Why do you need statistics form No. 5-Z?

The form in question is a statistical reporting document and should, based on the results of the 1st quarter, half a year and 9 months - before the 30th day of the month following the reporting period, be sent to Rosstat by all legal entities that are not SMPs, banks, insurance and other financial firms, and also those not included in the budget system.

Small businesses include companies that:

- have a staff of up to 100 people (subclause 2, clause 1.1, article 4 of the law “On the development of small and medium-sized businesses” dated July 24, 2007 No. 209-FZ);

- have revenue not exceeding RUB 800,000,000. per year (clause 1 of the Decree of the Government of the Russian Federation dated July 13, 2015 No. 702).

- have an authorized capital of which no more than 25% belongs to the state (or municipality), 49% to foreign or other legal entities that are not subjects of the SMP.

Such firms are not required to send the reporting document in question to Rosstat.

Using Form 5-Z, Rosstat is informed about the company’s expenses for the production and sale of goods, services and work. This information is reflected for the entire legal entity as a whole - the document also takes into account those figures that characterize the activities of the company’s divisions.

At the same time, Form 5-Z is submitted to Rosstat by the company, its subsidiaries, as well as organizations dependent on it, separately. Information about subsidiaries and dependent organizations is not recorded by the reporting company in the financial statements.

Form No. 5-Z, current in 2021, was approved by Rosstat order No. 320 dated July 15, 2015.

NOTE! Instructions for filling out Form 5-Z for 2021 were approved by Rosstat Order No. 65 dated February 12, 2018 and are applied taking into account additions from Order No. 63 dated February 12, 2019.

New rules for filling out statistical form No. 5-З*

Starting with reporting for the first quarter of 2010, organizations submit updated statistical form No. 5-Z “Information on the costs of production and sale of products (goods, works, services).” In February, Rosstat approved new Guidelines for its application, which also need to be applied from the first quarter of 2010. The agency took the easy path and decided not to make scrupulous amendments to the existing document, but to replace everything in one fell swoop. Let's see what has really changed.

Because of two words, the entire form was replaced

Quarterly form No. 5-Z “Information on the costs of production and sale of products (goods, works, services)” is submitted for the first quarter, half a year and 9 months no later than the 30th day after the reporting period. It is rented out by all legal entities (commercial and non-commercial, producing goods and services for sale to third parties), except for small enterprises, simplified enterprises, budgetary organizations, banks, insurance and other financial and credit organizations.

In 2009, organizations submitted Form No. 5-Z, approved by Rosstat Order No. 235 dated September 23, 2008. In 2010, it is necessary to submit Form No. 5-Z approved by Rosstat Order No. 153 dated July 28, 2009 “On approval of statistical tools for the organization Federal statistical monitoring of enterprise activities." We remind you that along with this form, forms No. 1-enterprise, No. 4-TER, No. 6-TP (hydro), No. 6-TP, No. 1-cooperative, No. 1-ХО, No. PM-prom, No. 5 have been updated -Z, No. P-5 (m), Appendix 2 to form No. P-1, No. 1-IP (months).

When you look at the old and new forms No. 5-Z, you remember a child’s game like “find seven differences.” It is not possible to immediately find the differences. Having spent a sufficient amount of time, we finally found them in the names of the indicators of lines 1 and 2.

Line 1: “Shipped goods of our own production, performed works and services ourselves (without VAT, excise taxes and similar mandatory payments).” Line 2: “Sold goods of non-own production (excluding VAT, excise taxes and similar mandatory payments).”

In 2009, instead of the words “and similar mandatory

payments" in lines 1 and 2 the phrase "and

other

similar payments" was used. A purely technical change: the wording has been brought into line with the wording of the income statement (accounting form No. 2).

Important

- If organizations present distorted statistical data or violate reporting deadlines, statistical authorities have the right to recover from such organizations damages arising in connection with the need to correct the results of consolidated reporting (Article 3 of the Law of the Russian Federation of May 13, 1992 No. 2761-1 “On Liability for Violation of Order” presentation of state statistical reporting" as amended on December 30, 2001). An administrative fine of 3,000 to 5,000 rubles may be imposed on responsible officials of such organizations. (Article 13.19 of the Code of Administrative Offenses of the Russian Federation).

