note!

2020 was the last year in which a CHR report had to be filed. From 2021, it is abolished by law dated January 28, 2021 No. 5-FZ. Information on the number of employees will be transmitted to the Federal Tax Service as part of the calculation of insurance premiums.

What will happen if the deadline for submitting the SSC report is violated?

All organizations in case of late submission of a report receive a fine in accordance with paragraph 1 of Article 126 of the Tax Code of the Russian Federation. You will have to pay a little - 200 rubles. Additionally, the director or chief accountant may bear financial liability. They are given a fine of 300 to 500 rubles.

Such responsibility is provided for absolutely any legal entity, even if it does not yet have employees. In this case, reporting must be submitted, it will simply be zero.

Similar articles

- Information on the average number of employees

- Average headcount for newly created organizations

- Average number of employees - when to submit?

- How to calculate the average number of employees per month?

- Information on the average number of employees

The deadline for the completion of the SSR is in 2021

Information on the average payroll number is submitted by:

Existing individual entrepreneurs and organizations

Based on the results of the calendar year, no later than January 20.

For 2021, the SChR information must be submitted by January 20, 2020

.

Newly created organizations

No later than the 20th

the month following the month in which the organization was created.

Upon liquidation of an organization or closure of an individual entrepreneur

No later than the official date

liquidation of an organization or closure of an individual entrepreneur.

Who to consider

The Declaration has not undergone major changes, but the legislator regularly amends regulations. The form was approved by Order of the Federal Tax Service of Russia dated March 29, 2007 No. MM-3-25/ [email protected] , but the requirements for calculation are contained in the Instructions set forth in Rosstat Order No. 772 dated November 22, 2017.

In order to correctly calculate the average headcount for individual entrepreneurs with employees, it is necessary to follow certain rules. The main requirement: citizens with whom an employment contract has been concluded are taken into account. This is a general rule that requires clarification.

What should an entrepreneur remember about the average headcount?

| Rule | Explanations |

| Submitting reports on average headcount | Mandatory for entrepreneurs who are employers, that is, concluding employment contracts with employees |

| Where to take it | Federal Tax Service Inspectorate at the place of registration |

| Deadline | Until January 20 for the reporting year (01/20/2020), until the 20th day of the month following the month in which registration occurred, for the time elapsed from that moment |

| Responsibility for failure to provide | Fine in the amount of 200 to 500 rubles |

Failure to provide the form will be a reason not only for a fine, but also for an inspection.

Where to take the SChR in 2021

A report on the average number of employees is submitted to the tax authority:

- Individual entrepreneur - at the place of residence;

- LLC - at its location (legal address).

The address and contact details of your tax office can be found using this service.

Note

: the average number of employees by location of separate units does not need to be submitted. Data on department employees is indicated in a general report for the entire organization, which is submitted to the Federal Tax Service of the head office.

How to fill out a document

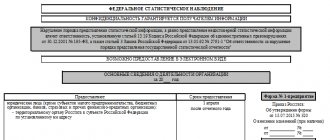

In the KND form 1110018 the following must be filled out:

- TIN, KPP, full name of the organization or full name. individual entrepreneur;

- the name of the territorial division of the Federal Tax Service to which the report is submitted, and its code;

- the date as of which the indicator was calculated;

- data on the number of hired personnel;

- signature and seal (if available).

There is no need to fill out the lower right block; it is intended for a tax official.

The rules for filling out the KND form 1110018 “Average number of employees” are given by the Federal Tax Service of the Russian Federation in letter dated April 26, 2007 No. CHD-6-25/ [email protected]

Recommendations for filling out individual fields:

- In the “TIN” field indicate the unique identifier specified in the registration certificate.

- The “Checkpoint” field can only be filled in by legal entities.

- In the “Tax Inspectorate Name” field, you must indicate the name of the department. For example, “Inspectorate of the Federal Tax Service of Russia No. 43 for Moscow.” The tax code always consists of 4 digits.

- In the “Name of Taxpayer” field, indicate the full name of the legal entity or individual entrepreneur.

