The deadline for submitting annual accounting (financial) statements for 2021 is approaching. In what cases is an audit mandatory?

An exhaustive list of grounds for conducting a mandatory audit of the accounting (financial) statements of companies is given in Article 5 of the Federal Law of December 30, 2008 No. 307-FZ “On Auditing Activities” (hereinafter referred to as Law No. 307-FZ).

AUDITING SERVICES

Thus, the following are subject to mandatory audit:

- all joint-stock companies without exception (regardless of type - CJSC, OJSC, PJSC and JSC);

- credit, insurance, clearing organizations, mutual insurance companies, organizations that are professional participants in the securities market, funds (non-state pension funds (except for state extra-budgetary funds), mutual funds, AIF);

- companies with revenue from the sale of products (goods, works, services) for the previous reporting year exceeding 400 million rubles (with the exception of state and local government bodies, state and municipal institutions, state unitary enterprises and municipal unitary enterprises, agricultural cooperatives and their unions) or with the amount balance sheet assets at the end of the previous reporting year exceeded 60 million rubles;

- companies whose securities are admitted to organized trading, presenting and (or) publishing summary (consolidated) accounting (financial) statements. Exceptions include bodies of state power and local self-government, state extra-budgetary funds, as well as state and municipal institutions;

- companies in other cases established by federal laws.

For example

, for organizers of gambling, the obligation to conduct an audit is established by clause 12 of Article 6 of the Law of December 29, 2006 No. 244-FZ “On state regulation of activities for the organization and conduct of gambling and on amendments to certain legislative acts of the Russian Federation”, for political parties - Federal Law of July 11, 2001 No. 95-FZ “On Political Parties”, for the Russian Science Foundation - Federal Law of November 2, 2013 No. 291-FZ “On the Russian Science Foundation and Amendments to Certain Legislative Acts” RF".

Mandatory audit of accounting (financial) statements for 2018

The list of cases of mandatory audit of accounting (financial) statements for 2021 is given in Letter of the Ministry of Finance of the Russian Federation dated January 15, 2019, No. b/n.

Thus, the following are subject to mandatory audit:

- state corporations and companies, state companies (clause 2 of article 7.1 and clause 8 of article 7.2 of the Federal Law of January 12, 1996 No. 7-FZ);

- microfinance companies (clause 4 of article 15 of the Federal Law of July 2, 2010 No. 151-FZ);

- lottery operators (Article 23 of the Federal Law of November 11, 2003 No. 138-FZ);

- organizers of gambling (clause 12 of article 6 of the Federal Law of December 29, 2006 No. 244-FZ);

- management companies and specialized depositories carrying out activities provided for by Federal Law No. 117-FZ of August 20, 2004 (clause 1 and clause 2 of Article 29 of Law No. 117-FZ);

- housing savings cooperatives (clause 1 of article 54 of the Federal Law of December 30, 2004 No. 215-FZ);

- credit cooperatives, if the number of individuals who are its members exceeds 2,000 people (Clause 1, Article 31 of the Federal Law of July 18, 2009 No. 190-FZ);

- organizations that are self-regulatory organizations (clause 4 of article 12 of the Federal Law of December 1, 2007 No. 315-FZ);

- organizations that are developers that attract funds from participants in shared construction for the construction of apartment buildings and (or) other real estate (except for industrial facilities) (clause 5 of article 3 of the Federal Law of December 30, 2004 No. 214-FZ);

- tour operators operating in the field of outbound tourism (if the total price of the tourist product in the field of outbound tourism for the previous year amounted to more than 400 million rubles) (Article 17.7 of the Federal Law of November 24, 1996 No. 132-FZ);

- other organizations in cases established by Federal laws.

Criteria for conducting a mandatory audit 2018

The main regulatory act that regulates the reporting of an enterprise upon request in the Russian Federation is 307-FZ. According to Article 5 of this law, a list of criteria and subjects of mandatory audit is defined.

The criterion for a mandatory audit is a legal or cost basis. Legal grounds for carrying out control are the belonging of a business entity to a certain type of organizational and legal form or to a specific area. The second point is exceeding restrictions on revenue or volume of assets. If a legal entity complies with the specified points, the audit for it will be mandatory.

Taking into account the latest changes, legal entities are required to undergo control if the two years preceding the reporting period:

- the amount of revenue is more than 800,000,000 rubles;

- the amount of assets on the balance sheet is above 400 million rubles;

- The official number of personnel is more than 100 people.

According to the legal criterion for conducting a mandatory audit, the following are subject to annual control:

- joint stock companies;

- credit companies;

- trade organizers;

- professional participants of the RCB;

- companies providing insurance and clearing services;

- non-state pension funds and their managers;

- investment, mutual funds and their managers.

