Definition of special equipment objects

Special equipment in accounting is a term that combines concepts such as special-purpose equipment, fixtures, and tools.

Accounting for special equipment is determined by the Methodological Guidelines for the accounting of special tools, special devices, special equipment and special clothing (hereinafter referred to as Guidelines No. 135n), which were approved by a separate order of the Ministry of Finance dated December 26, 2002 No. 135n. In paragraphs 1–9 of this document describe in detail what is meant by the concepts of special equipment, special devices and special tools, and examples are given. The main features of special equipment are as follows: firstly, it is a means of labor, and secondly, it is used to perform individual operations that go beyond the scope of standard or standard production. In other words, special assets are contrasted with fixed assets that are constantly used to manufacture standard products.

Depending on the specifics of production, the company must specify in its accounting policy which items should be classified as special equipment.

IMPORTANT! Starting from 2021, the procedure for accounting for inventories, including special equipment, changes significantly. Everyone will have to keep records according to the new standard - FSBU 5/2019 “Inventories”. Recommendations from ConsultantPlus experts will help you prepare for the transition to the new rules. Get trial access to the system for free and proceed to the material.

What is special equipment

Special equipment requires the presence of different categories of objects:

- Tools with special purpose devices.

- Special type of equipment.

- Workwear.

In the first case, we are talking about technical assets that are endowed with a unique set of characteristics. Their purpose is to provide the ability to produce specific products or provide certain types of services. The category of special devices and tools includes molds for pressing and stamps, molds, variants of model equipment and stocks. These include rolling rolls and chill molds.

ATTENTION! Assets that are used for the manufacture of template products (standard varieties of products) cannot be taken into account along with special devices.

Equipment differs from tools and devices in the ability to use them as tools of labor on a repeated basis and in the fact that this type of special equipment is needed to implement non-standard operations in the technological cycle. The special equipment group reflects the movement of technological assets for working with chemical elements, objects used for metalworking, heat treatment, welding and forging type equipment. Special equipment also includes equipment for implementing control measures and tests, stands and mock-ups of future finished products, and control panels. Separate types of this type of special equipment are reactor and decontamination types of equipment.

Overalls are necessary to ensure the safety of personnel during the work process. It is represented by a set of personal protective equipment. The kit may include:

- clothing items (jackets with robes, sheepskin coats or sheepskin coats, trousers, mittens);

- shoes with a special protective coating or increased strength properties;

- safety devices in the form of glasses, helmets, respirators and gas masks.

The enterprise's accounting policy must contain information about the list of objects that will be shown in accounting as part of special equipment.

NOTE! The main distinguishing feature of special equipment is the presence of unique characteristics that provide the ability to carry out non-standard operations and produce non-standard products.

Accounting for receipt and write-off of special equipment objects

Special equipment is acquired by the organization at its actual cost when transferring property rights to it and in case of independent production. The company has the right to choose the method of accounting and writing off the cost of the special equipment item as expenses. One of the main selection criteria is the service life of specific equipment.

Option 1. Service life of special equipment is more than 12 months

Guidelines No. 135n provide a choice of 2 accounting methods indicated below:

1. Accounting is maintained as required by PBU 6/01 “Accounting for fixed assets”, approved by Order of the Ministry of Finance dated March 30, 2001 No. 26n.

If the cost of special equipment is less than 40,000 rubles, then the enterprise’s accounting department has the right to take it into account as inventories (clause 5 of PBU 6/01), and it can be written off as costs at a time when it is put into production.

If the cost exceeds 40,000 rubles, then the special equipment is recognized as a fixed asset.

Fixed assets are written off as expenses using the institution of depreciation over their useful life.

For details on methods of depreciation of fixed assets, read the article “Rules for calculating depreciation of non-current assets.”

2. The accounting department should reflect the objects of special assets as a debit to the 10th account “Materials”, the subaccount “Special equipment and clothing in the warehouse” in correspondence with accounts 60 “Settlements with suppliers and contractors”, 71 “Settlements with accountable persons”, 76 “Settlements with different debtors and creditors." In case of independent production, the costs accumulated on accounts 20 “Main production” or 23 “Auxiliary production” will need to be transferred to the 10th account using the subaccount “Special equipment and clothing in the warehouse”. Moreover, this is done even when the equipment item bypasses the warehouse and is sent directly to production (clause 17 of Guidelines No. 135n).

Methodological guidelines establish the need for analytical accounting. In circumstances where a special asset is transferred to production immediately from a warehouse, it is necessary to reflect this operation on the following sub-accounts:

- Dt 10 subaccount “Special equipment and protective clothing in operation” Kt 10 subaccount “Special equipment and protective clothing in the warehouse”.

