The Federal Tax Service (FTS) reminds you of the deadlines for filing an income tax return in Form 3-NDFL. In 2021, you must file a tax return on income received in 2021 by May 3, 2018.

A declaration of income received in 2021 must be submitted by May 3 (Thursday) inclusive. The Federal Tax Service of Russia reminds us of this on its official website. We are all accustomed to the fact that the declaration campaign ends no later than April 30. A special feature of this year is that the weekends from April 28 and January 7 have been moved to April 30 and May 2, respectively, so the deadline for filing declarations ends on May 3.

As a general rule, a tax return is submitted by taxpayers specified in Art. 227-228 of the Tax Code, no later than April 30 of the year following the expired tax period (clause 1 of Article 229 of the Tax Code of the Russian Federation). But since in 2021 the weekends from April 28 and January 7 have been moved to April 30 and May 2, respectively (Resolution of the Government of the Russian Federation of October 14, 2017 No. 1250), then taking into account clause 7 of Art. 6.1 of the Tax Code of the Russian Federation, the deadline for filing a declaration has been postponed to the next working day - May 3, 2021.

It is important to remember that the deadline for filing a return of May 3, 2018 does not apply to receiving tax deductions - in this case, you can send a return at any time during the year

.

Who must submit an income tax return this year?

READ ON THE TOPIC:

In 2021, the 3-NDFL declaration will be submitted using a new form.

Reporting for 2021 According to the regulations of the tax service, individual entrepreneurs, notaries, lawyers who have established law offices or notary offices, tutors and other persons engaged in private practice, foreign citizens working under a patent must submit a declaration in form 3-NDFL.

It is necessary to report income if a person sold an apartment in 2021 that was owned for less than three years, or a car. Citizens who rented out an apartment or received other income from which tax was not withheld must also report.

Such income includes, for example, winning the lottery or receiving a gift of real estate not from close relatives, the message explains. It is also necessary to declare income received by an individual from foreign sources, as well as other income on which tax is not withheld.

Thus, according to current standards, if a citizen is given an apartment by close relatives, this is not considered income and there is no need to pay anything to the state. By close relatives we mean mother, father, spouse, brother, sister, daughter, son.

If real estate is inherited from first and second cousins, nephews or great-nephews, father-in-law or mother-in-law, great-aunts and uncles, then the real estate gift tax will be 13 percent of the total cost of the apartment.

Tax officials remind you that when filling out a declaration in Form 3-NDFL, you should take into account the changes that were made to it this year. The declaration form can be downloaded from the department’s website or taken from the tax office. You can submit a declaration through the “Taxpayer Personal Account for Individuals” on the Federal Tax Service website, bring it to the inspectorate in person, or send it by mail.

It is important to take into account that the mere sending of a declaration to the tax authority does not mean that a person must immediately pay tax. There is a deadline for paying the calculated personal income tax - no later than July 15 of the year following the reporting year. But since this year July 15 falls on a Sunday, taxes can be paid until July 16 inclusive.

Documents for a tax refund for a particular year can only be submitted next year.

Tax authorities must have an understanding of how much you paid in taxes on income to the treasury during the calendar year in order to return this amount to you. You cannot submit a declaration in advance in form 3-NDFL, even if you, for example, understand that by the end of the year you will not receive any income on which income tax is paid.

The only exception is if you do not collect the deduction yourself, but entrust it to your employer. You can write a deduction application to your accounting department or management in advance; they will take the necessary actions when it is possible.

Deadline for payment of 3 personal income taxes in 2021 for individuals

KNOW that you have the right to personally fill out and submit the 3-NDFL declaration without resorting to paid services. Both methods have their pros and cons: you can save some money (for example, services for preparing a declaration to obtain a property deduction cost an average of about 3 thousand rubles) passport data; TIN number (if available); certificate in form 2-NDFL from the place of work (from all places of work for the reporting period - 2021); agreements related to the receipt of income, documents confirming the receipt of funds under agreements, acts to agreements; other documents confirming receipt of income; documents confirming the right to receive standard, social and property deductions.

We recommend reading: Is it worth refinancing a mortgage with VTB 24

Date of submission of the 3-NDFL report by individuals

The report on additional profit is filled out using form KND 1151020, regulated by Order of the Federal Tax Service of Russia No. ММВ-7-11/569 dated 10/03/2018. The declaration is filled out by hand, on a PC or in a special program.

When individuals file a tax return, it is stated in paragraph. 2 p. 1 art. 229 ch. 23 Tax Code of the Russian Federation Federal Law No. 117 dated 08/05/2000 (as amended on 12/25/2018). The deadline for submitting personal income tax 3 is the year following the reporting year. Thus, the annually completed form for reporting additional profits must be submitted by April 30. But tax authorities have the right to change the deadline for filing the 3rd personal income tax declaration depending on the length of the year, as well as public holidays. The difference does not exceed 2-3 days. The legislation regulates two situations in which the terms are reduced:

- If a foreign payer stops working in Russia and plans to leave the country, then 3-NDFL is provided no less than 1 month before departure.

