Fixed Asset Accounting

Fixed asset (FPE) that came into the hands of an organization of any form of ownership, including real estate, is accepted:

- for accounting - on the date when the initial cost of the object was formed (clauses 4, 7 of PBU 6/01);

- for tax accounting - on the date of commissioning (clause 4 of article 259 of the Tax Code of the Russian Federation).

To complete these procedures, you need to create:

- act of acceptance and transfer of property (OS-1);

- inventory card (OS-6).

After this, accounting and tax accounting begin, when the accountant regularly makes entries for depreciation of fixed assets. Although in essence they are the same thing, in practice they are different. Let's consider what is the reflection of depreciation of fixed assets in accounting.

ConsultantPlus experts discussed how to calculate depreciation on fixed assets. Use these instructions for free.

Accrual of AOC for leased facilities

Usually, when an object is transferred for a long-term lease, it remains the property of the lessor and therefore he continues to charge depreciation. However, leasing agreements may provide for other features:

- At the end of the leasing agreement, the object can be finally transferred (sold) to the lessee

- It is provided that depreciation of the object during the period of use is carried out by the lessee

In these cases, the AOS is accrued and reflected in the accounting records by the receiving party, and at the end of the contract it is written off.

Example 8. Lessee of an excavator worth 1,500,000 rubles. For 4 years of leasing, a total depreciation amount of 750,000 rubles was accrued. After this, the property was purchased from the lessor.

The leased object was accepted for accounting Dt 01 subaccount “Property under lease” Kt 08 “Investments in VNA”.

Accrued AOS Dt 25 Kt 02 - 750,000.

On the date of purchase of the excavator, depreciation DT 02 Kt 01 -750,000 is written off.

The correct calculation of depreciation and the preparation of entries according to established rules are aimed at providing truthful and objective information about the real value of fixed assets as of a calendar date, the degree of their wear, and the gradual transfer of AOC according to cost items. Errors made when carrying out these operations distort the values of cost indicators in the balance sheet and reporting of business entities.

Top

Write your question in the form below

Chart of accounts

To summarize information about depreciation accumulated during the operation of fixed assets, account 02 is used. Posting is carried out on it; if depreciation of fixed assets is accrued, accrued depreciation is reflected on the credit of this account, and the debit reflects the disposal of fixed assets (sale, write-off, transfer, etc.). This means that account 02 is passive, although it is not directly involved in the formation of the balance sheet liability. It only reduces the residual value of fixed assets that are reflected in it, and all postings for depreciation of fixed assets are carried out with its help. This is due to the fact that the balance sheet uses the so-called net valuation of fixed assets, and to correctly display their actual value, depreciation shown in account 02 is subtracted from the original amount. It corresponds with most accounts used to record expenses.

The property subject to depreciation is the company's expensive intangible assets. To account for their depreciation, a separate account 05 is used. The principle of its application does not differ from account 02; it is also passive and corresponds with the accounts on which expenses are recorded.

Analytics should be carried out in the context of all fixed assets that are on the organization’s balance sheet. This is defined in the order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n, which approved the current chart of accounts. Accounting entries for accounting for the costs of restoring depreciation of fixed assets, using a standard chart of accounts, are carried out by the accountant, based on this order, other legal regulations, PBUs and the accounting policies of the organization.

Offers

Some professors see in depreciation, like their great predecessors, a source of investment in fleet renewal: 1) removing depreciation from the cost price and including it in the sales price and 2) rejecting the linear method of its calculation as the only correct one. According to the authors, the first approach will ensure the availability of funds for depreciation, and the second will increase the renovation fund itself. Let's consider these statements.

Now depreciation is part of the cost. It is accrued on the credit of a special account in correspondence with the accounts: Main production (the part of depreciation attributable to work in progress), Finished goods (goods produced but not sold) and Sales. The data in this account reflects both shipped (sold) and paid products. Only in the last part is depreciation filled with money (and even this is not obvious).