An addressee has been added for strategic enterprises

Order No. 260 of Rosstat dated November 18, 2009 established an additional address for submitting Form No. 5-Z (in addition to submission to the territorial body of Rosstat in the constituent entity of the Russian Federation at the address established by it). Since 2010, organizations of the industrial and defense-industrial complexes (according to the list determined by the Ministry of Industry and Trade of Russia) must also submit the specified form to the Ministry of Industry and Trade of the Russian Federation.

The above also applies to other forms of federal statistical observation (details of Rosstat orders that approved the corresponding forms are given in brackets): No. 1-BZ (investments), No. S-2 (dated 08/14/2008 No. 189, dated 07/10/2009 No. 132) ; No. 1-license (dated 08/20/2008 No. 199, dated 08/20/2009 No. 179); No. BM (from 09.23.2008 No. 235, from 07.28.2009 No. 153); No. P-2, No. 11 (dated 07/10/2009 No. 132); No. 3-F (dated July 15, 2009 No. 138); No. P-3 (dated July 16, 2009 No. 139); No. 1-enterprise, No. 5-Z (dated July 28, 2009 No. 153); No. 7-trauma (dated 08/07/2009 No. 163); No. 1-trading (dated 08/20/2009 No. 178); No. P-4, No. 1-T, No. 1-T (working conditions) (dated 08.26.2009 No. 184); No. P-1, No. P-4 (NZ) (dated 10/14/2009 No. 226); No. 2-science, No. 1-technology, No. 4-innovation (dated 10.30.2009 No. 237).

Directions instead of Order

Order No. 86 of Rosstat dated February 11, 2010 approved the Instructions for filling out the federal statistical observation form No. 5-Z “Information on the costs of production and sale of products (goods, works, services)” (hereinafter referred to as the new Instructions). Rosstat Resolution No. 20 dated February 15, 2007 (as amended on February 12, 2008), which approved the Procedure for filling out and submitting the specified old form (hereinafter referred to as the old Procedure), has become invalid.

We discovered about fifty changes, among them very important semantic ones. We will focus special attention on them.

In the general part of the new Directives, a phrase has appeared that the head of a legal entity appoints officials authorized to provide statistical information on behalf of the legal entity. In fact, this had to be done before, and in relation to all statistical reporting, by virtue of clause 5 of the Regulations on the conditions for the mandatory provision of primary statistical data and administrative data to subjects of official statistical accounting, approved by Decree of the Government of the Russian Federation of August 18, 2008 No. 620 .

In the old Order there was clause 4 with the following content: “The form is used only to obtain summary statistical information. It cannot be used for tax purposes and provided to other commercial organizations.” There is no such norm in the new Instructions (accordingly, in the new Instructions all points are shifted back by one compared to the old Order). Will the territorial statistics office now be able to provide your Form No. 5-Z for a fee to other organizations without your consent? Hardly. In accordance with Art. 9 of the Federal Law of November 29, 2007 No. 282-FZ “On official statistical accounting and the system of state statistics in the Russian Federation”, primary statistical data contained in the forms of federal statistical observation are information of limited access (with the exception of information, the inadmissibility of restricting access to which is established by federal laws). The form itself bears the stamp “Confidentiality is guaranteed by the recipient of the information.” It is not clear why the provision of paragraph 4 was removed when drawing up the new Directives.

Before moving on to a detailed consideration of the instructions for filling out the indicators in Section I of the form, we note that the instructions for filling out the indicators in Section II “Information on the production of electrical and (or) thermal energy, transmission services and the costs of their production and transmission” remained unchanged. However, the “Features of filling out certain indicators by organizations of RAO UES of Russia” existing in the old Procedure were not included in the new Instructions (we recall that RAO UES was reorganized and actually ceased to exist).

Now let's move on directly to changes in the instructions for filling out the numerical indicators of section II of the form. In this section, line 01 reflects the volume of sold goods of own production, works and services, and line 02 - the cost of sold purchased goods of non-own production. All subsequent lines of the section reflect the expenditure side of the reporting organization's activities.

Sales volume of goods, works and services of own production

Line 01 shows the volume of all goods of own production shipped or released by way of sale, direct exchange (under an exchange agreement), trade credit, works performed and services rendered in-house in actual selling (sales) prices (excluding VAT, excise taxes and similar mandatory payments ), including the amount of compensation from budgets of all levels to cover benefits provided to certain categories of citizens in accordance with the legislation of the Russian Federation. Filling out line 01 is stated in paragraph 8 of the new Instructions, and was previously stated in paragraph 9 of the old Procedure.

