- New BCC (budget classification codes) for 2021, table, changes

- How KBK has changed in 2021

- KBC for insurance premiums for 2021

- KBK for personal income tax for 2021 for legal entities

- KBK for income tax 2021 for legal entities

- BCC for VAT in 2021

- KBK on excise taxes in 2021

- BCC of property tax in 2021 for legal entities

- KBK transport tax in 2021 for legal entities

- KBK according to the simplified tax system for 2021

- BCC for other taxes, fees and obligatory payments for 2018

New BCC (budget classification codes) for 2021, table, changes

Incorrect BCCs in payments when transferring taxes and contributions lead to arrears.

Of course, the details in field 104 can be clarified. But this takes time. After all, you need to draw up an application and submit it to the inspectorate. Therefore, it is easier to check the BCC in advance not only in payments, but also in calculations and declarations. This article will help you fill out the BCC correctly in payment orders and reporting. It contains all KBK 2021 (budget classification codes) for 2021. Just select the desired tax and the most suitable code. We have brought all the BCCs taking into account the changes of 2018. After all, the budget classification codes have changed.

Budget classification code (BCC): table

Home / Other

The concept of budget classification code (BCC) was introduced by the Budget Code of the Russian Federation dated July 31, 1998 No. 145-FZ.

BCCs are special 20-digit digital codes that are used to group income, expenses and sources of financing of the state budget. Thus, these codes help to identify and organize the receipt and expenditure of funds.

Legal entities and individuals require these codes to fill out payment and reporting documentation when one of the parties to the relationship (recipient of payments, regulatory authority, etc.) is the state or one of its departments.

For example: BCC are indicated in some tax returns (for VAT, income tax, etc.), thus, Federal Tax Service inspectors record the debt on the taxpayer’s personal account.

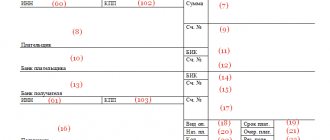

Then the taxpayer indicates the BCC corresponding to a specific tax in the payment order (field 104 is reserved for the BCC) when actually transferring this tax to the budget. When this amount is credited to the subject’s personal account, the previously recorded debt is repaid.

In this case, it is allowed to indicate only one code in one payment order. If payments relate to different BCCs, the required number of payment orders is issued.

KBK table for 2021

KBK structure

In accordance with Order of the Ministry of Finance of the Russian Federation dated 07/01/2013 No. 65n (with amendments that came into force on 01/01/2018), the structure of the code using an illustrative example (KBK, corresponding to the personal income tax paid by the tax agent, is taken as an example) is as follows:

Where,

- The first 3 digits identify the revenue administrator. In the example given, code 182 corresponds to the Federal Tax Service.

- The next 3 digits establish the income group and subgroup. In our case: 101 – taxes on profits, income.

- Values from 7 to 20 digits inclusive are determined in strict accordance with Appendix 1.1 to the List approved by the above order.

In this case, the following groups of element values can be distinguished:

- signs 7-11 contain the code of the income item and subitem. In this situation, the value corresponds to the article “Tax and non-tax income” and the subarticle “Taxes on profit, income” - “Personal income tax, the source of which is the tax agent.”

- signs 12-13 indicate which budget the income should go to. In the example given: 01 – federal budget.

- Signs 14-17 are determined by the revenue administrator for the purpose of separate accounting of incoming mandatory payments, penalties, fines and interest. In our example: 1000 is a mandatory payment.

Note: currently the Federal Tax Service groups revenues into the following groups: 1000 – mandatory payments, 2100 – penalties, 2200 – interest, 3000 – fines.

- signs 18-20 indicate what type of financial transactions this income belongs to. In this case: 110 – tax revenues.

KBK codes are approved by orders of the Ministry of Finance of the Russian Federation. Changes are made quite often, so when making payments and preparing reports, it is recommended to check the available information with the latest KBK classifier and information posted on the official websites of government departments.

Errors in KBK

When transferring budget payments, you should be careful, since an error made when filling out the BCC can lead to a situation where the funds go to the wrong destination or remain “hanging” in the category of unknown.

If we are talking about taxes or contributions, the payment will need to be clarified by submitting the appropriate application. It should be noted that in accordance with the letter of the Ministry of Finance dated January 19, 2017 No. 03-02-07/1/2145, an error in the BCC does not prevent the determination of the type of payment, therefore the tax is considered paid.

Additional difficulties may arise if the BCC is incorrectly indicated when paying the state fee. In this case, the organization or individual will be denied the provision of relevant public services, and it will most likely not be possible to return or offset the amount of the fee transferred to the budget (subclauses 1-5, clause 1, article 333.40 of the Tax Code of the Russian Federation).

Did you like the article? Share on social media networks:

- Related Posts

- Individual entrepreneur reporting in 2021

- LLC reporting in 2021

- Tax holidays for individual entrepreneurs in 2021

- Book of accounting of income and expenses (KUDiR) in 2021

- Personal income tax for employees (income tax)

- Personal income tax (NDFL)

- Fixed contributions for individual entrepreneurs in 2021

- Insurance premiums for employees in 2021

Leave a comment Cancel reply

How KBK has changed in 2021

In 2021, apply the new budget classification codes. They have changed for those companies that:

- pay income tax on income received in the form of interest on bonds of Russian organizations in rubles issued during the period from January 1, 2021 to December 31, 2021 (Order of the Ministry of Finance of Russia dated June 9, 2021 No. 87n);

- list excise taxes (Order of the Ministry of Finance of Russia dated June 6, 2021 No. 84n).

See the table below for new BCCs taking into account the changes for 2021.

New BCC 2021 for income tax (bond income)

| Tax | 182 1 0100 110 |

| Penalty | 182 1 0100 110 |

| Fine | 182 1 0100 110 |

In payment orders for the payment of excise taxes, the following codes should be entered in field 104:

- 18210302360010000110 – excise taxes on electronic nicotine delivery systems produced on the territory of the Russian Federation;

- 18210302370010000110 – excise taxes on nicotine-containing liquids produced on the territory of the Russian Federation;

- 18210302380010000110 – excise taxes on tobacco (tobacco products) intended for consumption by heating, produced on the territory of the Russian Federation.

