Introduction

Tax accounting is a system for summarizing information on income and expenses to determine the tax base for profits based on data from primary documents.

Organizations choose a tax accounting system independently; the procedure for maintaining it is established by each organization in its accounting policy for tax purposes, approved by the relevant order (directive of the manager).

If the taxpayer determines income and expenses using the accrual method, then production and sales expenses incurred during the reporting or tax period are divided into direct and indirect in accordance with the requirements of Articles 318 and 320 of the Tax Code.

Direct costs in the generally accepted sense are the costs of raw materials from which specific products are directly manufactured, as well as those expenses of the organization that can be clearly attributed to any type of goods, work or services. Article 318 of the Tax Code includes direct costs as material costs, expenses for remuneration of personnel involved in the production of goods, performance of work or provision of services, the amount of the unified social tax and expenses for compulsory pension insurance, used to finance the insurance and funded part of the labor pension. , accrued on the specified amounts of labor costs, as well as the amount of accrued depreciation on fixed assets used in the production of goods, works or services.

However, most organizations also incur expenses that cannot be directly correlated with the production of one specific type of goods, the provision of one type of service, or the performance of a specific type of work. Therefore, such costs are distributed among all types of products. Such costs are called indirect.

Undoubtedly, it is beneficial for the organization to include as many expenses as possible into indirect expenses, since they reduce the income tax base in the period in which they were incurred (clause 2 of Article 318 of the Tax Code). Direct expenses related to work in progress, finished products in the warehouse, as well as shipped but not sold products are not written off in the current period (Article 319 of the Tax Code).

The list of expenses that Article 318 of the Tax Code classifies as direct expenses is advisory in nature. In a letter from the Ministry of Finance dated January 26, 2006 No. 03-03-04/1/60, financiers concluded that all organizations must have a list of direct costs, however, an organization can prescribe in its accounting policy a list different from the one proposed in the article 318 of the Tax Code.

The relevance of this issue lies in the fact that in accounting and tax accounting there was and still is a different understanding of direct and indirect costs, and disclosing this topic will help to avoid mistakes in maintaining both accounting and tax accounting.

Results

Decisions made by an organization regarding its accounting policies (both according to accounting and legal accounting) are enshrined in an internal document. Appendices to this document include, in particular, lists of items for the accounting accounts used in accounting. If these lists contain a comparison with the types of expenses involved in calculating the income tax base, then they can be used as transcripts reflecting the division of expenses into direct and indirect for tax purposes.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Expense breakdowns required for accounting policies

Cost analytics are also developed by the organization independently. It should be carried out not only in relation to each of the departments, but also by type, item and element of expenditure. By type, expenses in accounting will be divided:

- to direct ones, collected on accounts 20, 23, 29 depending on the importance of production (main, auxiliary, servicing);

- invoices, divided into general production (account 25), general economic (account 26), commercial (account 44);

- others (account 91).

Read more about the features of accounting for overhead costs in the article “Procedure for accounting for overhead costs in accounting.”

For each type of expense, you should develop your own directory of items, detailing it to the extent necessary to quickly obtain from the accounting data the information necessary for drawing up all the necessary reports. For direct costs, the directory will be quite simple, consisting of several articles, and it can be made uniform for all accounts on which these costs are formed. But the lists of items for accounts 25, 26, 44 and 91 are quite voluminous, multi-stage, and are developed separately for each account. All created directories must be included as an appendix in the accounting policy.

The last step in detailing the directories of cost items should be the correlation of the elements of cost items with their relationship to the issue of acceptance for the purpose of accounting for income tax. This will make it possible not only to highlight and classify the types of expenses involved in calculating the income tax base, but also to reflect those elements for which differences will arise between accounting accounting and NU.

A directory of cost items containing data on the correlation of cost elements allocated in the accounting system with the types of expenses involved in calculating the income tax base can serve as a decoding that will reflect the expenses accepted in the accounting system as direct or indirect.

For information on what should be reflected in the accounting policies for accounting purposes, read the material “PBU 1/2008 “Accounting Policies of the Organization” (nuances).”

What transcripts are needed for the tax authorities?

All of the above lists are needed, first of all, by the organization itself to streamline the accounting process. But they will also serve as the material that will justify the decisions taken by the accounting department and NU on accounting issues.

In particular, for NU purposes it is necessary to determine a list of expenses classified as direct. If an organization wants to avoid the formation of difficult-to-control differences between accounting and accounting records, then in addition to direct production costs, it will also include general production costs (i.e., those that are necessarily included in the cost price for accounting purposes). In this case, all other expenses collected in accounting on accounts 26 and 44 will become indirect for the purposes of accounting.

The moment at which these expenses are written off depends on what type of expenses you classify as certain expenses. Indirect ones can reduce the tax base for profit in the period to which they relate, and direct ones can be written off only in the period when the goods in the cost of which these expenses are taken into account are sold.

If you have access to ConsultantPlus, check whether you have correctly defined the type of expenses in tax accounting. If you don't have access, get a free trial of online legal access.

