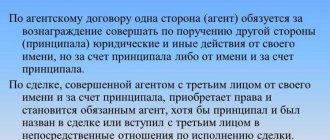

Intermediary remuneration

Regardless of the nature of the order given by the customer, the intermediary is entitled to a reward for its execution. Under agency and commission agreements, payment of remuneration is mandatory (Articles 991, 1006 of the Civil Code of the Russian Federation). Under an agency agreement, remuneration may not be paid only if this is expressly provided for in the agreement (Clause 1, Article 972 of the Civil Code of the Russian Federation).

In practice, the intermediary's remuneration may be determined by:

- as a fixed amount fixed in the contract;

- as a percentage of the transaction amount;

- as the difference between the price of goods (work, services) at which they were sold to customers and the price of goods (work, services) at which they were transferred to commission (if under the contract the intermediary is entrusted with the sale of goods (work, services) of the customer);

- as the difference between the amount received from the customer for the execution of the order and the amount paid to the supplier (if, under the contract, the intermediary is entrusted with the purchase of goods (works, services) for the customer).

VAT on commission fees

The commission agreement is considered one of the most effective tools for tax optimization, and therefore it has become widely used in the modern financial and economic environment.

The terms of the commission agreement allow one of the parties to transfer their own goods or funds for a long period, thereby reducing the size of their own assets. The other party undertakes to sell these goods (or make a purchase with the money received) for a fee, and the assets received are not recognized as income.

The conditions and procedure for commission trading are described by the Civil Code of the Russian Federation and the Rules of commission trading approved by the Government of the Russian Federation.

Commission trading is understood as a type of business activity in which one party purchases or sells goods for another party, receiving monetary compensation for these services. For convenience in describing this procedure, the following terms are used:

- principal - a person (organization or individual entrepreneur) who gives an order to complete a transaction and transfers his own funds to another person for this purpose;

- commission agent - a person who acts as an intermediary in trade relations between the principal and a third party in the purchase or sale of any goods on the instructions of the principal and for a fee.

All conditions of such transactions are carried out on the basis of a commission agreement concluded between the principal and the commission agent. The agreement describes:

- Subject of the contract (what exactly needs to be bought or sold).

- In what time frame must the consignor receive (ship) the goods?

- What amount of remuneration will the commission agent receive for his services?

The contract also provides for the conditions under which the goods may be returned or not sold (not purchased), in connection with which the commission agent may incur costs for its storage.

The contractual amount of the commission can be specified either as a fixed amount or calculated as a percentage of the transaction amount.

Most often, a commission agreement is concluded for the purpose of selling the principal's goods by the commission agent. In this case, the ownership of the goods that the commission agent received to carry out the transaction belongs to the principal.

When transferring goods from the principal to the commission agent, in the principal's accounting, the goods are reflected as part of the own assets and are accounted for in account 45 “Goods shipped”. The fact of transfer of goods to the commission agent must be reflected by posting Dt 45 Kt 41.

Let's imagine that a commission agreement has been concluded between Globus and Globus, where Status is the principal and Globus is the commission agent.

Under the agreement, Globus receives an order from Status to sell office supplies at a cost of 20,000 rubles. Sale price - 32,100 rubles, VAT 4,896 rubles. On May 1, 2015, the buyer transferred funds in advance.

| Dt | CT | Description | Sum | Base |

| 45 | 41 | “Status” transferred stationery to “Globus” for sale | 20,000 rub. | waybill, acceptance certificate |

| 76-"Globe" | 62 | Globus announced the receipt of 100% advance payment for the goods | RUB 27,204 | payment order received from Globus |

| 76-"Globe" | 68 | VAT on prepayment (18%) | RUB 4,896 | payment order received from Globus |

The principal takes into account the amount of commission to the intermediary in account 44 “Sales expenses”. This includes not only remuneration, but also possible expenses of the commission agent incurred in connection with the storage and sale of goods.

All payments to the intermediary are made according to the commission agent's report.

