Let's start with the question of what kind of certificate KND 1120101 is. The form reveals information about the absence or presence of arrears in fiscal and budget payments to the state treasury. The certificate can only be issued upon official request. It is important to understand that this is not only about current arrears. Tax authorities take into account all types of penalties, penalties, interest and fines. Moreover, the form does not indicate a breakdown of the existing arrears. The inspection will indicate whether there is a debt or not. For additional detail of calculations with the budget, you should request another document - a certificate of the status of calculations KND 1160080.

Why do you need a form?

Confirming the absence of tax debts may be required in different situations. For example, current cases when KND form 1120101 is required:

- Registration of borrowed capital in a credit institution. For example, if an organization applies to a bank for a loan, it will have to confirm that the taxpayer does not have any late payments or debts on fiscal payments.

- Participation in state or municipal procurement. The procurement participant is obliged to confirm his integrity and solvency. One of the evaluation criteria is the absence of debts on taxes and fees.

- Participation in competitions and government grants also requires the provision of reporting documentation confirming the absence of debt to the budget, including taxes.

- The founder or owner of the organization has the right to request information about the absence of tax delinquencies. Information is necessary when planning and distributing the budget for the corresponding year.

- Information is required for analysis and management decision-making. The certificate will be useful to accounting employees when preparing reports and financial documentation.

The form may also be useful when carrying out control activities. For example, during an on-site inspection by the Tax Inspectorate and other inspectors.

Who issues

A certificate of taxes and duties is issued only by a representative of the Federal Tax Service. Other representatives of government agencies are not authorized to issue such documents.

You should request the form at the territorial office of the Federal Tax Service at the place of registration of the taxpayer. If an organization has separate divisions and branches, then information will have to be requested from all Federal Tax Service Inspectors at the location of the branch network.

IMPORTANT!

You can only get a certificate of absence of tax debts from the Federal Tax Service!

Help contents

The certificate will indicate the following:

- name of the tax authority that issued the document;

- information about the taxpayer;

- the date as of which the applicant has or does not have tax debts;

- status of tax payments (indicate one of the options “Has” or “Does not have” debt);

- FULL NAME. and signature of the head of the tax authority, seal.

What form is used?

The form was approved in Appendix No. 1 to the Order of the Federal Tax Service dated July 21, 2014 No. ММВ-7-8/ [email protected] The structure of the document is simple and does not contain special fields. The form gives a clear answer: whether the taxpayer has an outstanding debt or not. If there are overdue tax payments, the Federal Tax Service inspector will indicate the code of the territorial office in which the penalty or arrears are listed.

For example, an organization liquidated a branch. Made calculations with the budget and paid all fiscal tranches. But based on the results of a desk audit, the inspectorate accrued a tax arrears of 5 rubles. No notifications were received to the company's head office. The received certificate confirming the presence and absence of tax debt will reveal information about the debt. The form will indicate that there is a tax debt. And in the application, the inspector will indicate the code of the Federal Tax Service, in which the delay is listed.

How the certificate form has changed

The certificate form has recently undergone changes - due to serious changes associated with the transfer of part of the powers from funds to tax authorities. Changes in tax legislation have led to changes in documentation. The previous form of certificate 39-1 was canceled due to the transfer of administrative rights for insurance premiums to the Federal Tax Service. The previous form of the certificate did not provide for the reflection of data on the status of settlements for insurance premiums. The new form was approved by Order of the Federal Tax Service of Russia dated December 28, 2016 No. ММВ-7-17/ [email protected] (KND form 1160080).

A current sample form can be viewed here.

The certificate on paper is signed by the head or deputy head of the tax authority and certified with an official seal.

What do you need to receive

An official certificate of tax debt is issued only upon special request. It can be sent in several ways:

- in person by filling out an application to the Federal Tax Service;

- through an authorized representative (an official power of attorney is required);

- by sending an application by registered mail;

- by submitting an electronic request through the taxpayer’s personal account;

- by sending a forgiveness through the single portal “State Services”;

- by contacting the multifunctional center (if there is no Federal Tax Service Inspectorate in the locality).

When applying in person, you must present a passport of a citizen of the Russian Federation, as well as documents confirming your authority to represent the interests of the organization. For example, if the head of the company contacted the Federal Tax Service, then a passport is sufficient. And if the registration is carried out by a deputy or another person, then a power of attorney is required.

The procedure for applying for a certificate and issuing it

Approving the previous form of the certificate, representatives of the Federal Tax Service in the Guidelines for filling it out also prescribed some details of the procedure for issuing it. Thus, it was stipulated that this document should be provided to the Federal Tax Service at the place of registration of the taxpayer upon his written application signed by the head of the organization. The tax authority was given 10 days from the date of receipt of the application to prepare the certificate. However, the Procedure does not contain similar provisions.