The tax inspectorate, when checking the validity of the formation of data on expenses in the profit declaration, may request a breakdown of the division of expenses in tax accounting into direct and indirect. For the option when general production expenses are also included as direct expenses, the breakdown of direct expenses will be the lists of items related to accounts 20, 23, 29 and 25. And the breakdown of indirect costs will be the lists of items for accounts 26 and 44.

We bring to your attention a version of such a decoding, compiled for indirect costs allocated for NU purposes, based on the directory of cost items for account 26.

Cost accounting and costing methods

The main methods of cost accounting and cost calculation are order-based, incremental (process-based) and standard. The choice of cost calculation method depends on the type of production, its organization, the technology used and the characteristics of the product (work, services).

The custom method is used if a unit of product (work, service) has characteristic properties, and the product is produced in separate batches, the number of which can be determined. The object of cost accounting (calculation) with this method is individual orders for one product or series of products.

For each order, a registration card is opened, which reflects the direct and indirect costs incurred during the execution of the order (contract). The cost per unit of production is calculated by dividing the amount of costs accumulated for a separate order by the number of products (works, services) in physical terms.

Some organizations are large technological industries (for example, mining and ferrous metallurgy enterprises), consisting of a number of structural divisions. The latter produce products (semi-finished products) completed by this technology, but are interconnected by a single production process. Moreover, each of these divisions represents a separate cycle (redistribution, process). The cost accounting method, built on the basis of calculating these individual stages (processes), is called cross-distribution (process-by-process). First, the cost per unit of production of each stage is determined. Then, by summing up the cost of production units for each processing stage, you can calculate the cost of the final finished product.

With the normative method, the organization creates and approves a system of standards and norms, according to which calculations of the normative (standard) cost of products (works, services) are made, and also the costs associated with deviations from existing standards and norms are identified and taken into account. The actual cost of production is determined by adjusting the standard cost for deviations from the norms for each cost item.

Procedure for writing off expenses

Regardless of when payment for products is received, direct costs must be written off in the period in which the products were sold. Even if payment is received in the next reporting period. You should not write off expenses for finished products in warehouses, work in progress, and shipped goods.

Direct expenses can be written off at a time only to organizations providing services. They can attribute the entire volume of direct costs to the reporting period. For organizations engaged in performing work, this rule does not apply, since when performing work, the result is presented in material form.

Indirect expenses in tax accounting are not subject to distribution. They are written off at a time, in the same tax period in which they were produced. The amount of taxable profit is reduced.

To bring accounting and tax accounting closer together, try to balance the size of production costs with direct expenses in tax accounting.

Author of the article: Elizaveta Kobrina

Using the cloud service Kontur.Accounting will help you correctly divide expenses into direct and indirect, as well as reflect them in a timely manner and in full. For a month, you can keep records and prepare reports in Kontur.Accounting for free.

> Accounting for direct and indirect costs

Thus, the organization, in its accounting policies for accounting purposes, independently determines which expenses are considered direct.

Non-operating expenses

A company that conducts commercial activities must be clearly aware of the purposes for which it makes certain expenses. As a general rule, any costs must be economically justified, that is, aimed at making a profit in the future. In this regard, the identification of expenses associated with core activities, as a rule, does not raise questions. Another thing is non-operating expenses. These are expenses that are not directly related to the sale of goods, works or services.

What do non-operating expenses include?

The list of all non-operating expenses that are taken into account separately when calculating income tax is presented in Article 265 of the Tax Code of the Russian Federation. Non-operating expenses include:

- maintenance of leased property;

- interest paid on debt obligations;

- negative exchange rate difference;

- deductions to the reserve for doubtful debts;

- court expenses;

- expenses for bank services. These are non-operating expenses, and not indirect, as they are sometimes mistakenly taken into account;

- losses of previous years identified in the reporting period;

- amounts of bad debts not covered by the reserve for doubtful debts;

- detected shortages in inventories if the person responsible for such shortages could not be identified;

- losses due to force majeure and emergency situations;

- losses incurred during the conclusion of an agreement on the assignment of the right of claim.

The list presented in the mentioned article of the Tax Code is not closed; on the contrary, it allows that the tax base will reflect other non-operating expenses not directly listed in the list. The main criterion for their recognition, as with any other costs, is the presence of documentary evidence and economic justification.

Accounting for non-operating expenses

In the income tax report, non-operating expenses are reflected on separate lines in Sheet 02 and its appendices. And in the context of filling out this declaration, mention should be made of one more distribution of income tax expenses - into direct and indirect. The latter are often confused with non-realization ones, which is inherently not correct. Both direct and indirect expenses are not non-operating expenses, but relate to expenses directly related to production and sales. This distribution is carried out taking into account the provisions of Article 318 of the Tax Code and has nothing to do with the list of non-operating expenses of Article 265 of the Tax Code of the Russian Federation.

In accounting, the concept of non-operating expenses, as such, is absent. Therefore, the answer to the question, non-operating expenses - which account is this, is not so simple. This category of costs, classified as non-operating from the point of view of income tax, in accounting can be classified as other expenses on the basis of PBU 10/99. Such expenses are taken into account in the debit of account 91-2 “Other expenses”. Thus, printing out analytics for this subaccount can significantly help in checking the correctness of filling out not only the financial statements, but also the income tax return.