The volume of goods shipped in the new Instructions means the cost of all goods produced by a given legal entity and actually shipped (transferred) in the reporting period to the party (to other legal entities and individuals, as well as provided to its employees as payment for labor

), including goods handed over to the customer on the spot according to the act, regardless of whether the money was credited to the seller’s account or not. The old Order did not directly mention wages in kind, so there were two different opinions on the need to reflect it as a shipment to individuals on the side.

According to the new Instructions, when shipping goods to a non-resident recipient, the moment of shipment is considered the date of its delivery to the transport or communications authority, determined by the date on the document (bill of lading, invoice, railway receipt, waybill, etc.), certifying the fact of acceptance of the cargo for transportation by the contracted party. organization or own transport division

, or document of the communication authority. In the old Order, instead of words in bold, the phrase “transport organization” was used. As a result, upon formal reading, it could be understood that the transfer of products to its transport division for delivery to its destination does not characterize the moment of shipment.

Also in the new Instructions there was an addition: “The cost of delivery of goods from the departure station to the destination station is not included in the volume of goods shipped.” Indeed, the temptation to include delivery in the shipment volume was present earlier, despite the presence of a separate expense line 41 “Expenses for payment for work and services of third-party organizations, of which: for the transportation of goods” in form No. 5-Z.

For convenience, we have placed changes in the features of determining the indicator of line 01 for various types of activities in the table. Please note that we are not considering changes of a purely editorial nature (when, for example, “and others” are replaced by “and other agreements”).

Landlords should pay attention to including in the scope of rental services the amounts of utility bills reimbursed by tenants. However, it must be taken into account that this procedure, in our opinion, may be fair in a situation where the lessor is considered the subscriber of the services, and not the tenant.

If the subscriber is a tenant, and the landlord only acts as an intermediary for collecting payments, then the landlord should not include payments in the scope of rental services. Such an intermediary for utility payments includes the amount of intermediary remuneration in line 01 indicator.

As we can see, most of the changes relate to construction activities and the housing and communal services sector. For example, the specifics of filling out line 01 have been determined separately for various housing and communal services entities: customer services, management organizations, homeowners' associations and housing-construction cooperatives.

Sales volume of purchased goods

Let's move on to changes in the features of filling out line 02 “Sold goods of non-own production (excluding VAT, excise taxes and similar mandatory payments)” of form No. 5-Z.

This line records the sales value of not only sold goods purchased externally directly for resale, but also any sold inventories of non-own production that were not used in production. Including the one reflected in the debit of account 91 in correspondence with the credit of accounts 10 and 11 (based on the totality of all possible correspondence of accounts from this group).

Data on line 02 are given in actual sales prices excluding VAT, excise taxes and similar mandatory payments. This line does not show the sale of own fixed assets, intangible assets, currency values, and securities.

According to the new Instructions, “line 02 shows the resale of energy, gas, water with the involvement of third-party organizations for their transportation.” In the old Procedure it was: “... line 02 shows the resale of energy, gas, water (without transporting them on our own).” You might think that there are practically no changes. However, in our opinion, a narrower formulation was used. The previous one allowed the inclusion of resale in the line for situations where transportation was carried out by the buyer. The concept of “third-party organizations,” in our opinion, does not include the second party to the contract - the buyer of energy, gas, water.

The old Procedure stated that the cost of sold gaseous fuel is reflected on line 02 by organizations that resell gaseous fuel purchased externally:

— gas distribution organizations;

— organizations and individual entrepreneurs carrying out gas purification from impurities, production of liquefied gas or pumping gas into cylinders.

Now the new Instructions for resale add: “organizations exporting gaseous fuel purchased externally.” Indeed, previously foreign buyers may not have fit into the concept of “gas distribution organizations.”

Features of reflecting material costs

Material costs are reflected on lines 03-20 of form No. 5-Z. The changes affected the filling of only a small part of these lines.

Thus, according to the new Instructions on line 03, organizations that resell purchased energy (electricity, heat), gas, water reflect their purchase price. In the old Order, instead of the word “resale”, “sale” was used. In our opinion, these words in this context do not differ from each other.

