Should an individual entrepreneur on a patent keep a book of income and expenses?

An individual entrepreneur on a patent is required to take into account income subject to this taxation system. An income limit has been established for him, upon reaching which the PSN cannot be applied. Confirmation that the size limit has not yet been reached can only be done by accounting in accordance with the rules.

The income of an individual entrepreneur for all patents cannot exceed 60 million rubles per year. If you combine PSN and simplified tax system, income under both tax regimes is considered.

In the book of income and expenses on a patent, an individual entrepreneur must take into account only income from sales. Non-operating income and income under other tax regimes do not need to be reflected.

Income book

According to the Tax Code of the Russian Federation, Article 346.53, paragraph one, all individual entrepreneurs located on the PSN are required to keep an income accounting book (IAL) of their profitability. It consists of a strict reporting form in which the entrepreneur enters the profit received in chronological order. Each individual type of activity has its own CUD. The document is prepared in Russian. It is allowed to keep a book in a foreign language, provided that a translation of the text into Russian is located next to it.

Many people confuse the name KUD with KUDiR (book of accounting for income and expenses), although these are two different documents used in different taxation systems. Therefore, you should not look for a KUDiR for an individual entrepreneur on a patent; in the PSN it is more correct to use the KUDiR sample for filling out 2021.

You can keep a book of income accounting for individual entrepreneurs using the patent taxation system both electronically and in paper form. If accounting is kept on a computer, at the end of the reporting period it is printed, laced and numbered.

Varieties of this type of document preparation include:

- special programs (Bukhsoft, etc.);

- sample form in Excel, which can be downloaded on the Internet;

- online services.

If you choose the option of filling it out by hand, then first the KUD is stitched and numbered, and then the data is entered. The book must have a title page. The reporting itself is maintained in a table where the entrepreneur displays the transactions performed as they occur. Similar transactions during the day are combined and written on one line. Everything is filled out with a black or blue ballpoint pen. On the last page of the KUD, the number of sheets in the book is indicated, a seal (if any) and the signature of the individual entrepreneur are affixed.

An income accounting book is compiled for the duration of the patent and a new one is purchased when the next reporting period occurs. At the same time, only one CUD is carried out in one direction of the patent.

There are no ideal documents; if filled out by hand, errors often occur.

Naturally, no one will rewrite the entire book, so if inaccuracies are discovered, you must:

- Check the source documents on the basis of which the adjustment is made. In the future, they will confirm the validity of the operation.

- Cross out incorrect information.

- Write a correction.

- Certify the edits with the individual entrepreneur’s signature and seal.

If there is an error in the electronic version, everything is much simpler; the document is edited and printed again.

The absence of an income accounting book is fraught with a fine for the entrepreneur in the amount of 10,000 to 30,000 rubles, depending on the scope of the violation. Therefore, we will consider the rules for drawing up this document, which consists of a title page and section I income.

We recommend you study! Follow the link:

Documents and conditions for obtaining a patent for individual entrepreneurs

Rules for maintaining a book of income accounting for individual entrepreneurs on a patent

KUDiR must be filled out in chronological order. All records are kept only in Russian.

Information about income received is entered on the basis of primary accounting documents - payment orders, bank orders, reports on cash register shifts and other documents that an individual entrepreneur can issue instead of cash receipts. They can be compiled both in Russian and in other languages. In the latter case, interlinear translation is required.

You can keep a book of income and expenses for an individual entrepreneur on a patent either on paper or electronically. It opens every calendar year. After the end of the next year, the electronic document must be printed.

The completed pages of the book should be numbered and laced. The last sheet indicates their number. It is confirmed by the signature of the individual entrepreneur and certified by a seal (if you use it in your activities).

We recommend reading: Should an individual entrepreneur on a Patent keep a cash book and deposit cash in the bank?

Making entries

The title page of the income journal indicates information about the individual entrepreneur, the tax period and details of current accounts.

Records of individual entrepreneurs' income are entered in Section I on the day cash is received or money is credited to the account. Returns are reflected with a minus sign. Replenishing an account with an individual entrepreneur’s personal money, receiving or repaying loans are not considered income, and therefore are not entered into the ledger.