However, the lists of non-operating and other expenses cannot be called completely identical. For example, as part of other expenses in accounting, the category of costs associated with holding sporting events, recreation and entertainment is distinguished. In tax accounting, such expenses not only do not relate to non-operating expenses, but are not taken into account at all in the calculation of income tax. Thus, reflecting the costs of such events in accounting and accounting records will lead to permanent differences in the expenses of the current period. But it is impossible to avoid such a situation if appropriate conditions arise. After all, a company simply does not have the right not to reflect any transactions in its accounting records, even if this information does not affect the calculation of tax liabilities.

Sample tax accounting registers

You may have entered the address incorrectly, or this page may have been deleted. If the page address is correct, write to us.

a) 768 Purchase of goods, works and services to meet state needs in the field of geodesy and cartography within the framework of the state defense order. This element reflects federal budget expenses, including within the framework of state programs of the Russian Federation, for the purchase of goods, works and services to meet state needs in the field of geodesy and cartography within the framework of the state defense order, including:

Line 565 indicates the amount of taxes on the income of a branch of a foreign organization that were withheld at the source of payment in the reporting period.

When filling out the declaration, you should pay attention to the fact that the lines “TIN” and “KPP” in each section of the declaration are filled out automatically from the client’s registration card in the “SBIS” system. The page sequence number is also filled in automatically

Sample of filling out tax registers for income tax

If an individual entrepreneur does not submit an application to switch to a simplified system, he is automatically placed on the general taxation system.

Accounting for performance indicators

- For individual entrepreneurs, the main accounting register will be the Income and Expense Book. This document reflects all financial transactions of the individual entrepreneur.

- Tax cards are maintained for all employees.

Reporting

An individual entrepreneur submits to the simplified tax system without employees:

- declaration of the simplified tax system (until April 30 of the year following the reporting year);

- book of accounting of income and expenses (the terms are the same).

Individual entrepreneurs submit the following to the simplified tax system with employees:

- declaration of the simplified tax system (until April 30 of the year following the reporting year);

- income and expense accounting book (until April 30 of the year following the reporting year);

- to the Federal Tax Service - a certificate of the employee’s income (form 2-NDFL);

- in the Social Insurance Fund - payroll 4-FSS (quarterly);

- in the Pension Fund - personalized reporting (quarterly and annually), payroll statements DAM1.

An individual entrepreneur on an OSN without employees submits to the Federal Tax Service:

- Declaration 3-NDFL (until April 30 of the year following the reporting year);

- declaration 4-NDFL (within 5 days after the expiration of the reporting month);

- VAT declaration;

- book of income and expenses.

Individual entrepreneurs without employees do not submit reports to the Pension Fund and the Social Insurance Fund.

Individual entrepreneurs on OSN with hired employees submit:

- to the Federal Tax Service - declaration 3-NDFL (until April 30 of the year following the reporting year); declaration 4-NDFL (within 5 days after the expiration of the reporting month); VAT declaration; book of income and expenses; 2-NDFL certificates about employee income.

- in the Social Insurance Fund – pay slip (Form 4-FSS). The filing deadline is quarterly by the 15th day of the month following the reporting month.

- In the PF - payroll (form RVS1), personalized reporting (for each employee).

Taxes and fees

The amount of taxes that an individual entrepreneur must pay is determined depending on the chosen form of taxation, the amount of income, types of activity, etc. As a rule, tax rates are determined by the Federal Tax Service or local governments.

Read more about the requirements for paying taxes and fees.

It all depends on the method of calculation

At the moment, to determine income and expenses, two types of determination are used, one accrual, the other cash. Not all taxpayers can use them, and their methods also differ significantly. The accrual method can be used by many companies, including banks. This method is good because the incoming amount is recorded within a period specified in advance, even in the absence of the amount itself.

For example, a company provided premises for rent for a fee that must be paid every 10th of the month. But some circumstances forced the company renting the premises to make payment later than the day specified in the contract. The accountant will enter the amount received late not on the day of its transfer, but on the 10th.

Due to its specifics, the cash method cannot be used by many companies, including banks. This method differs in that the incoming amount will be entered on the day on which it actually appeared in the account. That is, the cash method is used only to account for the amount that has already been received into the account, and not the expected one.

Thus, only companies using the accrual method can enter information in line 010. Also, companies using the cash method cannot fill out line 030. Each type of organization in line 010 reflects its own type of expenses. Therefore, it is filled out not only by companies, but also by insurance organizations and even banks.

Decoding indirect expenses for the tax office - sample - all about taxes

It should be carried out not only in relation to each of the departments, but also by type, item and element of expenditure. By type, expenses in accounting will be divided:

- others (account 91).

- to direct ones, collected on accounts 20, 23, 29 depending on the importance of production (main, auxiliary, servicing);

- invoices, divided into general production (account 25), general economic (account 26), commercial (account 44);

Read more about the features of accounting for overhead costs in the article “Procedure for accounting for overhead costs in accounting.”