There are no special rules for applying for a certificate and its issuance and the Administrative Regulations of the Federal Tax Service for the provision of public services for free information (including in writing) to taxpayers, which was approved by Order of the Ministry of Finance of Russia dated July 2, 2012 N 99n (hereinafter referred to as the Regulations). Nevertheless, an analysis of its provisions allows us to conclude that in the situation under consideration one should be guided by paragraphs 125 - 144 of the Regulations. These rules describe the procedure for informing taxpayers about the status of their settlements with the budget, or, more simply, the procedure for providing the relevant certificate, which has already been mentioned.

Thus, in order to obtain this document, the taxpayer must contact the Federal Tax Service at the place of registration with a written request, the recommended form of which is given in Appendix No. 8 to the Regulations. At the same time, the latter provides the opportunity to indicate in the appropriate fields what kind of certificate the business entity is requesting - about the status of settlements with the budget, the fulfillment of the obligation to pay taxes, or both at once.

According to clause 127 of the Regulations, a certificate of the status of settlements is provided within 5 working days from the date the inspection receives the corresponding written request. Apparently, a certificate of fulfillment of tax obligations must now be issued within the same period.

The request can be submitted by the taxpayer to the Federal Tax Service either in person or by mail. Likewise, it must indicate how the applicant wishes to receive the certificate - in person at the inspectorate or by mail. If this is not done, the document will be sent to him by post. When receiving the certificate in person, you will need to present an identification document. Otherwise, the document will again be sent by mail. This outcome awaits the applicant if, within 5 working days from the expiration of the deadline for issuing the certificate in person, as indicated in the request, he does not appear for it.

It should be borne in mind that the request may also be refused. However, the grounds for such a refusal are, for the most part, errors made when filling out the request, or rather, the absence of any mandatory information in it. These include:

- full name of the organization (last name, first name, patronymic (if any) of the individual entrepreneur);

- TIN of the applicant;

- postal address (email address) of the applicant;

- signatures and indications of the surname and initials of the individual - representative of the organization who submitted and (or) signed the request;

- an imprint of the organization's seal (in a request submitted on paper and not on the organization's letterhead produced by printing).

In addition, the basis for refusal may be the lack of authority of the person who signed the request to contact the tax authority to obtain information about the applicant or his failure to provide documents confirming such authority.

Finally, submitting a request whose text is not legible will also not lead to the desired help.

If the above grounds are present, the request will simply be returned to the applicant. At the same time, at his request, the responsible official of the Federal Tax Service must put on the request a mark indicating refusal to accept the request, his last name, initials and position, and the date of refusal. When sending a request by mail, a special notice of refusal to accept the request will be prepared and sent to the taxpayer.

If everything is fine, then the inspection specialist must put a mark on the second copy of the request about its acceptance (and the documents attached to it), surname, initials, position and date of receipt of the request.

But even after accepting the request, the issuance of a certificate may still be refused. The list of reasons for this is given in paragraph 30 of the Regulations, but all of them are irrelevant if the request is filled out by the taxpayer strictly according to the form without indicating unnecessary requests, questions, etc.

Features of receiving in paper form

You can obtain a completed sample of KND certificate 1120101 about tax debts at any branch of the Federal Tax Service. To do this, you will have to fill out an application in the form approved in Appendix No. 8 to the Administrative Regulations, approved by Order of the Ministry of Finance of the Russian Federation dated July 2, 2012 No. 99n.

In your application, please provide the following information:

- In the header of the document: Full name. the head and the name of the Federal Tax Service to which you are submitting the request.

- We indicate what type of information is required for registration. Place a tick in the required field.

- Enter the date or period for which information is required. If the data is not specified, the inspectorate will prepare information as of the date the request is received.

- Applicant details. It is necessary to identify the taxpayer for whom information is needed. We indicate the full name of the organization, address, tax identification number and checkpoint.

- We prescribe the method for receiving the answer.

- We put the seal and signature of the manager.

The response from the Federal Tax Service will be ready within 10 working days from the date of receipt of the official request.

Rules for obtaining documents

Obtaining a certificate of no debt is not difficult. This can be done by both a legal entity and an ordinary citizen. You must first draw up a request and send it to the appropriate authority at your location (for enterprises) or place of residence (for individuals). There is no unified request form. There is only a general order of presentation of information, taken as a model. The following request is written in the form of a regular statement:

- First, the details of those to whom and from whom it is sent are indicated at the top right.

- On the left is the date and outgoing number (for the organization).

- The word “request” is written a little lower in the center and its purpose is indicated.