Line 15 shows the cost of all types of purchased energy (electricity, heat, compressed air, cold and other types) spent on technological, energy, propulsion and other production and economic needs of the organization (lighting, heating of buildings and other needs). Line 16 shows the cost of electrical energy, from which line 17 highlights the cost of electricity (power) purchased on the wholesale market (WEC), line 17 is filled in by organizations that have the status of a wholesale market entity in accordance with current legislation

, line 18 indicates the cost of thermal energy. In other words, these lines reflect the purchased energy used in production (according to actually accrued payments), attributed to production costs in the reporting period, at the cost recorded in the debit of cost accounting accounts 20, 23 (25, 26), 29 and 44 in correspondence with the credit of accounts 60 (76) (for the totality of all possible correspondence of accounts of this group) (clause 17 of the new Instructions). The old Procedure did not explain who should fill out line 17.

Let us note that the procedure for a legal entity to obtain the status of a wholesale market entity (WECM entity), a participant in the circulation of electrical energy on the wholesale market, is regulated by Art. 35 of the Federal Law of March 26, 2003 No. 35-FZ “On Electric Power Industry” (as amended on November 23, 2009) and Section II of the Rules of the Wholesale Electric Energy (Power) Market of the Transitional Period, approved by Decree of the Government of the Russian Federation dated October 24, 2003 No. 643 (as amended dated 03/04/2010).

Taxes, fees, insurance payments

In connection with the reform of compulsory social insurance and the replacement of the unified social tax with insurance contributions to extra-budgetary funds, the new Instructions provide specifics for filling out line 26 of the form. Now this line shows the amounts of accrued insurance contributions to the Pension Fund of the Russian Federation for compulsory pension insurance, the Social Insurance Fund of the Russian Federation for compulsory social insurance in case of temporary disability and in connection with maternity, the Federal Compulsory Medical Insurance Fund and territorial compulsory health insurance funds for compulsory medical insurance. These are the amounts recorded as the debit of cost accounts 20, 23 (25, 26), 29 and 44 in correspondence with the credit of the corresponding subaccounts of account 69 (68) (based on the totality of all possible correspondence accounts from this group). Here, for some reason, the score 68 was inserted in parentheses, although it was more suitable for the abolished Unified Social Tax.

As before, organizations paying a single agricultural tax, a single tax on imputed income, using a simplified taxation system, show in line 26 the amount of insurance contributions for compulsory pension insurance. We remind you that in 2010 “special regime residents” pay insurance premiums at preferential rates (in fact, only 14% in the Pension Fund of the Russian Federation). However, from 2011 they will not be any different from other payers of insurance premiums, and then this rule for filling out line 26 will lose meaning for them.

Line 35 reflects the amounts of taxes and fees, state duties, payments and other mandatory deductions accrued in accordance with the procedure established by law and taken into account as part of the costs of production of products, goods, works, services (water tax, land tax, mineral extraction tax minerals, transport tax, payments for environmental pollution, fees for the use of wildlife and for the use of aquatic biological resources, payments for maximum permissible emissions, discharges, levels of harmful effects, waste disposal limits, etc.).

This line does not reflect taxes accrued based on the financial results of the organization (income tax, gambling tax, UTII, Unified Agricultural Tax, unified tax under the simplified tax system).

According to the new Instructions, line 35 also does not reflect the unified social tax (now abolished), the amount of VAT, excise taxes, customs and export duties, the amount of payments for excess emissions of pollutants into the environment, payments paid under the terms of restructuring debts to the budget and extra-budgetary funds, and also the amounts of taxes accrued to budgets of various levels if such taxes were previously included by the taxpayer as expenses when writing off the taxpayer's accounts payable for these taxes.

Thus, property tax is excluded from exclusion payments, so it should be taken into account on line 35. In our opinion, in the old Procedure this tax was included among the exceptions erroneously. After all, it is not accrued based on financial results.

Line 32, as before, shows accrued payments for compulsory insurance of various types (except for contributions to compulsory social insurance, taken into account on line 26, and payments for voluntary insurance, taken into account on line 32 of the form).

In accordance with clause 29 of the new Instructions, line 32 of Form No. 5-Z shows accrued voluntary insurance payments made in accordance with the legislation of the Russian Federation and taken into account in production cost accounts, in particular, under contracts:

— insurance of property used in activities aimed at generating income;

— liability insurance for causing harm;

— risk insurance;

— non-state pension provision in favor of employees (please note that expenses in the form of contributions to non-state pension provision are reflected precisely on line 32, and not on line 26).