Let's assume that depreciation has been accrued in the amount of 1000 thousand rubles. By the time the balance is drawn up, there will be 350 thousand rubles in the balance of work in progress, 400 thousand rubles in finished goods inventories, 150 thousand rubles in shipped but unpaid finished products, 100 thousand rubles in shipped and paid goods. rub. Consequently, in the liability side the entire volume of the supposed depreciation fund is 1,000 thousand rubles, but in the asset it is opposed by only 100 thousand rubles. They lie on the current account and are used in the current turnover of the company, so some German accountants treat them as a loan and propose to accrue interest on them.

But the most important thing is that in a market economy, the selling price may give a very small profit, or may not have any at all. Consequently, even in the case of the sale of finished products, not in all cases depreciation is even partially covered by cash, especially in cases where valuables are sold by barter and not for money. Moreover, the share of accrued but not realized depreciation in work in progress, unsold finished products and shipped but not paid for products may be different, and the speed of liquidity, i.e. conversion into money is not the same for them.

It is now clear that the amount of accrued depreciation is always significantly greater than the share of cash related to it in the company’s revenue.

Sometimes supporters of the renovation fund understand this circumstance and therefore propose to abandon the capitalization of part of the depreciation charges (work in progress and finished goods) and write off all depreciation as a debit to the Sales account. But, firstly, this is a return to the 19th century, when they did exactly this, and secondly, this will no longer result in real money in the current account; thirdly, this will reduce the financial result of the current reporting period.

All this makes the first proposal hardly acceptable.

As for the second proposal, it must be said that the biggest misconception of many economists is that they believe that the methods of calculating depreciation may result in more or less money at the disposal of the owners of business entities. In fact, of course, the same depreciation can be calculated in different ways, but this will not make any more or less money.

In fact, even if there is some money in the revenue related to depreciation, then anyway this part is actually mixed with the entire money supply entering the current account, and it is natural that these amounts, again, if they really exist , and this, as we have seen, is very problematic, the owner disposes of it as cash, at their expense he pays wages and taxes, pays for goods, etc. etc., i.e. the real owner does not single out renovation and does not connect it with depreciation, because he buys new equipment not at the expense of depreciation, but at the expense of either his own cash or a loan received.

Accounting entries

Accountants usually record transactions related to depreciation of fixed assets using the following entries:

| Debit | Credit |

| 08 “Investments in non-current assets” | 02 “Depreciation of fixed assets” 05 “Depreciation of intangible assets” |

| 20 "Main production" | |

| 23 “Auxiliary production” | |

| 25 “General production expenses” | |

| 26 “General business expenses” | |

| 29 “Service industries and farms” | |

| 44 “Sales expenses” | |

| 91 “Other income and expenses”, etc. |

Depreciable and non-depreciable property

Not all operating systems are subject to wear and tear and write-off. PBU 6/01 states that the following property does not wear out:

- values that are not used and conserved for mobilization purposes;

- OS whose consumer properties do not change over time are land plots, museum values and natural objects (reservoirs, forests, etc.).

In addition, non-profit organizations do not calculate the depreciation of their fixed assets, because they do not have entrepreneurial activities, and therefore do not need to attribute the cost of fixed assets to expenses. Depreciation of a land plot also does not appear in accounting, as well as other similar natural objects. No postings or accruals are needed in this case.

Accounting policies and depreciation methods

According to PBU 6/01, depreciation is calculated in one of four ways:

- in a linear way;

- reducing balance method;

- write-off of the cost of fixed assets based on the sum of the numbers of years of useful use;

- write-off of the cost of fixed assets in proportion to the volume of products (works).