Changes to mandatory audit criteria in 2021 are aimed at exempting small businesses from inspections by bringing revenue and staff indicators into strict compliance with standards.

Requirements for a chief accountant

The status of a small business entity does not always save you from an audit

Let us recall that on June 20, 2021, Order No. 64n of the Ministry of Finance of Russia dated May 16, 2016 came into force, changing simplified accounting methods for small and non-profit organizations. This means that small companies will be able to prepare reports for 2021 using simplified forms. A simplified reporting procedure can be used by organizations that are allowed to conduct accounting in a simplified way.

MANDATORY AUDIT

Such organizations include (Article 7 of the Law of December 6, 2011 No. 402-FZ “On Accounting”):

- small businesses;

- NPO;

- organizations that have received the status of participants in the Skolkovo project.

The criteria by which companies are classified as small businesses are established by Federal Law No. 156-FZ dated June 29, 2015:

- the amount of revenue for the previous year from the sale of goods, works or services (excluding VAT) does not exceed 800 million rubles;

- the average number of employees is no more than 100 people;

- the share of third parties in the authorized capital of the company is no more than 49 percent.

Such small companies can conduct accounting in a simplified way. The indicators of the accounting reporting items also depend on the chosen method of accounting.

But the situation changes dramatically if a small company is subject to mandatory audit. In this case, the company is faced with the need to generate a complete set of financial statements, ensure that differences between accounting and tax accounting are maintained in the accounts (i.e. apply PBU 18/02*, approved by Order of the Ministry of Finance of the Russian Federation dated November 19, 2002 No. 114n), create a reserve for vacation pay (i.e. apply PBU 8/2010, approved by Order of the Ministry of Finance of the Russian Federation dated December 13, 2010 No. 167), etc.

Note*

It is possible to refuse to use PBU 18/02 only if a small enterprise has the right to use simplified methods of accounting. And “little ones” who are subject to mandatory audit do not have the right to do this (clause 1, clause 5, article 6 of Law No. 402-FZ).

If a company applies special tax regimes (UTII, simplified tax system, unified agricultural tax), then PBU 18/02 can not be applied, having stated this in the accounting policy.

Usually

, a small enterprise with the organizational and legal form of a joint-stock company is deprived of such simplified benefits (clause 1, clause 1, article 5 of the Federal Law of December 30, 2008 No. 307-FZ “On Auditing Activities”, hereinafter referred to as Law No. 307-FZ ). At the same time, the legislation of the Russian Federation provides for a special procedure for conducting a mandatory audit in a joint-stock company, in the authorized capital of which there is a certain share of state participation (clause 4 of article 5 of Law No. 307-FZ).

The “baby” may have revenues from the sale of products (goods, works, services) for the previous reporting year amounting to more than 400 million rubles, or the amount of balance sheet assets at the end of the previous reporting year - more than 60 million rubles (clause 5, clause 1, art. 5 of Law No. 307-FZ). And in this case, a small enterprise is subject to mandatory audit and you can forget about simplified forms of accounting reporting.

AUDITOR CONSULTATION

The concept of mandatory audit, which is the criterion for its conduct

Mandatory audit is a set of verification activities carried out by:

- annually;

- independent auditors;

- to express an opinion on the reliability of accounting (financial) statements;

- in relation to an economic entity falling under the legally established criteria.

This follows from paragraph 3 of Art. 1, paragraph 2, art. 5 of the Law “On Auditing Activities” dated December 30, 2008 No. 307-FZ.

The main criteria for mandatory audit are listed in paragraph 1 of Art. 5 of Law No. 307-FZ and in tabular form can be presented as follows:

| Mandatory audit criteria | Reference to subparagraph 1 of Art. 5 of Law No. 307-FZ | |

| group | content | |

| Organizational and legal form (OLF) | Joint Stock Company (JSC) | Subp. 1 |

| Features of the activity | The organization's securities (securities) are admitted to organized trading | Subp. 2 |

| Kind of activity | The organization is a credit history bureau (credit history bureau), a professional participant in the securities market, a non-governmental pension fund (non-state pension fund) or another fund, etc. | Subp. 3 |

| Financial indicators |

| Subp. 4 |

| Preparers of consolidated financial statements | The organization presents and (or) discloses annual summary (consolidated) financial statements | Subp. 5 |

| In other cases established by federal laws | Subp. 6 | |

Find out what other criteria taxpayers may encounter in the course of their activities from the materials on our website:

- “Criteria for incentive payments to teachers in 2016”;

- “Commentary to Art. 105.14 Tax Code of the Russian Federation" .

What if, contrary to the law, the company submits reports using simplified forms?