This line does not reflect voluntary medical and other insurance payments made at the expense of profits and other targeted revenues of the organization. Thus, line 32 reflects the indicated payments, recorded as the debit of cost accounts 20, 23 (25, 26), 29 and 44 in correspondence with the credit of the corresponding subaccounts of account 76 (according to the totality of all possible correspondence accounts from this group).

Let us note that in the old Procedure the types of insurance were not clearly named and non-state pension provision was not indicated.

Changes in the rules for filling out line 01 of form No. 5-З

| Provisions of paragraph 9 of the old Order | Provisions of paragraph 8 of the new Instructions |

| PUBLIC CATERING | |

| Line 01 also reflects the cost of culinary products and culinary semi-finished products sold through retail facilities (shops and culinary departments, pavilions, tents) of public catering organizations | Line 01 also reflects the cost of culinary products and semi-finished culinary products sold by public catering organizations through their retail trade facilities (shops and culinary departments, pavilions, tents) |

| CONSTRUCTION | |

| Works and services of a construction nature (including repair and construction) performed in-house are reflected on line 01 on the basis of established documents on their acceptance by customers (form No. KS-3 “Certificate of the cost of work performed and expenses”) | Construction works and services (including repair and construction) not for personal consumption , carried out in-house, are reflected on line 01 on the basis of established documents on their acceptance by customers (form No. KS-3 “Certificate of the cost of work performed and expenses”) |

| If an organization carries out construction, installation and other work using materials produced auxiliary divisions of this organization, then the cost of these materials is not excluded from the scope of work performed in-house under construction contracts | If an organization carries out construction, installation and other work using materials produced by divisions of this organization, then the cost of these materials is not excluded from the scope of work performed on its own under construction contracts |

| Line 01 also reflects the volume of work performed by the organization that is the customer (developer) and at the same time carries out the construction of objects on its own, including with the involvement of funds from shareholders (legal entities and individuals) for subsequent sale and provision of shared construction agreements | When an organization combines the functions of a contractor and a customer (developer), regardless of the adopted accounting policy when forming costs for the construction of residential buildings on account 20 “Main production” with subsequent attribution to account 08 “Investments in non-current assets” or only on account 08 without prior accounting for In account 20, the cost of construction work and services performed on one’s own is reflected in this section on line 01. Profit received from the sale of residential buildings and non-residential buildings to other legal entities and individuals (including equity holders) relates to the type of activity “construction” and is accordingly reflected in this section on line 01 |

| Provisions of paragraph 9 of the old Order | Provisions of paragraph 8 of the new Instructions |

| DEPARTMENT OF HOUSING AND UTILITIES | |

| Organizations that only charge and collect utility bills and are not directly involved in supplying the population with electricity and heat, natural gas and water, show on line 01 the amount of commission for the provision of this service. For utility services, the amounts of accrued payments for the provision of these services are reflected. Services for the operation and maintenance of housing stock are reflected in this line in the amount of the total amount of income from the sale of services to all consumers (this value does not take into account compensation for the difference between economically justified tariffs and current tariffs from budgets of all levels and compensation of costs from the federal budget for the maintenance of housing facilities utilities accepted into municipal ownership - these values relate to subsidies from the budget) | Managing organization in the housing and communal services sector, line 01 shows the total amount of income from the sale of services to all consumers, performed in-house, including with the involvement of third-party organizations, for the operation, maintenance and repair of the housing stock, provision of utilities (including the cost of utility resources purchased from the resource supplying organization , regardless of the accounting account in which their acquisition is reflected). For housing and communal services objects accepted into municipal ownership, subsidies from budgets of all levels are not taken into account, which compensate for the difference between economically justified and current tariffs. HOA and housing cooperative on this line (if they are not management organizations in relation to the owners of premises in an apartment building) reflect income from the rental of common property (premises, advertising space, etc.), the provision of consulting and other information services to other legal and physical entities persons, as well as other types of activities for the performance of work and provision of services to the outside. The activities of the HOA in the operation, maintenance and repair of the housing stock are not reflected. Organizations Those who only charge and collect utility bills show the amount of the commission on line 01. Customer service reflects income depending on the functions performed. When concluding an agreement for the management of an apartment building (Article 162 of the Housing Code), it reports as a management organization. If such an agreement has not been signed by the customer’s service, line 01 shows the income received from work performed and services provided on its own for the maintenance and operation of the housing stock. On line 06, a management organization in the housing and communal services sector, which has entered into an agreement for the management of an apartment building and provides housing and communal services, must reflect the cost of utility resources (cold and hot water, electricity, gas, heat energy) purchased from the resource supply organization |