When accounting for acquiring receipts, income is offset by the amounts actually paid by buyers. Money from the bank to the individual entrepreneur’s account is received minus the commission, so reflecting only the amount received is not enough.

Example: On May 15, 2021, 14,600 rubles were received into the individual entrepreneur’s current account under an acquiring agreement, the bank’s commission for the operation was 400 rubles. Therefore, for May 15, you need to reflect income in the amount of 15,000 rubles. (14,600 + 400).

The column “Date and number of the primary document” reflects data on the documents on the basis of which the entry is made, for example, “05/15/2020, 13” or “05/23/2020, 9-11”. Documents of the same type can be grouped into one record by specifying the appropriate range of numbers. Here you are also allowed to specify the type of document, then the entries will become as follows: “05/15/2020, bank order 13” and “05/23/2020, BSO 9-11”.

The entry in the column “Content of the transaction” should reflect its economic essence, for example, “Receipt of proceeds from the sale of goods through acquiring”, “Receipt of proceeds from the provision of services in cash” or “Receipt of an advance payment for the performance of work to the current account”.

Income is recorded in rubles accurate to two decimal places, for example, 500.02. The results are summed up for the entire calendar year.

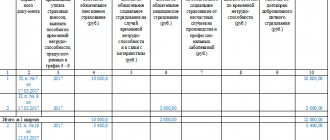

Sample of filling out an income book for an individual entrepreneur on a patent

CUD on a patent is available on the tax website or a specialized reference service for free. You can fill it out according to our sample. It is designed taking into account the most typical retail operations, but can be used as a basis for other types of activities.

An example of filling out the CUD on a patent for retail trade:

Tax accounting under the patent taxation system. Income book

From January 1, 2021, many individual entrepreneurs switched to using PSN. Unlike UTII, when working on a patent you do not need to file a tax return. But individual entrepreneurs have a new responsibility - to keep tax records.

Why should an entrepreneur keep tax records when applying PSN?

One of the restrictions when applying the patent tax system is the limit on the amount of income. An individual entrepreneur loses the right to use PSN if, from the beginning of the calendar year, its revenue exceeds 60 million rubles. This is established by Section 346.45 of the Internal Revenue Code. And in order to track the amount of revenue from a patent, Article 346.53 of the Tax Code introduced an obligation for entrepreneurs to keep records of income from sales in the income book.

How is sales income determined when applying PSN?

With a patent, income is determined on a cash basis. Let us recall that under the cash method, income is considered received on the day of its actual receipt in the current account or cash register of the entrepreneur. Income in foreign currency is accounted for in rubles at the official exchange rate of the Central Bank of Russia on the date of receipt of income.

Revenue is summed up for all types of activities for which the entrepreneur received a patent.

If an entrepreneur combines the simplified tax system and the PSN (which is not prohibited by the Tax Code), income received from activities on the simplified tax system is taken into account when determining the maximum amount of turnover on a patent. That is, income under the simplified tax system and PSN in total should not exceed 60 million rubles from the beginning of the calendar year. Otherwise, the individual entrepreneur loses the right to use PSN.

How is income recorded under PSN?

Accounting for revenue received from “patent” activities is kept in the income ledger. This is the main and only document of an individual entrepreneur, which reflects his income from the patent. Its full name is the Book of Income Accounting for Individual Entrepreneurs Using the Patent Tax System. Its form is approved by the Russian Ministry of Finance. He also approves the procedure for filling it out. Today, the form of the Book approved by Order of the Ministry of Finance of the Russian Federation N 135n dated October 22, 2012 is in force.

From the very title of the book it is clear that it takes into account only the income of individual entrepreneurs. The entrepreneur is not required to take into account the costs of the PSN, since they do not in any way affect the calculation of the cost of the patent or the conditions for applying the PSN.

What sections does the “patent” income accounting book consist of?

The book consists of:

- title page

- Section “Income” (section I)

Rules for maintaining a patent ledger

The book is written in chronological order.

The basis for making an entry in the book is only primary documents.

The book is written in Russian. If the source documents are not in Russian, they must be translated line by line into Russian.

