Who should fill out KUDiR

There are several types of Books:

- For a simplified taxation system.

The book is filled out by individual entrepreneurs and LLCs using the simplified tax system. The form of the document is the same for all simplifiers, regardless of what object of taxation they apply. The only difference is that under the 6% simplified tax system, only income is entered into KUDiR, and under the 15% simplified tax system, both income and expenses are entered.

- For the patent tax system.

It is filled out by entrepreneurs using the PSN, and only income is entered there. In this taxation system, actual income does not affect the amount of tax, i.e. for the cost of the patent. But the Income Accounting Book is needed in order to track compliance with the income limit, because PSN can only be used for incomes up to 60 million rubles.

- For the general taxation system. It is filled out only by individual entrepreneurs on OSNO to calculate personal income tax.

- For individual entrepreneurs using the Unified Agricultural Tax.

How to conduct KUDiR

The general rules for maintaining KUDIR are as follows:

- The book is kept for one year.

- Records of business transactions are entered in chronological order.

- Each entry must be supported by a primary document.

- KUDiR can be maintained manually and electronically, but even in this case, at the end of the year it needs to be printed, stapled, numbered page by page, signed and stamped (if any).

- The absence of business transactions does not relieve the need to form a KUDiR. If no activity was carried out, you need to create a Book with zero indicators.

- There is no need to submit the KUDiR to the tax office, but you must be ready at any time to provide it for inspection at the request of tax officials. The tax inspectorate will fine you for the absence of KUDiR.

The rules for filling out the KUDiR for each taxation system are contained in the regulatory documents that approved the corresponding form:

- The book is kept for one year.

- Records of business transactions are entered in chronological order.

- Each entry must be supported by a primary document.

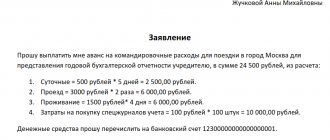

How to apply for KUDiR

In 2021, it is not enough to download and maintain KUDiR for free in electronic form: by the end of the tax period it must be printed and bound. Former supplicants may have questions about this: what are the requirements, how to certify and seal? First, about the firmware:

- We fold the sheets in the correct order and make holes where they are stitched. To do this, you can use a needle, or you can use a hole punch if the file is thick. There are no general regulated requirements for this.

- We thread the threads and make a knot on the back of the document. You can also use tape for this.

For KUDiR on a patent there are no special requirements for registration and storage. Now let's look at the sealing process. There are two ways. Here you can see what the KUDiR looks like, which should be stored at the enterprise.

- Take a sheet of paper and glue it: the narrow side should be on the back side of the document, and the wide side should be on the front. On the front side we write the following information: number of pages (in words and numbers), date, name of the certifier. You can also use a seal if available. Moreover, the signature and seal must extend beyond the sealing sheet.

- We make a hole through all the pages of the book of income and expenses. You can do it as in the example, through the upper right corner, or you can just do it from the side. We thread the thread or ribbon. We make a knot on the back side of the document, and fix the end on the front side with a piece of paper with the information already listed above. The signature and seal (if any), again, must go beyond the limits.

Other blog posts

Setting up OFD on Evotor 7.2

February 04, 2021 Read more

Evotor 7.2: working with receipts

February 04, 2021 Read more

Registration of Evotor 7.2 cash register

February 03, 2021 Read more

Features of filling out KUDiR on the simplified tax system

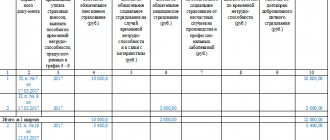

The form consists of 5 sections.

Section I “Income and Expenses”

All business transactions are entered into this part in chronological order, indicating:

- dates and numbers of the primary document (z-report, payment order, sales receipt, act, invoice, etc.);

- contents of the operation. For example, “Receipt of payment for goods shipped by Gamma LLC”;

- amounts.

If the operation is profitable, then the amount is entered in column 4, if it is expenditure, in column 5.

On the simplified tax system 6%, column 5 is not filled in.

You only need to record those amounts of income and expenses that are included in the tax calculation. For example, receipt and repayment of loans, payment of authorized capital, and contribution of own funds - all this is not considered taxable income, so there is no need to enter such transactions into KUDIR.

A complete list of income and expenses that affect the amount of tax is given in Articles 346.15 and 346.16 of the Tax Code of the Russian Federation, and the recognition procedure is in Article 346.17.

When to enter income

The simplified tax system uses the cash method, which means that all receipts are deposited into KUDiR at the moment the money is received in the current account or at the cash desk.