The Federal Law on Accounting states that the organization must reflect the chosen accrual method in its accounting policies. There, the description indicates not only how depreciation is calculated, the method of displaying it and the subaccounts used, but also how the useful life of the fixed assets and the annual amount of depreciation are determined, as well as the write-off of depreciation of fixed assets upon disposal. Other articles on this can help you on:

- Depreciation in tax accounting;

- Accounting policy for tax accounting purposes. We compose it correctly.

Depreciation and amortization: fixed or variable costs, profit, asset and liability

Contents:

The foundation of a company, on which its stability completely depends, is fixed capital. It includes buildings and structures, equipment, transport and other expensive assets. Closely related to fixed capital are concepts such as depreciation and amortization. They are often confused, so we will look at their main differences, as well as the roles they play in the activities of the enterprise.

General information

All property purchased by the company is subject to wear and tear. It means the gradual loss of fixed assets (OS) of their original properties and functions.

There are two types of wear:

- physical , implying the physical destruction of objects under the influence of their active exploitation or the forces of nature;

- moral , associated with the development of new technologies in the production of equipment and other types of operating systems.

Their main difference is that, due to complete physical wear and tear, objects can no longer function properly, and with obsolescence, the OS could still be used in activities, but this no longer becomes relevant and threatens to lag behind in the competition.

It is the susceptibility of property to various types of wear and tear that makes it necessary to apply the depreciation process to fixed assets.

With its help, an enterprise can gradually return the funds spent on the acquisition or construction of objects by including them in small amounts in the cost of manufactured products or services, or in costs in the case of trading companies.

Note!

This need arose due to the fact that the cost of the operating system is quite high, and its one-time inclusion in the cost or expenses is not possible.

The concepts of depreciation and amortization are closely related to each other also because without assessing the rate of wear and tear it is impossible to calculate monthly depreciation charges. The calculation of depreciation is based on the useful life of the property, which refers to the period of operation of the objects until they are completely worn out.

Differences between them

The difference between wear and depreciation is the following:

- Their functions are completely opposite. Under the influence of wear and tear, fixed assets lose value, but depreciation, on the contrary, allows their value to be restored.

- Depreciation does not allow the redistribution of lost value, and in the process of depreciation, the value written off in parts is included in the cost of products or services.

- These concepts are applied in different fields. Depreciation is an integral part of accounting and tax accounting, and depreciation is calculated in order to analyze the company’s activities, as well as to assess the cost of assets being sold.

Thus, despite the close connection of these concepts, they are not interchangeable. Next, we will consider other important nuances regarding accounting for depreciation in an enterprise.

Nature of depreciation costs

As has been mentioned more than once, monthly depreciation payments must be included in the cost of production. In this regard, they can be classified in the same way as other production costs.

According to the first classification, reflecting the dependence of costs on production volumes, there are:

- variables , the size of which increases in proportion to the volume of output;

- constants , which are not affected by output volume in any way.

The nature of depreciation costs will depend on the method of their calculation.

When using the method of writing off costs in proportion to production volumes, these will be variable costs, since the amount of depreciation charges is recalculated monthly based on the number of units produced by the enterprise.

When using all other accrual methods, payments for depreciation are the same size from month to month, and therefore are classified as fixed costs.

Another classification allows you to divide costs based on whether they relate to the production of a specific type of product or relate to the activities of the company as a whole. These are the following types of costs:

- direct , related to the cost of a particular type of product;

- indirect , which cannot be directly included in the cost.

Here, the type of depreciation costs depends on the role that the depreciated equipment plays in production.

If the cost of a machine used for only one specific type of product is recovered, this will be a direct cost.

If general workshop equipment is being depreciated, then these costs will have to be distributed in proportion to some other expenses, for example, the earnings of workshop workers. Such costs will already be indirect in nature.

Reflection Rules

Depreciation is reflected in accounting on the credit of accounts “02” and “05”, according to which the gradually written-off cost of fixed assets and intangible assets accumulates. These accounts are passive, but this does not mean that depreciation must be shown in the liability side of the balance sheet.