Classification of budget revenues

The classification of budget revenues is a grouping of budget revenues of the budget system of the Russian Federation. The budget income classification code consists of twenty characters.

The structure of the twenty-digit code for the classification of budget income is uniform for the budgets of the budget system of the Russian Federation and includes the following components:

- code of the chief administrator of budget revenues (1 - 3 digits);

- code of the type of budget income (4 - 13 digits);

- budget income subtype code (14 - 20 digits).

Structure of the budget income classification code

| Main code administrator | Budget income type code | Budget income subtype code | |||||||||||||||||

| group | subgroup | article | sub-article | element | Subspecies group | Analytical group subspecies | |||||||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 |

KBC for insurance premiums for 2021

Check the BCC for insurance premiums with the tables below before sending the payment to the bank. Please note that there are no separate codes for additional pension contributions for old periods. Although the codes for other contributions are divided by year. The BCCs for these contributions are not divided into periods, since this is not necessary. All contributions for additional tariffs must be transferred to single codes.

BCC for insurance premiums for employees for 2021 (table)

| Payment type | KBK | |

| contributions for periods up to 2021 | fees for January, February, etc. in 2017-2018 | |

| Pension contributions | ||

| Contributions | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

| Contributions for temporary disability and maternity | ||

| Contributions | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

| Contributions for injuries | ||

| Contributions | 393 1 0200 160 | 393 1 0200 160 |

| Penalty | 393 1 0200 160 | 393 1 0200 160 |

| Fines | 393 1 0200 160 | 393 1 0200 160 |

| Contributions for compulsory health insurance | ||

| Contributions | 182 1 0211 160 | 182 1 0213 160 |

| Penalty | 182 1 0211 160 | 182 1 0213 160 |

| Fines | 182 1 0211 160 | 182 1 0213 160 |

KBC for insurance premiums for 2021 (table for individual entrepreneurs)

| Pension contributions | KBK for periods up to 2021 | KBC for 2017-2018 |

| Fixed contributions to the Pension Fund based on the minimum wage | 182 1 0200 160 | 182 1 0210 160 |

| Contributions at a rate of 1 percent on income over RUB 300,000. | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

| Medical fees | ||

| Contributions | 182 1 0211 160 | 182 1 0213 160 |

| Penalty | 182 1 0211 160 | 182 1 0213 160 |

| Fines | 182 1 0211 160 | 182 1 0213 160 |

KBC for insurance premiums for 2021 (table) at additional rates

| Additional pension contributions at tariff 1 | ||

| Contributions | 182 1 02 02131 06 1010 160, if the tariff does not depend on the result of the special assessment 182 1 02 02131 06 1020 160, if the tariff depends on the result of the special assessment | |

| Penalty | 182 1 02 02131 06 2100 160 | 182 1 02 02131 06 2100 160 |

| Fines | 182 1 02 02131 06 3000 160 | 182 1 02 02131 06 3000 160 |

| Additional pension contributions at tariff 2 | ||

| Contributions | 182 1 02 02132 06 1010 160, if the tariff does not depend on the result of the special assessment 182 1 02 02132 06 1020 160, if the tariff depends on the result of the special assessment | |

| Penalty | 182 1 02 02132 06 2100 160 | 182 1 02 02132 06 2100 160 |

| Fines | 182 1 02 02132 06 3000 160 | 182 1 02 02132 06 3000 160 |

The concept of KOSGU

According to budget standards, the decoding of KOSGU is a classification of operations of the general government sector. The three-digit code is part of the account classification, which allows you to group public sector costs depending on the economic content of the business transaction. The codifier includes a group, article and subarticle.

Since 2021, KOSGU codes are not used by recipients of funds when creating income and expense plans, but are used in accounting and reporting. In 2021, it is necessary to apply them to public sector institutions and organizations when drawing up a working chart of accounts, maintaining records and reporting. Order No. 209n provides a breakdown of the KOSGU for 2021 for budgetary institutions, and the procedure for approving the chart of accounts for budgetary accounting is enshrined in Order No. 162n of the Ministry of Finance (as amended on December 28, 2018).

The public administration sector operations codifier represents the following groupings:

| 100 | Income |

| 110 - tax revenues | |

| 111 - taxes | |

| 112 — state duties | |

| 130 — income from the provision of paid services | |

| 180 - other | |

| 200 | Expenses |

| 211 - salary | |

| 213 - payroll accruals | |

| 221 - communication services | |

| 222 - transport services | |

| 223 - utilities | |

| 224 – rent for the use of property | |

| 225 - works and services for property maintenance | |

| 226 - other works and services | |

| 228 - services for capital investment purposes | |

| 290 — other expenses | |

| 300 | Receipt of non-financial assets (NA) |

| 310 - increase in the cost of fixed assets | |

| 320 — increase in the value of intangible assets | |

| 330 - increase in the value of non-produced assets | |

| 340 - increase in the cost of inventories | |

| 341 - increase in the cost of medicines | |

| 400 | Retirement |

| 410 - decrease in the value of fixed assets | |

| 411 - depreciation of fixed assets | |

| 420 - decrease in the value of intangible assets | |

| 430 - decrease in the value of non-produced assets | |

| 440 - decrease in the cost of inventories | |

| 500 | Receipt of financial assets (FA) |

| 510 - receipt of cash and cash equivalents | |

| 520 — increase in the value of securities | |

| 530 - increase in share price | |

| 600 | Retirement of FA |

| 610 - cash outflow | |

| 620 — decrease in the value of securities | |

| 630 - decrease in share price | |

| 700 | Increase in liabilities |

| 710 — increase in debt on domestic borrowings | |

| 720 — increase in debt on external borrowings | |

| 730 — increase in other accounts payable | |

| 800 | Reducing liabilities |

| 810 — reduction of debt on domestic borrowings | |

| 820 — reduction of debt on external borrowings | |

| 830 - reduction of other accounts payable |

Previously, KOSGU was used in the structure of the budget classification code (BCC), but since 2015, in terms of costs, the code has been replaced by a code for types of expenses. It is important to clearly understand the difference between KBC and KOSGU. The budget classification code is 20 characters long and determines the content of the transaction. For specialists, this means that state (municipal) expenses and revenues are classified according to various criteria: planned and unplanned, current and capital, according to the level of ownership of the corresponding budget, etc. The public administration sector operations codifier (KOSGU) is used to further detail budget accounting operations.