This document contains a calculation and detailed description of the expenses incurred, supported by documents, and is subject to mandatory approval by the principal.

| Dt | CT | Description | Sum | Base |

| 76 | 51 | "Jupiter" transferred funds to "Venera" for the purchase of printing materials | RUB 45,600 | Bank statement |

| 41 | 76 | LLC "Venera" purchased the goods and transferred them to LLC "Jupiter" | RUB 38,664 | waybill, acceptance certificate |

| 19 | 76 | VAT reflected 18% (of the cost of the goods) | RUB 6,956 | waybill, acceptance certificate |

| 41 | 76 | The commission amount is included in the cost of the goods received (excluding VAT) | RUB 4,638 | waybill, acceptance certificate |

| 19 | 76 | VAT reflected 18% (of the commission amount) | 834 rub. | waybill, acceptance certificate |

| 68 | 19 | The VAT amount is accepted for deduction | RUB 7,790 | waybill, acceptance certificate |

| 76 | 51 | Jupiter LLC paid Venera LLC a commission | RUB 5,472 | commission agent's report |

Transactions made using a commission agreement are quite common, as they are a convenient and mutually beneficial way of conducting business transactions for both parties - the principal and the commission agent.

Intermediary services in Russia are recognized as subject to VAT at a standard rate of 18%. The commission agent's fee is considered his income from ordinary activities. The commission agent's profit is calculated as the difference between the amount of the fee under the commission agreement minus VAT and the costs of selling the tenant's property.

VAT will not be charged on the commission agent’s income if his earnings consist of tax-free activities:

- folk art products crafts with recognized value (except for excisable goods);

- ritual services and funeral items (according to a closed list);

- medicines (the list is closed);

- leasing space to foreigners and foreign companies that have been accredited in the Russian Federation.

The taxable base for VAT is the difference between the money received as a fee under a commission agreement and the costs of its implementation. All money accepted from the employer and used in the transaction is not included either in the expenses or in the income of the commission agent.

When a commission agent sells the property of a principal, he draws up an invoice for the customer on his own behalf within 5 days, then informs the principal of his details and accepts an invoice from him with the same data. An accepted invoice is subject to registration in Part 2 of the register of received and issued invoices and is not recorded in the purchase book.

Payment of remuneration

Regardless of the nature of the order, the intermediary may or may not participate in settlements with counterparties.

If the intermediary is involved in settlements, he can independently withhold the amount of his remuneration:

- from revenue received from customers (if the subject of the contract is the sale of goods (works, services) of the customer);

- from funds received from the customer (if the subject of the contract is the purchase of goods (works, services) for the customer).

If the intermediary does not participate in the settlements, the customer transfers the remuneration for the execution of the order to him. The size, conditions and procedure for payment of intermediary remuneration must be specified in the contract.

This follows from the provisions of Articles 410, 972, 997, 1011 of the Civil Code of the Russian Federation.

Typical mistakes in commission agent accounting

Error No. 1. Accounting for money received from the principal for the commission agent to perform his duties in the income of the commission agent's enterprise. Accounting for money spent by the commission agent under the commission agreement, compensated by the principal, among the expenses of the commission agent's company.

Funds compensated by the principal are taken into account exclusively in the accounting of the principal, not the commission agent.

Mistake #2. Failure to reflect in the accounting entries of the commission agent the fact of payment by the buyer for the principal's property, when the commission agent performs the functions of an intermediary, but does not participate in the calculations.

D 62 K 76;

D 76 K 62.

Mistake #3. Absence in the commission agent's accounting department of a register of invoices issued for the principals in order to request the fee due for the work for the fulfillment of the intermediary's obligations under the commission agreement.

From January 1, 2015 The law establishes the obligation of the commission agent to make notes in the register of invoices sent to the employer to receive a fee in order to simplify the tax service’s procedure for assessing VAT on the commission agent’s funds.

Accounting

For an intermediary, the remuneration paid by the customer is revenue from the sale of intermediary services (clause 5 of PBU 9/99). The remuneration is recognized as income from ordinary activities, which is reflected in accounting on the date of approval by the customer of the intermediary’s report (clause 5, 12 of PBU 9/99).

For organizations that have the right to conduct accounting in a simplified form, a special procedure for accounting for income is provided (Parts 4, 5, Article 6 of the Law of December 6, 2011 No. 402-FZ).

In accounting, reflect settlements with the customer on account 76 “Settlements with various debtors and creditors”, to which it is advisable to open sub-accounts:

- “Settlements with the customer for sold goods (work, services)” (if the subject of the contract is the sale of goods (work, services) belonging to the customer);

- “Settlements with the customer for purchased goods (work, services)” (if the subject of the agreement is the acquisition of goods (work, services) required by the customer);

- “Settlements with the customer for reimbursement of expenses”;

- "Settlements with the customer for remuneration."

