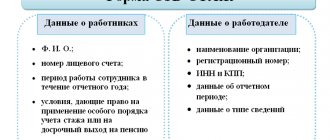

VAT 2018: new types of goods and services

The legislator introduced the following innovations:

18% is now levied on imports of electronic services and goods.

Previously, only Russian suppliers of similar services paid VAT. Foreigners sold their electronic goods and services on the territory of the Russian Federation without VAT. The Russian government is seeking to increase the competitiveness of its own Internet companies. That is why new rules appeared.

How did the market react to the initiative of the Russian authorities?

Google’s reaction to changes in the pricing of their services in Russia is now known. The company simply increased the tariff so as not to lose profits.

Any clarifications, additional/amendment documents and calculations must be submitted remotely via EDI.

Previously, even if the VAT return was sent remotely through communication channels, explanations during the “camera meeting” could be transmitted in any way convenient for the taxpayer, even brought in person on paper. Now the law has tightened the rules: all documents must be sent electronically.

Failure to submit a VAT return correctly is now punishable by a fine.

Previously, errors in declarations made involuntarily or with malicious intent were also punishable by fines. But now submitting a VAT return with such inaccuracies will lead to significant fines, since their amount has changed upward. The regulations for conducting desk audits have changed. The new system has become tougher in relation to the taxpayer.

PLEASE NOTE: submission of explanations on paper is now equivalent to the absence of explanations as such, the fine for such a violation is 5,000 rubles; a similar repeated violation will entail a penalty of 20,000 rubles.

The changes affect the report form itself and the KBK used to pay the tax.

In a new way, you need to report starting from January 2021. Those who submit reports monthly have already been affected by this rule. Other VAT payers will learn about it in March-April 2021, when they will need to report for the 1st reporting period of this year.

Deadlines for submitting the declaration in 2021: table

In 2021, the VAT return must be submitted no later than the 25th day of the month following the expired quarter (Articles 163, 174 of the Tax Code of the Russian Federation). The deadline is the same for submitting a declaration on paper and in electronic form. The reporting months in 2021 are January, April, July, October.

In 2021, VAT payers can submit a VAT report via the Internet. And only tax agents can submit a declaration “on paper”. The exception is an agent who does not pay VAT. That is, a person applies a special regime or is exempt from paying tax under Article 145 of the Tax Code of the Russian Federation. Then it is allowed to submit the declaration “on paper” or electronically.

If the deadline for submitting the declaration falls on a weekend or holiday, as a general rule, you can report on the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). Below we provide a table with the deadlines for submitting the VAT declaration in 2021.

| Reporting period | Deadline for submitting the VAT return |

| 4 sq. 2021 | January 25, 2021 |

| 1 sq. 2021 | April 25, 2021 |

| 2 sq. 2021 | July 25, 2021 |

| 3 sq. 2021 | October 25, 2021 |

| 4 sq. 2021 | January 25, 2021 |

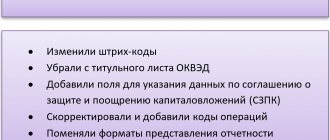

VAT return: new form in 2018

Tax agents, payers by force of law and intermediaries must still pay and submit VAT reports. The form should be filled out clearly on the basis of purchase and sales books, information from tax and accounting registers.

Now the document is marked with a 16-digit barcode. It has new sections. Now there will be no problems with filling out the gas customs declaration. There are now multiple lines for this value. For each declaration number there is its own line.

Deadline for submitting the VAT return

The form must be submitted strictly before the 25th day of the month following the report, inclusive. For example, if you report quarterly, be sure to submit the form by April 25 (25 is the last day you can still report without penalties).

IMPORTANT: the main way to submit the form is electronic; exceptions are reserved for companies in special regimes and companies with up to 100 employees; they can still choose the method of sending the report.

What sections need to be filled out?

If the deadline for filing a VAT return remains the same, then the sections to be filled out have changed. Each tax regime has its own nuances.

Sections to fill out on OSNO

Taxpayers as usual must fill out:

- Title page and sections 1, 3, 8-9;

- If you are an intermediary, be sure to complete sections 10 and 12;

- Section 12 Those who have transactions with a non-taxable base must also fill out;

- If you are a tax agent, section 2 of the form is provided for you;

- Exporters must provide information in sections 4-6 of the form;

- Section 7 – for those who sold goods not subject to VAT, performed work/services in a territory other than the Russian Federation, it is also filled out by those who actually received advances for the production of long-cycle products from a special list.