KBK for personal income tax for 2021 for legal entities

In field 104 of the payment slip, the tax agent indicates the budget classification codes. The latest changes have not affected the BCC for personal income tax for employees in 2021. But remember that the codes are different for the tax itself, penalties and fines. The BCC for personal income tax for employees in 2021 is in the table below.

KBK for personal income tax on the income of employees, legal entities and individual entrepreneurs for 2018

| Employee income tax | 182 1 0100 110 |

| Penalties on employee income tax | 182 1 0100 110 |

| Employee income tax penalties | 182 1 0100 110 |

| Tax paid by entrepreneurs on the general system | 182 1 0100 110 |

| Penalties on the tax paid by entrepreneurs on the general system | 182 1 0100 110 |

| Tax penalties paid by entrepreneurs on the general system | 182 1 0100 110 |

Basic definitions

The budget classification of the Russian Federation is a systematized and structured grouping of expenditure and revenue transactions of all levels of budgets of the RF BS, sources of financing budget deficits and operations of public legal entities.

KBC are needed for:

- classification of completed payment transactions;

- tracking movements (movements) of funds;

- determining the amount of outstanding payments;

- facilitating the work of employees of public sector bodies.

Back in June 2021, the Russian Ministry of Finance adjusted the current procedure for applying budget classification for 2021 and the planned two-year period. Innovations in 65n “Budget classification” are enshrined in order No. 87n dated 06/09/2017.

IMPORTANT!

Instruction 65n has been cancelled! Instead, use the new one, which was approved by Order of the Ministry of Finance dated June 8, 2018 No. 132n “On approval of the Procedure for the formation and application of budget classification codes of the Russian Federation”!

KBK for income tax 2021 for legal entities

If you indicate the wrong KBK or completely forgot to write down the code, inspectors will receive a notification of refusal to accept the declaration. It will say: there was an error in filling out the data for the “Budget Classification Code” indicator. The error code is 300300027.

If you do not solve the problem and are late in submitting the report, then a fine cannot be avoided. Delay the report for more than 10 days and tax inspectors will suspend transactions on bank accounts. To avoid such troubles, check

KBK of income tax to the federal and regional budgets - 2018

| Purpose of payment | Mandatory payment | Penalty | Fine |

| to the federal budget (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| to the budgets of the constituent entities of the Russian Federation (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| to the federal budget (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| to the budgets of the constituent entities of the Russian Federation (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| when implementing production sharing agreements concluded before October 21, 2011 (before the Law of December 30, 1995 No. 225-FZ came into force) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| from the income of foreign organizations not related to activities in Russia through a permanent representative office | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| from the income of Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| from the income of foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| from dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| from interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| from the profits of controlled foreign companies | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

Classification of budget expenses

The classification of budget expenditures is a grouping of budget expenditures of the budget system of the Russian Federation and reflects the direction of budget funds for the performance by federal government bodies (state bodies), government bodies of the constituent entities of the Russian Federation, local government bodies (municipal bodies) and management bodies of state extra-budgetary funds of basic functions , solving socio-economic problems.

The budget expenditure classification code consists of twenty characters.

The structure of the twenty-digit code for the classification of budget expenditures is uniform for the budgets of the budget system of the Russian Federation and includes the following components:

- code of the main manager of budget funds (1 - 3 digits);

- section code (4 - 5 digits);

- subsection code (6 - 7 digits);

- target article code (8 - 17 digits);

- expense type code (18 - 20 digits).

Structure of the budget expenditure classification code

| Main code manager budget funds | Code section | Code subsection | Target article code | Expense type code | |||||||||||||||

| Software (non-program) article | Direction expenses | group | subgroup | element | |||||||||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 |

BCC for VAT in 2021

A company that mistakenly indicated the KBK of another tax in its payment has the right to clarify the payment. This was officially confirmed by the Federal Tax Service. For example, a profit tax code was entered in the VAT payment slip. Because of this, a debt arose for VAT, and an overpayment arose for profits.

If you submit an application to clarify the payment, then the tax authorities must correct the BCC in the budget settlement card and reset the penalties to zero (clause 7 of Article 45 of the Tax Code of the Russian Federation). But in order not to create unnecessary problems for yourself, check the KBK of value added tax for 2021 in advance using our table.

KBC for VAT transfers in 2021

| Payment Description | Mandatory payment | Penalty | Fines |

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

KBK on excise taxes in 2021

Execute payment orders for the transfer of excise tax in accordance with the Regulations of the Bank of Russia dated June 19, 2012 No. 383-P and the Rules approved by Order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n. In field 104, put KBK - we have listed them in the table below.

KBC for the transfer of excise taxes in 2021

| Purpose | Mandatory payment | Penalty | Fine |

| Excise taxes on goods produced in Russia | |||

| ethyl alcohol from food raw materials. In addition to distillates of wine, grape, fruit, cognac, Calvados, whiskey | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| ethyl alcohol from non-food raw materials | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| wine, grape, fruit, cognac, calvados, whiskey distillates | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| alcohol-containing products | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| tobacco products | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| electronic nicotine delivery systems | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| nicotine-containing liquids | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| tobacco and tobacco products intended for consumption by heating | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| automobile gasoline | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| straight-run gasoline | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| cars and motorcycles | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| diesel fuel | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| motor oils for diesel, carburetor (injection) engines | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| fruit, sparkling (champagne) and other wines, wine drinks, without rectified ethyl alcohol | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| beer | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| alcoholic products with a volume fraction of ethyl alcohol over 9 percent. Except beer, wines, wine drinks, without rectified ethyl alcohol | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| alcoholic products with a volume fraction of ethyl alcohol up to 9 percent. Except beer, wines, wine drinks, without rectified ethyl alcohol | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| cider, poiret, mead | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| benzene, paraxylene, orthoxylene | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| aviation kerosene | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| middle distillates | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| wines with a protected geographical indication, with a protected designation of origin, except for sparkling wines (champagnes) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| sparkling wines (champagnes) with a protected geographical indication, with a protected designation of origin | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise duties on goods imported from member states of the Customs Union (payment of excise duty through tax inspectorates) | |||