The rules for reflecting depreciation costs in the balance sheet are specified in PBU4/99.

Paragraph 35 of the regulation establishes that all indicators must be included in the balance sheet only in a net assessment, that is, it is necessary to subtract regulatory values from them.

Thus, the amount of accumulated depreciation is not reflected separately in the balance sheet. It is used only to reduce the cost of fixed assets and intangible assets included in the asset (accounts 01 and 04).

See also: File a Complaint Against a Collection Agency

Including depreciation in the income statement

Depreciation, like other types of expenses, must be reflected in the income statement. The report form involves dividing expenses into several categories. Depreciation charges can fall into any of them, depending on the nature of the use of the property for which they are charged:

- If depreciable objects serve directly for production purposes, depreciation must be reflected in the line “Cost of sales” (clause 5 of PBU 10/99).

- When calculating depreciation on fixed assets and intangible assets used in trading activities, these amounts are reflected in the line “Business expenses”.

- Depreciation on property used for general business purposes is entered in the line “Administrative expenses” (clause 7 of PBU1/2008).

- For facilities involved in non-core activities, depreciation is reflected in the line “Other expenses” (clause 11 of PBU 10/99).

The presence of depreciation amounts in the financial statements, even if not directly, as is the case in the balance sheet, is another distinctive feature that allows us to distinguish between the concepts of depreciation and depreciation. This once again proves the differences in the scope of their application and the inadmissibility of mixing these terms.

Earnings before interest, taxes, depreciation and amortization are described in this video:

Source: https://uriston.com/kommercheskoe-pravo/buhgalteriya/vneooborotnye-aktivy/amortizatsiya/i-iznos.html

Posting example

Vesna LLC owns a machine used for the production of materials. Its initial price is 550,000 rubles. The useful life is determined to be 20 years. The organization uses a linear method. Before posting, you need to determine the amount.

The depreciation rate per year is:

Or it is calculated for a year like this:

100% / 20 = 5%.

In total this is:

550,000 × 5 / 100 = 27,500 rubles.

This means that every month you need to write off 2291.67 rubles. This is the amount of accrued depreciation. As a result, the depreciation of the machine is recorded in accounting by posting:

Dt sch. 20 “Main production” Ct. 02 “Depreciation of fixed assets” - 2291.67.

When using other methods, the amount of wear will change, but the postings will remain the same.

Depreciation charges are a constant part of accounting costs

A specific rate of distribution of funds – depreciation costs – has a significant impact on the final result of the financial activity of an enterprise. These deductions, along with the share of profit that remains within the organization, relate to its own internal sources of financial resources (investments).

See also: Law Against Collectors and Banks

Basic definitions

The gradual transfer of the value of tangible assets to the final cost of goods produced by an organization is called depreciation. This accounting scheme ensures, regardless of moral and material wear and tear, the preservation of:

- Integrity of fixed capital;

- The total value of tangible assets.

The use of funds from the depreciation fund (FA) must be targeted and directed to:

- For capital construction;

- For the repair of fixed assets (real estate, structures, vehicles, equipment, production facilities and office equipment);

- To modernize production.

The use of the depreciation method (JSC) by enterprises makes it possible to:

- Preserve financial resources within the enterprise;

- Reduce the amount of taxation.

An enterprise can gradually accumulate financial resources for the modernization and repair of production or office fixed assets and equipment. An organization has the right to choose the following accounting methods independently, based on the principles of optimal use of fixed assets and compliance with state regulations:

- Straight write-off;

- Reducing balance method;

- Annuity method;

- The method of transferring funds is proportional to the degree of loading of funds;

- Accelerated depreciation.

If a market situation arises (competition, changes in legal and trade regulations) leading to a decrease in the price of a product and an increase in the period for writing off fixed assets to depreciation, it is more appropriate for an enterprise to pursue a policy of rational use of assets, thereby extending their service life.

