Accounting and tax accounting in an organization

Any accountant probably knows that there are several types of accounting, the most common (and probably the most important) of which are accounting and tax.

Take our proprietary course on choosing stocks on the stock market → training course

Accounting is a reflection of the entire economic life of an organization through primary documents. When maintaining accounting records, all events that occur in the life of the company are taken into account. The purpose and outcome of operations in the field of accounting is the preparation of annual reports. The year-end financial report is prepared for:

- Internal users. Their role is played by the owners or top managers of the company. Based on the report data, they draw conclusions about the success of the organization during the year and make the necessary decisions

- External users. These include primarily creditors and tax authorities.

Based on the accounting report, the state of the organization and its development prospects are assessed. Reporting helps make important management decisions .

The main documents regulating accounting are the Law “On Accounting” and the Accounting Regulations (PBU).

Tax accounting is a system that is built on the basis of primary documents and summarizes information that is used to calculate the amount of taxes.

The lion's share of all tax accounting is the calculation of income tax. The main act that regulates this type of accounting is the Tax Code .

The main feature of tax accounting is that not all transactions reflected in accounting are accepted for calculating the amount of tax liabilities. Some expenses are not accepted at all, while others are rationed.

Types of differences that may arise during operation

Due to the fact that for accounting purposes all amounts of income and expenses are accepted, and for tax purposes only selectively, differences arise when calculating income tax. These differences can lead to either a tax decrease or an increase. Moreover, in both cases, the tax change can be either permanent or temporary . If such differences arise in the company, then the following entries are generated in accounting:

- Calculation of income tax, reflects the organization's debt to the budget D99 K68.04

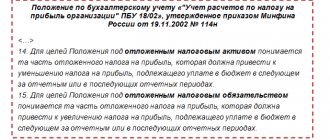

- If there are differences that increase tax:

– constantly D99 K68

– temporarily D09 K68

- If there are differences that reduce tax:

– constantly D68 K99

– temporarily D68 K77

It must be taken into account that accounts 09 and 77 are subsequently closed with reverse entries.

| IMPORTANT! Temporary differences do not affect the company's net profit |

Let's look at what the differences look like using an example. Initial data:

revenue 150 thousand rubles, cost 50 thousand rubles, wage fund 20 thousand rubles, artificial fountain in the director’s office 30 thousand rubles, gratuitous receipt from the founder 50 thousand rubles, fines and penalties for taxes 30 thousand roubles.

| Index | Accounting | Tax accounting |

| Revenue | +150 | +150 |

| Cost price | -50 | -50 |

| Payroll fund | -20 | -20 |

| Fountain | -30 | – |

| Proceeds from the founders | +50 | – |

| Fines, penalties | -30 | |

| Profit before tax | +70 | +80 |

It turns out that according to accounting data, it would be necessary to pay less tax than required by tax accounting. Taking into account the differences, accounting data must be brought to the same level as tax accounting data.

It must be borne in mind that the amount of income tax for transfer to the budget is calculated as conditional income (that is, the profit before tax that is obtained according to accounting data), adjusted for all resulting differences. If everything is done correctly, the tax received by this calculation will coincide with the amount of tax according to the declaration.

SHE calculation

The account records OTA amounts that arise when there are deductible temporary differences between the data on income and expenses in accounting and tax accounting. The SHE indicator is defined as follows:

SHE = Vvr * STn;

Where:

- Вр - deductible temporary difference;

- STn is the rate for calculating income tax for a given enterprise.

The concept of deferred tax assets (DTA)

Deferred tax assets are formed due to differences in the values of indicators in tax and accounting. When such assets arise, there is a temporary tax increase, which means that the tax deduction will be made later .

Deferred tax assets are often created when depreciation is calculated. However, after the object is completely depreciated, the difference will disappear, and, therefore, the deferred asset.

Another interesting case is advertising costs. They are standardized except for cases where advertising is placed in the media, at exhibitions or fairs. At the same time, advertising expenses can be taken into account in tax accounting in the amount of 1% of revenue. That is, if advertising costs 100 thousand rubles, and 1% is 80 thousand rubles, then the difference between the two types of accounting in the company will be 20 thousand rubles, the tax on it is 4 thousand rubles. and for this amount it is necessary to create a deferred tax asset.

It is also very important to remember that if at the end of the period there is a loss, then you can submit a declaration with zero profit, and form a deferred tax asset for the amount of the loss.

Practical calculation examples

For a clearer understanding of deferred tax assets and deferred tax liabilities, several practical examples can be considered.

EXAMPLE 1.

A company sells a machine to another organization. In both types of accounting, a loss of 24,000 rubles is recorded. It is entered into accounting records immediately, and into tax records - evenly throughout the remaining period of operation. Therefore, a positive difference of 24,000 rubles arises. Since the base tax rate is 20%, the value of the deferred asset is 24,000 * 20% = 4,800 rubles.

If we assume that at the date of sale the remaining service life of the equipment was another 12 months, then in tax accounting the resulting loss should be evenly distributed over each month, i.e. 24000/12 = 2000 rubles/month. Therefore, the value of the deferred asset will decrease by 2000 rubles every month.

EXAMPLE 2.