Companies are also allowed to keep such records off the balance sheet. This is done for the convenience of monitoring safety in circumstances when the special asset is completely written off for production.

There are 3 ways to write this off:

- in direct proportion to the volume of products produced (work performed or services rendered);

- linearly (based on the provisions of clause 24 of Methodological Instructions No. 135n);

- repayment in full at the time of transfer to production (based on the provisions of clause 25 of Methodological Instructions No. 135n).

The cost of special assets is written off by debiting the production cost accounts and crediting account 10 “Materials”, subaccount “Special equipment and clothing in use”.

Example:

The company purchased welding equipment for a special limited edition of garden fences. The cost of the welding machine is 78,000 rubles; the amount includes 18% VAT. It is planned to use this device for 15 months. The accounting policy states that such equipment is accounted for as part of inventories, and the linear method is used for write-off.

Despite the fact that the time of use of special equipment will exceed a year, and the cost is more than 40,000 rubles, it can be taken into account in current assets. The purchase transaction is reflected as follows:

Dt 10 subaccount “Special equipment and clothing in the warehouse” Kt 60 - 66,102 rub.

Incoming VAT reflected:

Dt 19 Kt 60 — 11,898 rub.

The special equipment has been transferred to production:

Dt 10 subaccount “Special equipment and special clothing in operation” Kt 10 subaccount “Special equipment and special clothing in the warehouse” - 66,102 rubles.

The monthly write-off amount for 15 months will be 66,102 / 15 = 4,407 rubles.

Special equipment was written off as expenses in the 1st month of operation:

Dt 20 Kt 10 subaccount “Special equipment and protective clothing in operation” - 4,407 rubles.

Important! Recommendation from ConsultantPlus Write off damaged goods, materials and other valuables that have become unusable, as well as shortages of these valuables, from inventory accounts. Debit their cost...(for more details, see K+).

Option 2. Service life of special equipment is less than 12 months

Accounting is carried out only with the help of Methodological Instructions No. 135n, as discussed in paragraph 1 of this article.

Example:

A ceramics factory has purchased molds for casting that will be used to produce a holiday batch of flower pots. Purchase cost 280,000 rubles. without VAT. It is planned to produce 7,000 pieces. pots in 5 months. The accounting policy states that such devices are taken into account as part of the inventory, and costs are charged in proportion to the volume of production.

Despite the fact that the service life of this special asset is less than 12 months, it should still be written off not at a time, like ordinary inventories, but proportionally. This helps to evenly reflect the cost of production across months, without sudden jumps due to one-time write-offs.

In the 1st month, 1,500 units were produced, in the 2nd - 1,000 units, in the 3rd - 1,700 units, in the 4th - 1,800 units, in the 5th - 1,000 units .

The purchase is reflected by the following entry:

Dt 10 subaccount “Special equipment and clothing in the warehouse” Kt 60 - 280,000 rub.

Special equipment is transferred to production:

Dt 10 subaccount “Special equipment and special clothing in operation” Kt 10 subaccount “Special equipment and special clothing in warehouse” - 280,000 rubles.

The write-off amount in the 1st month will be 280,000 / 7,000 × 1,500 = 60,000 rubles.

The write-off amount in the 2nd month will be 280,000 / 7,000 × 1,000 = 40,000 rubles.

The write-off amount in the 3rd month will be 280,000 / 7,000 × 1,700 = 68,000 rubles.

The write-off amount in the 4th month will be 280,000 / 7,000 × 1,800 = 72,000 rubles.

The write-off amount in the 5th month will be 280,000 / 7,000 × 1,000 = 40,000 rubles.

Special equipment is written off as expenses each month of operation by wiring:

Dt 20 Kt 10 subaccount “Special equipment and clothing in operation.”

Summarize. The table below lists all possible ways to account for special equipment and the cases in which they are applicable.

| Accounting method | Conditions of use |

| The method is available for any equipment and for all cases. |

| The method is available for any equipment and for all cases. |

| The method is available when the useful life of special equipment exceeds 12 months. |

| The method is available if the useful life of the special equipment exceeds 12 months and if its cost does not exceed 40,000 rubles. It is allowed to establish a different value threshold in the accounting policy, but in any case it should not exceed 40,000 rubles. |

Account, typical transactions

Special equipment classified as MPZ must be taken into account in the 10th count. To debit its value to this active account, you must have proof of ownership of a specific asset.