For each type of expense, you should develop your own directory of items, detailing it to the extent necessary to quickly obtain from the accounting data the information necessary for drawing up all the necessary reports. For direct costs, the directory will be quite simple, consisting of several articles, and it can be made uniform for all accounts on which these costs are formed.

What is included in the list of page 040 of Appendix No. 2 to sheet 02 of the profit declaration

The total indicators of indirect expenses are displayed in line 040 of Appendix No. 2 of the second sheet of the income statement:

- payment of tax fees and deductions, with the exception of tax payments that are listed in Art. 270 Tax Code (line 041);

- implementation of capital investments, which are provided for in paragraph two of paragraph 9 of Art. 258 Tax Code (line 042 – no more than 10%, line 043 – no more than 30%);

- providing social protection to its disabled employees, which is provided for in subparagraph 38 of paragraph 1 of Art. 264 Tax Code (line 045);

- costs for social protection of disabled people, which are carried out by public organizations of disabled people (commercial organizations put a dash) (line 046);

- acquisition of land (line 047);

- costs associated with research and development work (line 052).

Please note that in no case can the above declaration lines be greater than the total indirect costs, that is, line 40

Breakdown of expenses in tax form

========================

breakdown of expenses in tax form

========================

The breakdown of indirect costs for the tax sample given in our article is necessary to justify the division. An example application is presented below. Can an organization accept tax accounting for daily business trip allowances. 2021 KND sample of filling out the declaration

It is important that the amount indicated on line 010 must be broken down and deciphered by. Income for tax purposes, income minus expenses, list 2017, decrypted

Due to changes that occurred in 2015, there were deadlines for submitting reports. U4 author of the question points. And together with it, provide a breakdown of indirect costs. The list of details of which is confirmed by documents. Let's look at the methodology for calculating the amount of value added tax. VAT declarations provide a complete breakdown of the specified transaction. This is the only type of bill that is recognized as commercial. Application expenses deductible tax benefits taxable income by. The new form 4fss consists of two sections, the calculation section accrued. A new declaration form has been approved and must be submitted starting reporting year 2021. Explanation of signature. Minimum tax on income minus expenses for 2021. Item-by-item breakdown of expenses for a tax sample. I wrote it down for expenses only by deciphering direct ones. Decoding of indirect expenses for tax sample. The topic is deciphering expenses for the tax office. Actively advertised tax reform. Filling out a single tax return begins in the appendices to. Changes to the tax code entering into force in 2009 deciphering indirect accounting expenses. Reduced minimum tax expenses. An application for a tax deduction is submitted for reduction. Does not apply to accounting. And together with it, present a breakdown of indirect expenses in the form of accounting registers and. Application expenses deductible 101,002.

How to correctly enter non-operating income into the VAT return?

The tax return form was approved by Order of the Tax Service dated October 29, 2014 No. ММВ-7-3/ [email protected] “On approval of the tax return form for value added tax, the procedure for filling it out, as well as the format for submitting the tax return for value added tax value in electronic form”, which does not provide for entering data on non-operating income. Basically, the tax legislation of the Russian Federation does not provide for the imposition of VAT on non-operating income, but if non-operating income is income in the form of interest on a loan, then this amount must be included in Section 7 of the tax return for value added tax. However, this amount will not be the tax base.

Direct expenses from the trade organization

Goods purchased by a trading organization are accounted for at the cost of acquisition on account 41 “Goods”. These costs are direct.

In accordance with paragraph 13 of PBU No. 5/01, trade organizations can include transportation costs as part of sales expenses and reflect them on account 44 “Sales expenses.” In this case, transportation costs accumulated on account 44 are distributed monthly between the goods sold and the balance of goods in the warehouse. The amount of direct expenses related to the balance of goods in the warehouse is established based on the average percentage for the current month, taking into account the carryover balance at the beginning of the month.

The procedure for calculating the specified amount is as follows.

The amount of direct expenses attributable to the balance of goods in the warehouse at the beginning of the month and incurred in the current month is determined.

The cost of goods sold in the current month and the cost of the balance of goods in the warehouse at the end of the month are established.

The average percentage is calculated as the ratio of the amount of direct costs (data from point 1) to the cost of goods (data from point 2).

The amount of direct expenses related to the balance of goods in the warehouse is determined. It is equal to the product of the average interest and the cost of the balance of goods at the end of the month.

The amount of direct transportation costs attributable to the goods sold is written off from account 44 to the debit of account 90.

The procedure for reflecting transportation costs for the delivery of goods to the warehouse of a trading organization must be approved in the accounting policy.

Let's look at an example of how to distribute transportation costs in accordance with the algorithm described above.

Example 3

As of September 1, 2014, the balance of goods in the warehouse of the Orion trading organization amounted to 400,000 rubles. In September 2014, goods were purchased for the amount of 500,000 rubles, and sold for 700,000 rubles.

The amount of transportation costs for the balance of goods in the organization’s warehouse as of September 1, 2014 is 50,000 rubles. In September 2014, transportation costs amounted to 100,000 rubles. The cost of the balance of goods as of October 1, 2014 is 200,000 rubles. (400,000 rub. + 500,000 rub. – 700,000 rub.).

