A cash book is a financial reporting document that allows you to keep records of cash flows in an enterprise, organization, institution, or individual entrepreneur. The document records the issuance and acceptance of funds.

Using a cash book, you can monitor the financial condition of an organization. It is useful not only for those checking the method of accounting at the enterprise (often this is the tax office), but also for the enterprise itself, since the amount of funds received and spent is determined.

This is a mandatory official document that exists in the organization in a single copy. It is not allowed to maintain several different cash books at the same time.

Who should lead it?

A cashier at an enterprise is a financially responsible specialist in the financial sector who manages the cash register, issues and receives material assets and securities. The cashier accepts and issues accountable money, in the case of receiving cash - salaries, financial assistance, bonuses, etc., fills out income and expense papers.

The chief accountant monitors the implementation of cash transactions and the work of the cashier. There are cases where there is no position of chief accountant in an organization, then financial control is carried out by the director (general director), the head of the enterprise.

Rules of conduct

The procedure for maintaining a cash book in an updated version has existed since 2014 in accordance with the instructions of the Central Bank. This instruction establishes a new format for carrying out cash transactions, however, the appearance of the document remains the same.

Maintaining a cash book depends on the format of its existence.

As you know, today it is possible to maintain a cash book in two versions:

- printed (filled out by hand);

- electronic (automated version).

Rules for filling out a printed cash book:

- The forms are the same for everyone and have a prescribed form. There cannot be any “special” cash book at the enterprise that would differ from that established by law. This is due to the simplification of the registration procedure for the enterprises themselves. Unification simplifies accounting and helps achieve a single and clear result.

- The cash book is drawn up every year , that is, the reporting period showing cash flow in the enterprise is equal to a calendar year.

- As for filling out, each sheet is numbered. Skipping pages is not allowed. All pages of the book are stitched together, the total number of numbered sheets is indicated at the end, the book itself is sealed with the signature of the head and the seal of the organization.

- The cashier keeps entries in duplicate in a hand-written book. This is due to the fact that one copy is an element of the cash book, and the second is an element of the report to the accounting department. Every cashier must avoid corrections, errors and any blots.

Rules for filling out the electronic cash book:

- In practice, there are minor differences between a printed manual and an e-book , but certain nuances still exist. A book issued in electronic form is printed to have a tangible appearance.

- At the end of the year, like a “handmade” book, it is signed and sealed. The cover is also printed at the end of the year.

- If the enterprise maintains an electronic cash register, quarterly registration of the cash book is allowed. Unlike the handwritten version, in which the second copy is cut along the corresponding vertical line, e-books are cut horizontally, and the second version is also a cashier's report.

- The cashier is required to make entries daily , indicating at the beginning of the working day the balance in the account, and at the end of the day, after taking into account the transactions carried out for the day, the total for the day, where he records the amount deposited in the cash register, as well as waste. Every transaction carried out during the day must be reflected in the ledger.

What is a cash book?

A cash book is a piece of paper that records the movement of money within the company's cash register. It reflects this information:

- The amount of cash that came into the cash register.

- The amount of money that was withdrawn from the device.

The recorded data must be compared with the cash limit that is approved in a particular company. If the limit is exceeded upward, the excess is sent for storage to a banking institution.

In the legislation, a cash register is understood not only as a machine itself, but as any facility where money is received and issued. This can be any place where there is a reception and disbursement of funds. That is, a cash register can be located not only at an enterprise, but also in any entity. The main feature of a cash register is the movement of funds. By movement we mean these operations:

- Issuance of salary.

- Provision and return of travel allowances.

- Provision and return of money on account.

Receiving money from customers in a store or service center is also a movement of funds. The use of the cash register must be accompanied by the maintenance of a cash register. When maintaining it, auxiliary registers are used. In particular, these are incoming and outgoing orders. Based on these papers, entries are made in the CC. The book records information about documentation. For example, these could be the following documents: gasoline coupons, employee meals, vouchers.