Annuity method

With this method of accounting for depreciation of fixed assets, the percentage of monthly transfer is determined depending on the object. The accrual is made every year on the initial cost of the structure, equipment, and office equipment. The calculation may be adjusted over time.

Proportion method

The transfer of funds to the cost account occurs during the period when equipment, machinery or production capacity is loaded.

Straight write-off

The straight-line method of accounting for depreciation of fixed capital implies uniform (equal shares, monthly) write-off of the designated depreciation percentage (%A) throughout the entire period of operation.

The advantage of this method is the simplicity of calculations, and the disadvantage is “neutrality” in relation to scientific and technological progress.

With uniform write-off, depreciation rates are built without taking into account the age of the equipment (new or old) that is used. In this case %A is the same.

In modern conditions, fixed capital quickly ages (for example, computer equipment), both morally and technologically (physically). To correctly and optimally account for the fact of depreciation, the “accelerated depreciation” (AC) method is used.

Accelerated depreciation

The idea of this method is that in the first years of operation of new means of labor, a part of their cost is written off as costs, significantly exceeding what could be in the case of proportional write-off throughout the entire service life.

An example of calculating the operating balance using the reducing balance method:

Conclusion: with a depreciation rate of 25% per year, in the first two years the enterprise will receive significant additional internal resources to invest in capital repairs, construction or the purchase of new equipment.

The main benefits of using the accelerated method of calculating depreciation costs include the following facts:

- Insurance against losses – depreciation of fixed capital under the influence of scientific and technological progress;

- Increased competitiveness - the accelerated accumulation of most of the FA in the first two years allows you to purchase higher quality, high-tech equipment with increased productivity;

- The released monetary resources can be used in any area of business as entrepreneurial income;

- The rapid transition of fixed capital into cash equivalent attracts entrepreneurs to investments as a source of accumulation.

An accelerated method for creating FA will allow you to reduce the costs of the technological process and improve the quality of the final product.

The relationship between the selling price of a product and depreciation

Let's look at how FA is related to the price of the final product using an example:

The company purchased a grinding machine at a price of 100 thousand rubles. The service life of such equipment is 10 years. According to the accounting policy of the enterprise, a certain percentage is written off monthly to FA.

After 10 years, the organization can sell the machine at a residual value of, for example, 30 thousand rubles.

The company has the opportunity to purchase new equipment using funds from the FA (which includes a percentage of the cost of the machine), which is repaid through the pricing of the final product.

How is the depreciation percentage calculated?

%A is influenced by two factors:

- Market (competition, changes in market situation, force majeure);

- Wear and tear (moral and physical).

The percentage that determines the monthly amount of transfer of fixed assets to account for costs is otherwise called the depreciation rate.

Let's look at an example of how to calculate %A:

The company purchased a car for 500,000 rubles, with a warranty period of 5 years. First, we find the total amount of depreciation charges per year:

JSC (year) = 500,000 / 5 years = 100,000 rubles.

The following is the depreciation rate:

NA = 100,000 / 500,000 * 100 = 20%.

The role of the state in the process of establishing depreciation rates is twofold. On the one hand, depreciation deductions are not taxed. On the other hand, it indirectly controls the process of updating materially or physically obsolete fixed assets at the enterprise (for example, it sets the depreciation percentage not 5%, but 25%).

Source: https://buh-spravka.ru/buhgalterskij-uchet/amortizaciya-iznos-os/amortizacionnye-izderzhki.html

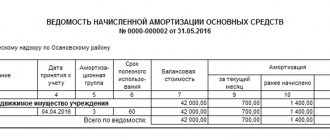

Postings for the first year of OS operation

Clause 21 of PBU 6/01 states that the accrual of depreciation charges for fixed assets begins on the first day of the month following the month of acceptance of such fixed assets for accounting. Standard accounting entries for the acquisition of an object and the calculation of depreciation for the first year of operation using the example of real estate look like this:

- The building was accepted for registration in February 2021 - Dt 01 Kt 08 - RUB 10,000,000. (02.02.2021).