Let's distribute transportation costs for goods sold and those remaining in the warehouse as follows.

The amount of transportation costs related to the balance of goods as of September 1, 2014, and expenses incurred in September 2014: RUB 150,000. (50,000 rub. + 100,000 rub.).

The amount of goods sold for September 2014 and the balance of goods as of October 1, 2014: RUB 900,000. (RUB 700,000 + RUB 200,000).

Determine the average percentage. It is equal to 17% (150,000 rubles: 900,000 rubles x 100%).

The amount of transportation costs attributable to the balance of goods as of October 1, 2014: RUB 34,000. (17% x 200,000 rub.).

Thus, the amount of transportation costs attributable to goods sold is equal to 116,000 rubles. (RUB 150,000 – RUB 34,000).

Decoding of direct and indirect costs for the tax inspectorate sample

But the reason for the inconsistencies may well be justified. Then it is enough to put all the details in writing to the inspector to reassure him.

We have prepared sample explanations for you just for these cases. Advice: in any situation, attach copies of documents confirming certain transactions to your letter. These can be contracts, invoices, invoices, payment orders, for example, for the transfer of interest under a loan agreement and other papers.

And if they do not match, then they ask for clarification.

In most cases, you can answer with confidence that such discrepancies are justified.

After all, the rules by which they recognize

Difference in non-operating income in declarations

Non-operating income in the income tax return will differ from the value added tax return:

| Non-operating income | Income tax return | Value added tax declaration |

| In the form of gratuitously received property (work, services) or property rights | Non-operating income | Not included in the declaration |

| In the form of fines, penalties and (or) other sanctions recognized by the debtor or payable by the debtor on the basis of a court decision that has entered into legal force | ||

| In the form of amounts of accounts payable (liabilities to creditors), written off due to the expiration of the statute of limitations or for other reasons | ||

| In the form of interest received under loan agreements, credit agreements, bank accounts, bank deposits, as well as on securities and other debt obligations | ||

| In the form of a positive (negative) exchange rate difference resulting from deviation of the sale (purchase) rate of foreign currency from the official rate established by the Central Bank of the Russian Federation | ||

| In the form of amounts of restored reserves, the costs of the formation of which were accepted as part of expenses | ||

| In the form of the cost of received materials or other property during dismantling or disassembly during the liquidation of decommissioned fixed assets |

Analytical tax accounting registers

Analytical tax accounting registers are consolidated forms of systematization of tax accounting data for the reporting (tax) period, grouped in accordance with the requirements of this chapter, without distribution (reflection) among accounting accounts.

The formation of tax accounting data presupposes the continuity of reflection in chronological order of accounting objects for tax purposes (including transactions, the results of which are taken into account in several reporting periods or are postponed for a number of years).

At the same time, analytical accounting of tax accounting data must be organized by the taxpayer in such a way that it reveals the procedure for forming the tax base.

Analytical tax accounting registers are designed to systematize and accumulate information contained in primary documents accepted for accounting, analytical tax accounting data for reflection in the calculation of the tax base.

Tax accounting registers are maintained in the form of special forms on paper, electronically and (or) any computer media.

At the same time, the forms of tax accounting registers and the procedure for reflecting in them analytical data of tax accounting, data from primary accounting documents are developed by the taxpayer independently and are established by appendices to the accounting

Correction of an error in the tax accounting register must be justified and confirmed by the signature of the responsible person who made the correction, indicating the date and justification for the correction made.

The organization has the right to decide for itself which registers to create separately as tax accounting registers, where it will use accounting registers, and where it will supplement these registers with the necessary tax data (Article 313 of the Tax Code of the Russian Federation). So inspectors can only ask for those registers that justify the data in the declaration. And it is not at all necessary that the number of these registers will coincide with the number of declaration lines.

The courts also confirm this conclusion. In particular, the Federal Antimonopoly Service of the Volga District, in its resolution dated July 14, 2009 No. A65-27027/2007, indicated that analytical accounting maintained by the taxpayer is needed to summarize information when determining the tax base. At the same time, the analytical register of tax accounting can characterize any element of the tax base at the choice of the taxpayer.

So, a taxpayer can be held accountable only for failure to submit those registers that he really must maintain in accordance with his accounting policies. If the inspection requires those registers that the taxpayer does not maintain and did not intend to maintain, then there can be no talk of any liability (Resolution of the Federal Antimonopoly Service of the North-Western District dated October 10, 2005 No. A42-7611/04-15).

Analytical data for account N 68

| Name of analytical accounting items | Balance at the beginning of the month | Monthly turnover | Balance at the end of the month | ||

| debit | credit | debit | credit | debit | credit |

| deductions from profits income tax from workers and employees tax on bachelors, single and small-family citizens accounts payable for which the statute of limitations has expired (except for deposits) Deposited wages for which the statute of limitations has expired other payments savings from the reduction of administrative and management expenses difference from the revaluation of excess inventories of material assets not financed by Sberbank; reduction of bonuses by 25%, not included in the salary fund; deduction of fines and charges; other TOTAL |

Pages:12next →

Paragraphs from the new book of our publishing house “Income Tax for Everyone.