| ethyl alcohol from food raw materials. In addition to distillates of wine, grape, fruit, cognac, Calvados, whiskey | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| distillates – wine, grape, fruit, cognac, calvados, whiskey | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| cider, poiret, mead | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| ethyl alcohol from non-food raw materials | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| alcohol-containing products | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| tobacco products | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| electronic nicotine delivery systems | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| nicotine-containing liquids | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| tobacco and tobacco products intended for consumption by heating | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| automobile gasoline | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| cars and motorcycles | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| diesel fuel | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| motor oils for diesel, carburetor (injection) engines | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| fruit, sparkling (champagne) and other wines, wine drinks, without rectified ethyl alcohol | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| beer | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| alcoholic products with a volume fraction of ethyl alcohol over 9 percent. Except beer, wines, wine drinks, without rectified ethyl alcohol | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| alcoholic products with a volume fraction of ethyl alcohol up to 9 percent. Except beer, wines, wine drinks, without rectified ethyl alcohol | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| straight-run gasoline | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| middle distillates | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| Excise taxes on goods imported from other countries (payment of excise duty at customs) | |||

| ethyl alcohol from food raw materials. In addition to distillates of wine, grape, fruit, cognac, Calvados, whiskey | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| distillates – wine, grape, fruit, cognac, calvados, whiskey | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| cider, poiret, mead | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| ethyl alcohol from non-food raw materials | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| alcohol-containing products | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| tobacco products | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| electronic nicotine delivery systems | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| nicotine-containing liquids | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| tobacco and tobacco products intended for consumption by heating | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| automobile gasoline | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| cars and motorcycles | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| diesel fuel | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| motor oils for diesel, carburetor (injection) engines | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| fruit, sparkling (champagne) and other wines, wine drinks, without rectified ethyl alcohol | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| beer | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| alcoholic products with a volume fraction of ethyl alcohol over 9 percent. Except beer, wines, wine drinks, without rectified ethyl alcohol | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| alcoholic products with a volume fraction of ethyl alcohol up to 9 percent. Except beer, wines, wine drinks, without rectified ethyl alcohol | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| straight-run gasoline | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| middle distillates | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

BCC of property tax in 2021 for legal entities

In 2021, pay corporate property tax to the budget according to the BCCs that we have given in the table below. Enter the budget classification code in field 104 of the payment order.

BCC of property tax for legal entities in 2021 (table)

| Purpose of payment | Mandatory payment | Penalty | Fine |

| for property not included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| for property included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

Codes for budgetary and autonomous institutions

A distinctive feature for budgetary and autonomous institutions is the simplified procedure for generating the code. That is, from 1 to 17 characters of the twenty-digit code, zero values are set. And from 18 to 20 signs - KVR - type of flow.

For example, the contractor must determine a code for purchasing a car for major repairs. Here's how to find out the BCC of government procurement for an organization:

- Open Part 3 of Appendix No. 9 of Order No. 207n.

- Check all groups. The code for the type of expense “major repairs” is assigned to group KBK 243 “Purchase of goods, works, services for the purpose of major repairs of state (municipal) property.”

- Create a code to pay for major car repairs - 000 0000 00000 00000 243.

For other orders, the decoding KBK 244 is used - other procurement of goods, works and services. According to the coding of types of expenses, household and office supplies, fuels and lubricants, building materials (current repairs), food products, inventories, and fixed assets are purchased.

And here is a sample budget classification code when paying for parental fees to an autonomous institution - 000000000000000000130 (clause 12.1.3 of Order 85n dated 06/06/2019).

KBK transport tax in 2021 for legal entities

In field 104 of the payment order, provide special budget classification codes when you transfer the transport tax. All BCCs for transport tax in 2021 are in the table below.

KBK – transport tax 2021 for individuals and legal entities

| Purpose of payment | Mandatory payment | Penalty | Fine |

| from organizations | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| from individuals | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

Structure of the KBK

This code consists of 20 characters - numbers, separated by hyphens into groups, it has the following form XX - X XX XX XXX XX - XXXX - XXX.

Each group of characters corresponds to an encrypted meaning determined by the Ministry of Finance. Let's consider the structure of the profitable BCC, since they are the ones that entrepreneurs mainly have to use (expense codes can be found mainly when returning funds under any government program).

1. "Administrator". The first three signs show who will receive the funds and is responsible for replenishing this or that part of the budget with them, and manages the received money. The most common codes for businessmen begin with 182 - tax authority, 392 - Pension Fund, 393 - Social Insurance Fund and others.

2. “Type of income” includes characters from 4 to 13. This group of characters helps to quite accurately identify income according to the following indicators:

- group – 4th character (that is, the first in this paragraph);

- subgroup – 5th and 6th characters; a two-digit code indicates a specific tax, duty, contribution, fine, etc.;

- article – category 7 and 8 (the value of the purpose of the received income is encoded in the settlement documents for the budget of the Russian Federation);

- subarticle – 9, 10 and 11 characters (specifies the item of income);

- element - 12 and 13 digits, characterizes the budget level - from federal 01, municipal 05 to specific budgets of the Pension Fund - 06, Social Insurance Fund - 07, etc. Code 10 indicates the settlement budget.

3. “Program” – positions 14 to 17. These numbers are designed to differentiate taxes (their code is 1000) from penalties, interest (2000), penalties (3000) and other payments (4000).

4. “Economic classification” – last three digits. They identify revenues in terms of their economic type. For example, 110 speaks of tax revenues, 130 - from the provision of services, 140 - funds forcibly seized, etc.

IMPORTANT TO KNOW! The 20-digit code must be entered correctly and without errors in the “Purpose of payment” field (field No. 104) of the payment order. In fact, it duplicates the information indicated in the “Base of payment” field, as well as partially in the “Recipient” and “Recipient’s current account” fields.

KBK according to the simplified tax system for 2021

The minimum tax on the simplified tax system with the object “income minus expenses” no longer has a separate budget classification code. It must be paid according to the KBK regular tax. This is what the Russian Ministry of Finance decided (order No. 90n dated June 20, 2021).