In the event that the balance sheet and financial results report are presented in simplified forms instead of the generally established (full) forms, or failure to submit certain forms of reports (appendices) may result in the company and its officials being held liable under clause 1 of Article 126 of the Tax Code of the Russian Federation, Part. 1 Article 15.6 of the Code of Administrative Offenses of the Russian Federation.

And according to clause 1 of Article 126 of the Tax Code of the Russian Federation, failure by the taxpayer to submit documents and (or) other information provided for by the Tax Code of the Russian Federation and other acts of legislation on taxes and fees to the tax authorities within the prescribed period entails a fine of 200 rubles for each document not provided.

INITIATIVE AUDIT

Responsibility for violations of the rules

Accounting verification is carried out upon request, otherwise the company faces serious fines. The requirement and deadlines for submitting conclusions to statistical authorities are clearly regulated by Art. 18 No. 402-FZ.

It is worth noting that the law provides for administrative liability not for refusal to undergo an inspection, but for failure to provide a report on its conduct. The penalties provided for in this case (regulated by the norms of the Code of Administrative Offenses):

- If the auditor's report is not submitted to the territorial statistics department on time, then for legal entities they are punished with a fine of up to 5,000 rubles, for an official - no more than 300-500 rubles. A fine is also provided for incomplete accounting reports. A repeated violation of this kind threatens not only a fine, but also disqualification for several years.

- If the joint-stock company does not publish the audit report on its website: employee liability - 30-50 thousand rubles, or disqualification from activities for a year or two, legal entity - from 700 thousand to 1 million rubles.

- For failure to submit the results of the audit on time to the EDF, legal entities face administrative liability in the form of a fine in the amount of 5-50 thousand rubles.

- If a tax audit reveals that the organization did not keep the report for the required 5 years, a fine of 5-10 thousand rubles is imposed.

Thus, changes in the mandatory audit criteria in 2018 are intended to make expert opinions more informative and transparent, as well as slightly ease the burden on small businesses.

Similar articles

- Criteria and subjects of mandatory audit

- Mandatory audit

- Main tasks and goals of auditing cash transactions

- Calculation of the level of materiality in an audit (example)

- Audit of enterprise financial statements

How is the fine amount calculated?

When calculating the fine, the full list of documents that the company must submit is taken into account (letters of the Federal Tax Service of the Russian Federation dated November 16, 2012 No. AS-4-2/19309, Ministry of Finance of the Russian Federation dated May 23, 2013 No. 03-02-07/2/ 18285).

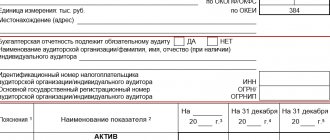

Thus, as part of the financial statements for 2021, the company must submit:

- balance sheet;

- income statement;

- statement of changes in equity;

- cash flow statement;

- explanations in tabular and text forms.

If the company fails to submit its financial statements on time, the fine will be 1,000 rubles (200 rubles × 5).

If the financial statements are not submitted to Rosstat of the Russian Federation in full, an administrative fine will be charged.

The head of the company faces a fine of 300 to 500 rubles, and the company itself can be fined in the amount of 3,000 to 5,000 rubles (Article 19.7 of the Administrative Code, letter of Rosstat of the Russian Federation dated February 16, 2016 No. 13-13-2/28-SMI) .

AUDIT OF JOINT STOCK COMPANY (JSC)

For small joint-stock companies, mandatory audit will be canceled

Who meets the criteria?

Today we will talk about mandatory audits for joint stock companies. Legislators have singled out the obligation to conduct audits by joint-stock companies as a separate case. Currently, if the legal form of a company contains the name “joint stock company”, you have an obligation to conduct an audit. In this case, it does not matter what turnover your company has, whether you are conducting business activities, whether this form was chosen by the owners when establishing the company or the JSC form it acquired after the transformation also does not play the role of JSC or PJSC.

Currently, there is a public joint-stock company (PJSC) and a non-public joint-stock company (NAO).

Public joint stock company (PJSC)

In a public joint stock company, anyone can purchase shares. Large companies are publicly listed on stock markets. Any investor can purchase a block of shares on the exchange without any additional questions or requirements. They are required to be completely transparent and make annual reports on financial results publicly available. The authorized capital must be at least 1000 minimum wages. Moreover, its formation can be carried out during the registration of a PJSC. The number of shareholders is not limited.

Non-public JSC

A non-public joint stock company is a business community whose shareholders are strictly determined at the stage of creating the organization and forming the authorized capital.

The number of owners holding shares of such a JSC is limited by the charter documents. The securities of such a company do not go into free circulation and cannot be sold outside the circle of shareholders, for example, put up on the stock exchange.

So, regardless of what form your joint stock company is, an audit of its activities is currently mandatory.