In the accounting of the intermediary, the remuneration due under the contract is reflected by transactions (excluding VAT transactions):

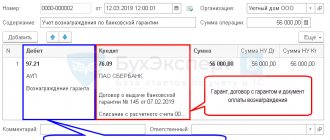

Debit 76 subaccount “Settlements with the customer for remuneration” Credit 90-1 - reflects the amount of remuneration for intermediary services (based on the agreement and the intermediary’s report);

Debit 76 subaccount “Settlements with the customer for sold goods (works, services)” Credit 76 subaccount “Settlements with the customer for remuneration” - intermediary remuneration is withheld from the proceeds received in payment for sold goods (works, services) of the customer (if the intermediary is involved in the settlements );

Debit 76 subaccount “Settlements with the customer for purchased goods (works, services)” Credit 76 subaccount “Settlements with the customer for remuneration” - intermediary remuneration is withheld from funds received from the customer for the purchase of goods (works, services) (if the intermediary is involved in the settlements );

Debit 51 (50) Credit 76 subaccount “Settlements with the customer for remuneration” - remuneration has been received for the performance of intermediary services (if the intermediary does not participate in the settlements).

Sales by a commission agent of the principal's goods

Costs for the sale of goods of the principal are not considered as expenses of the intermediary and are reflected only in the accounting of the intermediary. Transactions can be carried out with or without the participation of the commission agent in the calculations.

| The commission agent participates in settlements | The commission agent does not participate in settlements |

| 1. Money for the sold goods goes to the intermediary’s cash desk or to his current account; | 1. Funds from the buyer are transferred directly to the principal’s account; |

| 2. From this money, the commission agent retains a fee, the amount of which should not exceed the amount promised by the employer; | 2. When the principal receives the proceeds, he pays the commission agent his remuneration for the work done. |

| 3. The remaining funds are sent to the account of the consignor, the owner of the items sold. | |

| Postings: – D 004 (tenant’s property is included in the balance sheet) – D 51(50) K 62 (proceeds from the sale of entrusted property are taken into account) – D 62 K 76 sub. “Settlements with the principal” (sale of his property by an intermediary) – K 004 (goods delivered to the buyer) – D 76 K 51 (costs of the commission agent are reimbursed) – D 76 Sat. “Settlements with the principal” K 76 (debt of the employer for the costs of the intermediary) – D 76 Sat. “Settlements with the principal” K 90 (intermediation fee accepted) – D 90 K 68 (VAT is calculated from its amount) – D 76 Sat. “Settlements with the principal” K 51 (the principal receives money from sales minus the intermediary’s remuneration and the amount of reimbursement of his expenses) | Postings: – D 76 K 51 (payment of commission agent’s expenses from the employer’s money) – D 76 Sat. “Settlements with the principal” K 76 (the debt of the principal for expenses is indicated) – D 76 Sat. “Settlements with the principal” K 90 (remuneration for intermediary services accepted) – D 90 K 68 (VAT is determined on its amount) – D 51 K 76 sub. “Settlements with the principal” (remuneration and compensation for losses are transferred to the account) |

| ★ Best-selling book “Accounting from Scratch” for dummies (understand how to do accounting in 72 hours) purchased by {amp}gt; 8000 books |

BASIC

When calculating income tax, the intermediary includes intermediary remuneration in income as revenue from the sale of intermediary services (clause 1 of Article 249 of the Tax Code of the Russian Federation). The moment at which an intermediary’s income is recognized depends on the method of tax accounting chosen by the intermediary. For more information about this, see How to take into account income and expenses from intermediary operations for income tax purposes.

The intermediary must charge VAT on the amount of his remuneration and on any other income received during the execution of the contract (for example, from additional benefits) (clause 1 of Article 156 of the Tax Code of the Russian Federation). The exception is remuneration received for intermediary services for the sale of goods (work, services) specified in paragraph 1, subparagraphs 1 and 8 of paragraph 2 and subparagraph 6 of paragraph 3 of Article 149 of the Tax Code of the Russian Federation (clause 2 of Article 156 of the Tax Code of the Russian Federation). For more information, see How to calculate VAT on intermediary transactions.

The intermediary must issue an invoice to the customer for the amount of remuneration (clause 3 of Article 168 of the Tax Code of the Russian Federation).