- If the individual entrepreneur has closed the business, then the entrepreneur is given 5 working days to submit the report.

The fee itself in these cases is paid a maximum of 15 days after submitting the form. Also, on January 1, 2021, the Declaration Campaign 2019 program began, which obliges the submission of KND 1151020 for 2021 to report on funds received from financial transactions before the specified date - April 30, 2021. To facilitate the preparation of the form, tax authorities provide individuals with two software types, which is available on the official portal of the Federal Tax Service. The package includes installation instructions, annotation and installation file. Deadlines for filing 3-NDFL to receive a tax deduction>

The legislation of the Russian Federation applies not only to the deadline for filing an income tax return - using the KND 1151020 form, a citizen has the right to return part of the tax paid. This procedure is called tax deduction. The form contains the relevant sections where the types of deductions are indicated:

- Standard (Article 218 of the Tax Code of the Russian Federation): for the payer of fees or his children.

- Social (Article 219 of the Tax Code of the Russian Federation): expenses for charity, training, treatment, purchase of medicines, for the funded part of old-age benefits, voluntary insurance and social contributions.

- Investment (Article 219.1 of the Tax Code of the Russian Federation): funds spent on working with securities, if the citizen made a profit on an investment account and also deposited money into the investment account.

- Property (Article 220 of the Tax Code of the Russian Federation): from trade, purchase, construction of movable and immovable property, purchase of property for municipal needs.

- Professional (Article 221 of the Tax Code of the Russian Federation): profit received by a businessman, under a GPC contract, by persons engaged in private practice, bonuses, fees.

The deadlines for submitting KND 1151020 for refund are not regulated by law. The Federal Tax Service allows you to submit a return declaration throughout the year. But a citizen has the right to request and receive funds next year, counting from the date of expenses. For example, money for building a house was spent in 2021, which means it is possible to request and receive funds only in 2021.

srok_sdachi_ndfl.jpg

Related publications

Declaration 3-NDFL is a reporting document confirming that an individual has received income for a certain year. Information from this document is used by tax inspectors to verify the completeness of an individual’s payment of personal income tax to the budget. Submission of 3-NDFL to the Federal Tax Service is an obligation assigned to various categories of the population and entrepreneurs. Let's look at the features of this form and the deadlines for submitting it to the Federal Tax Service.

Deadline for submitting 3 personal income tax for 2021

Tax return 3 personal income tax for 2021 is submitted within the usual deadlines. In this sense, the new order of the Federal Tax Service did not change anything:

- For those who are required to report on income received in 2021 for the sale of real estate and transport, the deadline for submitting 3 personal income tax is April 30, 2021. This is a working day, it is not transferred anywhere, so there will be no delay next year.

- All other taxpayers entitled to receive tax deductions and personal income tax refunds can submit a declaration at any time. Moreover, next year you can submit not only 3 personal income taxes for 2021, but also for the two previous years - 2021 and 2021.

That is, the deadline for submitting 3 personal income taxes for 2021 is set only for sellers of real estate and transport. The rest choose the time of their visit to the Federal Tax Service at their own discretion. But, of course, it’s worth getting your money back the sooner the better.

Tax payment deadline for individual entrepreneurs

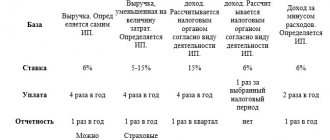

Individual entrepreneurship involves paying fees not only once during the reporting period, but also in advances (like a legal entity). Depending on the situation, the deadline for paying tax on the 3-NDFL declaration and the obligation to deposit funds change. There are three main situations in which an entrepreneur needs to pay a profit tax:

- A businessman has the right not to pay a tax contribution if he has declared the transition to UTII, NPD, PSN or simplified tax system. But three types of profits are subject to levy:

- a loan without interest from another organization: money saved on interest is subject to a fee;

- dividends from participation in organizations: here the individual entrepreneur does not pay the fee on his own - the tax agent pays for it. The tariff depends on the status of the businessman: resident - 13%, non-resident - 15%;

- after the sale of movable and immovable property.

- The individual entrepreneur did not declare a transition to another aid to navigation. In this situation, the work of a businessman is defined as activity on OSNO, payment of 3-NDFL is the direct responsibility of the individual entrepreneur. Dates for depositing tax funds for a businessman on OSNO:

- July 15—advance payment;

- October 15—advance payment;

- January 15—advance payment;

- July 15 of the next year - the calculated amount of the fee minus advances.