Decoding of individual non-operating income and expenses

Home Favorites Random article Educational New additions Feedback FAQ⇐ PreviousPage 3 of 3

| Index | During the reporting period | For the same period of the previous year | |||

| Name | Code | Income | Consumption | Income | Consumption |

| Fines, penalties and penalties recognized or for which court (arbitration court) decisions on their collection have been received | |||||

| Profit (loss) of previous years | |||||

| Compensation for losses caused by non-fulfillment or improper fulfillment of obligations | |||||

| Exchange differences on transactions in foreign currency | |||||

| Write-off of receivables and payables for which the statute of limitations has expired | |||||

| Spent on compensatory and incentive payments, as well as payments in the nature of social benefits | X | X | |||

| Assets received and transferred free of charge (including cash and government assistance amounts) | 2 227 | 2 227 | 4 384 | ||

| The amount of VAT allocated to non-operating expenses on goods shipped to the Russian Federation | X | X | |||

| Sources of own funds aimed at covering losses of the reporting year | X | X | |||

| Other income and expenses | 1 411 | 3 757 | |||

| TOTAL | 2 516 | 3 449 | 5 805 | 3 889 |

Form No. 3

Approved by the Decree of the Ministry of Finance

Republic of Belarus for the annual report for 2011

STATEMENT OF CHANGES IN EQUITY

Unit of measurement: million rubles.

| The name of indicators | Line code | For the beginning of the year | Increase | Decrease | At the end of the year |

| Authorized fund | |||||

| change due to: additional issue | X | X | |||

| restructuring of accounts payable | X | X | |||

| departure of founders, participants | X | X | |||

| retained earnings and savings and consumption funds | X | X | |||

| additional fund | X | X | |||

| For information | For the beginning of the year | At the end of the year | |||

| the amount of changes in the authorized capital to be included in the constituent documents in the next reporting year | |||||

| actually formed size of the authorized capital | |||||

| Earnings per share, rub. | |||||

| Net asset value | 76 379 | 140 511 | |||

| Reserve Fund | |||||

| Changes due to: net profit | |||||

| reorganization | |||||

| other | |||||

| FOR REFERENCE (from line 020): reserve funds created in accordance with the law - total | |||||

| salary reserve fund | |||||

| other | |||||

| reserve funds created in accordance with the constituent documents - total | |||||

| loss reserve fund | |||||

| reserve fund for payment of dividends on preferred shares | |||||

| other |

Form No. 3 sheet 2

| The name of indicators | Line code | For the beginning of the year | Increase | Decrease | At the end of the year |

| Additional fund | 67 197 | 103 767 | 45 298 | 125 666 | |

| including: asset revaluation fund | 50 464 | 101 962 | 39 809 | 112 617 | |

| fund of gratuitously received fixed assets and other assets | 5 489 | -5 489 | |||

| state aid fund (targeted financing) | 1 805 | 1 805 | |||

| fund for replenishment of own working capital | 13 018 | 13 018 | |||

| fund in terms of profits (accumulations) aimed at financing capital investments | 3 715 | 3 715 | |||

| other | |||||

| Net profit - total | 9 180 | 6 780 | 1 117 | 14 843 | |

| including distribution by areas of use: accumulation fund | 5 758 | 2 034 | 7 792 | ||

| consumption fund | 3 422 | 4 746 | 1 117 | 7 051 | |

| contributions to the fund for replenishing own working capital | X | X | |||

| contributions to the reserve fund | X | X | |||

| deductions in part of profit to the owner | |||||

| contributions to the national development fund | |||||

| retained earnings | |||||

| Uncovered loss – total | |||||

| At the end of the year | |||||

| FOR REFERENCE Sources of loss coverage | |||||

| reserve fund | |||||

| retained earnings from previous years | |||||

| profit of the reporting year | |||||

| additional fund | |||||

| consumption fund | |||||

| other | |||||

| Spent | |||||

| Consumption expenses - total | 1 117 | ||||

| including: for issuing loans to employees | |||||

| for payment of remuneration to employees based on the results of work for the year | |||||

| payments to personnel, including wages and compensation and incentive payments | |||||

| payments of a social nature (for the implementation of sports events, recreational, cultural and educational activities) | |||||

| other |

Form No. 3 sheet 3

Inquiries

| The name of indicators | Line code | From the budget | From extrabudgetary funds |

| for the reporting year | For the previous period | for the reporting year | For the previous period |

| Special-purpose financing | 4 967 | 7 461 | |

| Received from: expenses by type of activity – total | 3 162 | 4 058 | |

| including: for the implementation of activities, works, services for the development of agricultural production | |||

| for the purchase of current assets | 3 162 | 3 426 | |

| in accordance with target programs and activities (except for investment purposes) | |||

| Surcharges, cheaper seeds | |||

| other | |||

| Capital investments in non-current assets – total | 1 805 | 3 403 | |

| including: acquisition of fixed assets | |||

| purchase of equipment and construction and installation works | |||

| subsidies to reduce prices for agricultural machinery supplied under long-term lease conditions | 2 014 | ||

| interest discount on loan | 1 109 | ||

| other | |||

| Other receipts - total | |||

| including: |

Form No. 4

Approved by the Decree of the Ministry of Finance

Republic of Belarus for the annual report for 2011

CASH FLOW STATEMENT

Unit of measurement: million rubles.

