Payment of personal income tax for individual entrepreneurs using the simplified tax system without employees

Does individual entrepreneur pay personal income tax using the simplified tax system? If an individual entrepreneur receives funds from those types of activities that are reflected in the Unified State Register of Individual Entrepreneurs, he does not pay this tax to the budget, since the application of the simplified tax system implies an exemption from personal income tax on income received from business activities (with the exception of income from dividends and income subject to personal income tax under rates 35 and 9%). Basis - clause 3 of Art. 346.11 Tax Code of the Russian Federation.

If an individual entrepreneur receives income not related to business activities, his income is taxed at a rate of 13% in the same way as the income of any individual. At the same time, an individual entrepreneur can reduce his income by using the right to a tax deduction.

If an individual entrepreneur on the simplified tax system does not use hired workers in his activities, then the personal income tax of the tax agent is not paid to him

Personal income tax and insurance premiums for individual entrepreneurs and employees

The individual entrepreneur with a patent additionally pays taxes and insurance contributions for employees:

| Mandatory payments for employees | Bid | Peculiarities |

| Personal income tax | 13% | For all labor income of tax residents and persons equivalent to them, for the income of non-residents - 30% |

| Contributions to the Pension Fund | 22% | Until the maximum income is reached (in 2021 - 1,292 thousand rubles), if it is exceeded - 10% |

| Contributions to the Compulsory Medical Insurance Fund | 5,1% | Not paid for foreigners required to register in the voluntary health insurance system |

| Contributions to the Social Insurance Fund for temporary disability and maternity | 2,9% | Until the maximum income is reached (in 2021 - 912 thousand rubles), if it is exceeded - 0%. For those temporarily staying in Russia, rates of 1.8 and 0% are applied, respectively. |

| Contributions to the Social Insurance Fund for injuries | 0,2-8,5% | The rate is set taking into account the type of activity. Accrued on all income. |

We recommend reading: What kind of reporting does an individual entrepreneur submit to the tax authorities and funds: types, rules, dates and deadlines.

When do you need to pay personal income tax for individual entrepreneurs using the simplified tax system?

An individual entrepreneur using the simplified tax system is required to pay personal income tax if he receives:

- Prizes from participation in a promotion carried out by product manufacturers or commercial enterprises. The accrual condition is winnings over 4 thousand rubles (clause 2 of article 224 and clause 28 of article 217 of the Tax Code of the Russian Federation).

- Material benefits from interest savings. The income on which tax will be paid is calculated based on the difference of 2/3 of the refinancing rate and the amount of interest specified in the agreement. If the loan is received in foreign currency, income is calculated based on 9% per annum minus the interest specified in the agreement (clause 2 of Article 212, 224 of the Tax Code of the Russian Federation).

- Interest on deposits in rubles and foreign currency. For interest received in rubles, non-taxable income will be calculated based on the refinancing rate of the Central Bank of the Russian Federation + 5%. If interest is received in foreign currency, non-taxable income is calculated based on 9% per annum (Article 224 of the Tax Code of the Russian Federation).

- Dividends from activities in third-party organizations (Article 275 of the Tax Code of the Russian Federation).

- Income not related to business activities: gifts, lottery winnings, from the sale of one’s own property, royalties, income from which the tax agent did not withhold tax (Article 228 of the Tax Code of the Russian Federation).

When hiring employees or attracting individuals under civil contracts, the individual entrepreneur is obliged to transfer personal income tax to the budget from the employees’ earnings as a tax agent (clause 6 of article 226 of the Tax Code of the Russian Federation).

KBK personal income tax in 2021 for employees

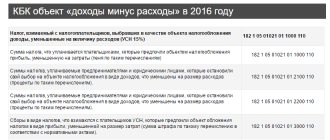

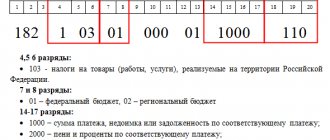

The budget classification code consists of twelve characters, which are combined into certain groups:

- Signs 1-3 indicate the income administrator code. Personal income tax is administered by the tax authorities. The code for them is 182.