- The entrepreneur worked in a special regime, but lost the right to use it and did not notify the Federal Tax Service about this. Then tax funds are deposited as for individual entrepreneurs on OSNO.

If the work of an individual entrepreneur has ceased, then you need to pay tax within 15 days after submitting 3-NDFL reports, which are submitted within 5 days after the registration in the Unified State Register of Entrepreneurs about the closure of the company.

Responsibility for non-payment of tax and late payment

Payment of taxes by individuals late will result in the accrual of penalties. Citizens pay penalties in the amount of 1/300 of the refinancing rate for each day of delay. The maximum amount of penalties cannot be greater than the amount of overdue tax debt (clause 3 of Article 75 of the Tax Code of the Russian Federation).

If a citizen understates the declared taxable income or the amount of personal income tax, he will have to pay a fine in the amount of 20% of the underpaid tax amount. This situation may arise, for example, when deductions are used improperly, income is understated, or tax is calculated at a lower rate.

If it turns out that the taxpayer deliberately distorted the amount of tax payable, the fine will be 40% of the amount of the arrears.

Sanctions for late payment for tax agents are stricter: untimely transfer of withheld personal income tax threatens not only the accrual of penalties, but also the payment of a fine in the amount of 20% of the amount of calculated tax (Article 123 of the Tax Code of the Russian Federation).

Penalties for the first 30 days of delay are calculated based on 1/300 of the refinancing rate for each day of arrears; from the 31st day the penalty rate doubles. The limitation on the maximum amount of fines established by clause 3 of Art. 75 Tax Code, also valid for legal entities.

At the same time, the tax agent may be exempt from the fine if he transfers the tax and penalties before the tax authorities declare a delay in payment (Clause 4 of Article 81 of the Tax Code of the Russian Federation, Resolution of the Constitutional Court of the Russian Federation dated 02/06/2018 No. 6-P).

Until April 30, 2019, submit a tax return 3-NDFL for individual entrepreneurs and private practices, as well as citizens who independently pay tax on their income.

- Individual entrepreneurs transfer tax surcharges to the budget, if any;

- independent citizens pay the entire tax;

- foreigners working on a patent will finally pay their taxes for 2021.

Citizens whose tax was not withheld by a tax agent due to the impossibility of doing so must pay personal income tax for 2018 by December 2, 2019 based on a notification from the Federal Tax Service.

Tax agents transfer personal income tax no later than the day following the day of payment of income, and for non-monetary income - within 24 hours after the cash payment closest to the date of receipt of income.

Order approving the new Form 3 of personal income tax for 2021

During the last reporting campaign, the tax service delayed for a very long time in approving the new Form 3 of personal income tax. As a result, it was adopted very late and came into force only on February 18, 2021, i.e. almost two months after the start of the campaign.

But this year, tax officials took into account their mistakes and approved Form 3 of personal income tax for 2021 even earlier than usual. Order of the Federal Tax Service dated October 3, 2018 N ММВ-7-11/ [email protected] was registered with the Ministry of Justice on October 16, 2018 under number 52438.

The order comes into force on January 1, 2021, and the income statement of individuals for 2021 is submitted using the form approved by this order.

When is a return required to be filed in 2021?

Reports are filled out and sent to the Federal Tax Service by individuals and individual entrepreneurs upon receipt of profit during the reporting period and to process a personal income tax refund.

If a person received taxable income during the year, he is required to fill out a declaration. Cases may be different:

- Renting out a residential property.

- Profit from investment activities, receipt of dividends

- Sale of movable and immovable property.

- Winning the lottery.

Persons carrying out entrepreneurial activities, lawyers and notaries report to the Tax Inspectorate according to the general taxation system.

If a person is going to apply for a tax deduction, he fills out a declaration. According to the law, a personal income tax refund is provided in the following cases:

- Opening an individual investment account.

- Buying a property.

- Mortgage.

- Education expenses.

- Receiving paid medical services.

- Contributions to a pension fund paid on a voluntary basis.

The main task of the 2021 declaration campaign comes down to managing and simplifying the submission of declarations for taxpayers of all categories.

Responsibility for failure to submit or violation of the deadline for filing 3-NDFL

Ignoring the deadline for filing a declaration or being late in submitting the form within the established time frame will result in a fine. Its amount is 5% of the amount of unpaid tax for each overdue month, regardless of whether it is full or not (Article 119 of the Tax Code of the Russian Federation). The amount of the fine is limited - it cannot be higher than 30% of the amount of unpaid tax. The minimum amount of the sanction has also been established at 1000 rubles. This is exactly the amount an individual entrepreneur can be fined for OSNO, who had no income in the reporting year and did not submit a zero 3-NDFL.