- Next comes a phrase asking for data for a specific date. If it is not specified, then the information is provided at the time of registration of the request.

- Then comes the signature of the head of the company, certified by the round seal of the enterprise.

- At the very bottom left is information about the artist.

A response to such a request is usually given within 10 business days. Other authorities have their own deadlines for providing data.

On paper

The application is submitted in paper form. It can be downloaded, printed and filled out in advance, or received from the tax office and filled out on the spot. When filling out, you will need the name of the organization, full name, tax identification number, checkpoint.

When sending an application by mail, you need to issue it as a registered letter with acknowledgment of receipt and enclose a list of documents. To receive a certificate by mail, you must indicate this in the “Method of receiving a response” column.

Features of receiving electronically

To receive an electronic document, make a request through your telecom operator or, in short, TKS. The electronic request will be generated using the KND form 166101 (approved by Order of the Federal Tax Service No. ММВ-7-6/ dated 06/13/2013). The procedure for drawing up an application is similar to an application on paper. The digital signature of the manager is signed and sent through the TKS operator to the tax office at the place of registration.

In response, the Federal Tax Service will send you a Federal Tax Service certificate confirming the absence of debt within the established ten-day period. The answer will arrive via telecommunication channels. The inspectorate responds to an electronic request faster than a paper one. Consequently, the taxpayer will be able to satisfy the counterparty’s request for confirmation of good faith more quickly.

KND certificate 1120101 - via the tax website.

The next available option for obtaining a certificate of no debt is to make a request through the tax office website.

To do this, you will need to register in the personal account of a legal entity on the Federal Tax Service website.

- Disadvantages of this method:

- To send a request through your personal account, you will need an electronic signature and a Crypto Pro license. The cost today ranges from 3000-5000 rubles.

- The received certificate KND 1120101 will be on paper, which will not allow the use of this certificate in the interface of some trading platforms.

Features of receiving in electronic form

You can submit your request via the Internet. For example, using specialized accounting programs, fill out a request and send it via secure communication channels. Or prepare an application through the taxpayer’s personal account or the State Services portal. The request is generated in a similar manner.

IMPORTANT!

When sending an application electronically, the Federal Tax Service will also prepare a response in electronic form. To receive a paper certificate (with a blue stamp), you will have to contact the inspectorate in person.

How to check the accuracy of the certificate

In fact, the certificate reflects the presence or absence of tax debt. The taxpayer may not be aware of the existence of a debt or penalty. The applicant can only check his details to see if the inspection made any mistakes in them.

If, according to the company’s accounting data, there are no fiscal debts, and the Federal Tax Service indicated in the certificate that there is a debt, then it is necessary to act:

- Request the Federal Tax Service for an amendment to your budget calculations.

- Reconcile accounting data and inspection information.

- Identify discrepancies and determine their causes.

- If the arrears are the fault of the company, repay the amounts in the general manner.

- Make adjustments to your accounting. For example, reflect underaccrued penalties and fines in an accounting statement.

- Prepare adjusting statements as necessary.

If the debt is unjustified and an error is suspected in the Federal Tax Service data, then you must contact the inspectorate. Prepare payment documents, tax registers and other documentation confirming the absence of debt. Provide evidence to the inspector. Upon request, a review will be initiated.

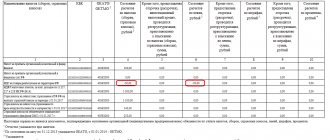

This is what a correctly completed sample certificate of no tax debt looks like:

Certificate on the status of settlements with the budget

The certificate form was approved by Order of the Federal Tax Service dated December 28, 2016 No. ММВ-7-17/ [email protected] It is generated on the date that the taxpayer indicated in the request. It includes information on all taxes that the company is required to pay. It includes information not only directly about the tax payment, but also about the status of payments for penalties and fines.

The certificate consists of a tabular part containing information about the taxpayer, document number and date on which the information is provided, and a tabular part containing information about tax payments.

The tabular section contains 10 columns. For each tax payment the following is indicated:

- name (column 1);

- KBK (column 2);

- OKTMO (column 3);

- balance on taxes, fees, insurance premiums (column 4), penalties (6) and fines (8);

- amounts of tax payments, penalties and fines for which installment plans were provided (columns 5, 7, 9);

- balance on interest provided for by the Tax Code of the Russian Federation.

If the balance is shown with a “+” sign, this indicates the presence of an overpayment for the corresponding fiscal fee. If with a “–” sign, it indicates the presence of arrears.

Analyzing the certificate, we conclude that LLC “Company” has a VAT arrears in the amount of 50 rubles. for tax and 20 rubles. for a penalty. There is an overpayment for income tax, insurance premiums and personal income tax.