Filling out a VAT return

You can read more about how to fill out a VAT return in the article Filling out a VAT return.

Where and what to indicate to companies on UTII and simplified tax system

and companies in special regimes enter data on the title page, fill out sections 1, 9 (if they are also a tax agent), 12.

PLEASE NOTE: submission of VAT reports (declarations) in 2018 is provided only for those companies on UTII and the simplified tax system that actually issued sales invoices with VAT; all other taxpayers do not submit declarations under special regimes.

Features of tax payment in 2018

How to pay tax in 2021? As before, it is not necessary to pay the entire amount immediately if you report quarterly. It is enough to divide the amounts into 3 equal parts and pay monthly for 3 months after the date of the report.

Let's see how this works with an example:

Let’s assume LLC “Dandelion” based on the results of the 1st quarter. 2021 has an obligation to pay VAT of RUB 5,893,630. How can he deposit this amount? You can pay at a time, or you can pay 1/3 within the following terms: until January 25 - until February 26 - until March 26. Everyone chooses what is convenient for them, taking into account the situation in the company. The main thing is that the 2021 VAT tax return is submitted within the prescribed period.

VAT declaration: procedure for filling out, deadlines for submission, fines

As part of control activities, inspectors most often identify the following errors in VAT returns:

1. Incorrect transaction code for the sale of goods (work, services) to VAT payers

In section 9 “Information from the sales book” of the declaration, taxpayers-sellers reflect transactions of the sale of goods (work, services) to buyers - VAT payers, using transaction type code 26 (“Sales of goods (work, services) to persons who are not VAT payers”). Invoices with code 26 do not participate in the process of comparing invoices from section 8 “Information from the purchase book” of the buyer’s declaration and invoices from section 9 of the seller, as a result of which auto claims are generated to taxpayers for identified discrepancies.

2. Errors when deducting VAT in parts

The right to deduction can be used within 3 years from the date of its occurrence, and the amount of tax on the invoice can be declared in installments over several tax periods (letter of the Ministry of Finance of the Russian Federation dated May 18, 2015 No. 03-07-RZ/28263). At the same time, taxpayers, when deducting VAT in parts, incorrectly fill out column 15 of the purchase book (cost of purchases according to the invoice) (line 170 of section 8).

Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 established that when accepting invoices for deduction in parts, column 16 of the purchase book (VAT amount on the invoice) (line 180 of the section reflects the part of the total tax amount that is accepted for deduction in the current quarter. And in column 15 of the purchase book (line 170 of the section) the cost of goods (work, services) is always indicated, indicated in column 9 on the line “Total payable” of the invoice, without dividing into parts.

reflects the part of the total tax amount that is accepted for deduction in the current quarter. And in column 15 of the purchase book (line 170 of the section) the cost of goods (work, services) is always indicated, indicated in column 9 on the line “Total payable” of the invoice, without dividing into parts.

In addition, in column 13b of the sales book (invoice value of sales) (line 160 of section 9) and in column 14 of the invoice journal (cost of goods) (line 160 of section 10) it is also necessary to reflect the total cost of sales according to the invoice - invoice without division.

3. Incorrect recording of import transactions

Taxpayers in the purchase book and section 8 of the declaration incorrectly reflect import transactions from EAEU member countries (transaction type code 19) and from other countries (transaction type code 20).

Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 established that when reflecting in the purchase book a transaction for the import of goods from the EAEU, in column 3 “Number and date of the seller’s invoice” of the purchase book, the registration number of the application for the import of goods from the territories of the EAEU states, assigned tax authority, and the date of registration of the application for the import of goods and payment of indirect taxes.

When reflecting in the purchase book a transaction for the import of goods from other countries not included in the EAEU, in column 3 “Number and date of the seller’s invoice” of the purchase book the number and date of the customs declaration are indicated.

4. Incorrect completion of the title page of the declaration if it is submitted by the legal successor

When submitting a declaration for another organization as a legal successor, in the title page in the column “Code of the place of submission,” code 215 (“At the location of the legal successor who is not the largest taxpayer”) or 216 (“At the place of registration of the legal successor who is the largest taxpayer”) is indicated with indicating the code of the reorganization form, TIN and KPP of the reorganized company in the appropriate columns. If in this situation, on the title page in the column “Code of the place of submission” you indicate code 213 (“At the place of registration as the largest taxpayer”) or 214 (“At the location of the Russian organization that is not the largest taxpayer”), the declaration will be considered submitted for oneself . As a result, the previously submitted form receives the status “irrelevant”.

