The responsibility for mentioning taxes withheld from employee salaries lies with the accounting department of the organization. However, not every novice financier knows how to reflect alimony in 6 personal income taxes .

The rules for document execution are regulated by the order of the Federal Tax Service of the Russian Federation of 2015. According to the law, the paper must contain all payments to employees and their wages for the reporting period. Information about alimony payments in the financial document is indicated in field 130.

Alimony in 6 personal income taxes: procedure for withholding obligations

The employer has the right to withhold funds from the employee’s salary and transfer them to other citizens on the basis of the following documents:

- writ of execution handed over to the employer by the bailiff service;

- a voluntary agreement drawn up between an employee of an organization and another person entitled to receive salary.

According to federal law, when calculating the amount of alimony payments, the following types of income are taken into account:

- salary;

- allowances and bonuses;

- vacation funds;

- unemployment benefits;

- sick leave payments;

- reimbursement for meals;

- motivational and compensation payments;

- remuneration to the classroom teacher for leading a school class;

- payments to health workers for receiving citizens;

- journalistic, author or writer's fees;

- payments for work in particularly difficult conditions;

- scholarship;

- pension accruals;

- profit from business activities;

- profit from the rental of real estate;

- dividends from financial institutions;

- profit from the sale of copyrighted objects.

The timing of collection of funds from an employee directly depends on the document that is the basis for paying alimony:

- If the basis is a writ of execution, the employer undertakes to collect the required amount and transfer it to the recipient no later than three days after payment of wages or other income.

- If the basis is a voluntary agreement between citizens, then the terms of payment of maintenance are set out directly in this agreement.

Registration of certificate 2 personal income tax

Today, these certificates are issued solely on the basis of the use of specialized programs. All types of income are included in the program. At the same time, each type of income has its own specific code. A lot depends on this aspect. The thing is that the program algorithm is created in such a way that, by specifying the code and amount of income, the tax deduction procedure is carried out.

We should also not forget about tax deductions, which allow us to reduce the income base in relation to taxes.

All deductions are also issued in code format. Income codes are displayed as a four-digit number. Deduction codes – three-digit number

Please note that only those people who work officially can apply for deductions. If you do not work officially, but receive some income, then you must independently draw up a certificate 3 personal income tax

Individual entrepreneurs who use special taxation systems in their work also cannot claim a tax deduction. Non-residents of the country cannot receive deductions.

As a result: algorithm for entering alimony into personal income tax certificate 6 and what income to take into account

According to the law, the accounting department of the company must deal with the issue of generating reporting documentation. These employees undertake to independently calculate the amount of alimony payments and transfer them to citizens who are indicated as recipients in the writ of execution from the bailiffs or in the agreement between the child’s parents. A complete list of earnings to be taken into account when calculating the amount of alimony payments is available in Government Decree No. 841 of 1996.

Video on the topic

Did you like the article?

Is alimony considered before or after personal income tax withholding?

Calculation of personal income tax when withholding alimony from material benefits. And also, if the debtor uses a tax deduction, is the employee who pays alimony payments entitled to a standard personal income tax deduction for a child.

As a general rule, any deductions from employee income are made after taxes have been withheld from them. Therefore, to the question of how alimony is withheld, with or without personal income tax, there is a clear answer - alimony is withheld after personal income tax is withheld.

Therefore, before determining the amount of deductions for the month, you need to calculate the personal income tax on the employee’s income.

After calculating the tax amount, a basic value is obtained, on its basis the maximum amount of alimony that will be withheld is determined.

Kugeiko Angela Sergeevna 05/16/2019 at 14:09 Hello, Oleg If you did not work, this does not mean that you do not need to pay alimony during this period.

They will be calculated for you based on the average salary in Russia. I wish you good luck and all the best!

Senkevich Valeria Aleksandrovna 05/16/2019 at 14:09 Hello! You can provide to the court any evidence you consider necessary, incl.

and certificates. Good luck to you and all the best!

Kolkovsky Yuri Valerievich 05/16/2019 at 14:11 The law provides for the possibility of reducing alimony if the financial or marital situation has changed.

Deduction of personal income tax and alimony

Depending on the number of children, the amount of child support deductions varies:

- a quarter of the monthly income for one child;

- a third of income for two children;

- half for three or more.

