If the company received a fixed asset, then in order to calculate depreciation, it is necessary to establish a service life for it.

This must be done for accounting purposes, and if the asset is recognized as depreciable in tax accounting, then for tax purposes.

A correctly established SPI will allow you to calculate depreciation and transfer funds invested in fixed assets to expenses, correctly forming the tax base for income and property taxes by the organization.

Concept

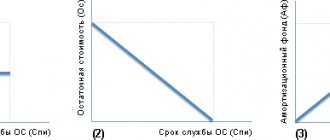

Useful life is the period of time during which an asset operates in accordance with its intended purpose with the required output.

It is generally accepted that at the end of this period, the property is physically worn out and must be removed from the balance sheet and disposed of. However, options for extending the joint investment project are possible in the case of technical re-equipment, improvements, modernization, and reconstruction.

The deadline is established both in accounting and tax. Moreover, the rules for determining it are different: for accounting they are established by clause 20 of PBU 6/01, for tax accounting – by Article 258 of the Tax Code of the Russian Federation.

The useful life period allows you to clarify the time during which the cost of an asset should be written off as expenses through depreciation.

The depreciation process continues throughout the entire period; it can only be suspended for the duration of long-term modernization or conservation for a period of more than one year.

The longer a fixed asset retains its performance qualities and characteristics, the longer its useful life and the longer the depreciation process.

SPI is established only for those assets that are recognized as depreciable fixed assets.

The latter concept includes assets that are intended for long-term use for the purpose of obtaining economic benefit.

Scope of application – production, management, trade. The property must not be resold.

The rule about the cost of the OS must also be followed - not less than the established limit.

In accounting, this is an amount within 40,000 rubles, which the company sets independently. In tax accounting it is 100,000 rubles.

In general, the rules for classifying property as fixed assets are prescribed in clause 4 of PBU 6/01 and Article 257 of the Tax Code of the Russian Federation.

Examples of determining useful life for:

- car;

- computer equipment;

- office furniture;

- buildings.

6 (117). In August 1976, the organization took into account the canteen building, the useful life of which upon commissioning is 83.3 years. For this fixed asset item, the linear depreciation method is used. As of January 1, 2015, the remaining useful life of the building was 45.8 years.

In 2015, depreciation was accrued only for the part of the dining room area not used in business activities (61% of the total area of the building).

How to determine the remaining useful life of the cafeteria building as of January 1, 2021?

Taking into account its extension for the period of non-accrual of depreciation, regardless of the percentage of use of the object in business activities.

As is known, organizations were given the right to temporarily not charge depreciation in the period from January 1 to December 31, 2015 for all fixed assets and intangible assets used in business activities.

In addition, the need was established to extend the standard service life and useful life for the period during which depreciation on these objects was not accrued (clause 2 of Resolution of the Council of Ministers of the Republic of Belarus dated February 16, 2015 No. 102; hereinafter referred to as Resolution No. 102) |*|.

* Information on the extension of standard service life and useful life of objects in 2021 is available for subscribers of the electronic “GB”

When resuming the calculation of depreciation from January 1, 2021, it is necessary to take into account the norms of Resolution No. 102 and the general procedure for calculating depreciation established by Instruction No. 37/18/6*.

______________________

* Instructions on the procedure for calculating depreciation of fixed assets and intangible assets, approved by Resolution of the Ministry of Economy, the Ministry of Finance and the Ministry of Construction and Architecture of the Republic of Belarus dated February 27, 2009 No. 37/18/6 (hereinafter referred to as Instruction No. 37/18/6).

Thus, the objects of depreciation are the fixed assets listed in the accounting records (except for those listed in off-balance sheet accounts) of the organization:

– used and unused in business activities;

– provided by an organization for temporary possession and (or) use for the purpose of generating income, taken into account as profitable investments in tangible assets, incl. investment real estate (clause 11 of Instruction No. 37/18/6).

For fixed assets used simultaneously in business activities and in non-business activities, the following is provided:

– the depreciable cost of the object is subject to division in terms of the specified use, depending on the ratio of the natural indicators of this use, incl. persons served, time spent.

The specified parts of the depreciable cost are used to include (attribute) depreciation charges to expenses depending on their use in the relevant activity on the basis of subparagraph. 4.2 clause 4 and clause 5 of Instruction No. 37/18/6;

– the useful life is set equal to the standard service life (clause 8 of Instruction No. 37/18/6).

As follows from the question, the object of accounting for fixed assets is the canteen building, which is accounted for as one object.

Taking into account the partial participation of the object in business activities, for the purposes of calculating and reflecting depreciation in the accounting accounts, the depreciable cost of the object must be divided into parts. Let us take into account that the useful life is established in accordance with the legislation as a whole for the depreciable canteen building - 83.3 years and it must be equal to the standard service life.

The standard service life and useful life of the canteen building must be extended for the period during which depreciation was not accrued on it. The specified periods are extended for the period of non-accrual of depreciation, regardless of what part of the building is used in business activities, since it is a single object of accounting and the terms are established for the entire object (see Resolution No. 102).

Therefore, the period of 83.3 years is subject to extension by 1 year and will be 84.3 years.

