Any business entity has both current and non-current assets necessary to carry out production and commercial activities.

Fixed assets, inventories of all types, cash funds and financial instruments - all this, as a rule, does not raise questions among business representatives and accountants when it comes to valuation, accounting and other tasks.

However, intangible assets (intangible assets) in this regard still remain a topic that requires detailed explanation.

The main problem of adequate perception of intangible assets is precisely that such objects do not have material expression, although they belong to the category of non-current assets.

It makes sense to talk about their existence only in the aspect of possessing certain legal rights.

Understanding the specifics of creating and using intangible assets is extremely necessary today, since these assets significantly affect the state of the business and its profitability.

What are intangible assets

Intangible assets are those objects that do not have a material embodiment, but at the same time generate profit and are used in production for more than one calendar year.

In general terms, intangible assets usually come down to copyrights, patent rights, know-how, breeding achievements, business reputation and other similar assets. In other words, intangible assets are objects of intellectual property that are directly used in production, but are not a tangible object that, roughly speaking, “can be touched.”

The absence of a material form is the key difference between intangible assets and fixed assets. Otherwise, from the point of view of use and accounting, these categories of assets are quite similar: they can be capitalized through purchase, independent creation or inclusion in the charter capital from the founder; they are depreciated, used for more than 12 months and are not intended solely for resale.

They are also shown differently on the balance sheet. There is a balance sheet line “Fixed assets”, there is a line “Intangible assets”. As for current accounting, entries related to intangible assets are posted to account 04 “Intangible assets”, as well as account 05 “Amortization of intangible assets”.

To recognize an object as an intangible asset, the ability to identify and separate it from other assets is important. For example, the professional qualities and skills of employees will not be considered intangible assets, since they are inseparable from the employee who possesses them.

For example, a bakery invented a new technology for producing pies and patented it. The equipment involved in the production process will be fixed assets, the products will be materials, the pies themselves will be finished products and goods, but the patented technology will be classified as intangible assets.

In which accounts should intangible assets be recorded?

The accounting account for an intangible asset depends on the right under which it was obtained.

| Right | Account | Example |

| Exclusive right | 0 102 XN 000 “Scientific research (research development)” 0 102 XR 000 “Experimental design and technological development” 0 102 XI 000 “Software and databases” 0 102 XD 000 “Other intellectual property” | Exclusive right to software - account 0 102 ХI 000; Exclusive right to a selection achievement - account 0 102 ХN 000; Exclusive right to a trademark - account 0 102 ХD 000; Exclusive right to an invention - account 0 102 ХN 000 |

| Non-exclusive right | 0 111 6N 000 “Rights to use scientific research (research developments)” 0 111 6R 000 “Rights to use experimental design and technological developments” 0 111 6I 000 “Rights to use software and databases” 0 111 6D 000 “Rights to use other objects of intellectual property" | Non-exclusive right to antivirus - account 0 111 6I 000; Non-exclusive right to a utility model - account 0 111 6N 000; Non-exclusive right to an electronic archive - account 0 111 6I 000; Non-exclusive right to a literary work - account 0 111 6D 000. |

Objects of intangible assets are grouped according to clause 37 of Instruction No. 157n. That is, objects received under exclusive right are accounted for in the corresponding account 102 00, where X can take the value 2 “Especially valuable movable property of the institution”, 3 “Other movable property of the institution” or 9 “Property in concession”.

More on the topic: Reporting for 2021: what clarifications should institutions take into account?

For example, on account 102 91 “Software and databases in concession” information about programs for electronic computers, databases, information systems and (or) sites on the Internet or other information and telecommunication networks that are the objects of concession agreements is subject to reflection. which includes such computer programs and (or) databases, or about the totality of these objects, as well as about operations that change them.

The grouping by type of property, designated by the letters N, R, I or D, corresponds to the subsections of the classification established by OKOF *(3) (clause 67 of Instruction No. 157n, letter of the Ministry of Finance of Russia dated September 17, 2020 No. 02-07-10/81813). Namely, OKOF provides for the following groups of intellectual property objects (OKOF code 700):

- scientific research and development (OKOF code 710);

- software and databases (OKOF code 730);

- other objects of intellectual property (OKOF code 790).

For example, multimedia applications are named in the “Software and Databases” group - OKOF code 732.00.10.08. Consequently, the exclusive right to this object, related to other movable property, is taken into account in account 102 3I. And if an institution has a non-exclusive right to multimedia applications, then it will be reflected in account 111 6I.