An example of how intermediary remuneration under a commission agreement is reflected in accounting and taxation. The intermediary participates in settlements, applies the general tax system and sells goods belonging to the customer. The commission is deducted from the amounts received from customers for goods sold.

On February 2, Torgovaya LLC (commission agent) sold to the buyer the goods of Alpha LLC (committee), transferred to Hermes on January 31 under a commission agreement. The selling price of goods specified in the contract is 236,000 rubles. (including VAT – 36,000 rubles). The commission is withheld by the commission agent from the amounts received from buyers and amounts to 5 percent of the sales price (RUB 11,800, including VAT - RUB 1,800). Payment from the buyer arrived at the intermediary's account on February 4. On the same day, the commission agent's report was approved by the committent. Hermes calculates income tax on a monthly accrual basis.

The Hermes accountant reflects settlements with the customer on account 76 “Settlements with various debtors and creditors” in the subaccounts: – “Settlements with the customer for goods sold”; – “Settlements with the customer for remuneration.”

The following entries were made in the accounting records of Hermes.

January 31:

Debit 004 – 236,000 rub. – goods were received for sale under a commission agreement.

February 2:

Debit 62 Credit 76 subaccount “Settlements with the customer for goods sold” – 236,000 rubles. – sales of goods to the buyer are reflected;

Loan 004 – 236,000 rub. – the goods of the principal are written off off-balance sheet.

February 4:

Debit 51 Credit 62 – 236,000 rub. – payment has been received for goods sold under a commission agreement;

Debit 76 subaccount “Settlements with the customer for remuneration” Credit 90-1 – 11,800 rubles. – the amount of commission is reflected;

Debit 90-3 Credit 68 subaccount “VAT calculations” – 1800 rubles. – VAT is charged on the commission amount;

Debit 76 subaccount “Settlements with the customer for goods sold” Credit 51 – 224,200 rub. (RUB 236,000 – RUB 11,800) – funds received from customers (less commission) were transferred to the principal;

Debit 76 subaccount “Settlements with the customer for goods sold” Credit 76 subaccount “Settlements with the customer for remuneration” - 11,800 rubles. – reflects the commission agent’s deduction of the commission amount.

When calculating income tax for February, the Hermes accountant took into account the amount of commission in the amount of 10,000 rubles as income. (RUB 11,800 – RUB 1,800).

An example of how intermediary remuneration under a commission agreement is reflected in accounting and taxation. The intermediary applies the general taxation system and, on behalf of the customer, purchases the necessary goods for him. The remuneration is received by the commission agent after the terms of the contract are fulfilled.

LLC "Torgovaya" (commission agent) purchases goods for LLC "Alpha" (committent). According to the terms of the commission agreement, the remuneration is transferred to the commission agent after he executes the transaction and amounts to 5 percent of the transaction price. On January 31, to fulfill the order, Hermes received 1,180,000 rubles from Alpha. On February 2, for this amount, the commission agent purchased goods worth 1,180,000 rubles for the principal. (including VAT – 180,000 rubles). On the same day, the goods were transferred to Alpha and the committent approved the commission agent’s report. On February 4, Alpha transferred to Hermes a commission for the execution of the transaction in the amount of 59,000 rubles. (RUB 1,180,000 × 5%), including VAT – RUB 9,000. Hermes calculates income tax using the accrual method.

The Hermes accountant reflects settlements with the customer on account 76 “Settlements with various debtors and creditors” in the following subaccounts: – “Settlements with the customer for purchased goods”; – “Settlements with the customer for remuneration.”

The following entries were made in the accounting records of Hermes.

January 31:

Debit 51 Credit 76 subaccount “Settlements with the customer for purchased goods” – 1,180,000 rubles. – funds were received from the principal for the purchase of goods.

February 2:

Debit 002 – RUB 1,180,000. – goods purchased for the principal are accepted for off-balance sheet accounting;

Debit 76 subaccount “Settlements with the customer for purchased goods” Credit 60 – 1,180,000 rubles. – the debt for purchased goods to the seller is reflected;

Debit 60 Credit 51 – 1,180,000 rub. – funds for the goods are transferred to the seller;

Loan 002 – 1,180,000 rub. – goods transferred to the principal are written off off-balance sheet;

Debit 76 subaccount “Settlements with the customer for remuneration” Credit 90-1 – 59,000 rubles. – reflects the amount of remuneration for execution of the commission agreement;

Debit 90-3 Credit 68 subaccount “VAT calculations” – 9000 rubles. – VAT is charged on the commission amount.