The remaining useful life as of January 1, 2015 was 45.8 years. Accordingly, the actual service life as of January 1, 2015 is 37.5 years (83.3 – 45.8), and as of January 1, 2016 – 38.5 years.

The remaining useful life is calculated as the difference between the useful life effective on the date of change in the procedure for calculating depreciation (resumption of its calculation), taking into account possible revisions, and the actual service life of this object as of the date of changing the procedure for calculating depreciation (full years, months) (clause 67 Instructions No. 37/18/6).

In the case under consideration, the remaining useful life must be calculated based on the extended useful life and the period of actual operation of the object until depreciation is resumed (including the period in which depreciation was not accrued).

Thus, this period is 45.8 years (84.3 - 38.5).

How to set it up in tax accounting?

The Tax Code establishes clear rules for determining the useful life of depreciable property - it is necessary to assign the asset to one of the depreciation groups and select the desired SPI from the proposed range.

Depreciation groups are contained in the Classifier approved by Decree of the Government of the Russian Federation No. 1 dated January 1, 2002, as amended. dated 07/07/2016.

For each group, the types of property included in it are specified.

As soon as the organization has accepted a new or used fixed asset, it is necessary to select a suitable depreciation group using the Classifier.

Next, look at what range of years is proposed to be accepted as the useful life, and select the required duration for the asset.

Often the Classification gives the general name of the group without explanation, then you should go to OKOF and see exactly which objects are included in it.

If the required type of property is not found in the Classifier, then you can independently determine the service life, focusing on the manufacturer’s technical documentation.

If the received fixed asset was previously used, that is, it was in use, then when establishing the service life, you can take into account the time of work with the previous owners. That is, the number of months of use is subtracted from the SPI for the depreciation group, expressed in months.

The selected useful life must be converted into months; this will allow depreciation deductions to be calculated in tax accounting and correctly taken into account in taxable expenses.

Depreciation groups according to the Classifier

To determine the SPI of fixed assets in 2021, you need to use a new Classification taking into account the updated OKOF.

The classifier has 10 depreciation groups.

For each group, a time period is given within which you can choose the useful life.

In this case, the lower extreme value of the range is not included, but the uppermost value is included.

For example, if for depreciation group 2 the SPI range is set to 2 - 3 years, this means that you can select a service time from 25 to 36 months inclusive.

Other rules for establishing private investment income in tax accounting do not apply.

The exception is cases when the object is not in the OKOF.

| Group number according to the Classifier | Useful life | |

| in years (including the upper border and not including the lower border) | in months (including borders) | |

| 1 | 1 … 2 | 13 … 24 |

| 2 | 2 … 3 | 25 … 36 |

| 3 | 3 … 5 | 37 … 60 |

| 4 | 5 … 7 | 61 … 84 |

| 5 | 7 … 10 | 85 … 120 |

| 6 | 10 … 15 | 121 … 180 |

| 7 | 15 … 20 | 181 … 240 |

| 8 | 20 … 25 | 241 … 300 |

| 9 | 25 … 30 | 301 … 360 |

| 10 | From 30 | From 361 |

The organization’s task is to correctly establish the depreciation group for the fixed asset. This will allow you to correctly determine the useful life.

An incorrectly selected service period will lead to incorrect calculation of depreciation charges. Accordingly, the income tax will not be calculated correctly.

What determines the useful life period and how to set it correctly

The expected lifespan of an asset is influenced by the following factors:

- the possibility of actual use of the object in economic activity;

- the process of operating an asset is a source of income for the enterprise or creates conditions for making a profit;

- recommendations of the product manufacturer on the approximate shelf life of spare parts for the facility and equipment in general.

The useful life also depends on membership in a specific depreciation group. The unified Classifier (its provisions are fixed by Resolution No. 1 of 01.01.2002) provides for 10 such categories:

- The first group contains assets that enterprises have used for no more than 2 years.

- The second group includes objects with a planned service life in the range of 2-3 years.

- The third group combines assets used for 3-5 years.

- The fourth category provides for a term limit of 5-7 years.

- The fifth group is characterized by setting deadlines at the level of 7-10 years.

- The sixth group lists assets with a service life of 10-15 years.

- The seventh group is represented by objects that are capable of bringing material benefits to their owners for 15-20 years.

- The eighth group contains assets with a useful life of 20-25 years.

- The ninth group includes fixed assets that continue to be used for 25-30 years.

- Objects with the longest periods of use are collected in group 10 (over 30 years).

NOTE! If the new fixed asset is not listed in any of the legally established groups, then the owner is given the right to independently determine the period of operation based on information from the technical documentation. In the absence of the necessary information about the period of use of the asset in the technical passport and other documents, the enterprise can formulate a written request to the manufacturer in order to identify the temporary potential for operating the asset.

Useful life should be established not only for new assets, but also for products that were previously used by others. With the linear method of forming depreciation charges for them, the depreciation period is set according to the following algorithm:

- Identification of the depreciation group for the received asset.

- Determination of the total number of years (months) during which such an object can be operated.