Thus, as a result of these errors, discrepancies arise, leading to increased paperwork and an undesirable burden on both the taxpayers themselves who committed violations and their counterparties.

LETTER from the Federal Tax Service of the Russian Federation for the Moscow Region dated December 9, 2016 No. 21-26/ [email protected] “About typical errors when filling out a VAT return”

The document is included in the ATP “ConsultantPlus”

Editor’s note:

Let us recall that as part of a desk audit, if contradictions are detected, tax authorities have the right to request clarification. If a company has an obligation to submit a VAT return in electronic form, then explanations to it are submitted in the same form.

Explanations on paper are not considered submitted.

How to submit explanations for a VAT return: see the algorithm of actions from the Federal Tax Service of the Russian Federation here.

A fine in the amount of 5 thousand rubles is collected in case of failure to submit (untimely submission) explanations to the tax authority when the updated tax return is not submitted on time (clause 1 of Article 129.1 of the Tax Code of the Russian Federation). In case of repeated violation - 20 thousand rubles.

How many VAT returns to file in 2018?

The reporting quarter has ended - there are 25 days to submit the declaration. This rule is prescribed by Article 174 of the Tax Code of the Russian Federation in paragraph 5. It turns out that the reporting form for the 4th quarter will be submitted first. 2021 by January 25, 2021. Further, for all those reporting quarterly, the reporting period will be the interval from January 1 to March 31, 2021. The form will need to be submitted strictly before April 25, 2021.

IMPORTANT: firms and entrepreneurs who import goods purchased in the EAEU countries report VAT every month, and are required to submit the form by the 20th of the next month, when the reporting month ends, which means that already in the 1st quarter of the current year they will have as many as 3 reports - for Dec. 17 (until 01/22/18), for Jan. 18 (until 02.20.18), for February. 18 (until March 20, 2018).

Features of the report of firms from EEC states can be found in the Treaty on the Eurasian Union No. 18 in paragraph 20.

VAT submission deadlines

Home → Accounting consultations → VAT

Current as of: January 19, 2021

The VAT return is submitted no later than the 25th day of the month following the reporting quarter (clause 5 of Article 174 of the Tax Code of the Russian Federation). Accordingly, the deadlines for submitting VAT reports in 2021 will be as follows:

Period for which the VAT return is submitted Deadline for filing the return

| For the fourth quarter of 2021 | 25.01.2018 |

| For the first quarter of 2021 | 25.04.2018 |

| For the second quarter of 2021 | 25.07.2018 |

| For the third quarter of 2021 | 25.10.2018 |

VAT submission deadline for the 4th quarter of 2021

The VAT return for this period must be submitted no later than 01/25/2019.

VAT on imports: deadlines for filing the declaration

Organizations and individual entrepreneurs importing goods from EAEU countries must report to the Federal Tax Service by submitting a VAT declaration on imports no later than the 20th day of the month following the month of registration of imported goods/payment deadline under the contract (clause 20 of Appendix No. 18 to the Agreement on Eurasian Economic Union).

In 2021, importers are required to submit the relevant VAT return within the following deadlines:

Period for which an import VAT return is submitted Deadline for filing the return

| For December 2021 | 22.01.2018 |

| For January 2021 | 20.02.2018 |

| For February 2021 | 20.03.2018 |

| For March 2021 | 20.04.2018 |

| For April 2021 | 21.05.2018 |

| For May 2021 | 20.06.2018 |

| For June 2021 | 20.07.2018 |

| For July 2021 | 20.08.2018 |

| For August 2021 | 20.09.2018 |

| For September 2021 | 22.10.2018 |

| For October 2021 | 20.11.2018 |

| For November 2021 | 20.12.2018 |

The VAT declaration for imports for December 2021 must be submitted already in 2021 - no later than 01/21/2019.

glavkniga.ru

Where to file a VAT return

The submission of a VAT return is regulated by the code. You must report to the tax office at your place of registration. Typically, the Federal Tax Service is assigned to the address of the taxpayer’s location. You can find out more about this at any inspection. They provide detailed advice to taxpayers. The website nalog.ru lists the telephone numbers of departments by region of Russia. The official website has a lot of useful information on filing reports and paying taxes.