BCCs under the simplified tax system vary depending on the object of taxation. For the object “income” there are some codes, for the object “income minus expenses” - others. In addition, BCCs differ depending on the purpose of the payment. If this is a basic payment, there is only one code. If penalties are different, for fines it’s third. See all BCCs under the simplified tax system in 2021 in the table below.

KBK on simplified tax system – 2021 (income)

| Purpose of payment | KBK |

| Advances and tax for the object “income” | 182 1 0500 110 |

| Penalties for the object “income” | 182 1 0500 110 |

| Fines for the object “income” | 182 1 0500 110 |

KBK on simplified tax system – 2021 (income minus expenses)

| Purpose of payment | KBK |

| Advances, tax and minimum tax for the object “income minus expenses” | 182 1 0500 110 |

| Penalties for the object “income minus expenses” | 182 1 0500 110 |

| Fines for the object “income minus expenses” | 182 1 0500 110 |

Unified work regulations

Recipients of budgetary funds, such as chief managers of budgetary funds (GRBS), government, budgetary and autonomous institutions, are required to keep records, draw up plans and reports according to uniform standards and in accordance with legal requirements. A list of requirements and rules for the use of special codes that determine the corresponding values of the budget (accounting) account are established by the Ministry of Finance for all participants in the process.

The work algorithm regarding the formation of budget classification codes is established in the order of the Ministry of Finance No. 85n with changes for 2020: the types of expenses of KOSGU were updated after the entry into force of the order of the Ministry of Finance No. 98n dated 06/08/2020. The regulation has updated the procedure for applying CWR for budgetary institutions - public sector accountants are required to work in a new way.

In addition, legislators adjusted the rules for the formation of KOSGU. A new order of the Ministry of Finance No. 209n dated November 29, 2017 (as amended on September 29, 2020) was approved. It is unacceptable to work using old algorithms.

A public sector accountant should pay special attention to the updated regulations - types of expenses, KOSGU according to Order No. 65n with amendments for 2021 are not relevant. It is necessary to work according to orders No. 85n and No. 209n. The use of outdated codes in accounting is not allowed, otherwise the manager will be held accountable.

BCC for other taxes, fees and obligatory payments for 2018

Below we present the BCC for all other taxes, fees, and obligatory payments. Check the codes on your payment slips with the tables to avoid errors.

KBK on UTII (single tax on imputed income) 2018

| Tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fines | 182 1 0500 110 |

KBK for 2021 for individual entrepreneurs (patent)

| Purpose of payment | Mandatory payment | Penalty | Fine |

| tax to the budgets of city districts | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| tax to the budgets of municipal districts | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| tax to the budgets of Moscow, St. Petersburg and Sevastopol | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| tax to the budgets of urban districts with intracity division | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| to the budgets of intracity districts | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

BCC for Unified Agricultural Tax for 2021

| Tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fines | 182 1 0500 110 |

KBK for water tax for 2021

| Tax | 182 1 0700 110 |

| Penalty | 182 1 0700 110 |

| Fines | 182 1 0700 110 |

BCC for land tax (table)

| Payment Description | KBK tax | KBK penalties | KBC fines |

| For plots within the boundaries of intra-city municipalities of Moscow and St. Petersburg | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| For plots within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| For plots within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| For plots within the boundaries of rural settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| For plots within the boundaries of urban settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| For plots within the boundaries of urban districts with intra-city division | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| For plots within the boundaries of intracity districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

KBC for mineral extraction tax 2018

| Payment Description | KBK tax | KBK penalties | KBC fines |

| Oil | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Combustible natural gas from all types of hydrocarbon deposits | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Gas condensate from all types of hydrocarbon deposits | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Extraction tax for common minerals | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Tax on the extraction of other minerals (except for minerals in the form of natural diamonds) | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Mineral extraction tax on the continental shelf of the Russian Federation, in the exclusive economic zone of the Russian Federation, when extracting minerals from the subsoil outside the territory of the Russian Federation | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Mineral extraction tax in the form of natural diamonds | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Mineral extraction tax in the form of coal | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

Payments for the use of subsoil (KBK 2018)

| Payment Description | KBK |

| Regular payments for the use of subsoil for the use of subsoil (rentals) on the territory of the Russian Federation | 182 1 1200 120 |

| Regular payments for the use of subsoil (rentals) for the use of subsoil on the continental shelf of the Russian Federation, in the exclusive economic zone of the Russian Federation and outside the Russian Federation in territories under the jurisdiction of the Russian Federation | 182 1 1200 120 |

Payments for the use of natural resources - KBK for 2018

| Payment Description | KBK for payment |

| Payment for negative impact on the environment Payment for emissions of pollutants into the air by stationary facilities | 048 1 1200 120 |

| Payment for emissions of pollutants into the atmospheric air by mobile objects | 048 1 1200 120 |

| Payment for discharges of pollutants into water bodies | 048 1 1200 120 |

| Payment for disposal of production and consumption waste | 048 1 1200 120 |

| Payment for other types of negative impact on the environment | 048 1 1200 120 |

| Payment for the use of aquatic biological resources under intergovernmental agreements | 076 1 1200 120 |

| Payment for the use of federally owned water bodies | 052 1 1200 120 |

| Income in the form of payment for the provision of a fishing area, received from the winner of the competition for the right to conclude an agreement on the provision of a fishing area | 076 1 1200 120 |

| Income received from the sale at auction of the right to conclude an agreement on fixing shares of quotas for the production (catch) of aquatic biological resources or an agreement for the use of aquatic biological resources that are in federal ownership | 076 1 1200 120 |

KBK for fees for the use of wildlife objects (2018)

| KBK for fees | BCC for penalties | KBC for fines |

| 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

BCC 2021 for fees for the use of aquatic biological resources

| Payment Description | Codes | ||

| Tax | Penalty | Fines | |

| Fee for the use of aquatic biological resources (excluding inland water bodies) | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Fee for the use of objects of aquatic biological resources (for inland water bodies) | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

