Structure of the reporting form

Let us remind you that from 01/01/2017, the administration of the main part of insurance premiums passed to the tax inspectorates, therefore the current structure of the 4-FSS report differs from the version that was in effect previously. Unnecessary fields have been removed from it and new columns have been added.

Also see

“New form 4-FSS in 2021: .”

The procedure for filling out 4-FSS in force in 2021 indicates that the form of this report consists of the following sections:

- title page;

- Tables No. 1, 2 and 5 are required to be completed by all policyholders without exception;

- Tables No. 1.1, 3 and 4 are prepared for individual categories of employers for whom the conditions specified in the instructions are met.

Also see

The amounts received in rubles and kopecks are entered in line 1 (columns 3–6).

Then all payment amounts reflected under Kt 73 are collected:

- material aid;

- loans;

- other payments not related to the performance of work duties.

To these are added payments accrued under Kt 70, 76, but not subject to contributions in accordance with clause 20.2 of the law “On compulsory social insurance against accidents at work and occupational diseases” dated July 24, 1998 No. 125-FZ:

- benefits;

- compensation;

- reimbursement of expenses incurred by employees in connection with the performance of work duties, etc.

The calculated amounts of non-taxable payments are entered in line 2 (columns 3–6).

The final base for calculating contributions for injuries is determined as the difference between the values indicated in line 1 and the values in line 2 and is recorded in line 4 (columns 3–6).

Organizations and individual entrepreneurs, if they have employees with disabilities of groups I, II, III, allocate payments made in their favor in a separate line 4 (columns 3–6). The separate reflection of these payments is due to the fact that the insurance tariff for them is 60% of the generally established one (Clause 1, Article 2 of the Law “On Insurance Tariffs...” dated December 22, 2005 No. 179-FZ, Art. 2 of the Law “On Insurance Tariffs... " dated December 14, 2015 No. 362-FZ).

Next, information on the size of insurance rates is collected to calculate the final value of the insurance tariff, taking into account discounts (surcharges). In particular, from the notification received from the Social Insurance Fund, you need to take the amount of rates, premiums and discounts on insurance premiums.

4-

FSS - Table 6 of this document is filled out when collecting information to calculate the base for contributions for injuries. Who should fill out this table and what information is entered into it, read our article.

Contract agreement based on 4-FSS

4-FSS in 2020-2021, submit on form, approved. by order of the FSS of the Russian Federation dated September 26, 2016 No. 381.

You can see samples of filling out Form 4-FSS for different reporting periods, as well as a line-by-line algorithm for filling out a report in ConsultantPlus. If you do not have access to this legal system, a full access trial is available for free online.

In the calculation of the Social Insurance Fund, the contract with an individual is displayed in the table. 1, 2 and 5 (provided that the accident contributions are paid by the customer).

Filling out table 1

If the GPC agreement does not provide for the calculation of insurance premiums against accidents, payments under the GPC agreement do not need to be included in line 1 (amount of payments and remunerations) and line 2 (payments not subject to contributions).

Example.

Smiley LLC entered into a GPD agreement with the individual Artemenko A.Yu. for office renovation work. The amount of remuneration under the agreement is 30,000 rubles. Contributions for injuries according to the GPC agreement are not accrued.

When submitting Form 4-FSS, the accountant, having studied our article, came to the conclusion that information about Artemenko’s income does not need to be included in Table 1.

Let's change the conditions of the previous example and assume that, according to the GPC agreement, Smiley LLC pays insurance premiums from Artemenko's remuneration against accidents. Then information about Artemenko’s income should be included in tables 1, 2 and 5

In table 1 contract fees must be added to wage accruals and the total recorded on page 1 gr. 3, as well as in gr. 4–6 by three reporting months. The amount is fixed in the month when the work was accepted by the customer according to the acceptance certificate.

Filling out table 2

As already noted, contributions for injuries are charged by the customer only on the condition that this is fixed in the contract (clause 1 of article 20.1, clause 1 of article 5 of the law “On compulsory social insurance against industrial accidents and occupational diseases” dated July 24, 1998 No. 125 -FZ).

If there is no such obligation, then reflect it in the 2nd table. do not need anything.

If the obligation to pay such contributions is assigned to the customer, the contractor’s remuneration is recorded on page 2 of table. 2 in the appropriate columns.

Reporting.

Since when paying remuneration under a contract to an individual, obligations arise to pay the above taxes and fees, therefore there is a need to report on these payments and deductions.

- – based on the results of the calendar year – we provide certificates in form 2-NDFL; (annual report)

- – quarterly, starting from the quarter in which remuneration was paid under the contract, we provide a report in Form 6-NDFL; (quarterly report). We rent every quarter until the end of the current year;

- – also quarterly, in the sections of pension and health insurance – Calculation of insurance premiums. (quarterly report). We rent every quarter until the year ends;

- – form SZV-Mza every month of the contract. (monthly reporting);

- – SZV-STAGE form for the calendar year. (annual report)

How should payments under civil contracts be reflected in the calculation using Form 4-FSS?