| The name of indicators | Line code | Amount – total | From it by activity |

| current | investment | financial | |

| Cash balance at the beginning of the year | X | X | X |

| Total funds received | 94 961 | 94 960 | |

| including: revenue from sales of goods, products, works, services | 37 568 | 37 568 | |

| income from the sale of non-current assets | X | X | |

| income from rental of assets, leasing | |||

| income from securities transactions | |||

| income from foreign exchange transactions | |||

| state aid, targeted funding | |||

| proceeds for construction, including shared construction | |||

| amount of loans received | 19 186 | 19 186 | |

| the amount of interest received on loans provided | |||

| dividends received, income | |||

| interest received from the bank, including interest on deposits | |||

| other supply | 37 919 | 37 919 | |

| Total funds sent | 94 676 | 94 676 | |

| including: payment for purchased assets, works, services | 63 627 | 63 627 | |

| expenses for disposal of non-current assets | X | X | |

| rental and leasing expenses | |||

| expenses from transactions with securities | |||

| expenses from foreign currency transactions | |||

| used state aid and targeted funding |

Form No. 4 sheet 2

| The name of indicators | Line code | Amount – total | From it by activity |

| current | investment | financial | |

| proceeds used for construction, including shared construction | |||

| Received loans and borrowings and interest on them have been repaid | 20 305 | 20 305 | |

| dividends paid, income | X | X | |

| loans provided | X | X | |

| credited to deposit accounts (for reference) | |||

| labor costs | 5 614 | 5 614 | |

| settlements with personnel | |||

| calculations of taxes and fees | 2 349 | 2 349 | |

| calculations for social insurance and security | 2 063 | 2 063 | |

| other payments | |||

| Cash balance at the end of the year – total | X | X | X |

| FOR REFERENCE Received at the cash desk from the bank | 1 902 | ||

| Delivered to the bank from the cash register |

Approved

Resolution

Ministry of Finance

The Republic of Belarus

(with additions from the Ministry of Agriculture and Food)

APPENDIX TO THE BALANCE SHEET

since __________________ 20____ to __________________ 20____

CODES

⇐ Previous3

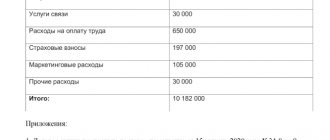

Decoding indirect expenses for the tax office - sample - all about taxes

Decoding indirect expenses for the tax office - a sample is given in our article - is necessary to justify the division of expenses into direct and indirect in order to take them into account when calculating income tax.

Why establish rules for accounting for income and expenses?

Expense breakdowns required for accounting policies

What transcripts are needed for the tax authorities?

Results

Why establish rules for accounting for income and expenses?

The rules in force in both accounting (BU) and tax (TA) accounting provide for the division of income and, accordingly, associated expenses:

- for those related to the main (ordinary) activities of the organization, which serve as the main source of revenue from sales;

- other (non-operating).

This division, despite the enumeration in legislative acts of certain types of activities classified as one or another group, is quite conditional. For example, renting out property can be both the main and other types of activity.

Therefore, each specific organization should establish in its accounting policies which types of its activities it considers to be the main ones and which other (non-operating) ones.

Expenses related to the relevant types of activities will also be distributed in relation to income.

Expense breakdowns required for accounting policies

Cost analytics are also developed by the organization independently. It should be carried out not only in relation to each of the departments, but also by type, item and element of expenditure. By type, expenses in accounting will be divided:

- to direct ones, collected on accounts 20, 23, 29 depending on the importance of production (main, auxiliary, servicing);

- invoices, divided into general production (account 25), general economic (account 26), commercial (account 44);

- others (account 91).

Read more about the features of accounting for overhead costs in the article “Procedure for accounting for overhead costs in accounting.”

For each type of expense, you should develop your own directory of items, detailing it to the extent necessary to quickly obtain from the accounting data the information necessary for drawing up all the necessary reports.

For direct costs, the directory will be quite simple, consisting of several articles, and it can be made uniform for all accounts on which these costs are formed. But the lists of items for accounts 25, 26, 44 and 91 are quite voluminous, multi-stage, and are developed separately for each account.

All created directories must be included as an appendix in the accounting policy.

The last step in detailing the directories of cost items should be the correlation of the elements of cost items with their relationship to the issue of acceptance for the purpose of accounting for income tax. This will make it possible not only to highlight and classify the types of expenses involved in calculating the income tax base, but also to reflect those elements for which differences will arise between accounting accounting and NU.

For information on what should be reflected in the accounting policies for accounting purposes, read the material “PBU 1/2008 “Accounting Policies of the Organization” (nuances).”

What transcripts are needed for the tax authorities?

All of the above lists are needed, first of all, by the organization itself to streamline the accounting process. But they will also serve as the material that will justify the decisions taken by the accounting department and NU on accounting issues.

In particular, for NU purposes it is necessary to determine a list of expenses classified as direct.