| TOURISM | |

| For tour operator activities, the cost of goods sold to the population or organizations is shown. vouchers (tours). For travel agency activities, either the amount of commission (agency) remuneration or the difference between the sale and purchase prices of the trip (tour) | For tour operator activities, the cost is shown formed and sold to the population or For travel agency activities, either the amount of commission (agency) remuneration or the difference between the sale and purchase prices of the tour is reflected (the travel agent is not involved in the formation of the tour and is not responsible to tourists or other customers, but only promotes and sells on its own behalf the tourist product purchased from tour operator, or sale of a tourist product on the basis of an agency agreement on behalf of and on behalf of the tour operator) |

| RENTAL | |

| In addition to rent, rental income includes all other payments of tenants related to obtaining property for rent (for electricity, heat, water and others), if they are not included in the rent | |

| FINANCIAL ACTIVITIES | |

| If a non-financial organization, along with other types of activities, provides services for financial activities and revenue is recognized in accounting as income from ordinary activities, then the cost of these services should be reflected in line 01. For example, for services provided in the form of financial lease (leasing) received leasing payments (without the redemption value of the leased asset) | |

| GAMING BUSINESS | |

| Organizations engaged in organizing gambling activities reflect gross income on line 01, which is the difference between the cost of sold tokens, entry fees and the amount of payments on winnings (excluding VAT and similar mandatory payments) | Organizations carrying out gambling activities (OKVED code 92.71) , on line 01 reflect the gross income, which is the difference between the cost of tokens sold, the entry fee and the amount of payments on winnings (excluding VAT and similar mandatory payments) |

| TRANSPORT and COMMUNICATION | |

| The cost of travel tickets, coupons for all types of transport, lottery tickets, telephone cards, express payment cards for communication services is included in the total volume of services provided to the party, reflected on line 01 by those organizations that carry out these types of activities. For example, transport organizations providing passenger transportation using coupons and travel tickets, communication organizations providing their services using telephone cards and express payment cards | |

| NPO | |

| Not reflected on line 01, including targeted income of non-profit organizations (membership fees, shares, donations, grants, etc.) | |

*Finished in the next issue.

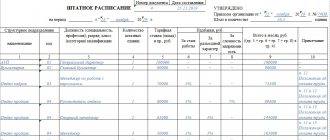

Section 1

Section 1 of Form 5-Z reflects the main economic indicators of the organization given in column 1 of the table in this section - for the reporting period, as well as for the same period last year.

The corresponding economic indicators can be classified into the following main groups:

1. Indicators of shipment and sale of goods, services and works.

Since 2021, it has been clarified that the sales volume in line 01 must be indicated without taking into account customs and export duties (Rosstat order No. 63 dated February 12, 2019).

2. Expenses:

- for the purchase of goods for resale;

From 2021, it is clarified that lines 03 and 04 reflect real estate acquired for resale, and there are also a number of clarifications for persons associated with construction (Rosstat order No. 63 dated 02.12.2019).

- for the purchase of raw materials, materials, semi-finished products for production;

- for the purchase of fuel, energy, water;

- for the purchase of raw materials, materials and semi-finished products purchased for production, but subsequently resold;

- for the reclamation of land areas;

- for wages, contributions to state funds;

- for insurance;

- for rent;

- to pay for the services of third-party companies;

- for the purchase of forest plantations;

- representative;

- others.

3. Balance indicators:

- for goods originally purchased for resale;

Starting from 2021, lines 04 and 05 reflect unsold real estate items as inventory balances (Rosstat order No. 63 dated February 12, 2019).

- on raw materials, materials and semi-finished products for production;

- for finished products;

- for work in progress.

4. Depreciation:

- fixed assets;

- intangible assets.

5. Taxes included in the cost of goods, services, and work.

Section 1 of Form 5-Z is also supplemented with a reference block. It records, in relation to the reporting period, as well as the same period last year:

- cost of used raw materials;

- the amount of VAT for the reporting period;

- the amount of subsidies received from the budget;

- the amount of fees for using the infrastructure given in lines 67–70 of the table in section 1 (as part of the costs).

The data in the table of section 1 is recorded in thousands of rubles.

How to fill out the form

There are usually no difficulties when filling out the title page: it is enough to correctly enter the name, address and OKPO.

The form includes two sections.