The book can be kept:

- in paper form

- electronic

If the Book is kept electronically, then after the end of the tax period it is printed.

The book must be laced and the pages of the book numbered. Accordingly, on the last sheet of the Book the total number of pages in the Book is indicated. This entry is certified by the signature and seal of the entrepreneur.

In the “Income” section the following is indicated:

- transaction number in order (column 1)

- date and number of the primary document (column 2)

- contents of the operation (column 3)

- amount of income from the operation (column 4)

That is, the book contains revenue for each day broken down by source of income - receipt of cash at the cash register, receipt in the current account, offset of mutual claims, receipt of income in kind. When using CCT, the primary document is the shift report. When receipt of proceeds to the current account - a payment order.

If you have the right not to apply CCT in relation to “patent” activities, then neither the Tax Code nor other Laws and regulations regulate which documents for the purpose of filling out the Income Book will be the primary documents indicating the date and amount of income received. We believe that in this case the entrepreneur independently determines the form of the primary document with which he will capitalize the cash proceeds. Let us recall that the Law “On Accounting” N 402-FZ in Part 2 of Art. 9 establishes mandatory details that must be in primary documents.

To avoid possible disputes with the tax authorities, you can also make an official request to them asking for clarification on which document to use to record cash proceeds in your particular situation.

Consequences of the absence (ignorance or failure to submit) of the individual entrepreneur’s accounting book on the PSN

Of course, the absence of an accounting book will not be the reason why an individual entrepreneur may lose the right to PSN.

However, failure to keep a book or failure to provide it at the request of the tax authority can lead to very serious consequences for an individual entrepreneur.

1.

Penalties

by the Tax Code of the Russian Federation, namely clauses 1 and 2 of Art. 120 of the Tax Code provides for a fine for gross violation of income accounting rules, even if they do not lead to tax violations. The fine is set at 10,000 rubles.

And if you do not keep a book for more than one tax period, the fine will already be 30,000 rubles.

2. Determining the amount of income of an individual entrepreneur according to the tax authority

Let us recall that an entrepreneur loses the right to use PSN if his income exceeds 60 million rubles from the beginning of the calendar year. And it is precisely in the income book that the individual entrepreneur is required to keep this record.

If an entrepreneur does not keep a book of income, he will not be able to present it to the tax authorities. Accordingly, the tax office will not be able to check whether you comply with the income limit.

The Tax Code provides for this situation. Tax authorities are given the right to determine the amount of income by calculation. The Plenum of the Supreme Arbitration Court of the Russian Federation, in its Resolution No. 57 of July 30, 2013, indicated that this approach is used even if instead of a book the entrepreneur presents other income accounting documents - for example, bank statements, cash register data and others.

Now imagine that if a violation is detected in February, the entrepreneur will pay a fine of 10,000 rubles, in March - already 30,000 rubles, in April - another 30,000 rubles. and so on. It's quite expensive to break the law, wouldn't you agree?

In fact, keeping records of income correctly, without violations and unnecessary risks, is not as difficult or expensive as it seems.

For our clients, from 01/01/2021, anti-crisis tariffs began to apply for keeping records of individual entrepreneurs’ income under the PSN and simplified tax system.

What is included in our services:

- Maintaining daily records in KUDIR for cash receipts

- Maintaining daily records in KUDIR on receipt of funds from acquiring

- Sending a new form of notification to the Federal Tax Service on payment of insurance premiums

- Calculation of the total cost of the patent to be paid minus insurance premiums

- Monitoring the payment of taxes and contributions and preparing all documents for payment

- Monitoring the expiration of a patent and ordering a new patent

The cost of the full package of services is from 2,100 rubles. per month (keeping records for one settlement object). Obviously, this amount is not comparable to the amount of fines when tax violations are detected, so it is not worth saving. Contact professionals right away so you can do what you love with peace of mind.

Shelf life of KUD

The patent income book must be kept for at least 5 years. The specified period begins on January 1 of the year following the reporting year. Before its expiration, the tax office has the right to request the CUD to conduct an audit. If you do not provide it within 10 days, you will be charged a fine of 200 rubles.

We recommend reading: Individual entrepreneur on a patent and VAT: in what cases you need to pay.