Only legal entities are required to maintain QC. Individual entrepreneurs are exempt from this obligation even if they carry out monetary transactions. Accordingly, individual entrepreneurs should also not follow the cash limit. Legal entities that are small enterprises may not pay attention to the cash register limit. But they are required to maintain QC.

IMPORTANT! If a person is obliged to maintain a CC, but does not do so, he is subject to a fine of 40,000-50,000 rubles (based on Article 15.1 of the Code of Administrative Offenses of the Russian Federation).

FOR YOUR INFORMATION! It is recommended to appoint an employee responsible for the correct maintenance of QC.

Instructions for filling

As mentioned above, there is a prescribed form of cash book. Let's take a brief excursion into the method and form of filling out the cash book.

In order to correctly fill out the cash book, you need to know the algorithm:

- Every book starts with a cover. The cover is the face. General information is indicated on the cover, that is, the name of the enterprise or personal information of an individual entrepreneur (last name, first name and patronymic). If the book is filled out in a structural unit of the organization, then its name. Also, the title page must contain the reporting period for which the book is being opened.

- Next come the usual standard sheets of the cash book, which, in fact, reflect the transactions. Each sheet consists of two parts that are tear-off in nature. The date is indicated at the top, that is, the day for which the records are kept, as well as the sheet number. Next comes a table divided into 5 columns: document number;

- the subject (individual, enterprise, entrepreneur) from whom the amount was received or to whom the amount was issued;

- number of the corresponding account (c/s);

- income amount;

- amount of expense.

After these tables of contents, the amount at the beginning of the day (balance) is indicated, and then the table is filled in in accordance with the names of the columns.

If there are fewer transactions per day than there are lines in the table for filling in information, then the empty columns are filled in with the capital letter “Z” to avoid making additions and corrections. At the end of the table, the total amount is added, as well as the balance at the end of the day. If wages and social benefits were paid on that day, then the corresponding item in the table is filled in; if there are no such expenses, a dash is placed.

At the end, the document is signed by the cashier with a transcript of the signature and certified by the accountant with a note about receipt of the cash document in two copies.

Rules and procedure for formation on paper

The main elements of the book are the loose leaf and the cashier's report. They are exactly the same, with identical page numbers for a given business day, but the loose leaf remains in the book, and the cashier's report is attached to the orders issued during the day.

The cashier balances the funds every working day, and their balances are automatically transferred to the next day.

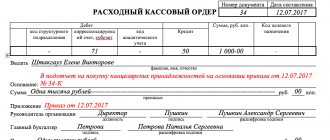

Received cash is documented with a receipt order, and cash issued is documented with an expenditure document.

These forms are assigned a serial, sequential numbering, information about them is recorded in the book.

The movement of financial assets and their records are submitted to the chief accountant for verification.

The cash book (form No. KO-4) is drawn up every calendar year, starting from the first day and ending with the last.

If there are many transactions and the pages have run out, then before the end of the reporting period the next one is drawn up, continuing the chronology of records.

Rules for maintaining a book and requirements for this procedure:

- Filling out by hand and using a computer is allowed;

- data is entered in order, without confusing the order of operations;

- the document is divided into 2 parts: the title page and the main pages of daily cash transactions;

- each sheet is presented in 2 copies: one remains in the book, the other is given to an accounting employee;

- all sheets are laced and numbered, their number is recorded on the last page;

- blots and amendments are not allowed in the document, but if correction is still necessary, then the incorrect data must be crossed out, and the correct data must be carefully entered and certified by the signature of the cashier and the chief accountant;

- can only be filled out with a ballpoint pen, without any “pencil” notes;

- carry out daily cash management, and if there is no cash flow, the sheets are not filled out;

- two books cannot be opened in one organization, the exception is if the organization has representative offices or branches, and copies of documents from the branch must be regularly sent to the parent organization.

Maintaining a cash book is also allowed electronically. The document is certified with an electronic digital signature.