Similar articles

- Zero VAT return

- Filling out the VAT return for the 3rd quarter

- VAT return for the 3rd quarter of 2017

- Filling out a VAT return

- Zero VAT return

Who submits VAT monthly in 2021

New in VAT from 2021

Particularly important processes are not taxed at all: the transport of oil and gas, the sale of goods in the space industry, and the export of precious metals have a zero rate. From 2021, other agents are also exempt from VAT. It is worth noting an important innovation: each enterprise can refuse the zero tax rate, the right to which must be proven.

If this fails, you will have to pay 18% for each counterparty.

VAT reporting for the tax period 2021

For the tax period 2021, the VAT report will increasingly include a rate of 10%. This is due both to the addition of new products to this category and to the increase in the number of companies that will be able to reduce this tax for themselves from 18 to 10%.

Main innovations for VAT 2021 Significant changes in the field of submitting VAT reports for the first half of 2021 and other reporting periods are as follows: In order to increase the competitiveness of Russian Internet enterprises, an 18% tax has been introduced on the services of foreign suppliers of electronic goods and services.

Procedure and deadlines for paying VAT in 2021

In certain situations, defaulters will also have to consider it. Information about input VAT should be recorded in the purchases ledger, and information about outgoing VAT in the sales ledger.

The difference is displayed in the declaration at the end of the quarter.

Purchase and sales ledger data is an integral part of this report.

The declaration must be submitted to the Federal Tax Service at the taxpayer’s place of registration no later than the 25th day of the month following the reporting quarter (clause

5 tbsp. 174 Tax Code of the Russian Federation)

Who must submit VAT returns monthly?

Payment is made in equal installments over 3 months following the reporting quarter.

Send payments by the 25th of each month following the reporting period. The declaration is submitted based on the results of each quarter.

The procedure and deadlines for submitting a declaration and paying advance payments and taxes are specified in Art.

287 and 289 of the Tax Code of the Russian Federation. Revenue and expenses in the income tax return are shown on an accrual basis from the beginning of the reporting year.

Payment is made in equal installments over 3 months following the reporting quarter.

Send payments by the 25th of each month following the reporting period. The declaration is submitted based on the results of each quarter. The procedure and deadlines for submitting a declaration and paying advance payments and taxes are specified in Art. 287 and 289 of the Tax Code of the Russian Federation. Revenue and expenses in the income tax return are shown on an accrual basis from the beginning of the reporting year.

In certain situations, defaulters will also have to consider it. Information about input VAT should be recorded in the purchases ledger, and information about outgoing VAT in the sales ledger. The difference is displayed in the declaration at the end of the quarter.

Purchase and sales ledger data is an integral part of this report.

The declaration must be submitted to the Federal Tax Service at the taxpayer’s place of registration no later than the 25th day of the month following the reporting quarter (clause 5 of Article 174 of the Tax Code of the Russian Federation)

For the tax period 2021, the VAT report will increasingly include a rate of 10%.

This is due both to the addition of new products to this category and to the increase in the number of companies that will be able to reduce this tax for themselves from 18 to 10%.

Main innovations for VAT 2021 Significant changes in the field of submitting VAT reports for the first half of 2021 and other reporting periods are as follows: In order to increase the competitiveness of Russian Internet enterprises, an 18% tax has been introduced on the services of foreign suppliers of electronic goods and services.

Who submits a VAT return in 2021

Organizations and entrepreneurs, including intermediaries, who are recognized as VAT taxpayers or act as tax agents for VAT, are required to prepare a VAT return.

Another VAT return in 2021 is submitted by VAT defaulters (for example, simplified companies) who have issued an invoice with the allocated VAT amount. Such companies reflect information from issued invoices in their VAT returns. Yes, in this case a zero VAT return is submitted.

If you miss the VAT reporting deadlines in 2021

The Federal Tax Service will be happy if in 2021 you submit your VAT return 5-10 days before the end of the deadline. However, if you submit your VAT return electronically, then there is nothing to fear. After all, the date for sending the declaration is fixed, and you will also have a corresponding protocol. If in 2021 you violate the deadlines for submitting a VAT return, then the liability in the form of a fine will be 5% of the unpaid amount of VAT payable on a late return for each full or partial month that has passed from the day set for submitting the return to day of delivery. However, the fine cannot be more than 30% of the amount of tax due and not paid on time and not less than 1000 rubles (clause 1 of Article 119 of the Tax Code of the Russian Federation).