KBK 2021 for trading fee

| Payment Description | KBK for payment |

| Trade tax in federal cities | 182 1 0500 110 |

| Penalty trading fee | 182 1 0500 110 |

| Interest trading fee | 182 1 0500 110 |

| Fines trade fee | 182 1 0500 110 |

KBK 2021: tax on gambling business

| BCC for tax | BCC for penalties | KBC for fines |

| 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

State duty: BCC for 2021 (table)

| Payment Description | KBK |

| State duty on cases considered in arbitration courts | 182 1 0800 110 |

| State duty on cases considered by the Constitutional Court of the Russian Federation | 182 1 0800 110 |

| State duty on cases considered by constitutional (statutory) courts of constituent entities of the Russian Federation | 182 1 0800 110 |

| State duty on cases considered by the Supreme Court of the Russian Federation | 182 1 0800 110 |

| State duty for state registration: – organizations; – individuals as entrepreneurs; – changes made to the constituent documents of the organization; – liquidation of the organization and other legally significant actions | 182 1 0800 110 |

| State duty for the right to use the names “Russia”, “Russian Federation” and words and phrases formed on their basis in the names of legal entities | 182 1 0800 110 |

| State duty for carrying out actions related to licensing, with certification in cases where such certification is provided for by the legislation of the Russian Federation, credited to the federal budget | 182 1 0800 110 |

| Other state fees for state registration, as well as performance of other legally significant actions | 182 1 0839 110 |

| State duty for re-issuance of a certificate of registration with the tax authority | 182 1 0800 110 |

Income from the provision of paid services and compensation of state costs: KBK 2018

| Payment Description | KBK for payment |

| Fee for providing information contained in the Unified State Register of Taxpayers | 182 1 1300 130 |

| Fee for providing information and documents contained in the Unified State Register of Legal Entities and the Unified State Register of Individual Entrepreneurs | 182 1 1300 130 |

| Fee for providing information from the register of disqualified persons | 182 1 1300 130 |

KBC 2021: fines, sanctions, damages

| Payment Description | KBK for payment |

| Monetary penalties (fines) for violation of legislation on taxes and fees, provided for in Art. 116, 118, paragraph 2 of Art. 119, art. 119.1, paragraphs 1 and 2 of Art. 120, art. 125, 126, 128, 129, 129.1, art. 129.4, 132, 133, 134, 135, 135.1 | 182 1 1600 140 |

| Monetary penalties (fines) for violation of legislation on taxes and fees provided for in Article 129.2 of the Tax Code of the Russian Federation | 182 1 1600 140 |

| Monetary penalties (fines) for administrative offenses in the field of taxes and fees provided for by the Code of Administrative Offenses of the Russian Federation | 182 1 1600 140 |

| Monetary penalties (fines) for violation of legislation on the use of cash register equipment when making cash payments and (or) payments using payment cards | 182 1 1600 140 |

| Monetary penalties (fines) for violation of the procedure for handling cash, conducting cash transactions and failure to fulfill obligations to monitor compliance with the rules for conducting cash transactions | 182 1 1600 140 |

Source

Source

Application of budget classification in 2021

25.03.2018

The budget classification of the Russian Federation is a grouping of income, expenses and sources of financing the budget deficit and (or) operations of the general government sector, used by institutions in maintaining budget (accounting) records, preparing budget (accounting) and other financial statements that ensure comparability of budget indicators of the budget system of the Russian Federation . We will talk about which KOSGUs are used by healthcare institutions in 2021 when making income and expense transactions in this consultation.

The main document regulating the rules for applying the budget classification of the Russian Federation is Instructions No. 65n

. Changes are regularly made to this document by orders of the Ministry of Finance. In particular, when drawing up and executing the budget for 2018 (and for the planning period of 2021 and 2021), the adjustments made to Instructions No. 65n by orders of the Ministry of Finance are taken into account:

– Order No. 177n dated November 2, 2017

;

– Order No. 210n dated November 29, 2017

;

– Order No. 255n dated December 27, 2017

.

Not all changes made to Directive No. 65n are of interest to healthcare institutions, since they do not affect their activities. Among the above orders for these institutions, the provisions of Order No. 255n, which introduce adjustments to the articles of KOSGU, are of greatest interest. Order No. 255n additionally detailed the articles and sub-articles of KOSGU in order to ensure completeness of reflection in the accounting (budget) accounting of information about the operations carried out by the institution. For the convenience of transition to the application of new subarticles of the KOSGU, a comparative table of codes for the classification of operations of the general government sector for 2021 is posted on the website of the Ministry of Finance (in the “Budget/Budget Classification” section). In the same section there is a comparative table of the procedure for applying the classification of operations of the general government sector established by Order No. 65n (2018), and the procedure for applying the classification of operations of the general government sector established by Order of the Ministry of Finance of the Russian Federation dated November 29, 2017 No. 209n

(2019). Those who are interested in the changes that are mandatory for use next year can familiarize themselves with the information posted in this table.

Let's consider the new provisions of Directive No. 65n regarding the application of KOSGU.

Article 120 “Income from property”

Details of this article, as well as articles 130

,

140

,

180

, subarticles of KOSGU is dictated by the need to accurately determine the institution’s source of income.

Thus, due to the fact that from January 1, 2021, the provisions of the Federal Accounting Standards Service “Rent”

, establishing the need for separate accounting of operations for operating and financial (non-operating) leases,

Article 120

of KOSGU is supplemented

with subarticles 121

“Income from operating leases”,

122

“Income from financial leases”.

Also, individual sub-articles indicate the income received by the institution in the form of interest on deposits ( sub-article 124

), provided borrowings (

sub-article 125

), etc.

Not all sub-articles supplementing Article 120

, are relevant for healthcare institutions.