- Depreciation accrued for the first month - Dt 20 Kt 02 - RUB 54,3245. (03/01/2021).

Depreciation entries are made until the cost of the property is fully repaid or the property is written off from accounting.

Legal documents

- PBU 6/01

- Art. 259 Tax Code of the Russian Federation

- Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n

Depreciation: Definition

The production process is impossible without an appropriate base, which includes fixed assets and intangible assets (buildings, workshops, machines, equipment, PCs, computer programs, brands, etc.).

They not only provide the process of creating a product, but, when worn out, transfer part of their own value to its price. It is through gradually accruing depreciation that the cost of the fixed asset passes into the cost of the manufactured product.

The process of monthly accrual and write-off of depreciation amounts to expenses defines the concept of depreciation in economics.

Depreciation: concept

So, as the property classified as fixed assets and involved in production ages, its value gradually decreases through the monthly write-off of part of the cost.

These amounts form depreciation and are included in the cost of the final product.

Subsequently, in order to develop production, a depreciation fund is created from part of the profit received from the sale of products, by decision of the company management, which is used to update the OS.

Helpful advice!

Depreciation is equal to the cost of the object when the cost of the object has completely become an expense. In this case, the fixed asset is considered fully depreciated, and its cost becomes zero.

Often, fixed assets with zero value are used in production for a very long time (if they retain normal production potential), can be reconstructed, revalued and acquire a new useful life.

Thus, depreciation is not only an indicator of the value expression of the price of an asset, but also has the function of monitoring the process of updating the company’s existing facilities.

Depreciation expenses and depreciation rate

Expenses related to depreciation are considered to be the same amounts that make up part of the cost of the object, which are gradually transferred to the price of the product, forming a cost item in the cost called “depreciation.”

Their size is determined by standards established as percentages and calculated in accordance with current legislative acts. The main criterion for this division is the useful life (SPI) of the object, i.e.

the period during which the operating system generates income for the company. In accounting, SPI is determined on the basis of the expected periods of effective operation, expected physical wear and tear, and legal regulations.

The useful life in tax accounting is established in accordance with the depreciation group of the approved Classification of fixed assets to which the object belongs. Often the SPI for accounting coincides with the tax one.

All fixed assets are divided into 10 depreciation groups. Thus, the 1st group includes OSes with a service life of no more than 2 years, and the 10th group includes objects whose use is planned for more than 30 years.

The percentage of deductions is called the depreciation rate and is calculated as the ratio of one to the number of months of effective use of the object (SUI). So, depreciation is costs calculated as a percentage of the cost of an asset, allocated to production costs and included in the cost of the manufactured product.

Depreciation: calculation example

A metalworking company has a milling machine worth 300,000 rubles on its balance sheet. and a service life of 20 years. Let's calculate the amount of monthly depreciation:

- 20 years x 12 months. = 240 months

- 300,000 / 240 = 1,250 rubles.

Using the depreciation rate, it is calculated as follows:

- HA = 1/240 = 0.004167

- 300,000 x 0.004167 = 1,250 rubles, i.e., over 20 years, the wear and tear of the machine in the amount of 1,250 rubles is invested monthly in production costs, and, consequently, in the formation of the cost of the manufactured product.

In economic analysis, depreciation is classified as a fixed or semi-fixed expense, since its size is predictable.

Where is depreciation shown?

Accounting for depreciation is carried out on account 02 “Depreciation of fixed assets”. This account is accompanying the main balance sheet account 01 “OS”, the debit balance of which records the initial cost of the OS.

Depreciation of fixed assets is accumulated on the loan account. 02, and the difference between the debit of the account. 01 and credit account. 02 is the residual value of the company's fixed assets as of the reporting date.

Depreciation begins to be calculated from the beginning of the month following the month the facility was put into operation.