New procedure for the return of insurance premiums for compulsory health insurance

On December 31, 2021, the Constitutional Court recognized the restriction of the employer’s right to receive from the budget overpaid funds for compulsory pension insurance (OPS) as inconsistent with the Constitution of the Russian Federation. The reason for the refusal is that information about the amounts paid is posted on the individual personal accounts of the insured persons. The government was obliged to correct the situation and ensure that overpayments of insurance premiums are offset in 2021, including for compulsory insurance.

The State Duma adopted amendments to the Tax Code of the Russian Federation aimed at establishing a new procedure for the reimbursement of insurance premiums for compulsory health insurance. Tax authorities will take into account the structure of the insurance payment tariff (its joint and several parts) and the fact whether a particular insured person has an insured event. If the employee has retired and a change in the information on the personal account will lead to a decrease in pension benefits, the amount of overpaid (collected) payments to the compulsory pension insurance will not be returned to the employer. In all other cases, the policyholder will receive compensation based on an application for the return of this amount. The new rules will begin to work on January 1, 2021, after the law is signed by the president. Until then, the Federal Tax Service authorities consider all applications for compensation individually, based on the position of the Constitutional Court of the Russian Federation.

Updated instructions from ConsultantPlus

To guarantee a refund and not be refused, use a ready-made solution (here is free access):

Go to instructions

Reasons for not accepting benefits for credit

There are different types of credits: sick leave, maternity and child benefits. Why do they need to be counted at all? The funds are initially paid by the employer. However, the latter’s expenses are compensated by the Social Insurance Fund. Benefits are accepted based on the results of their verification. Paragraph 1 of Article 4.2 and paragraph 4 of Article 4.7 of Federal Law No. 255 “On Mandatory Social Insurance” dated December 29, 2006 states that the Social Insurance Fund may not accept benefits for deduction in these cases:

- Funds were paid based on incorrectly executed documents.

- Social security laws were violated.

- There is no documentation at all.

Question: The organization paid the employee a maternity benefit, the amount of which was not accepted by the Federal Social Insurance Fund of the Russian Federation. The organization is notified that the amount of maternity benefits not offset by the Federal Social Insurance Fund of the Russian Federation is subject to insurance contributions. Is this legal? View answer

FOR YOUR INFORMATION! The Social Insurance Fund may detect signs that the company has artificially created conditions for paying benefits. For example, these could be forged certificates of incapacity for work.

Options

If the Social Insurance Fund has not accepted benefits for deduction, there are two options:

- Challenging the decision.

- Making changes to accounting.

Options for action depend on the nuances of a particular situation.

Question: The Federal Social Insurance Fund of the Russian Federation refused to credit part of the maternity benefit due to the artificially inflated salary of the employee before maternity leave. The organization did not agree and sent documents to court. What is the procedure for assessing personal income tax during the trial? Should the policyholder, after the decision of the Federal Insurance Service of the Russian Federation on refusal, calculate personal income tax benefits from the refused amount and submit tax reports? View answer

Who makes the return decision?

The body making the decision on the return of overpaid insurance contributions, penalties and fines depends on the reporting period for which the policyholder filed an application for overpayment. When applying for reporting (calculation) periods that expired before 01/01/2020, the decision is made by the authorities of the Pension Fund - for payments to compulsory pension insurance and the Social Insurance Fund of the Russian Federation - for payments for temporary disability and injuries.

This happens in agreement with the Federal Tax Service. To do this, within 10 working days from the date of receipt of a written application for

refund of the overpayment, the authorized bodies make a decision and no later than the next working day send a notification to the territorial tax authority at the place of registration of the policyholder for the actual transfer of overpaid amounts of insurance contributions, penalties and fines (letter of the Ministry of Finance dated 06/09/2017 No. 03-15-05/36284). There are still 30 days for this.

The decision to return overpaid deductions, penalties and fines for reporting (calculation) periods formed after 01/01/2017 is made by the tax authority (Article 78 of the Tax Code of the Russian Federation). The algorithm is fully consistent with the return of overpaid taxes.

What you need to prepare for reimbursement of costs to the Social Insurance Fund

Reimbursement will only take place if the employer provides the territorial Social Insurance Fund with a full package of supporting documents.

The main forms are an application for the allocation of funds (compensation, reimbursement), a certificate of calculation and an explanation of expenses. All forms are recommended. If the policyholder has a need, he can modify the registers for his company by providing explanations to the Social Insurance Fund.