IMPORTANT! For a special object, it is necessary to accurately determine the actual cost and create a separate sub-account 10.10. This subaccount is used for capitalization in places designated for storage of received special equipment and devices.

The receipt of new assets is reflected in debit turnover, disposal into production or for other reasons is recorded in credit movement. Typical wiring when producing a special asset on your own at a subsidiary workshop:

- material costs incurred are taken into account in D23 and K10 ;

- the accrued earnings of the workers involved in the process are accumulated in expenses using postings D23 - K70 with the simultaneous reflection of insurance contributions under D23 and K69 ;

- the cost of the future product includes depreciation charges for equipment and other fixed assets that were used in the production of asset D23 - K02 ;

- D10.10 - K23 with this correspondence, the entire generated cost price is shown as the cost of special equipment, which is recognized as a finished product and accepted for accounting.

In order to transfer special equipment to the production workshop according to accounting data, it is necessary to create another subaccount 10.11. It will accumulate cost estimates of special assets in operation. The fact of transfer is confirmed by wiring between D10.11 and K10.10 . In case of a one-time write-off of the cost of an object as expenses, the amount is withdrawn from K10.11 and credited to the debit of the expense account. If the residual value of an asset is written off, then D91.2 . When purchasing special equipment from third-party organizations, it is recorded as D10.10 - K60 with the simultaneous allocation of VAT D19 - K60 .

Additionally, you can enter a subaccount for the 10th account for workwear into the working chart of accounts. When a special asset is recognized as a fixed asset, its accounting is kept not on account 10, but on account 01.

Results

Thus, depending on the choice of the organization, on its features and specifics, special equipment can be accounted for as ordinary materials and written off at a time when released into production, or it can be written off evenly as fixed assets or materials.

The accounting policy must describe in detail how the organization reflects special equipment, in accordance with which regulations.

It is worth noting that for different types of special assets, different methods of non-lump sum write-off are possible. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Transfer of special clothing into service

In order to ensure the safety of workwear in operation, it is necessary to organize its accounting on the off-balance sheet account MTs.02 “Workwear in operation” (clause 8 of FSBU 5/2019, Chart of Accounts 1C).

The method for assessing materials (including workwear) upon disposal is established by the organization independently in its accounting policies according to (clause 36 of FSBU 5/2019) and (clause 8 of Article 254 of the Tax Code of the Russian Federation) by selecting it from the following methods:

- at average cost;

- using the FIFO method;

- at the cost of each unit (not automated in 1C).

To automate the write-off of the cost of workwear, the 1C accounting policy (Main - Settings - Accounting Policy) establishes a unified method for valuing materials in accounting and NU and, therefore, this method must be fixed in the accounting policy for accounting and NU.

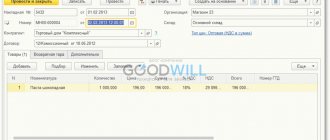

Issue the workwear with the document Transfer of materials into operation on the basis of Receipt (act, invoice, UPD) (or in the section Warehouse - Transfer of materials into operation).

Workwear tab with the donated workwear:

- An individual is an employee who has received special clothing.

In our example, the costs of purchasing and using workwear are taken into account as part of the direct costs of production.

- The method of reflecting expenses is the method of accounting for the costs of purchasing workwear, selected from the directory. The method of reflecting expenses: Cost account - 20.01 “Main production”;

- Cost items - the cost item for which expenses will be accumulated. Selected from the directory Cost items, Type of expense - Material costs .

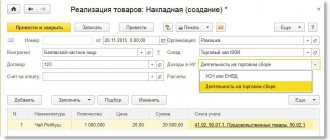

Postings according to the document

The document generates transactions:

- Dt 20.01 Dt 10.10 - special clothing was put into operation;

- MC.02 - the cost of workwear in operation is reflected off the balance sheet.

Documenting

The organization must approve the forms of primary documents, including those for the transfer of workwear into operation. In 1C, the Record Sheet for the Issue of Workwear (MB-7) is used.

The form can be printed by clicking the Print button - Issuance record sheet (MB-7) of the document Transfer of materials into operation . PDF

See also:

- Receipt of workwear and its transfer into operation

- Accounting for workwear in 1C 8.3: step-by-step instructions

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- Receipt of workwear and its transfer into operation until 2021. Accounting for workwear in 1C 8.3 is fully automated. Let's take a closer look at each...

- Test No. 25. Write-off of materials for general business needs...

- Test No. 39. Write-off (transfer into operation) of business equipment as part of distribution costs...

- Transport and procurement costs when purchasing materials: legislation and 1C You need to think about accounting for transport and procurement costs (TPC) at the stage...