- Characters 4-13 – code of the type of income. Personal income tax is classified in group 100 (tax and non-tax revenues). Group 101 includes taxes on profits and income.

- Characters 14-17 – income subtype code.

The latter is classified into the following subspecies:

- 1000 – payment amount. This includes recalculations, debts on the corresponding payment, and arrears.

- 2000 – penalties and interest on the corresponding payment.

- 3000 – the amount of monetary penalties (fines) for payment in accordance with the legislation of the Russian Federation.

Characters 18-20 indicate the code of the general government sector operations classifier. Tax income corresponds to code 101.

According to established legislation, personal income tax in 2021 must be paid no later than the day following the day the employee is paid income. For example, an employer paid an employee wages for January on February 9. But the date of receipt of income will be considered January 31. And the tax withholding date is February 9. Personal income tax must be transferred the next day, that is, January 10th. If this day falls on a day off, calculations must be made on the first working day after the day off.

KBK personal income tax for employees in 2021: 182 1 0100 110

If you specify an incorrect budget classification code, funds will be transferred to the wrong account. Accordingly, the taxpayer will be in arrears in paying the mandatory income tax. Tax authorities, as a result of identifying this violation, issue fines and penalties. They are also assigned specific budget classification codes.

Methods of paying personal income tax by individual entrepreneurs

Individual entrepreneurs on OSNO must necessarily pay personal income tax on the income received.

Step-by-step instructions for calculating and paying personal income tax by entrepreneurs on OSNO were developed by ConsultantPlus experts. Get a free trial access to K+ and watch the action guide.

Personal income tax must be paid in two ways:

- Advance payments, which from 2021 are calculated in a new way: from actually received (and not planned, as before) income and are transferred within the following terms:

- until April 25 - for the 1st quarter (until 04/27/2020 - taking into account the transfer from the weekend). Due to non-working days from March 30 to May 11, 2020, the deadline for paying the advance payment has been postponed;

- before July 25 - six months (until July 27, 2020);

- until October 25 - for the 3rd quarter (until October 26, 2020).

- After submitting the declaration to the Federal Tax Service, you must either pay additional tax or return the overpaid funds from the budget (offset for the future).

If the advance payment was transferred with a delay, penalties will be charged for the debt that arose for this reason (Article 75 of the Tax Code of the Russian Federation).

Tax adjustment and transfer

After calculating personal income tax and generating a declaration, you must either pay extra or return the tax from the budget (offset).

IMPORTANT! Starting from 2021, individual entrepreneurs do not submit a declaration in form 4-NDFL. Read about the presentation of 4-NDFL here.

At the end of the year, individual entrepreneurs submit a 3-NDFL declaration to their Federal Tax Service by April 30. Due to the introduction of a non-working days regime from March 30 to April 30, 2021, the deadline for submitting 3-NDFL for 2021 has been extended until 07/30/2020 (see Government Decree No. 409 dated 04/02/2020).

Read about filling out an individual entrepreneur's tax return here.

As for the individual entrepreneur who hires employees, he is an agent and must deduct tax from their salaries. The timing of tax payment depends on the type of income paid. Personal income tax from sick leave and vacation pay is transferred no later than the last day of the month in which they are paid, from wages and bonuses - no later than the day following the day of their payment (Clause 6 of Article 226 of the Tax Code of the Russian Federation).

We also draw your attention to the fact that individual entrepreneurs have the opportunity to use the right to deductions in relation to income that is subject to personal income tax at a rate of 13% (clause 3 of Article 210 of the Tax Code of the Russian Federation):

- standard (Article 218 of the Tax Code of the Russian Federation);

- social (Article 219 of the Tax Code of the Russian Federation);

- investment (Article 219.1 of the Tax Code of the Russian Federation);

- property (Article 220 of the Tax Code of the Russian Federation), except for deductions related to the sale of real estate and/or vehicles that were used in business activities (subclause 4, paragraph 2, Article 220 of the Tax Code of the Russian Federation);

- professional tax deductions (Article 221 of the Tax Code of the Russian Federation);

- in the form of losses from transactions with securities and transactions with financial instruments of futures transactions carried forward to the future (Article 220.1 of the Tax Code of the Russian Federation);

- in the form of losses from participation in an investment partnership as a result of their transfer to future periods (Article 220.2 of the Tax Code of the Russian Federation).