- When indicating the date as of which the headcount indicator is displayed in the KND form 1110018, it is necessary to take into account the requirement specified in the footnote. If the data is indicated for the past calendar year, the taxpayer enters January 1 of the current year. Newly registered organizations indicate the first day of the month following the month of registration.

KND 1110018 “Information on the average number of employees”: sample filling

Methods for filing SCR in 2021

The average number of employees can be submitted:

- In paper form (in 2 copies). One copy will remain with the tax office, and the second (with the necessary marking) will be returned. It will serve as confirmation that you have submitted the declaration.

- By mail as a registered item with a description of the contents. In this case, there should be an inventory of the investment and a receipt, the number in which will be considered the date of delivery of the number.

- In electronic form via the Internet (under an agreement through an EDF operator or a service on the Federal Tax Service website).

note

, when submitting SCR information in paper form, some Federal Tax Service Inspectors may additionally require you to attach a file with an electronic version of the report on a floppy disk or flash drive.

Form and sample SSC report for a new organization

A report on the average headcount of a newly created organization must be submitted on the form established by higher authorities - KND form 1110018. It was approved by the Federal Tax Service, which is recorded in order No. MM-3-25 / [email protected] dated March 29, 2007.

The document itself is quite simple. But new organizations may have questions related to filling it out. The answers to them can be found in the filling recommendations established by the Federal Tax Service in its letter No. CHD-6-25 / [email protected] dated April 26, 2007.

In order to correctly display all the information and the average number of employees of the newly created organization, the sample presented below should be used by those who have never encountered filling out such documents.

Similar articles

- Average number of employees of individual entrepreneurs without employees

- How to calculate the average number of employees per month?

- Average number of employees - when to submit?

- Average headcount in 2021

- Deadline for submitting the average number of the newly created organization

How to calculate the average number of employees (formula)

To calculate the average number of personnel for a calendar year, you must first make a calculation separately for each month:

Step 1. Calculate the number of full-time employees

To do this, we use the following formula:

Ch1 = Chm / Dm

World Cup

– the sum of the average number of employees for each day of the month (that is, it is necessary to calculate the average number of employees for each day of the month and add it up);

Dm

– the number of calendar days in a month.

The result does not need to be rounded

.

The number of employees for a weekend or holiday is taken to be equal to the number for the previous working day.

When calculating the average payroll number, they are not taken into account

:

- External part-time workers (employees whose main place of work is another organization).

- Individuals working under GPC agreements (of a civil nature).

- Women on maternity or child care leave.

- Employees on study leave without pay.

If an employment and civil law contract is concluded with an employee at the same time, then he must be taken into account as one person in the calculation.

Employees working part-time at the initiative of the employer

(probationary period and homeworkers), as well as workers for whom the law establishes

a shortened working day

(including disabled people), are taken into account as

whole units

.

Step 2. We count the number of employees who worked part-time

Employees working under an employment contract part-time (including those who did not come to work due to illness or business travel) are taken into account in proportion to the time worked

.

This is done according to the following formula:

Ch2 = Total / Trd / Drab

Total

– the total number of man-hours worked by these employees in the reporting month.

Trd

– length of the working day, based on the length of the working week established in the organization. For example, with a 40-hour five-day work week, this figure will be 8 hours, with a 36-hour week - 7.2 hours, and with a 24-hour week - 4.8 hours.

Drab

– the number of working days according to the calendar in the reporting month.

The result does not need to be rounded

.

Example

. The employee worked part-time (4 hours) for 22 working days per month, while the working day in the organization is 8 hours. The average number in this case will be equal to:

0,5

(88 / 8 / 22).

Step 3. Calculate the average number of employees for the calendar year

To calculate the average number of employees, it is necessary to add up the headcount indicators ( Ch1

and

Ch2

) for all months of the year and divide the result by

12

months.

If the result is a non-integer number, it must be rounded

(discard less than 0.5, and round 0.5 or more to the whole unit).

Calculation example

Initial data

LLC "Company" has a 40-hour, five-day work week.