The company purchased materials from a supplier in the amount of 100,000 rubles. The accountant immediately wrote off the materials for production, but the payment was not transferred to the supplier. In this regard, the company cannot take into account the expenses incurred in tax accounting, however, the accounting materials are written off according to the usual procedure. Therefore, a positive difference appears, which can be calculated using the basic income tax rate, i.e. 100000*20% = 20000 rub. This is “SHE”.

It is known that in the same year the company also suffered a loss of 100,000 rubles, which reduced the income tax base. Since an ONA was already created for this amount earlier, this year the accountant must reduce the size of the asset.

Expert opinion

Kochergin Sergey

Tax specialist, financial manager, website expert

Previously, we provided a sample response to the tax authorities’ requests for clarification; you can see an example here.

Deferred tax asset accounts

The accounting entries relating to deferred tax assets have already been given above.

As you can see, when such assets arise, two accounts appear:

- Account 68 with the corresponding subaccount. The credit of the account reflects our income tax debt to the budget and the creation of a deferred tax asset

- Account 09, which is called “Deferred tax assets”. The debit of the account reflects the creation of an asset, and the credit reflects its closure

In the explanation to the financial statements of the first two forms, it is necessary to reflect information about contingent expenses, differences and accrued deferred assets.

Reflection of SHE in the balance sheet of the organization

In the balance sheet, such assets are reflected in balance sheet asset line 1180.

It must be borne in mind that information on this line can be specified without detail. Moreover, in collapsed form, the amount of deferred tax assets is indicated only if they are taken into account when calculating income tax.

The amount of the deferred tax liability is the balance in the debit of account 09.

In order to find the amount of such an asset by calculation, you need to multiply the temporary difference in expenses by the approved income tax rate.

In addition to being reflected in the balance sheet, deferred tax assets are indicated in Form No. 2. To do this, the change in the deferred asset is calculated as the difference between the credit and debit closing balance of account 09. In this case, the sign of the calculation result does not change.

Change in deferred liability indicator (posting)

Movements by account 77 are carried out within strictly limited limits, operations can be carried out to reduce or increase the indicator:

| Operation | DEBIT | CREDIT |

| Reduction or full settlement of deferred tax liabilities | 77 “Deferred obligations” | 68.4 “Calculations for income tax” |

| Increasing the cost of debt to increase the amount of income tax | 68.4 | 77 |

| Removal of deferred tax liability from the balance sheet | 77 | 99 “Profits and losses” |

Not only the amount of debt, but also the temporary difference is subject to write-off.

Example of writing off a deferred liability (posting)

The company decided to sell its fixed asset to a partner. At the date of sale the following depreciation charges were observed:

- in accounting – 295 thousand rubles,

- in tax accounting – 387 thousand rubles.

The accountant checks the deferred tax savings in account 77:

- RUB 387,000 – 295,000 rub. = 92,000 rubles,

- 92,000 rub. x 20% = 18,400 rubles.

The following is written off from the balance sheet:

Dt 77 Kt 99 – 18,400 rubles for the amount of the deferred liability.

An example of calculating and reflecting the amount of deferred tax assets in the balance sheet

Let's give a small example of calculating deferred assets and take the most common cases - advertising expenses and depreciation.

| Operation | Accounting | Tax accounting | Difference | Tax rate 20% | Wiring |

| Advertising expenses | -200 | -150 | 50 | 10 | D09 K68 |

| Depreciation | -2667 | -2000 | 667 | 133 | D09 K68 |

We show the indicator values with a minus, so these are the expenses incurred. By posting, we accrue the amount of the deferred tax asset, which will be taken into account in the following periods. Accordingly, according to advertising, the value of the deferred asset is 10, and according to depreciation, 133.

The accounting “plane” for account 09 will be the following scheme:

| Debit | Credit |

| 10 | |

| 133 | |

| Turnover 143 | |

| Final balance 143 |

The amount of the final balance is the organization's prepayment for the future. This amount must be reflected in the balance sheet.

At the same time, the value of these assets, along with other indicators, is reflected in the credit of account 68.

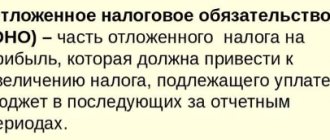

Deferred tax liabilities: essence and understanding

Deferred tax liabilities represent amounts of income taxes payable in future periods.

When income tax expense exceeds the amount of income tax payable as a result of not recognizing any non-cash income on tax returns, a portion of the income payable is deferred to the future. The lower income tax payable on tax returns creates a deferred tax liability that companies must meet in the future. Deferred liabilities may be presented as current liabilities if the temporary difference between accounting income and taxable income is reconciled in the following year.

Important! A deferred tax liability arises when a business has a certain amount of income during an accounting period and that amount differs from the taxable amount on its tax return. When the amount is less than the estimated tax, the entry is included in the balance sheet as a liability.

Example No. 2. Example of a deferred tax liability.

Company XYZ owns machinery, which is classified as an asset. They prefer to use a specific accelerated depreciation method that allows for higher deductions early in ownership of the asset and lower deductions later.

This differs from the slower straight-line depreciation method used by tax authorities, which means that depreciation is spread evenly over the useful life of the asset.

The depreciation method affects the amount of accruals for each reporting period.

Since the depreciation method chosen by XYZ Company will initially result in a larger deduction than the method used by the tax authorities, their income will be higher than what would be considered taxable income. In this case, the temporary difference will be added as a liability to the balance sheet.