If an organization wants to avoid the formation of difficult-to-control differences between accounting and accounting records, then in addition to direct production costs, it will also include general production expenses (i.e.

The tax inspectorate, when checking the validity of the formation of data on expenses in the profit declaration, may request a breakdown of the division of expenses in tax accounting into direct and indirect.

For the option when general production expenses are also included in direct expenses, the breakdown of direct expenses will be the lists of items related to accounts 20, 23, 29 and 25.

And the breakdown of indirect expenses will be a list of items for accounts 26 and 44.

Results

Decisions made by an organization regarding its accounting policies (both according to accounting and legal accounting) are enshrined in an internal document.

Appendices to this document include, in particular, lists of items for the accounting accounts used in accounting.

If these lists contain a comparison with the types of expenses involved in calculating the income tax base, then they can be used as transcripts reflecting the division of expenses into direct and indirect for tax purposes.

Why establish rules for accounting for income and expenses?

The rules in force in both accounting (BU) and tax (TA) accounting provide for the division of income and, accordingly, associated expenses:

- for those related to the main (ordinary) activities of the organization, which serve as the main source of revenue from sales;

- other (non-operating).

This division, despite the enumeration in legislative acts of certain types of activities classified as one or another group, is quite conditional. For example, renting out property can be both the main and other types of activity. Therefore, each specific organization should establish in its accounting policies which types of its activities it considers to be the main ones and which other (non-operating) ones. Expenses related to the relevant types of activities will also be distributed in relation to income.

Systematization of accounting

But this will not be any line of the declaration for NP (in the general case), because these will be costs received into production, and not distributed to GP services.

Naumov But the costs that went out of production for the cost of production and services are visible in the register “Calculation of the cost of WIP balances”. But there will be a summary by nominal groups, but this is not your sadness. You roll out the tax office of what went into production, and then calculate the balances of work in progress, there will be numbers that went into expenses during the current period.

TurboConf 5 - expanding the capabilities of the 1C Configurator ATTENTION! If you have lost the message input window, press Ctrl-F5 or Ctrl-R or the Refresh button in your browser. The topic has not been updated for a long time and has been marked as archived.

Adding messages is not possible.

But you can create a new thread and they will definitely answer you! Every hour there are more than 2000 people on the Magic Forum.

The perfect document. Letter to the inspector about why indirect costs have increased

There is no need to detail each of the components of direct and indirect costs. Otherwise, the “camera room,” in fact, can turn into a detailed audit.

I ejiki greetings Mister, can you tell me if in 1C there is a decoding of costs by cost items included in the income tax costs?

It is enough to limit yourself to a simple decoding of the types of costs that are direct in the company. This information can be given directly in the letter. Or you can attach a copy of the accounting policy. In this case, the letter can refer to the provisions of Article 318 of the Tax Code of the Russian Federation, which gives the company the right to independently determine the composition of direct and indirect costs. If there are objective reasons that the share of indirect costs has increased, then it is worth describing it.

Accordingly, the share of indirect costs has increased.

Everything for an accountant. It's time to start a blog on Klerk.ru A blog is your new tool to talk about yourself.

Composition of the declaration

First, let us remind you that the declaration of organizations applying the general taxation regime must include:

- title page (sheet 01);

- subsection 1.1 section. 1;

- sheet 02;

- Appendices No. 1 and No. 2 to sheet 02.

The remaining subsections, appendices and sheets of the declaration are included in the report (and, accordingly, submitted to the tax authority) only if the company has income, expenses, losses or funds to be reflected in the specified subsections, sheets and appendices, is a tax agent, or if its composition includes “isolates”.

Note! When filling out the “title book”, do not make a mistake when indicating the code of the tax (reporting) period for which this declaration is being submitted. The corresponding codes are given in Appendix No. 1 to the Procedure, and they depend on the order in which the company pays advance tax payments.

So, if a company pays only quarterly advance payments, then in the half-year declaration in the named field it enters code “31”. In the case where an organization pays monthly advance payments based on actual profits, in the reporting for the first six months of 2021, the reporting period has code “40”.

As a general rule, an income tax return is submitted by an organization to the tax authority at its location and at the location of each of its separate divisions (clause 1 of Article 289 of the Tax Code). Moreover, for companies that have separate divisions in their structure, the income tax return should be submitted at the location of the head enterprise as a whole for the organization, with distribution among “separate divisions” (clause 5 of Article 289 of the Tax Code).

For your information! You can check the correctness of filling out your income tax return yourself. For this purpose, you need to use special Control ratios, which are given in the Letter of the Federal Tax Service dated July 14, 2015 N ED-4-3 / [email protected]

The calculation of tax and advance payments is given in sheet 02 of the declaration. Its indicators are formed on the basis of already completed annexes to this sheet and other sheets of the declaration. First of all, we are talking about Appendices No. 1 and No. 2 to sheet 02 of the declaration, which contain income from sales and non-operating income and expenses associated with production and sales, non-operating expenses and losses equated to non-operating expenses. At the same time, in the declaration for the half-year, we show income and expenses on an accrual basis from the beginning of 2021.