So how much will an audit cost you for a small joint-stock company?

A simple search in a search engine gives a minimum figure of 50,000 rubles, the upper limit, as you understand, depends on many parameters and can reach several million rubles, and in large public joint stock companies the cost of an audit can cost several million dollars.

But we are now talking about small joint-stock companies, so the figure of 50-100 thousand rubles is reasonable for a joint-stock company when things are going well. But now, during a pandemic, when any expenses can negatively affect the activities of small joint-stock companies, auditing is becoming quite a burden.

And here is great news that the owners of the joint-stock company will rejoice at and the auditors will be upset).

As the professional magazine “Joint Stock Company” writes, the Ministry of Economic Development has published draft laws for public discussion that propose to make annual audits of financial statements optional in small non-public joint stock companies (JSCs).

Refusal from an audit will be possible by unanimous decision of the shareholders of such companies, the ministry’s bills say.

According to the projects of the Ministry of Economic Development, the option of refusing the annual audit will be available only to small

JSC – with revenue not exceeding 400 million rubles or asset value up to 60 million rubles.

A similar business size limit is now set for limited liability companies (LLC), which have the right to avoid an annual audit until these thresholds are reached.

In any case, non-public joint-stock companies in which the state or municipality has a share, as well as banks, credit history bureaus, insurers, organizations that are professional participants in the securities market, clearing organizations will not be able to avoid an audit - they are required to do such an audit according to the law “On Auditing”. activities."

The changes are in demand by the business community and help optimize the activities of small joint-stock companies, as well as removing additional financial burden from them,” says the explanatory notes to the projects on the unified portal for disclosing information about upcoming draft regulations. The Ministry of Economic Development proposes to amend the Civil Code (Civil Code) of the Russian Federation and the laws “On joint stock companies” and “On auditing activities”.

A very timely and correct initiative.

I hope that not much time will pass from the bill to its entry into force. The first digital registrar STATUS takes care of its clients; if you need the services of an auditor, you can use the services of trusted partners, leave a request, they will call you back!

JSC mandatory audit 2021

1. After the audit, the CJSC is obliged to enter information into the “Unified Federal Register of Legally Significant Information on the Facts of the Activities of Legal Entities, Individual Entrepreneurs and Other Economic Entities” https://se.fedresurs.ru/

Deadline: no later than 3 business days from the date of drawing up the audit report.

2. Fine for not posting information (Part 6 and Part 7 of Article 14.25 of the Code of Administrative Offenses of the Russian Federation):

— from 5,000 rubles to 10,000 rubles;

- repeated violation entails a fine of 50,000 rubles or disqualification from one to three years.

3. The audit must be carried out before the annual report is submitted to the owners for approval. The obligation to hold annual meetings to approve the annual balance sheet is determined by your Charter (Clause 1, Article 47, Federal Law of December 26, 1995 N 208-FZ (as amended on March 7, 2018) “On Joint Stock Companies”). And the annual report must include an auditor's report. The deadline for holding a meeting to approve the annual report for 2021 of the CJSC is 06/30/19 and before convening the annual meeting, the board of directors must approve the reporting no later than 25 days before the meeting of shareholders.

Those. for 2021 preliminary approval of reporting by the Board of Directors until 06/03/2019.

Without approval of the annual report, dividends cannot be paid, and if the head of the organization evades conducting a mandatory audit, liability is provided.

clause 2 art. 15.23.1. Code of the Russian Federation on Administrative Offenses dated December 30, 2001 N 195-FZ Violation of the procedure or deadline for sending (delivery, publication) a notice of a general meeting of shareholders (general meeting of owners of investment shares of a closed-end mutual investment fund), as well as failure to provide or violation of the deadline for providing information (materials) subject (to be) provided in accordance with federal laws and other regulatory legal acts adopted in accordance with them, in preparation for holding a general meeting of shareholders (general meeting of owners of investment shares of a closed-end mutual investment fund) - entails the imposition of an administrative fine on citizens in the amount of two thousand to four thousand rubles; for officials - from twenty thousand to thirty thousand rubles or disqualification for a period of up to one year; for legal entities - from five hundred thousand to seven hundred thousand rubles.

What documentation of a CJSC is subject to mandatory audit

According to the provisions of the Federal Law “On Accounting”, audits of closed joint stock companies and other economic entities subject to audit are not carried out on the basis of simplified financial statements, as this may negatively affect the results of its implementation.

List of documents in which annual financial statements should be displayed:

- balance sheet;

- financial report on the results of activities performed;

- a report showing changes in the authorized capital;

- financial report, which details the flow of funds in the accounts of the joint-stock company;

- explanations (the presence/absence of this document directly depends on the specifics of the organization’s activities).