Accounting books for individual entrepreneurs: new forms

Resolution of the Ministry of Taxes and Taxes dated January 30, 2019 No. 5 approved the Instructions on the procedure for keeping records of income and expenses (hereinafter referred to as Instruction No. 5) and the forms of accounting documents for individual entrepreneurs. The specified documents apply from 04/05/2019.

Instruction No. 5 determines the procedure for keeping records of income and expenses for individual entrepreneurs <*>:

— paying income tax from individuals <*>;

— paying a single tax <*>;

- applying the simplified tax system and keeping records in the Book - in relation to income subject to income tax, and if they decide to keep records of income and expenses on a general basis <*>.

In addition, individual entrepreneurs on the simplified tax system with accounting in the Book must be guided by Instruction No. 5 when drawing up primary accounting documents and drawing up written decisions on the principles and methods of accounting <*>.

Instruction No. 5 establishes a list of new forms of accounting documents (Appendices 2 - 11), which must be maintained by individual entrepreneurs depending on the tax they pay. As before, accounting documents can be maintained both on paper and in electronic form <*>.

Let us consider the main changes that have occurred in the forms of books and the procedure for maintaining records.

Previously, individual entrepreneurs paying a single tax kept records of revenue for tax purposes in Section I of the book of accounting for gross proceeds from the sale of goods (work, services), accounting for goods imported into the territory of the Republic of Belarus from member states of the EAEU. From 04/05/2019, individual entrepreneurs are required to account for revenue in a separate ledger for accounting for revenue from the sale of goods (work, services) <*>. Compared to the previous edition, the names of the columns in the new book have not changed.

In the book of total accounting of goods, the names of some columns have been changed. This is due to the fact that now the book should take into account goods intended for retail and (or) wholesale trade <*>. Previously, this book was intended only for accounting for goods in retail trade <*>.

The forms of accounting books have not changed, compared to previously existing books:

— fixed assets <*>;

— intangible assets <*>;

— individual items as part of working capital <*>;

— raw materials <*>;

— goods (finished products) <*>.

At the same time, the individual entrepreneur is given the right not to use the above books. In return, they need to develop their own forms, providing them with the necessary indicators for maintaining records and calculating the tax base <*>.

Note that currently individual entrepreneurs are given the opportunity to maintain one general accounting document. In this case, in its individual sections, in accordance with the specifics of the activity, accounting of fixed assets, intangible assets, individual items as part of working capital, raw materials and supplies, goods (finished products), VAT, total accounting of goods <*> is carried out. Previously, this possibility was not provided.

Changes have been made to the names of individual columns in the book of income and expenses. This is due to the fact that in 2021 individual entrepreneurs - “income earners” - are given the right to choose the principle of accounting for income from sales (by payment or by shipment) <*>.

Please note that now, when paying income to individuals in cash, individual entrepreneurs have the right to draw up a payslip in any form. At the same time, it must contain the mandatory details for primary accounting documents <*>.

How to simplify the accounting of goods by individual entrepreneurs

Currently, accounting for the receipt and sale (disposal) of goods by individual entrepreneurs is carried out in the book of accounting of goods (finished products) (hereinafter referred to as the book of accounting of goods) in the form in accordance with Appendix 6 to the Instructions on the procedure for keeping records of income and expenses by individual entrepreneurs (notaries performing notarial activities in a notary office, lawyers carrying out legal activities individually), approved. by resolution of the Ministry of Taxes and Taxes of December 24, 2014 No. 42 (hereinafter referred to as Instruction No. 42)

Such records are kept for each supplier in the context of each document confirming the purchase (receipt) of goods, indicating the name (variety, article) of the goods. For each name (variety, article) of goods, the required number of lines is allocated. In order to simplify the maintenance of individual accounting of goods in retail trade, the Ministry of Taxation proposes to grant this category of payers the right to carry out accounting of goods in total terms, in the context of each shipping document confirming the purchase (receipt) of goods. Therefore, it is proposed to supplement Instruction No. 42 with a separate appendix “Book of total accounting of goods”, as well as a separate chapter “Total accounting of goods”.

The Ministry of Taxation requests that comments and suggestions on the draft chapter “Total accounting of goods” (together with the appendix “Book of total accounting of goods”) be sent no later than 04/21/2017 to an email address marked “ On the accounting of individual entrepreneurs”.