The specified amounts are withheld from the alimony payer only after income tax has been deducted. In other words, this type of social benefit is paid exclusively from “net” income.

Tax legislation establishes the maximum amount of alimony, which cannot exceed 70% of the payer’s income.

In practice, alimony is withheld when the main part of the salary is paid, that is, in the second half of the month. But if the amount is large, for example, for three children, then it is advisable to make payments twice a month: from the advance payment and from the basic salary.

Reflection of alimony in the 6-NDFL report

The issue of reflecting alimony concerns, as a rule, field 130 of the 6-NDFL report. This line reflects all income received by the taxpayer from which the organization withholds tax.

First, let's figure out exactly how income is reflected here. According to the order of the Federal Tax Service, which approved this form, this column must reflect the entire amount of income received by taxpayers without deducting taxes withheld or deductions provided. That is, the amount that will be reflected in 2-NDFL.

Deductions (in particular, alimony) from the income of an individual do not reduce the tax base for personal income tax. This follows from Art. 210 Tax Code of the Russian Federation. Accordingly, the company will first accrue the employee’s income, calculate the tax, and then calculate alimony. And the employee will receive the amount minus tax and alimony.

This means that on line 130 the company will reflect the amount that was accrued and not given to the employee.

If you submitted a report to the inspectorate and indicated in line 130 the amount minus alimony, then you must submit an updated report with the correct full income of the taxpayer. Otherwise, there is a high risk of imposing a fine on the company for providing false information - 500 rubles.

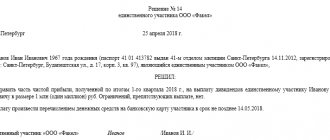

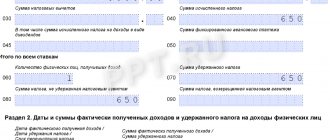

An example of filling out the 6-NDFL calculation in case of withholding alimony

For clarity, let’s look at the situation with alimony using an example and see how to fill out the calculation correctly.

Let's reflect this operation for July in the 2nd section of 6-NDFL:

This is interesting: How to get alimony without divorce

What taxes are imposed on alimony?

When receiving alimony, many people have a question: is this considered income and do they have to pay taxes on it?

In the Tax Code in Art. 208 contains a list of income of individuals subject to personal income tax. There is no alimony on the list. Therefore, from the point of view of tax legislation, they are not subject to taxation.

This is confirmed by paragraph 5 of Art. 217 of the Tax Code of the Russian Federation, which states that all alimony payments are exempt from personal income tax: for children, parents, spouses.

REFERENCE! The penalty accrued for alimony debt is also not taxed.

At its core, this is a certain part of the funds that would still be spent on the child if the parents lived together.

Perhaps you will

Taxpayer status when transferring alimony

Payment of alimony is not a tax payment, which is paid into a non-budget system.

The Ministry of Finance has developed rules for filling out payment slips only for money transfers to the budget (Order of the Ministry of Finance of Russia No. 107n dated November 12, 2013):

- taxes;

- insurance premiums;

- fees;

- customs payments, etc.

In Appendix No. 5 to this order there is a list of statuses from two-digit codes, which must be entered in field 101.

But, since the transfer of alimony is a transfer not to the state budget, these rules in the preparation of a payment order do not apply to it, and nothing is entered in the payer status; the field remains empty.

In this case, the “Purpose of payment” field contains the following information:

- the purpose of the payment is the transfer of alimony;

- object of deduction - from the salary, full name of the employee;

- employee tax identification number;

- for what period is the transfer;

- basis - number and date of the writ of execution.

Personal income tax alimony

This question arises quite often. According to the Labor Code of the Russian Federation, the employer is obliged to pay wages twice a month. Therefore, I would also like to withhold alimony from my salary for the first half of the month. However, this is not at all necessary: Article 109 of the Family Code of the Russian Federation states that alimony is withheld on a monthly basis. Another argument in favor of withholding alimony once a month: as a rule, organizations do not withhold personal income tax from wages for the first half of the month. The personal income tax amount is determined when calculating for the entire month, taking into account standard deductions. And to calculate alimony, you need to take into account the withheld personal income tax. Thus, the employer has every right to withhold alimony only at the end of the month and not pay alimony from the advance.

On reflecting alimony withholding in the 6-NDFL calculation: how to reflect alimony

Alimony is money that is forcibly (judicially) withheld from an individual’s income for the maintenance of minor children or other disabled relatives.