February 4:

Debit 51 Credit 76 subaccount “Settlements with the customer for remuneration” - 59,000 rubles. – the amount of commission was received from the principal for the execution of the commission agreement.

When calculating income tax for February, the Hermes accountant took into account the amount of commission in the amount of 50,000 rubles as income. (RUB 59,000 – RUB 9,000).

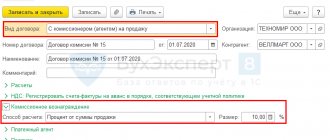

Acceptance of goods for commission in 1C 8.3

To reflect the acceptance of goods for commission, the program uses the document “Receipt: Goods, services, commission”. To create a document, go to the “Purchases” menu, submenu (link) “Receipts (acts, invoices)”. In the window with a list of documents, click the “Receipt” button. A drop-down list will open in which you need to select “Products, services, commission”. A window for creating a new document will open.

We select an organization if the program keeps records for several enterprises. We indicate the warehouse where the received goods will be stored. In the counterparty field, select the principal.

Separately, I would like to say about the “Contract” props. The fact is that the certificate for the document says that in order to indicate that the goods are accepted for commission, you need to select the type of operation “Purchase, commission”. In fact, the document does not have any type of operation. More precisely, there is, and we have already selected it - “Goods, services, commission”.

Now we need to make the program understand that this is still a commission. This is done through a contract. It is necessary to create an agreement with the counterparty of the form “With the principal (principal) for sale.” Click the down arrow in the “Agreement” field and select “Create” (or the “Show all” link and click the “Create” button in the list form). We create and insert a commission agreement. Only in this case will the document correctly reflect the operation of accepting goods for commission.

Note: There is one more condition - for commission trading it is necessary to create separate product cards with the Item Type “Products on Commission”.

We fill out the tabular part with the accepted goods. The most convenient way is to use the “Selection” button.

Here is an example of a completed document:

Now you can post the 1C document and see how it is reflected in accounting. Click the “Pass” button, then the button. A window with postings will open:

It can be seen that the goods arrived at the off-balance sheet account 004.01 - “Goods on commission (accepted to the warehouse).”

simplified tax system

Regardless of the object of taxation on which the organization pays a single tax, the amount of intermediary remuneration is included in the income that is taken into account when calculating the tax base (clause 1 of article 346.15, clause 1 of article 249 of the Tax Code of the Russian Federation).

Since intermediaries using the simplified tax system are exempt from paying VAT (except for VAT on import transactions and under simple partnership agreements, trust management of property and concession agreements), this tax is not charged on the amount of intermediary remuneration (clause 3 of Article 169 of the Tax Code of the Russian Federation).

If the intermediary cannot immediately determine the amount of his remuneration, then the entire amount of funds received from the customer must be included in income. For more information about this, see How an intermediary on the simplified tax system should take into account income and expenses for intermediary operations.

Typical accounting entries for a commission agent

The commission agent acts on the instructions of the principal and pays with his money, therefore the main accounts. The postings are reflected specifically with the employer. The intermediary essentially sells his service and receives payment for it.

When making an entry about the receipt of profit for the provision of intermediary services in the accounting. registers, cash receipts from other organizations and individuals are not recognized as income of the commission agent under commission agreements in favor of the principal.

The commission agent's expenses while working for the principal are reimbursed by the employer, which may include payments to employees, rental of premises, etc. Various costs are not recorded in several accounting entries, but are recorded as a total amount in the item of costs for the sale of property, increasing its cost.

We suggest you read: How to contact debt collectors

The property of the commission agent, which belongs to him by right of ownership, is accounted for in the accounting registers separately from the property of third-party organizations, capitalized only for the duration of the cooperation, as the property of the principal.