Do not apply to intangible assets

- R&D that did not produce a positive result, was not completed or was not formalized in the prescribed manner;

- things in which the results of intellectual activity and equivalent means of individualization are expressed (for example, CDs with programs recorded on them);

- financial investments;

- expenses associated with the formation of a legal entity (organizational expenses);

- intellectual and business qualities of the organization’s personnel, their qualifications and ability to work.

Reflection of intangible assets in accounting and financial statements

Intangible assets are recorded on account 04 “Intangible assets”, amortized and reflected in the balance sheet at their residual (book) value as part of non-current assets on line 1110 “Intangible assets”.

A breakdown of the information on intangible assets is given in tables 1.1 – 1.5 of the Explanations to the balance sheet and financial results statement (Appendix No. 3 to Order of the Ministry of Finance of Russia dated July 2, 2010 N 66n).

Which assets are covered by IAS 38?

IAS 38 prescribes accounting rules for all intangible assets, excluding intangible assets covered by other standards.

Assets that are not covered by IAS 38 and are accounted for in accordance with other standards:

- Deferred tax assets - IAS 12 Income Taxes,

- Goodwill - IFRS 3 Business Combinations,

- Intangible assets held for sale - IFRS 5 Non-current assets held for sale and discontinued operations

- Financial assets - IAS 32 Financial Instruments: Presentation and IFRS 9 Financial Instruments

- Assets covered by IFRS 6 Exploration for and Evaluation of Mineral Reserves

- Expenses for the development and production of minerals, oil, natural gas and other non-renewable resources.

Reasons for the occurrence of intangible assets

Intangible assets arise on certain grounds. Their presence must be documented. This is especially important when accounting for intangible assets. You can confirm the grounds for obtaining rights with the following documentation:

- Patents.

- Agreements for the transfer of rights.

- Purchase and sale agreements.

- Licenses for the right to operate.

- Agreements on the transfer of rights to inventions and know-how.

Intangible assets can be either created by the enterprise itself or acquired. In the first case, you need to obtain a patent. For example, a company made an invention in the manufacturing industry and is actively using it. However, the discovery will not be included until a patent is granted. Another example: an organization uses the invention of another person. To obtain rights to it, you need to draw up an agreement for the transfer of an intangible asset.

The discovery may belong to the employees of the enterprise. In this case, an agreement on the execution of R&D is concluded with employees. The mere fact that an employee invented something does not mean that the discovery belongs to the enterprise.

Valuation of intangible assets

The principles for valuing intangible assets were invented by economist Leonard Nakamura, working in the United States. He proposed three main criteria for assessment:

- Estimated financial result. That is, you need to calculate how much profit the acquired or developed asset will bring.

- Costs associated with the creation or acquisition of intangible assets.

- Increase in operating profit due to the introduction of intangible assets.

IMPORTANT! The cost is determined based on the price of the item at the time of its receipt. Typically, the primary cost can be determined based on the concluded contract for the transfer of rights. They can be transferred to the company free of charge. In this case, the assessment is carried out based on the market value of similar objects.

The basis for the assessment may be the totality of costs associated with obtaining the asset. The list of expenses may include:

- amount paid to the seller;

- payment for intermediary services;

- receiving advice related to the acquisition of an asset;

- customs duties.

It will be more difficult to evaluate assets that were created by the enterprise itself. The price will include the following expenses:

- developer salaries;

- social Security contributions;

- material costs for carrying out development activities.

The original cost can only change when revalued or depreciated. For example, an organization bought a patent, the market value of which jumped. However, later there was a sharp decline. The value of the asset indicated in the accounting documents should be brought into line with its actual value.

How should the property be initially assessed?

The valuation of an intangible asset is the procedure for determining its value in monetary terms.

It is always carried out according to a regulated method, the choice of which depends on the situation.

The need to carry it out at an enterprise usually arises if it is necessary to solve a specific problem caused by the use of property rights that exist in relation to intellectual property objects or, alternatively, means of individualization.

Estimation of the value of an intangible asset is usually performed in the following typical situations:

- acquisition/creation of a business;

- liquidation of an enterprise (termination of activities);

- obtaining a bank loan on the terms of providing intangible assets as collateral;

- purchase/sale;

- execution of a license agreement;

- assignment of a fee for use (royalty payment);

- other tasks.

Methods

If the useful life of an asset exceeds 12 (twelve) months, the cost of such an object, current when it is entered into the organization’s economic balance sheet, is usually assessed using one of the following three methods:

- comparative (market) method;

- profitable way;

- expensive way.

Comparative (market) method

The essence of this approach is to determine the value of an intangible asset based on market prices of similar assets that have comparable utility.