- Determining the period of use of a fixed asset at a given enterprise - the period of time during which the object was actually operated by other owners is subtracted from the total number of years or months.

- When a positive value is obtained, it is taken as the basis for calculating depreciation.

- If the estimated useful life is zero or negative, the new owner of the asset sets the operating period independently, taking into account safety standards.

The peculiarity of fixed assets is that the results of depreciation calculation for tax and accounting may differ. This is due to different methodology for calculating and determining the service life. According to the accounting standards stated in PBU 6/01, the period of use is identified with reference to the following factors:

- the expected lifespan of the asset by the enterprise;

- the rate of physical and moral deterioration of fixed assets.

FOR REFERENCE! In accounting, there is no mandatory linking of depreciation calculations to the classification categories of fixed assets; for tax accounting, the influence of this classification system is fundamental.

For each of the depreciation groups of fixed assets, minimum and maximum values for the duration of operation are provided. Enterprises are given the right to independently set the service life in the proposed range. If changes are introduced to legislative norms that affect the procedure for calculating depreciation or determining the service life of assets, then business entities must adhere to the following line of behavior:

- for all objects that are put on the balance sheet and put into operation after the start date of legislative initiatives, new standards and rules are applied;

- For assets that were accepted for accounting and began to be used before the date of amendments to the legislation, the previous rules continue to apply; there is no need to revise their useful lives.

If facts of erroneous assignment of one or more objects to a specific depreciation group are identified, it is necessary to correct the error in depreciation calculations and recalculate the income tax base. In situations where such an error caused an underpayment of tax obligations, it is necessary to draw up and submit an updated declaration to the regulatory authority, without waiting for an inspection by the Federal Tax Service, and make an additional tax payment with the obligatory transfer of the amount of the penalty. In accounting, such a complex of transactions is recorded using an accounting certificate.

How to determine it in accounting?

Legislation in the field of accounting is more loyal to the establishment of SPI, giving companies the opportunity to independently choose a suitable service life, taking into account a number of requirements prescribed in clause 20 of PBU 6/01:

- expected operating time with expected returns;

- planned wear, taking into account the conditions of use of the object, influencing factors, and intensity of operation;

- provided restrictions for a specific case, for example, when choosing a private investment investment for leased property, such a restriction may be the lease term.

After analyzing these factors together, the organization can select the required period of use.

In order to minimize discrepancies between accounting and tax accounting, organizations often choose a service life equal to that established for tax purposes.

That is, according to the Classification, taking into account the appropriate depreciation group.

However, the use of the Classifier is not mandatory for organizations. It is possible to establish different SPI, but this will complicate the depreciation process for accounting and tax purposes.

Change and revision of the SPI of an OS object during operation

SPI is established by the organization for depreciable property immediately upon receipt. If the object was in operation, then the service time is reflected in the acceptance certificate, on the basis of which the asset is accepted for accounting. The specified time is subtracted from the useful life.

Changing the service life during operation of a fixed asset is possible in the case of capital investments in an object in order to improve its performance, characteristics, and capabilities.

This is only possible with modernization, reconstruction, and retrofitting. In this case, capital investments are allocated to increase the initial cost of the OS, and the service life can be revised at the discretion of the owner.

The right to review and change the useful life is enshrined in both PBU 6/01 and the Tax Code of the Russian Federation.

How much the service period will be extended is decided by the organization, based on a number of factors.

From an accounting point of view, an upward revision of SPI is possible if:

- the production capabilities of the fixed asset have improved;

- operating mode adjusted;

- The characteristics and parameters of the object have been changed for improvement.

For tax accounting in accordance with paragraph 2, paragraph 2, Article 258 of the Tax Code of the Russian Federation, a change and revision of the period is possible, but only within the range that is established for the depreciation group of the object.

The organization is not obliged to increase the SPI; this is its right, not its obligation.

In practice, the useful life is usually increased by the number of months or years that are needed to write off capital investments through depreciation.

The revision of the SPI is also carried out upon receipt of an OS previously used.

Based on the supplier’s documents for such fixed assets, the established period can be reduced by the duration of operation.

This can be done for both accounting and tax purposes.

If there are no documents confirming the service life, or the asset was accepted from an individual, then a reduction is not allowed.

Useful life of intangible assets in questions and answers

Can the useful life change during the operation of intangible assets?

Yes. The company is obliged to check accounting data for intangible assets every year and, if necessary, adjust the deadline to reflect any deviations that have arisen.

Is it necessary to check accounting data for assets with a previously undefined period?

Yes, it is necessary on a general basis.

Is it possible to revise the terms of use of intangible assets at NU?

No, the deadlines are fixed and cannot be revised.

How to determine the SPI of a company website?

In most cases, the site's PPI is not reflected in the documents. A company can set such a deadline independently, reflecting it in internal orders or local NAs. You need to be prepared for claims from the Federal Tax Service. The inspection may require recognition of the impossibility of establishing the actual SPI of the resource and use a period of 10 years for NU purposes. However, the position of the fiscal authorities is not indisputable.

How is depreciation calculated on intangible assets of non-profit organizations?

Such assets owned by non-profit organizations are not subject to depreciation.