At what point should you enter expenses (only for simplified tax system 15%)

It all depends on the nature of the expenses.

- Material costs are incurred when the materials are both shipped and paid for. That is, the latest date will appear in KUDiR. If the materials have already been paid for, but not yet received, or vice versa, the amount of expenses is not yet included in taxation and an entry is not made in the KUDiR.

- Expenses for fixed assets (purchase, construction, manufacturing) and intangible assets are paid on the last day of the quarter based on calculations from Section II.

- Expenses for the purchase of goods intended for resale are paid only as they are sold. That is, the purchase price of goods that have not yet been sold and are in storage cannot be taken into account as tax expenses.

In the certificate at the end of section I on the simplified tax system 6%, fill out only line 010.

Based on the final data of KUDiR by quarter and year, advance payments and annual tax are calculated, and a tax return is filled out according to the simplified tax system.

Section II “Calculation of expenses for the acquisition of fixed assets and intangible assets”

This section is intended only for simplifiers with the “Income minus expenses” object.

Data is entered into it only for those fixed assets that have already been put into operation and only within the limits of paid amounts.

Costs must be distributed evenly across the quarters remaining until the end of the calendar year.

For example, if a fixed asset was purchased in February, that is, in the first quarter, for 200 thousand rubles, then the costs will be written off in 50 thousand increments on the last date of the first, second, third and fourth quarters. And if the purchase was made in July, that is, in the third quarter, for 300 thousand, then 150 thousand each must be written off in the third and fourth quarters. Expenses for OS purchased in the fourth quarter will be written off in one amount on the last date of the fourth quarter.

The calculated amount to be written off for the current quarter from column 12 of section II is entered into column 5 of section I on the last day of the quarter.

Columns 7, 8, 14 and 15 are intended for those cases where the fixed asset was purchased before the transition to the simplified taxation system.

Section III “Calculation of amounts of losses from previous periods that reduce the tax base”

This part is also intended only for those who apply the simplified tax system of 15%, had losses in previous periods and can reduce the tax base by the amount of these losses.

Section IV “Expenses that reduce the amount of tax”

This section is filled out by those who apply the simplified tax system of 6%.

It includes the amount of insurance premiums, sick leave paid at the expense of the employer, contributions for voluntary insurance of employees, i.e. those amounts by which the simplified tax system (USN) tax will then be reduced to 6%.

Section V “Calculation of amounts of trade duty that reduces tax”

This part is filled out by those who apply the simplified tax system “Income” and pay a trading fee.

Become a user of the “My Business” service, and you will not have to fill out the Income and Expense Account Book yourself. You will enter data on revenue and expenses, and the service itself will generate a KUDiR and tax return.

If all receipts and expenses go only through a current account, then creating a KUDiR in our service is even easier - you just need to upload a bank statement.

Our service will help you calculate taxes and contributions, report to regulatory authorities and pay taxes. The system accompanies all actions with step-by-step instructions and tips, so the chances of making mistakes are reduced to zero.

Book of movement of labor books

Home / Work book

| Table of contents: 1. General requirements for the log book 2. Instructions for filling out the book 3. Sample of filling out the accounting book 4. Corrections in the book + fines | Document: Download the book of accounting for the movement of labor books Download a sample book |

Current legislation obliges the employer to keep strict records of work records. For this purpose, Rules for maintenance and storage were developed, approved by Decree of the Government of the Russian Federation of April 16, 2003 No. 225 (hereinafter referred to as the Rules).

According to the Rules, each employer must, in the prescribed manner, keep a book of records of the movement of work books and inserts in them. In everyday life, this document is also often called a registration journal or a register of work books.

The accounting book records all movements of work books within the company:

- Receiving a work report from a new employee hired.

- Registration of a new book, if the document is created by the employer’s personnel service in the case where this is the first place of work for the hired employee.

- Issuance of a duplicate if the work book has been lost or has become unusable.

- Filling out the insert if the book runs out of pages.

- Issuance of a book against signature to a dismissed employee or to the employee’s relatives in the event of his death.

General requirements for the work record book

The book is filled out and stored in the administrative service of the organization, whose functions include the hiring and dismissal of personnel: personnel department, accounting, secretariat, etc.

This register is maintained by an official appointed by order of the manager (IP), who is responsible for receiving, recording, storing and issuing work books.

Basic requirements for the appearance of the document:

1) Hardcover. The book has an extremely long shelf life - 75 years. A soft cover will not allow you to keep the document in a usable form for such a period.