The calculation certificate and breakdown of expenses are analogues of tables 1 and 2 from the previous form of the 4-FSS report. The reference material (similar to Table 1), which is prepared for reimbursement purposes, indicates:

- the total amount of debt at the beginning and end of the reporting period (month, quarter, half year);

- the total amount of accrued insurance premiums;

- additional charges;

- expenses not accepted for reimbursement;

- funds spent on social security needs.

And this is not all that can be indicated in the certificate. Let us repeat once again - the form is not unified, and if you have a need to include information related to industry specifics, include and justify changes to the form.

The cost breakdown (similar to Table 2) provides a complete breakdown of all insurance costs for the employer. This is an important nuance - many people mistakenly include in the transcript only those expenses that they plan to compensate.

An application for the allocation of funds is a direct appeal to the insurance authority. The essence of the application is reimbursement of expenses, so we indicate all the related information in the text. We write down the full name of the policyholder, the reason for the application, the amount of costs to be reimbursed and the details for transferring money.

The last component of applying for reimbursement of expenses is the supporting documentation. The policyholder must justify the costs of social security for its employees, so you will have to provide all forms confirming the payments made. This is what the FSS will require from you:

- Temporary disability: work record book or employment agreement with an employee, sick leave, calculation of compensation.

- Pregnancy and childbirth: work record book or agreement, sick leave from the antenatal clinic, calculation of benefits, certificate of registration in the early stages of pregnancy, application and order for maternity leave.

- A one-time benefit for the birth of a child: a work record book or agreement, a certificate from the registry office about the birth of a child, an application for compensation, a certificate from the second spouse stating that his employer did not pay a similar benefit.

- Monthly childcare benefit for a child up to one and a half years old: work book or agreement, payment calculation, birth certificate, certificate from the second spouse stating that his employer did not pay a similar benefit.

- Social benefits (funeral): work book or agreement, certificate from the registry office, application.

The insurer can also compensate for the payment of additional days off to one of the parents if he needs care for disabled children who have not reached the age of majority.

The list of situations for reimbursement of expenses is closed. This means that the FSS does not provide any other grounds for compensation.

Social insurance specialists study the documents and issue a positive or negative verdict. If the decision is affirmative, the policyholder's expenses are reimbursed within ten days.

Counter checks on submitted applications are also common - FSS employees initiate on-site or desk control if the information provided is unfounded or incomplete. In such situations, compensation is transferred after verification activities are completed and all errors are corrected.

Sources:

On the procedure for calculating and paying insurance premiums

On the procedure for financial support for insurers' expenses

How to apply for an overpayment to the Social Insurance Fund

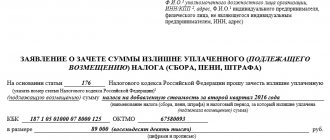

The FSS approved the application forms by order dated February 17, 2015 No. 49 (as amended on November 17, 2016)) in accordance with the norms of Part 1 of Article 21 of the Federal Law dated July 3, 2016 No. 250-FZ. It is impossible to issue a letter for refund of overpayment of insurance premiums in free form.

To return contributions for VNIM and injuries, you should contact the Social Insurance Fund with a prepared application for the return of overpayments on contributions in Form 23.

How to return erroneously transferred funds

Most often, such errors occur during transfers between individuals from card to card. And if there is no banking error, but only erroneous user actions, banks often do not take any measures to solve the problem, and all this falls on the shoulders of the client.

What urgent actions need to be taken

It should be remembered that the sooner you can contact the bank after an erroneous transaction, the more likely it is that this situation will be resolved easily and quickly.

As long as the funds have not been transferred to the incorrect account, the operation can be canceled. To do this you need:

- Contact the bank's support service as quickly as possible.

- Come to the office and submit an application.

In the application addressed to the head of the institution, you must indicate:

- Information about the applicant.

- Request for cancellation of the transaction and refund.

- The account where the funds should be returned.

Voluntary return

The case where funds were mistakenly transferred to a legal entity is more favorable. First, it is worth negotiating peacefully, but if the problem is not resolved, send an official complaint to the organization.

The claim can be submitted to the organization in person by putting an incoming mark on your copy, or sent by mail with notification. A legal entity is obliged to respond to the complaint in writing, but if this does not happen, it should contact law enforcement agencies.

The case where an error occurred in a transfer between individuals is much more complicated. The bank does not have the right to disclose personal information about its client, as a result of which the victim cannot contact the other party. In this case, you need to contact the police, who will make an official request to the bank.