The settlement department of the enterprise withholds monthly from the income of an employee obligated to pay alimony the amount of money, the amount of which was established in court. Alimony begins to be deducted from an individual’s wages from the moment the accounting department receives a writ of execution, which specifies the amount and timing of penalties. Decree of the Government of the Russian Federation No. 841 of July 18, 1996 contains a list of all types of income from which alimony can be withheld (including salaries, additional payments, bonuses and other payments). In the article we will talk about how alimony withholding is reflected in the 6-NDFL calculation.

This is interesting: Article 81 of the Family Code of the Russian Federation, the amount of alimony

Alimony as a type of deduction from wages

Alimony is a type of collection of funds from all types of earnings according to executive documents. Basically, these are deductions from parents for the maintenance of children under the age of majority. The writ of execution specifies the period and amount of the penalty.

The Family Code stipulates that the transfer must be made no later than three days from the date of payment of wages and other accruals.

The dates of receipt of income according to the Tax Code of the Russian Federation are presented in the table:

The first part of Article 137 of the Labor Code of the Russian Federation defines cases of deductions from the earnings of individuals. Decree of the Government of the Russian Federation No. 841 of July 18, 1996 approved the list of earnings from which deductions are made. Tax-free income includes alimony received by taxpayers. This does not apply to payers under executive documents.

From all of the above, we can conclude that the calculation of personal income tax is not affected by penalties under writs of execution. Below we present the completion of the second section, taking into account accrued personal income tax and collected alimony from the income of individuals. An example calculation will help you understand typical situations.

Grounds for withholding funds for a child

The need to pay money to a minor arises when the organization of the alimony provider’s employer receives a writ of execution. Funds for the child can be paid from the salary of any individual. A common point of view is that payments should be taken from the income of the father whose marriage has ended. However, today you can find more and more mothers obligated to pay alimony who are forced to pay money for a little person on an equal basis with men.

The obligation to withhold funds is established by a court decision or an agreement concluded between the former spouses. You need to calculate and transfer money in accordance with these documents. They will indicate the percentage that is supposed to be collected from the payer’s income, or the exact amount.

The collection of alimony by the employer can be initiated by the bailiff, the debt collector and the employee himself. If an accountant ignores this legal requirement, he will be subject to administrative or even criminal liability. In view of this, the financier or the employer himself is obliged to know whether child support is taxed, what is the standard procedure for calculating the payment, and how the subordinate’s income is reflected in various certificates.

https://www.youtube.com/watch?v=Mfi5tmiuk3k

Filling out certificates and declarations

2-NDFL

A certificate in form 2-NDFL is a document that reflects the income of an individual with coding of their type, the amount of accrued and withheld tax. From the document you can obtain information about the employer and personal data of the employee. It is also a source of information about tax deductions, if any.

It is important to know that if alimony is withheld from an employee, it is not reflected in the certificate in any way.

Often, parents responsible for paying child support want to reduce the amount withheld and provide false documents indicating a lower income level. This is a criminal offense and can be classified as official forgery and forgery of forms.

You can check the authenticity of a document in several ways:

- evaluate by appearance, study the features of the seal and the signature of the chief accountant;

- verify the authenticity of the information by contacting the organization where the document was drawn up, in writing, by telephone or in any other available way;

- through an official application to the Pension Fund.

Verification can also be carried out in other available ways, including through personal communication channels.

6-NDFL

Form 6-NDFL is submitted to the tax service quarterly for additional control over the level of income and accrued personal income tax. Payment of alimony is not a reason to reduce the overall tax base. That is, income tax is first withheld from the employee, and then the share of alimony.

In the certificate on form 6-NDFL, these transactions are recorded in field 2, line 130 and 140 - these are the amounts of actual income and withheld tax. That is, there is no line for entering data on alimony. This suggests that the real social payment is not indicated in the certificate in form 6-NDFL.

3-NDFL

The Tax Code states that alimony is a category of payments that is not subject to income tax.

Consequently, the recipient of alimony, when filling out a declaration in Form 3-NDFL, does not indicate this type of payment as income. In fact, personal income tax is collected from them by the payer, because alimony is withheld at the place of work only after deducting the income contribution. Tags: accountant, job description of the general director, capital, tax, personal income tax, order, expense, means