2) Continuous numbering. Based on established practice, the magazine can be numbered either page by page or simply by sheet. Since both methods ensure the impossibility of removing individual elements from the document.

3) Firmware. The journal must be stitched and sealed with a wax seal or sealed. This requirement is clearly stated in clause 41 of the Rules, therefore the standard fastening of the free ends of the threads using a pasted sheet of paper containing a certification note will in this case cause complaints from the inspection authorities.

4) Certification record. Done on the back cover of the book and must contain:

- document's name;

- number of sheets (pages), written in numbers and in words;

- log start date;

- signature of the responsible person with a description of the position and full name.

Please note: the head of the organization (IP) must sign the back of the book. The person responsible for maintaining the register does not have the authority to affix a certification signature.

Unlike most accounting journals, the book is not created for one reporting period, but is used from year to year until the pages run out. Upon completion of the current book, a new one is issued.

Instructions for filling out the accounting book

The unified accounting book form was approved by Resolution of the Ministry of Labor dated March 10, 2003 No. 69 (Appendix No. 3) and is a table of 13 columns, which are filled out as follows:

| Column ordinal number | Content |

| 1 | The serial number of the record is indicated |

| 2, 3, 4 | The date of entry is indicated in the format: DD.MM.YYYY |

| 5 | Fill in the full name of the owner of the work book. It is prohibited to indicate initials; first and middle names (if any) must be entered in full |

| 6 | The details of the work book or its insert are indicated. In this case, the details of the insert need to be written down only if it was issued by this company. If a newly hired employee submits a work report containing an insert issued at one of his previous places of work, only the number and series of the book itself are indicated. Details may vary depending on the year the form was issued: from 1938 to 1974 - the unified forms did not have a series or number, so when filling out the details you need to put a dash or write “b/n”; from 1974 to 2003 – work books of the AT-I – AT-X series with a 7-digit number were issued; from 01/01/2004 to the present - work book forms have the series TK, TK-I - TK-V (inserts - VT, VT-I), the number also consists of 7 characters |

| 7 | The employee’s position is filled in strict accordance with the employment contract (hiring order, minutes of the general meeting) |

| 8 | Indicate the short name of the employer and the name of the structural unit (service, department, etc.) in which the employee will work |

| 9 | The details of the employment order or other document on the basis of which the employee takes office are entered. When filling out the insert for the work book, a dash is placed in this column |

| 10 | The signature of the official responsible for maintaining the journal is affixed |

| 11 | The amount contributed by the employee to pay for the new form is indicated. If the employer’s regulations do not provide for charging employees for new forms or the entry is not related to the preparation of a new work book or an insert for it, a dash is placed in this column |

| 12 | The last working day of the employee in this organization is indicated. If an employee went on vacation with subsequent dismissal and received a paycheck and work book on the last working day, you need to write down the date of dismissal according to the order (in this case, such a date will be the last day of vacation) |

| 13 | Depending on the situation:

|

Note: sometimes a new personnel employee, appointed responsible for maintaining work books, discovers that the company’s accounting book was not kept.

In this case, it is necessary to notify the head of the organization (IP) about the identified violation in writing (for example: draw up a report), create a journal and enter in it in chronological order information about all work books stored in the organization.

In this case, there is no need to sign in column 10, since the new responsible employee did not personally accept these labor documents from the employees.

A sample of filling out a book for recording the movement of labor books

How to make corrections to a book

Corrections to the accounting book are entered in the same way as accounting registers are adjusted:

- On the blank line immediately below the erroneous entry or after the last entry, o is entered;

- The line below makes a new entry containing reliable information;

- Under the correct entry, the full name, position and signature of the person who made the changes, as well as the date of the transaction, are indicated.

Responsibility for non-compliance with accounting rules

For non-compliance with the Labor Code of the Russian Federation and other normative acts of labor law, administrative liability is imposed under Art. 5.27 Code of Administrative Offenses of the Russian Federation:

- warning or imposition of a fine on the responsible official (individual entrepreneur) in the amount of 1,000 to 5,000 rubles;

- warning or imposition of a fine on the organization in the amount of 30,000 to 50,000 rubles.

Read in more detail: Book of movement of labor books

Did you like the article? Share on social media networks:

- Related Posts

- Notification of receipt of work book

- Application for issuance of a work book

- Changing the last name in the work book

- Application for issuance of a copy of the work book

- Entry in the work book about the renaming of a position

- Certificate of acceptance and transfer of work books

- An example of a dismissal entry in a work book

- Entry of employment in the work book