Section 1

The first section records economic indicators; the tabular part resembles a cost estimate. Line 01 records the cost of goods, works, and services sold, excluding VAT. This line does not need to reflect funding for certain purposes, such as maintaining the organization and conducting activities of non-profit organizations. Also, you should not show goods of your own production aimed at the needs of the enterprise. The cost of delivery from station to station is not taken into account.

Line 02 records the cost (excluding VAT) of goods sold for resale, recorded on account 41. In particular, this line records the sale of energy, water and gas by intermediaries who engage special organizations for transportation.

Commission agents, attorneys and agents do not fill out line 02, but principals and principals who are the owners of goods show the cost of sales in line 02.

Line 02 also records the release of goods to employees on account of wages; the cost of selling inventory items previously purchased for production or management needs, but not spent.

Line 03 records the costs of purchasing goods for resale. For example, realtors will record here the costs of assessing the apartment they purchased for subsequent sale.

The balances of goods for resale at the beginning and end of the period are recorded in lines 04 and 05, respectively.

Line 06 records expenses for the purchase of raw materials, spare parts, supplies, semi-finished products, workwear used in the production process and for sale. The listed material assets are usually taken into account in accounts 10, 11, 15 and 16.

From line 06 to lines 07-09, expenses for imported materials, gas, delivery with storage of material assets are allocated.

Expenses for the purchase of fuel are taken into account in line 10. Petroleum products, natural gas, coal and other fuels are separately distinguished from the total amount of fuel. Expenses by type of fuel are recorded in lines 11-14.

Total energy costs are recorded in line 15. Costs for electrical and thermal energy are separated from it (lines 16-18).

The purchase of water is reflected in line 19. Here, consumed water is taken into account, written off as a debit to expense accounts.

Line 20 from lines 06, 10, 21 identifies those raw materials (spare parts, materials, containers, etc.) that were purchased for production, but sold in the current year without processing.

Lines 21 and 22 record warehouse balances of inventories in thousands of rubles. For example, agricultural structures in the listed lines note the remains of fertilizers, animal feed, seeds, work equipment purchased or received free of charge for production and sale.

Lines 23-48 record various types of enterprise expenses, including depreciation, taxes, wages, insurance, travel expenses, rent, repairs, third-party services, etc.

Lines 52, 53 record the balances of finished industrial products in warehouses and with commission agents for sale. Work in progress is recorded in lines 54 and 55. Industrial products within the framework of filling out form 5-Z are understood as products of mining industries (coal, oil, etc.), products of manufacturing industries (meat, animal skins and leather, offal, toys, umbrellas etc.), gas, energy, steam, water, waste oils, scrap, secondary raw materials, chemically hazardous waste, paper and plastic waste, etc. For a complete list of industrial products, see the special classifier (sections B-E).

The data is recorded on lines 61-70 for reference. Line 61 records the cost of unpaid processed customer-supplied raw materials (account 003).

Line 62 indicates sales VAT. On line 63, subsidies from the budget for production should be recorded, then you need to allocate subsidies from this line to cover losses on sales (line 64).

Line 67 shows the rent for the use of cars (the amount is allocated from line 09). On line 68 from line 09, the fee for freight transportation is allocated. On lines 69 and 70 from line 42, rental fees for the use of wagons and fees for freight transportation are allocated, respectively.

Section 2

Section 2 of Form 5-Z reflects data on electricity and thermal energy produced by the company and supplied to the market. In correlation with such indicators as production volume, as well as production and transmission costs - for the period from the beginning of the year to the reporting and similar periods of last year, the following information is indicated:

- on electricity production;

- on the production of thermal energy;

- about transmission services for each type of energy.

The data in the table in section 2 is also recorded in thousands of rubles.

Information on the costs of production and sale of products (goods, works, services)

They must comply with at least one of the requirements provided for in paragraphs. 1 clause 1.1 art. 5 of the Federal Law “On the Development of Small and Medium Enterprises in the Russian Federation”, for example, the share of state participation, public organizations and charitable foundations here should not be more than 25 percent, and foreign organizations - 49.

On the form containing information on a separate division of a legal entity, the name of the separate division and the legal entity to which it belongs is indicated (for example: Branch No. 19 of Krasny Tekstilshchik CJSC).

Reports prepared for submission should consist of:

- "General Economic Indicators" . This section indicates basic data on the volume of goods shipped to customers, as well as information on services provided and work performed for customers. Information about the costs incurred is also provided.