A small life hack for users of modern banking services: in order to contact a person to whom funds were transferred by mistake, you can send a small amount (for example, a ruble) to the same account, and write a message in the comments to the payment.

If neither peaceful negotiations, nor a claim, nor an appeal to the police helps, the next step is to file a lawsuit.

Refund through court

In order to return erroneously transferred funds through the court, a standard statement of claim is drawn up, in which you must indicate:

- Information about the court district and the judge, the plaintiff and the defendant.

- Describe all events in detail.

- Regulatory acts on which the petition is based.

- Requirements for the court . All amounts must be supported by calculations.

- Application . All documents attached to the claim: transaction receipts, claims, screenshots.

In addition to the funds that appeared in the transfer itself, the applicant may also request reimbursement of other costs: legal costs, state fees.

If the case involves an amount of less than fifty thousand rubles, then the magistrate’s court will deal with it, and if more, then the district or regional court. Disputes between legal entities are resolved in arbitration court.

Refund of overcharged amounts

If the tax authorities excessively collect amounts for periods expired before 01/01/2017, the question arises of how to return the overpayment of insurance premiums from the tax office in 2021 in such a situation? The decision to return excessively collected payments to OPS and VNiM for these periods is made directly by the Pension Fund of Russia and the Social Insurance Fund. The norms of the Tax Code do not apply (letters of the Federal Tax Service of the Russian Federation dated July 27, 2017 No. ED-4-8/14778, dated June 20, 2017 No. GD-4-8/ [email protected] , letter of the Ministry of Finance dated July 19, 2017 No. 03-02-07 /2/ [email protected] ).

Things are different if the policyholder wants to know how to return the overpayment under the Social Insurance Fund in 2021 that arose after 01/01/2017. The procedure is determined by tax legislation. During this period, the decision is made by the tax authorities in accordance with the provisions of Article 79 of the Tax Code of the Russian Federation. It is enough to contact the Federal Tax Service Inspectorate in writing with a statement in the established form.

IMPORTANT!

There is no general algorithm for how to return insurance premiums from the Pension Fund in 2020. The Federal Tax Service will develop it after the amendments to the Tax Code of the Russian Federation enter into force.

Previous forms are partially relevant!

The forms of documents valid until the end of 2021 for the return and offset of insurance premiums through the Social Insurance Fund were adopted by order of the Social Insurance Fund dated February 17, 2015 No. 49. By the way, their names, number and names of forms are the same as from 2021 according to the FSS order in question dated November 17 2021 No. 457.

Please note that from 2021 the previous forms cannot be used for personal injury contributions. However, they remain relevant if it is necessary to return (offset) contributions for illness and maternity for reporting periods before January 1, 2021. Such a clause is given in the FSS order No. 458 dated November 17, 2021.

Refund of overpayment from FSS

Be careful: if you make a mistake in the KBK, you can clarify the code only within the budget of the Federal Social Insurance Fund of Russia. If the first three digits are “393,” then the budget administrator is the Social Insurance Fund. Such an error in the KBK can be clarified if, according to the information in field 24 “purpose of payment”, it is clear that the policyholder actually made errors in the payment order.

Confirmation of expenses under the Social Insurance Fund starting from 2021 under the credit system

- Appear in person at the fund or through a representative. In this case, an application for refund of the overpayment is submitted to the territorial department of the Pension Fund or Social Insurance Fund. If a representative approaches the fund, then a notarized power of attorney must be filled out for him.

- By mail. This method involves sending a registered letter with a list of attachments and acknowledgment of delivery. In this case, you will not need to contact the fund in person, but the waiting time will increase due to postal delivery time.

- Submitting an application for a refund of amounts paid before the 17th year to the Federal Tax Service. The latter began to be responsible for contributions only from January 1, 2017. Extra-budgetary funds are responsible for payments made before the 17th year. Therefore, the application must be sent specifically to these funds.

- Submitting an application for a refund without specifying the amounts. All amounts are specified through reconciliation of calculations. In particular, the application must indicate the exact amount of the overpayment and the amount of the arrears, if any. If the reconciliation is carried out incorrectly, then a difference is formed between the amount in the application and the amount in the personal account/registration.

- The wrong application form is being used. To draw up an application to the Federal Tax Service and extra-budgetary funds, different forms are used. When choosing a form, you must also take into account what kind of contribution is planned to be returned: for temporary disability or for injury.

We recommend reading: How to find out approval for purchasing a home using Matcap