The cash book is drawn up on the basis of several documents:

- a book of accounting for the issuance and acceptance of funds, showing the movement of money for the day;

- receipt and expenditure orders necessary for depositing cash into the cash register or issuing it;

- payroll issued for issuing wages to company employees;

- payroll, taking into account working hours, deductions and payment of remuneration for labor.

and a sample of filling out the KO-4 cash book can be found here.

How to sew correctly in a year - example of firmware

When starting to maintain a cash book, you should count and print the required number of sheets.

To leave room for changes, it is better to print a few additional pages.

If the identified inaccuracy does not in any way affect the cash total, then the error is crossed out and the correct inscription is written on top. The procedure for making corrections in the cash book.

If the final result changes, the incorrect page is completely canceled and the correct information is reflected on a new sheet.

Upon making amendments, a special certificate is issued. The cashier or other responsible employee indicates the changed values in it.

All pages must be numbered; continuous numbering is used. The cash book for the period is laced, stitched with thick threads, certified by the autographs of the head of the company and the chief accountant.

When stitching document sheets, special attention should be paid to the fact that sheets cannot be removed, changed, or added. The final sheet of the book contains information about the number of numbered sheets; they are written in both digital and alphabetic expressions.

Staples and other types of binding are not used, as they do not provide an absolute guarantee of the integrity of the document.

It is possible to seal the ends of the threads using a small rectangle of white paper.

Sample of a cash book, which is stitched, numbered and laced:

Shelf life

The Tax Code (Article 23) stipulates how many years tax and accounting documents are stored in an organization; the storage period is 4 years.

The Accounting Law (No. 402-FZ) determines the shelf life of the cash book - 5 years, the period must be counted from the next year.

The head of the enterprise is responsible for ensuring the safety of the cashier’s reports, the maximum storage period is 5 years.

Instructions of the Central Bank dated March 11, 2014 (No. 3210-U) exempt individual entrepreneurs from maintaining a cash book.

They are only required to create payroll and payroll statements when paying wages when making payments to employees in cash.

The abolition of this requirement for cash documentation for individual entrepreneurs does not mean that they do not need to maintain a book. How is the IP ledger maintained?

The instructions only relieve them from liability to regulatory authorities for its absence.

If it is convenient for an entrepreneur to keep records using a cash book, then this is his right.

The general rules for conducting cash transactions for organizations (except for individual entrepreneurs and small businesses) state the need to establish a cash limit.

If the organization has designated a cash register limit, then you can safely store funds in the cash register only within the stated limits.

At the end of each working day, the cashier cannot have more than the limit at his disposal. Excess funds must be handed over to a credit institution.

If there is a delay in the transfer of cash, and this fact is discovered by the regulatory authorities, then the enterprise faces a fine of 40 to 50 thousand rubles, and officials - from 4 to 5 thousand rubles (Article 2.4, 15.1 of the Code of Administrative Offenses of the Russian Federation).

The exception is the days of issuing wages to employees, benefits or scholarships. Funds are allowed to be kept in the cash register for these purposes for 5 days.

But if one of the staff has not received the money, then opposite his full name is written “deposited”, and the excess funds should be taken to the bank.

Corrections

Typos, typos, corrections, cross-outs and other errors are never welcome. But we are all human and sometimes we make our mistakes. Of course, this is not critical, but it is better to pay close attention to filling out the cash book. Any corrections are considered a violation, in connection with which you can receive a reprimand or incur some kind of punishment.

There are two types of mistakes that can be made:

- Not related to the amount reflected in the document and not affecting the outcome. This problem is solved by crossing out the incorrectly specified element and writing the correct option above it. The specified error is certified by the signature of the cashier preparing the report, as well as the checking accountant.