- Section of a specialized nature . It covers issues about the production of such types of energy as thermal and electrical. In this case, the costs of production and transmission to consumers must be indicated.

The data is presented in accordance with the accounting policies adopted in the current reporting period, but without recalculation into the prices of the reporting year, i.e. at prices in force in the corresponding period of the previous year.

Recently, changes have been made to Form 5 H, so it is extremely important to understand how to fill it out.

Products made from customer-supplied raw materials (raw materials and materials of the customer, not paid for by the manufacturer), are included by the manufacturer in the volume of shipped goods of its own production (work performed and services provided in-house) at the cost of processing, that is, without the cost of raw materials and materials customer.

Temporarily non-operating organizations, where production of goods and services took place during part of the reporting period, submit a form on a general basis indicating the time from which they have not been working.

At the same time, organizations carrying out trust management draw up and provide reports on the activities of the property complex in their ownership.

This line also indicates the sold surplus of raw materials and supplies, the purchase of which was recorded in the inventory accounts.

These indicators are compiled on the basis of synthetic and analytical accounting. Hints to the indicators are given on the basis of the Chart of Accounts for accounting the financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n.

In 2009, organizations submitted Form No. 5-Z, approved by Rosstat Order No. 235 dated September 23, 2008. In 2010, it is necessary to submit Form No. 5-Z approved by Rosstat Order No. 153 dated July 28, 2009 “On approval of statistical tools for the organization Federal statistical monitoring of enterprise activities."

The cost of goods accepted by the buyer and paid for by him, but left as an exception in the custody of the seller for reasons beyond his control and issued with safekeeping receipts, is included in the volume of goods shipped.

Associations of legal entities (associations and unions) in the specified form reflect data only on activities recorded on the balance sheet of the association, and do not include data on legal entities that are members of this association.

Organizations carrying out trust management of individual property objects provide the founders of the management with the necessary information about their property. The management founders draw up their reports taking into account information received from the trustee. The state, having imposed the obligation on legal entities to provide reporting on the costs of production, does not provide for the possibility of not providing this reporting, with the minor exceptions discussed above. If an organization for some reason did not send this form to Rosstat or missed the deadline for submitting this form, it will face a fine.

Document signature

The certification block of the form following Section 2 must include:

- date of completion of the document;

- signature of the head of the company or employee who has the authority to certify the document;

- an indication of the position of the person who signed the form, as well as his contact information.

This is the sequence of filling out form No. 5-Z. There are a number of nuances of working with the document that are useful to pay attention to - they are taken into account in the instructions for filling out Form 5-Z.

Filling out statistics form No. 5-Z: what to pay attention to?

When filling out form No. 5-Z, you must keep in mind that:

- the information indicated for a particular period of the previous year must completely coincide with that presented in the reports for the corresponding period earlier (unless the legal entity was reorganized or the methodology for reflecting indicators in the reports was changed);

- if the company was nevertheless reorganized or there were changes in the methodology for reflecting indicators in reporting, the information in Form 5-Z is provided based on the relevant changes;

- in any case, discrepancies between the indicators for the periods of last year, recorded earlier in the reporting and reflected in the current reporting, must be explained in the explanation to the document;

- information in the form is reflected on an accrual basis from the beginning of the year;

- data on business indicators reflected in the form must correspond to the documentation maintained by the company as part of accounting.

Form 5 "statistics" 2021: Is it possible not to provide reporting?

The state, having imposed the obligation on legal entities to provide reporting on the costs of production, does not provide for the possibility of not providing this reporting, with the minor exceptions discussed above. If an organization for some reason did not send this form to Rosstat or missed the deadline for submitting this form, it will face a fine. So, for a company it will cost from twenty to seventy thousand rubles, and for authorized persons - from ten to twenty. Moreover, if such an offense is committed repeatedly, the punishment becomes more severe - the organization will pay from one hundred to one hundred and fifty thousand rubles, and officials - from thirty to fifty.

Results

Rosstat, collecting data as part of scheduled observations, instructs legal entities that are larger in scale than small enterprises (but do not belong to economic entities in the financial and budgetary sectors) to inform the agency about the costs associated with the production and sale of goods. For these purposes, form No. 5-Z is used.

You can find other information about reporting to Rosstat in the articles:

- “Procedure and sample for filling out the P-2 quarterly form”;

- “Procedure and sample for filling out form No. 1-Enterprise.”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.