This method is advisable to use for intangible assets, which are often objects of purchase/sale.

The prices of such transactions are used as input data. A sufficient number of market analogies taken into account in the assessment minimizes the possible error.

Income approach

This method is based on the organization's determination of future (expected) economic benefits brought by the useful operation of the asset being valued. We are talking about establishing the fair value of an object.

This valuation method is usually used when selling or otherwise disposing of property.

Within the income approach, the value of an asset is calculated using one of two calculation methods:

- discounting expected income (bringing their value to the current point in time);

- direct capitalization of projected income.

Expensive

If you follow this approach, cost is defined as the totality of documented expenses incurred by the organization in creating (developing), acquiring (purchasing) or otherwise obtaining the asset being valued.

Reflection of an intangible asset in accounting at its primary cost is carried out using the costly method of valuation.

The composition of the necessary costs when determining the primary value of an asset depends on the method of its receipt on the balance sheet of the enterprise-right holder (acquisition, creation, exchange, gratuitous receipt).

Order and features

The starting point when performing a valuation is its correct classification.

Evaluation procedures are carried out in accordance with methodological recommendations specially developed by authorized government bodies.

To reliably determine the value of an asset, a description of the corresponding object, title documents for intangible assets, and justification for its service life will be required.

Independent (external) specialists may be involved in performing the necessary procedures.

Rules for accounting for intangible assets

The unit of measurement of intangible assets is an inventory object. This term refers to the totality of all rights associated with the purchase of one asset. An object may include rights to a collection of objects.

Objects are recorded in account 04 “Intangible assets”. The accounting must indicate their original cost. The situation is somewhat more complicated with depreciation. In relation to some assets, it cannot be reflected on account 05 “Depreciation of assets”. Accruals are indicated in the credit column of account 4 “Intangible assets”. The receipt of objects into the enterprise is reflected in the debit of account 04. The correspondence will be account 08 “Investments in non-current assets”.

How to carry out subsequent assessment and accounting?

Subsequently, intangible assets are valued in much the same way as fixed assets.

You can choose one of two valuation models:

- Cost model: An intangible asset is stated at its historical cost less accumulated depreciation and accumulated impairment losses.

- Revaluation model: An intangible asset is stated at its fair value at the date of revaluation less any subsequent accumulated amortization and any subsequent accumulated impairment loss.

It should be added that the revalued cost model is rarely used for intangible assets, since for such assets there is usually no active market to determine fair value.

You cannot use the revalued cost model for brands, trade names, patents, trademarks and similar assets.

The reason is that these assets are very specific and unique, and are not traded on an active market.

The accounting entries for depreciation and revaluation are almost the same as for fixed assets.

Depreciation and useful life of intangible assets.

As with property, plant and equipment, depreciation is the distribution of the amortizable amount of an intangible asset over its useful life.

Here you need to define:

- How much to depreciate or amortized amount (cost - residual value),

- How long to depreciate or what is the useful life of the asset, and

- How to depreciate or what depreciation method to use.

There is one specific feature regarding the depreciation of intangible assets - this is the useful life (English 'useful life').

Intangible assets may have:

- 'finite useful life' : in this case you can estimate the life of an asset, for example for software, or

- Indefinite useful life : There is no predictable limit to the period over which the asset will generate cash flows. This applies, for example, to brands.

When you have an asset with an indefinite useful life, you SHOULD NOT depreciate it.

Instead, you should review the useful life of the asset at the end of each financial year and look for indicators of impairment.

Depreciation

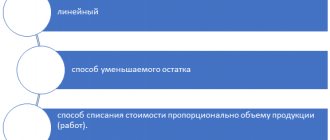

There are two methods used to calculate depreciation:

- Linear. The linear method takes into account depreciation rates determined on the basis of the period of use of the object.

EXAMPLE. The company acquired assets in the amount of 12,000 rubles. The period of use is 4 years. To calculate annual deductions, you need to divide the amount by the terms. Get 3,000 rubles. This amount can be divided by 12. This will determine the monthly deductions.

- Declining balance. Deductions are calculated based on the residual value at the beginning of the reporting period.

EXAMPLE. Assets were purchased for the amount of 10,000 rubles. To determine the annual rate, you need to divide 10,000 rubles by 100%. It will be 10%. The annual depreciation amount will be 1,000 rubles (10,000 times 10%). The residual value will be 9,000 rubles (10,000 – 1,000).

Intangible assets, despite the lack of physical form, must be correctly reflected in accounting. To do this, you need to know the signs of intangible assets and the rules for calculating depreciation charges.