- Related to incorrect indication of the balance amount. This option is more global in nature. In case of such errors, the sheet completely filled out by the cashier is crossed out, the mark “canceled” is indicated, and a new sheet is filled out. Since the cashier is responsible for incorrectly indicating this data, he draws up a memo (report) addressed to the accountant stating that he discovered an error of this nature. This report is reviewed by the established commission, which is responsible for making any corrections or adjustments. After this, the cashier makes the above corrections and, as a result, draws up a certificate of the changes made.

If mistakes are made

It is easier to correct inaccuracies in an electronic book, if it has not yet been submitted as a report; to do this, it is enough to erase the incorrect data and enter new ones. But this can be done strictly until the KO-4 form is certified with an electronic signature, so before you put it, you need to check all the data accurately again.

Things are more complicated with a book that is filled out manually. It is undesirable to make mistakes in it. But we are all human and no one is immune from typos, inaccuracies and other flaws when filling out documents. So, what to do if the error does appear? It turns out that there is a whole procedure for correcting it.

To do this, first of all, you need to draw up a report to the chief accountant or boss. Secondly, appoint a commission to monitor changes. Next, you will have to withdraw the incorrect order and issue a new one. After this, in fact, you can make changes to the cash book itself. You can use special method for correction (its procedure is prescribed by law) - carefully cross out the incorrect number or text. Please provide the correct information at the top and confirm it with the signature of the chief accountant and cashier. Next to the signatures write: “Corrected” and put the date.

Next, an accounting certificate-report is drawn up on the reasons for the corrections and the essence of the error, and data about the corrections is also indicated. The certificate is certified by the manager and the chief accountant.

How to stitch

The year-end book should be numbered and bound:

- the book is stitched with special threads so that the ends of the thread after tying are on the back of the book;

- a special paper is glued to the knot formed by the thread, on which the number of stitched and numbered sheets is indicated;

- such firmware is certified by the seal of the organization, individual entrepreneur, and signed by the manager.

Features of the cash book for individual entrepreneurs and LLCs

For individual entrepreneurs there is no obligation to maintain a cash book. But at the same time, entrepreneurs must still keep records of income in it. However, if an entrepreneur already keeps or wants to keep a cash book, no one limits him, this is his right.

If an individual entrepreneur keeps a cash book, then the nuances of filling out will concern only the internal sheets. Thus, in the plate indicated on the sheets of the book, the column indicating the corresponding account is not filled in, unlike in organizations. Entrepreneurs do not indicate a cash balance limit.

It is also noteworthy that individual entrepreneurs do not issue so-called consumables - cash orders.

As for limited liability companies, the procedure is also slightly simplified; the following is not specified:

- correspondent account;

- there is no column defined as “sub-account”;

- analyst codes;

- special purpose.

However, the cash limit is still indicated.

The procedure for storing cash books at the enterprise

Directive of the Bank of Russia N 3210-U dated March 11, 2014 provides the rules for maintaining cash accounting. However, many issues, including the procedure for maintaining and storing cash documentation and cash books, rest with the immediate manager of the company. In this case, management decisions should be formalized in some kind of summary document. This may include a provision for keeping records of cash transactions. It is necessary to specify in what form cash transactions will be recorded, that is, if company employees are required to maintain paper document flow, then the regulation states that the cash book will be kept by hand or using information technology, but at the same time it must must have a physical form - be located on paper. When management has chosen the electronic version of the documentation, it is necessary to indicate in the provision that there is no need to print a paper version of the document, and the certification of the KO-4 form will take place using electronic digital signatures. The place and period of storage of the cash book are also indicated here, and in the case of storing the cash book in electronic form, it is necessary to ensure that the number of persons who have the ability to view and change such information is properly limited, as well as to protect such information resources from unauthorized access.

Important ! When maintaining document flow at an enterprise in a specialized information system, the regulations on recording cash transactions in the organization should specify in detail the places of storage and backup of documentation, the list of persons who are allowed access to this information. You should also indicate the procedure for canceling accounts and changing passwords.

Also, with any option for maintaining cash accounting, an official should be appointed who will be responsible for the safety of information, as well as penalties for non-compliance with established rules and requirements.