From dividends

Special attention is paid to the payment of fees on foreign profits from transactions with securities. In this case, the payer calculates and transfers tax funds from the interest portion of the profit. To pay the fee from this money, the appropriate BCC is used. Personal income tax on dividends in 2021 is calculated at the standard rate of 13%. But if the payer is registered with the tax authorities not in Russia, but makes a profit here, then the collection on the money received is calculated at a 15% rate.

Table 5. Transfer of tax funds from dividends.

| Payment name | Encodings |

| Standard | 18210102050011000110 |

| Penalty | 18210102050012100110 |

| Fines | 18210102050013000110 |

Do individual entrepreneurs pay personal income tax while on UTII, PSN and Unified Agricultural Tax?

Payment by an entrepreneur of UTII exempts him from paying personal income tax only in relation to income received from activities subject to UTII (clause 4 of Article 346.26 of the Tax Code of the Russian Federation).

If the “imputed” person receives income from activities for which the entrepreneur is not registered as a UTII payer, then personal income tax is paid on such income.

An individual entrepreneur using the patent system does not pay personal income tax on income from those types of activities for which a patent has been obtained. If in his activities he uses those types of activities that do not fall under the PSN, he must pay personal income tax on income from these types of activities and submit a 3-NDFL declaration to the tax authorities.

Individual entrepreneurs who are agricultural producers and pay the unified agricultural tax are exempt from personal income tax in terms of income received from business activities (clause 3 of article 346.1 of the Tax Code of the Russian Federation). However, there is an exception for certain income. Thus, an individual entrepreneur on the Unified Agricultural Tax pays personal income tax on income from dividends and income subject to personal income tax at a rate of 35 and 9%.

If an individual entrepreneur on UTII, Unified National Social Economy or PSN uses the labor of employees in his activities, he has the obligation to withhold tax from their wages. It is paid at the place of registration of the individual entrepreneur. Before April 1 of the next year, it is necessary to submit information to the Federal Tax Service on income paid to employees and withheld tax in Form 2 of Personal Income Tax, and quarterly reporting in Form 6-NDFL.

Does the individual entrepreneur pay taxes for employees?

Yes, in most cases, individual entrepreneurs pay taxes for their employees. After registering as an individual entrepreneur, he is obliged to register with the Pension Fund and the Social Insurance Fund, and thus declare himself as a tax agent for his subordinates.

According to current legislation, an employee is not required to independently fill out a tax return and make contributions to extra-budgetary funds if his work is hired. These functions are assumed by the employer.

Thus, all funds contributed by an individual entrepreneur for his employees consist of two points:

- Income tax – 13%. The entrepreneur takes this amount not from his own pocket, but from the accrued salary of his employee. In fact, the employee pays, the employer only transfers the salary tax to the budget for him. Not all income is subject to personal income tax - the exceptions are pensions, maternity payments, and severance pay. The employer must transfer the withheld tax amount to the treasury on the day of payroll or the next day.

- Insurance contributions – 30% of the employee’s accrued salary . The employer takes this amount from his own funds, thus increasing his personnel costs. Starting from 2021, reporting on insurance premiums for employees is submitted to the tax service.

Results

If an individual entrepreneur pays income to employees or attracts individuals under civil contracts, then, regardless of the taxation system applied, he performs the duties of a tax agent, which means he is obliged to withhold and pay personal income tax on income paid, submit reports in form 2-NDFL and 6 -NDFL.

Under OSNO, the income of individual entrepreneurs is subject to personal income tax, and the obligation arises to pay advance payments and submit a 3-personal income tax declaration.

When applying special regimes, individual entrepreneurs are exempt from paying personal income tax on income received from business activities. But it is important to take into account that in the application of one or another special regime there are nuances and exceptions in which the payment of personal income tax becomes mandatory.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.