Project

CHAPTER

TOTAL ACCOUNTING OF GOODS

In retail trade, records of the receipt and sale of goods can be kept in total terms in the book of total accounting of goods in the form according to the appendix to the Instructions. The accounting procedure provided for in this chapter cannot be changed during the calendar year. In the book of total accounting of goods, goods intended for retail sale are subject to capitalization. The receipt of goods is carried out in the context of each commodity accompanying document confirming the purchase (receipt) of goods. Column 2 of the book of total accounting of goods indicates the date and number of the accompanying document confirming the purchase (receipt) of goods, or a calculation certificate in which the price of a unit of goods is calculated.

A calculation certificate is drawn up if the price of goods includes expenses associated with the acquisition of goods (commissions, customs duties, transportation costs, storage and other expenses associated with the acquisition (production) of goods). Such expenses are accounted for at actual prices (at negotiated prices, including VAT, if it is not deductible). At the same time, the invoice certificate, along with the data of the shipping document confirming the purchase (receipt) of goods, indicates the documents on the basis of which the specified expenses were made (agreements, invoices, etc.). The invoice certificate must be signed by the individual entrepreneur or the person responsible for this. authorized.

Column 5 of the book of total accounting of goods reflects the cost of received goods, indicated in the document confirming their acquisition (receipt), including VAT, if it is not accepted for deduction, or in the calculation certificate. Column 6 of the book of total accounting of goods indicates the retail price established by the individual entrepreneur. When establishing retail prices, a calculation must be drawn up indicating the amount of the applied trade markup to the selling price of the manufacturer (importer), hereinafter referred to as a register of retail prices. The register of retail prices is compiled in the context of each commodity accompanying document confirming the purchase (receipt) of goods, for each name (variety, article) of goods specified in this document.

If the initially calculated selling price of goods changes, the individual entrepreneur conducts an inventory of the balances of the relevant goods and compiles a new register of retail prices. At the same time, in the period in which the selling price changes, the indicator in column 6 of the book of total accounting of goods is adjusted by the amount of the change in the cost of goods in selling prices (a positive value - when the selling price increases, a negative value - when the selling price decreases).

In columns 7 and 8 of the book of total accounting of goods for goods received, records are made of their payment indicating the date, number of the payment document and the amounts paid for the purchased goods. If an advance payment has been made for the goods, the amount of which is reflected in column 10 of the book of accounting for income and expenses, in the book of total accounting of goods, payment for goods is reflected only as the paid goods are received, while simultaneously filling out columns 2, 5 and 6 of the book of total accounting of goods.

When switching to the application of the procedure for accounting for goods provided for by this chapter, filling out columns 3, 4, 7, 8 of the book of total accounting of goods is carried out on the basis of the data of the inventory report.

Depending on the method of retail sale of goods (individual service, sale of goods by samples, sale of goods by pre-orders, etc.), the form and method of calculation, column 9 of the book of total accounting of goods is filled out:

when using cash register equipment to accept cash - on the basis of daily (shift) reports (Z-reports);

when selling goods through vending machines - based on the data reflected in the monthly sales reports provided by the Republican Unitary Enterprise "Information and Publishing Center for Taxes and Duties";

when making non-cash payments using bank payment cards - on the basis of a payment order from the acquiring bank for the transfer of funds debited from the buyers' card accounts. In this case, column 6 reflects the total amount of funds written off from the buyers’ card accounts, taking into account the commission retained by the acquiring bank in accordance with the acquiring agreement;

in retail trade based on samples with delivery of goods by postal cash on delivery - on the basis of a receipt (other document) for a postal money order issued by the postal operator.

The totals for the current quarter in columns 10 and 13 of the book of total accounting of goods are transferred to the next quarter in columns 4 and 3 of the book of total accounting of goods, respectively.

Column 12 of the book of total accounting of goods indicates the value of the average percentage of the purchase price of goods in the cost of goods sold, rounded according to mathematical rules with an accuracy of 2 decimal places.

At the end of the reporting (tax) period, the total amounts for the quarter in columns 9 and 14 of the book of total accounting of goods are transferred, respectively, to columns 4 and 9 of the book of accounting for income and expenses.

In this case, the cost of goods sold in purchase prices is transferred from the book of total accounting of goods within the limits of the amounts paid for the goods:

in the first quarter – the cost of goods sold at purchase prices in column 14 of the book of total accounting of goods within the amount indicated in column 8 of the book of total accounting of goods in the line “Total for the first quarter”;

in the II (III, IV) quarter - the cost of goods sold in purchase prices according to column 14 of the book of total accounting of goods on the line “Total cumulative total from the beginning of the year” for the second (third, fourth) quarter within the amount indicated in column 8 of the book of total accounting of goods in the line “Total cumulative total from the beginning of the year” for the first (second, third) quarter minus the purchase cost of goods sold, transferred in the first (second, third) to column 9 of the book of income and expenses.