In 2021, from January to November, 15 people

(in December there were 11 of them left, since 4 people were laid off due to staff reduction).

For September and October, fixed-term part-time employment contracts were concluded with 5 new employees, according to which they worked 4 hours daily.

Throughout the year, the organization employed 3 external part-time workers who are on the payroll of another company.

Calculation of average headcount

In each month (from January to November) the average number of full-time

, was equal to

15 people

(external part-time workers are not taken into account in the calculation).

In December, the number of such workers was 11 people

.

part-time during the year

:

There were 22 working days in September and October, so the number in each of these months is:

(4 hours x 5 workers x 22 working days) / 8 hours / 22 working days = 2,5

Below is a table of the average number of employees for each month, taking into account the results obtained:

| Month | Average headcount | Month | Average headcount |

| January | 15 | August | 15 |

| February | 15 | September | 17,5 (15 + 2,5) |

| March | 15 | October | 17,5 (15 + 2,5) |

| April | 15 | November | 15 |

| May | 15 | December | 15 |

| June | 15 | Total | 181 people |

| July | 15 |

Thus, for 2021 the average number of employees is: 15 people

(181 people / 12 months).

Which employees are not taken into account when calculating the average headcount?

The average number of employees does not need to take into account women on maternity leave. In addition, persons who took leave in connection with the adoption of a newborn are not taken into account. Finally, employees who have taken parental leave are not taken into account (except for those who work part-time or at home while receiving benefits). Students and applicants who have taken leave without pay, as well as some other categories of workers (their list is given in paragraph 78 of the Instructions) should not be taken into account.

External part-time workers are excluded from the average headcount, that is, employees whose main place of work is another company or another individual entrepreneur. Persons working under civil contracts are also not included in the calculation. In a situation where the same person works simultaneously under an employment contract and a contract, he must be counted once in the average headcount.

Why is the average number of tax officials needed?

The average headcount indicator is involved in the calculation of some taxes, and the method of reporting to the tax authorities also depends on it.

So, for example, individual entrepreneurs and organizations with more than 100 people in a calendar year cannot use the simplified tax system and UTII.

For individual entrepreneurs with a patent, the average number of employees for all types of activities should not exceed 15 people.

There are other situations in which the exact number of employees may be of interest to tax authorities.

Who should provide information on the average number of employees

Both organizations and ordinary individual entrepreneurs are required to submit the necessary data on the average number of employees to the tax office. But there is a slight difference.

An individual entrepreneur must send information about the number of his employees only if hired personnel were used in the past year. For large organizations the conditions are more stringent. They must send the relevant information regardless of whether they have hired employees or not (this is indicated in the letter of the Ministry of Finance dated 02/04/2014 No. 03-02-07/1/4390).

Companies are required to report the number of employees annually, even if the data has not changed since the previous year.

Filling procedure and sample

A company or private businessman must indicate the following information in the certificate:

- TIN.

- Checkpoint (for companies only).

- Full name and code of the territorial tax service where the certificate is submitted.

- The full name of the company, in accordance with its registration documents, or the full name (the latter - if available) of a private businessman without abbreviations.

- The date as of which the average payroll number is given is indicated. For long-established firms and businessmen, the indicator must be calculated and current as of January 1 of the current year. For newly opened companies and entrepreneurs, the value of the indicator is reflected as of the first day of the month following the month of registration.

- The manager must write down his full name, affix his personal signature, and also certify it with a company stamp. It is necessary to indicate the date of preparation of the document.

- A private businessman must indicate his full name, sign the document with a personal signature and indicate the date of signing.

- If the report is filled out by a representative, he must indicate his data. If the representative is an individual, he indicates his full name in accordance with the identification document. If the representative is a company, the head of this company must affix his personal signature and certify with a company stamp. At the end, you must indicate the name and number of the document that confirms the authority of the representative. A copy is attached to the form.

A sample certificate of the average number of employees is given below:

Similar articles

- Certificate of average number of employees - sample

- KND 1110018

- Information on the average number of employees

- Certificate of number of employees of the organization - sample

- Information on the average number of employees