For example, subarticles 123

“Payments for the use of natural resources”,

127

“Dividends from investment objects” are unlikely to be used by them, since the transactions for which these subarticles of KOSGU are used are not typical for this type of institution. Below in the table we consider the sub-articles of KOSGU, which are relevant for healthcare institutions and have not previously been used by them in their work.

| Subarticle code | Sub-article name | Income attributable to this sub-item |

| 121 | "Income from operating leases" | Income from operating lease agreements in the form of rental payments, which are payments for the use of leased property (except for rental payments when providing land) |

| 122 | "Income from finance lease" | Income received by an institution under a non-operating (financial) lease agreement (excluding income from contingent lease payments), including: – income arising under a lease agreement providing for the provision by the lessor of an installment plan for payment of lease payments (rent and (or) redemption value of the leased property); – income arising under leasing agreements |

| 124 | “Interest on deposits, cash balances” | Interest income on the balance of funds placed in the form of deposits, as well as interest on balances in accounts with the Central Bank of the Russian Federation and credit institutions |

| 125 | “Interest on borrowings provided” | Income in the form of loans, microloans (loans) provided by budgetary (autonomous) institutions |

| 126 | “Interest on other financial instruments” | Income from the granting by an institution of non-exclusive rights to the results of intellectual activity and (or) means of individualization |

| 128 | “Income from the granting of non-exclusive rights to the results of intellectual activity and means of individualization” | Income from the granting of non-exclusive rights to the results of intellectual activity and (or) means of individualization |

| 129 | “Other income from property” | Income from property not allocated to subarticles 121 – 128 KOSGU, including income from the transfer of part of the profits of the Central Bank of the Russian Federation and other income from property |

Article 130 “Income from the provision of paid services (work), compensation of costs”

Article 130

usually used by budgetary and autonomous institutions, since it is they who, by virtue of the provisions

of Art.

298 Civil Code of the Russian Federation ,

art.

9.2 of the Law on Non-Profit Organizations provides the right to carry out income-generating activities.

The income received by the institution from such activities and the property acquired from these incomes shall be at the independent disposal of the institution. Previously, all income that an institution received from carrying out income-generating activities was reflected under Article 130

(including income from the provision of services under the compulsory medical insurance program), now each type of income has its own sub-article. The table provides a description of individual sub-articles of KOSGU, which are used by healthcare institutions.

| Subarticle code | Sub-article name | Income attributable to this sub-item |

| 131 | “Income from the provision of paid services (work)” | Income from the provision of paid services and work (except for income from the provision of services (work) under the compulsory medical insurance program), including: – income from the provision of paid services (work) to consumers of relevant services on the territory of the Russian Federation, in particular to the population of the Russian Federation, as well as citizens of other states (non-residents); – income from attracting convicts to paid work (in terms of provision of services (work)); – income of state (municipal) institutions from receipts of subsidies for financial support for their implementation of state (municipal) tasks; – other income from the provision of paid services (work) |

| 132 | “Income from the provision of services (work) under the compulsory health insurance program” | Income received by the institution from the provision of medical services provided to insured persons within the framework of the basic compulsory health insurance program |

| 134 | "Income from compensation of expenses" | Income from compensation of expenses, including: – reimbursement of state fees previously paid when going to court; – a fee charged to personnel when issuing a work book or an insert in it as compensation for the costs incurred by the employer in purchasing them; – income received by way of reimbursement of expenses aimed at covering procedural costs; – reimbursement of expenses for carrying out enforcement actions by bailiffs; – other income from compensation of expenses |

| 135 | “Income from contingent rental payments” | Income from reimbursement of costs for the maintenance of property leased in accordance with a lease agreement (property lease) or a gratuitous use agreement, including: – income from compensation of costs (expenses) for paying for utilities, as well as services for operation and maintenance of the rented building (premises); – other income received by way of reimbursement of costs (expenses) incurred in connection with the maintenance of property; – other similar income |

| 136 | “Budget revenues from the return of accounts receivable from previous years” | Receipts to budget revenues from the return of receivables from previous years generated by the recipient of budget funds |

Article 140 “Fines, penalties, penalties, compensation for damage”

Before Order No. 255n came into force, healthcare institutions reported income from administrative payments and fines, fees, sanctions, compensation for damages in accordance with the legislation of the Russian Federation under Article 140

KOSGU. In particular, this article was applied when recording:

– amounts of damage in the form of accrued interest for the use of someone else’s money due to their unlawful retention, evasion of their return, other delay in their payment or unjustified receipt or savings; – amounts of debt for compensation of damage in accordance with the legislation of the Russian Federation in the event of insured events; – amounts of debt for fines, penalties, penalties accrued for violation of the terms of contracts for the supply of goods, performance of work, provision of services, and other sanctions.

After the above order comes into force, each type of income is reflected in its own sub-item, which makes it easier to identify the type of income received by the institution. In the table we present the new subarticles of KOSGU.

| Subarticle code | Sub-article name | Income reflected by sub-item |

| 141 | “Income from penalties for violation of procurement legislation and violation of the terms of contracts (agreements)” | Income in the form of fines, penalties, penalties |

| 142 | “Income from penalties on debt obligations” | Income in the form of fines, penalties, penalties |

| 143 | "Insurance compensation" | Receipts of insurance compensation from insurance organizations |

| 144 | “Compensation for property damage (except for insurance compensation)” | Income from monetary penalties (fines) and other amounts in compensation for damage to property, including damage to financial assets |

| 145 | “Other income from forced seizure amounts” | Proceeds from monetary penalties (fines) imposed to compensate for damage caused as a result of illegal or misuse of budget funds, other monetary penalties (fines) for violation of legislation in the field of finance, taxes and fees, insurance, securities market, other monetary penalties ( fines), from confiscations, compensations, penalties, penalties and amounts of forced seizure not attributed to subarticles 141 – 144 KOSGU |

Article 170 “Income from transactions with assets”

This article has been supplemented by subarticles 175

“Exchange differences based on the results of recalculation of accounting (financial) statements of foreign institutions” and

176

“Income from the valuation of assets and liabilities” of KOSGU.

subsection 176

is of greater interest . This sub-item includes transactions that reflect the financial result from the assessment of financial and non-financial assets and liabilities, including fixed assets, intangible assets, non-produced assets, and inventories.