In cases where in the book of total accounting of goods, the amount of payment for goods made in the expired calendar year, in column 8 in the line “Total cumulative total from the beginning of the year” for the fourth quarter exceeds the cost of goods sold at purchase prices in the expired calendar year in column 14 according to the line “Total cumulative total since the beginning of the year” for the fourth quarter:

in column 8 of the book of total accounting of goods in the line “Total on an accrual basis from the beginning of the year” for the fourth quarter, the amount of such excess is displayed and the entry “Transferred to the first quarter of 20__ (the next calendar year is indicated);

in column 8 of the book of total accounting of goods for the first quarter of the next calendar year, the indicated excess of the amount of payment to suppliers for goods over the amount of expenses is transferred and the entry is made: “Paid to suppliers in the fourth quarter of 20__” (the expired calendar year is indicated).

When the buyer returns goods sold by an individual entrepreneur, on the date of such return the indicator in column 9 of the book of total accounting of goods is adjusted (by entering a negative value).

When an individual entrepreneur returns goods to the seller (supplier), on the date of such return, the indicators in columns 3 and 4 of the book of total accounting of goods are adjusted (by entering a negative value).

When disposing of (transferring) goods, the cost of which is included in the book of total accounting of goods, for purposes not related to their retail sale, columns 2, 5, 6 and 8 of the book of total accounting of goods are filled in.

Column 2 of the book of total accounting of goods indicates information about the person in whose favor the goods are disposed of (if any), as well as the date and number of the document on the basis of which the goods are disposed of (shipping documents, write-off acts, disposal acts, etc.) .

For the cost of disposed (transferred) goods for reasons not related to retail sales, the indicators of columns 5, 6 and 8 of the book of total accounting of goods are reduced (by entering a negative value). In this case, column 8 of the book of total accounting of goods is filled in provided that the corresponding goods were paid for at the time of such disposal. At the same time, disposed goods are recorded in the goods accounting book (finished products).

Data on the cost of goods sold in acquisition prices (expenses for the purchase of goods) and in sales prices is clarified during the inventory of goods, carried out at least once a year.

During the inventory, the actual presence of remaining goods at purchase prices and at sales prices is checked. When a shortage of goods is established based on the inventory results:

as a result of natural loss, within the limits established by law, data on their value in purchase prices from column 3 of the book of total accounting of goods (a negative value is entered) is transferred to column 9 of the book of accounting of income and expenses within the amount reflected in column 8 of the book of total accounting of goods;

in excess of the norms of natural loss, in column 6 of the book of income and expenses, the amount of income is reflected, defined as the difference between the discrepancy in the cost of goods in sales prices, identified by the results of the inventory in relation to accounting data, and the corresponding discrepancy in the cost of goods in acquisition prices (minus the cost of goods disposed of). as a result of natural loss within the limits established by law).

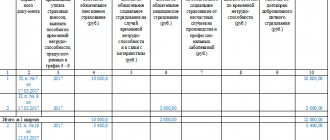

Application

Book of total accounting of goods

for ____________________ year (four digits of the year)

| Recording date | Name of the document, its date and number | Cost of goods in balances at the beginning of the quarter (RUB) | Cost of goods received (RUB) | Paid | Cost of goods in selling prices (RUB) | Average percentage of purchases of the cost of goods in the cost of goods sold ((gr.3+gr.5)/gr.11x100) | Cost of goods in balances at the end of the quarter in purchase prices (rub.) (gr. 10xgr. 12/100) | Cost of goods sold in purchase prices (RUB) (gr.3+gr.5-gr.13) | |||||

| in purchase prices | in sales prices | in purchase prices | in sales prices | date, payment instruction number | amount* (RUB) | sold during the quarter | in balances at the end of the quarter (column 4+gr.6-gr.9) | total (gr.9+ gr.10) | |||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

| X | X | X | X | X | X | X | |||||||

| Total for the I (II, III, IV) quarter | X | X | X | ||||||||||

| Total cumulative total since the beginning of the year | X | X | X | X | X | ||||||||

*the line “Balance at the beginning of the tax period” indicates the amount of excess payment over the cost of purchased goods for the previous tax period