| Operation | DEBIT | CREDIT |

| Accounting for the principal's property | 004 “Goods accepted for commission” | 004 “Goods delivered to the customer” |

| Accounting for property purchased for the tenant | 002 “Inventory assets accepted for safekeeping” | – |

| Making a record of the fee for mediation | 76 s/ch “Settlements with the principal” | 90 “Sales” account 90-1 “Revenue” |

| Receiving payment from the buyer who purchased the consignor's goods | 51 | 76 s/ch “Settlements with buyers” |

| Indication of debt to the principal | 76 s/ch “Settlements with buyers” | 76 s/ch “Settlements with the principal” |

| Sending proceeds to the principal | 76 s/ch “Settlements with the principal” | 51 |

| Reflection of intermediary costs | 90 “Sales” account 90-2 “Cost of sales” | 44 “Sales expenses” |

| Accounting for the profit of the commission agent's company | 90 “Sales” account 90-9 “Profit/loss from sales” | 99 “Profits and losses” |

CJSC “Company” entrusted LLC “Posrednik” with property for resale. The commission agreement states that the proceeds from the sale should amount to 360 thousand rubles (including VAT - 60 thousand rubles). The cost of the property is 180 thousand rubles. LLC “Intermediary” will receive a fee for mediation of 36 thousand rubles (including VAT of 6 thousand rubles).

LLC “Posrednik” performed the work by selling the tenant’s property. Expenses under the agreement amounted to 9 thousand rubles. The agreement provides for the commission agent to deduct his fee from the proceeds for the principal's goods.

| DEBIT | CREDIT | Amount (RUB) | The essence of the operation |

| 004 | – | 360000 | Accepted property of CJSC “Company” |

| – | 004 | 360000 | The property is given to the customer |

| 76 Sat. “Settlements with customers” | 76 Sat. “Settlements with the principal” | 360000 | The customer’s debt to pay for goods and the commission agent’s debt to the employer are taken into account |

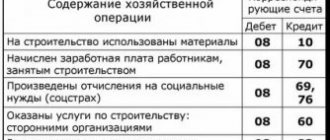

| 44 | 02(70,69…) | 6000 | Expenses under the commission agreement |

| 51 | 76 Sat. “Settlements with customers” | 360000 | Receipt of money from the customer to the account of OOO “Posrednik” |

| 76 Sat. “Settlements with the principal” | 90-1 | 36000 | Remuneration received for intermediary services |

| 90-2 | 44 | 9000 | Write-off of commission agent's expenses |

| 90-3 | 68 Sat. “VAT calculations” | 6000 | VAT on remuneration |

| 76 Sat. “Settlements with the principal” | 51 | 324000 (360000 – 36000) | Revenue sent to the principal from which payment for the work of the intermediary was withheld |

| 90-9 | 99 | 21000 (36000 – 6000 – 9000) | The profit of Posrednik LLC was calculated |

| DEBIT | CREDIT | amount (rub) | The essence of the operation |

| 004 | – | 360000 | The principal's property accepted within the framework of cooperation was capitalized |

| – | 004 | 360000 | Goods delivered to buyer |

| 44 | 02(70,69…) | 9000 | Reflection of commission agent's expenses |

| 76 Sat. “Settlements with the principal” | 90-1 | 36000 | Reflection of the fee received |

| 90-3 | 68 Sat. “VAT calculations” | 6000 | VAT on fees |

| 90-2 | 44 | 9000 | Write-off of expenses of Posrednik LLC |

| 51 | 76 Sat. “Settlements with the principal” | 36000 | Remuneration from LLC “Company” was transferred |

| 90-9 | 99 | 21000 (36000 – 6000 – 9000) | Profit of LLC “Posrednik” |

| The purchase and sale agreement with the buyer of goods is concluded by the commission agent, but the money for these goods goes directly to the principal, i.e. LLC “Intermediary” does not have the ability to monitor whether money has been received for the purchased property or not. And if no money has been received, then the principal (Company LLC) has no right to make claims against the customer, because there is no direct agreement between them. Therefore, there are several more entries made in order for the commission agent to gain control over payment for goods. | |||

| 62 | 76 | 360000 | Reflection of the customer’s debt to LLC “Company” |

| 76 | 62 | 360000 | Reflection of the repayment of the customer’s debt to LLC “Company” |

UTII

The object of UTII taxation is imputed income (clause 1 of Article 346.29 of the Tax Code of the Russian Federation). As a general rule, intermediary activities are not transferred to UTII (clause 2 of Article 346.26 of the Tax Code of the Russian Federation). The possibility of paying UTII on the amount of intermediary fees exists only when conducting retail trade and depends on the type of intermediary agreement and the conditions under which the intermediary conducts trading activities. In other cases, taxes must be paid on the amount of intermediary fees in accordance with the general or simplified taxation system.