Article 180 “Other income”

Instructions No. 65n, as amended before the entry into force of Order No. 255n, provided for all income not included in Articles 110 – 170

, reflect under

Article 180

. By Order No. 255n this article was supplemented with the following sub-articles:

| Subarticle code | Sub-article name | Income reflected by sub-item |

| 181 | "Unidentified receipts" | Payments to be classified as unidentified revenues credited to the budgets of the budget system of the Russian Federation |

| 182 | “Income from gratuitous right of use” | Income in the form of the difference between the amount of lease payments under an agreement on free use (lease on preferential terms) and the amount of the fair value of lease payments |

| 183 | “Income from subsidies for other purposes” | Income received by state (municipal) institutions from the relevant budgets, from subsidies for other purposes |

| 184 | “Income from subsidies for capital investments” | Income from subsidies for capital investments received by state (municipal) institutions from the relevant budgets |

| 189 | "Other income" | Other income of state (municipal) institutions not included in other articles of KOSGU groups 100 “Income” and |

Subarticle 274 “Losses from impairment of assets”

From January 1, 2021, the concept of “asset impairment” is introduced in relation to the activities of state (municipal) institutions. Uniform requirements for the procedure for identifying signs of asset impairment, signs of reducing losses from asset impairment, the classification and composition of such signs are established by the federal accounting standard for public sector organizations “Impairment of Assets”, approved by Order of the Ministry of Finance of the Russian Federation dated December 31, 2016 No. 259n

.

In order to reflect transactions to recognize the impairment of assets, subarticle 274

of KOSGU was introduced.

Article 290 “Other expenses”

Until recently, Article 290

included expenses not related to wages, the purchase of works, services for state (municipal) needs, the needs of state (municipal) institutions, servicing state and municipal debt obligations, debt obligations of state (municipal) institutions, an approximate list of which was given in Instructions No. 65n.

By Order No. 255n, expenses previously attributed to Article 290

are distributed between subarticles.

| Subarticle code | Sub-article name | Expenses reflected under the named sub-item |

| 291 | "Taxes, duties and fees" | Expenses for paying taxes (included in expenses), state duties and fees, various types of payments to budgets of all levels: – value added tax and income tax (in terms of obligations of state (municipal) government institutions); – property tax; – land tax, including during the construction of the facility; – transport tax; – fees for environmental pollution; – state duties and fees in cases established by the legislation of the Russian Federation |

| 292 | “Fines for violation of the legislation on taxes and fees, legislation on insurance premiums” | Expenses for payment of fines, penalties for late payment of taxes, fees, insurance premiums |

| 293 | “Fines for violation of procurement legislation and violation of the terms of contracts (agreements)” | Expenses for payment of fines for violation of the legislation of the Russian Federation on the procurement of goods, works and services, as well as payment of penalties for violation of the terms of contracts (agreements) for the supply of goods, performance of work, provision of services |

| 295 | "Other economic sanctions" | Expenses for payment of other economic sanctions not included in subarticles 292 – 294 |

| 296 | "Other expenses" | Expenses not included in Articles 210 – 270 and 1) payment: a) scientists, scholarship workers; b) to individuals (except for individuals who are producers of goods, works, services) state bonuses, grants, monetary compensation, allowances, and other payments; c) state awards, grants in various fields; 2) compensation for losses and harm (in particular, compensation for moral damage by decision of judicial authorities); 3) purchase (production) of gift and souvenir products not intended for further resale: a) greeting cards and inserts for them; b) greeting addresses, certificates of honor, letters of gratitude, diplomas and certificates of laureates of competitions for awards, etc.; c) flowers and other gift and souvenir products; 4) other expenses: a) entertainment expenses for receiving and servicing delegations; b) compensation to plaintiffs for legal costs on the basis of judicial acts that have entered into legal force; c) purchase (manufacture) of special products; 5) fees for membership in organizations, except for membership fees in international organizations; 6) payment of daily allowances to witnesses, as well as to persons forcibly brought to court or to a bailiff; 7) other similar expenses |

Article 350 “Increase in the right to use an asset”

In accordance with clause 20 of the FSBU “Rent”

initial recognition of an operating lease accounting object - the right to use an asset, which is determined on the date of classification of lease accounting objects in the amount of lease payments for the entire period of use of the property provided for in a lease agreement (property lease) or a gratuitous use agreement, while simultaneously reflecting the lease obligations of the user (lessee) (lease payables).

The right to use the asset is reflected in account 0 111 00 000

. When using this account in digits 24 – 26 of the account number the following is indicated:

– article 350

“Increasing the right to use an asset” (the article is applied upon receipt and acceptance of a leased asset for accounting);

– Article 450

“Reduction of the right to use an asset” (the article applies upon termination of contractual relations).

Group 400 “Disposals of non-financial assets”

This group is detailed in Articles 410 – 450

KOSGU, within which operations for the disposal of non-financial assets are grouped, including during their sale, in terms of cash receipts and disposals.

By Order No. 255n, this group was supplemented with subarticles 412

,

422

,

432

of KOSGU.

Amounts of reduction in the value of fixed assets, intangible assets, and non-produced assets are now included in subarticles 411

,

421

, and not

articles 410

,

420

.

| Article code | Article title | Expenses reflected under the named item |

| 411 | "Depreciation of fixed assets" | Reflects the amount of decrease in the value of fixed assets as a result of their depreciation |

| 412 | "Impairment of fixed assets" | Refers to the amount of reduction in economic benefits and useful potential contained in an item of fixed assets arising as a result of their depreciation |

| 421 | "Amortization of intangible assets" | Refers to the amount of decrease in the value of intangible assets as a result of their depreciation |

| 422 | "Impairment of intangible assets" | Refers to the amount of reduction in economic benefits and useful potential contained in the object of intangible assets arising as a result of their impairment |

| 432 | "Impairment of non-produced assets" | Refers to the amount of reduction in economic benefits and useful potential embodied in an item of non-produced assets that is not associated with changes in their fair value in the normal course of use resulting from impairment |

* * *

At the end of the consultation, we note that the changes made by Order No. 255n to Directive No. 65n are aimed at:

– details of the income received by the institution in the course of its activities. In order to establish the source of income for institutions of Article 120

,

130

,

140

,

180

KOSGU supplemented with subarticles;

– details of expenses included by the institution in the group “Other expenses” ( Article 290

is supplemented by sub-articles between which expenses classified as part of this group by Instructions No. 65n are distributed);

– bringing their provisions into compliance with the requirements of federal standards that entered into force on January 1, 2021 (the document is supplemented by subarticles 274

,

412

,

421

,

422, articles 350

,

450

).

Silvestrova T., expert of the information and reference system “Ayudar Info”

Send to a friend