Question to the auditor

The organization pays remuneration to individuals under civil contracts. How to reflect these amounts in the calculation using Form 4-FSS?

Table 3 of Section I “Calculation of the base for calculating insurance premiums” of the FSS Form-4 reporting reflects:

- payments subject to contributions to the Federal Social Insurance Fund of the Russian Federation for the purposes of insurance in case of temporary disability and in connection with maternity (including those exceeding the maximum base value);

- payments exempt from the calculation of contributions to the Social Insurance Fund of the Russian Federation in accordance with Art. 9 of Federal Law No. 212-FZ of July 24, 2009 (hereinafter referred to as Law No. 212-FZ);

- final basis for calculating contributions.

Based on Part 3 of Art. 9 of Law No. 212-FZ, contributions to the Social Insurance Fund of the Russian Federation are not subject to remuneration to individuals under civil law contracts. Such payments must be indicated on line 2 of Table 3 (broken down by month of the reporting period) (clause 10.2 of the Procedure for filling out the calculation, approved by order of the Ministry of Labor of Russia dated March 19, 2013 No. 107n).

Table 6 of Section II “Base for calculating insurance premiums” of reporting in Form 4-FSS indicates, in particular:

- payments in favor of employees who are subject to contributions to the Federal Social Insurance Fund of the Russian Federation “for injuries”. Reflected in columns 3 and 4 of Table 6.

- payments that are not subject to “injury” contributions. Reflected in column 5 of table 6.

- insurance rate;

- discount or surcharge to the tariff.

Contributions “for injuries” are calculated in accordance with the procedure provided for by Federal Law No. 125-FZ of July 24, 1998 (hereinafter referred to as Law No. 125-FZ). Based on Art. 20.1 of Law No. 125-FZ, accruals under civil contracts are subject to contributions only when this is stipulated in these contracts. Accordingly, if a civil contract does not contain such a requirement, then there is no object for taxation of contributions “for injuries”.

Based on clause 29.3 of the Procedure for filling out the calculation, column 5 of Table 6 indicates those payments that are exempt from contributions in accordance with Art. 20.2 of Law No. 125-FZ. However, this article does not mention payments under civil contracts.

Based on the above, we can draw the following conclusion. If the insurer pays remuneration to individuals under civil contracts (in which there is no provision for the payment of contributions “for injuries”), then such accruals:

- are not subject to contributions to the Social Insurance Fund of the Russian Federation for the purposes of insurance in case of temporary disability and in connection with maternity. Nevertheless, they are reflected in Table 3 of Section I of the calculation, since they are listed in Art. 9 of Law No. 212-FZ;

- are not subject to contributions to the Federal Social Insurance Fund of the Russian Federation “for injuries”. However, they are not indicated in Table 6 of Section II of the calculation, since payments of this kind in Art. 20.2 of Law No. 125-FZ are not listed.

For this reason, the amount of payments according to Table 3 and Table 6 of the reporting may not coincide.

This follows from the very procedure for filling out the calculation in form 4-FSS.

Contract agreement and insurance contributions to the Social Insurance Fund

A work contract is a type of civil law contract, the parties to which are the customer and the contractor (performer).

The contractor, on the instructions of the customer, performs one-time work, the results of which the customer undertakes to accept and pay for (Clause 1, Article 702 of the Civil Code of the Russian Federation). In this case, the contractor can be either an enterprise (IP) or an individual. If the contractor is an individual, then the customer must pay insurance premiums for compulsory pension and health insurance and withhold personal income tax.

For details, see the material “Contract and insurance premiums: taxation nuances.”

At the same time, in the Social Insurance Fund, in relation to contributions in case of temporary disability and in connection with maternity, such payments are non-taxable. And in terms of contributions for injuries, remuneration is subject to contributions only if such an obligation is fixed in the contract. In this regard, FSS inspectors often enter into legal proceedings with customer companies, trying to reclassify a contract with an individual into an employment relationship in order to collect arrears on insurance premiums, as well as penalties and fines.

Thus, payments under the contract are not reflected in 4-FSS. They need to be recorded in the report only if this is provided for in the GPC agreement.

Payments under what other civil contracts may be subject to contributions for injuries, find out in ConsultantPlus. Trial access to the legal system is free.

How to draw up a contract correctly and avoid claims from inspectors, read here.

Occupational Safety and Health (OSH)

THE OCCUPATIONAL SAFETY MANAGEMENT SYSTEM (OHS) is also an important part of the organization’s management system.

She manages health and safety risks in the organization.

The OSMS includes:

- organizational structure;

- planning activities;

- distribution of responsibility;

- procedures for the development, implementation, achievement of goals, analysis of the effectiveness of occupational safety policies and measures in an organization (GOST R 12.0.006–2002 “General requirements for occupational safety management in an organization”).

We will compile the necessary minimum according to the legal requirements for an OSMS.

Personnel, labor protection. VIKING

Personnel accounting.

A set of necessary documents for maintaining records of an organization’s employees is personnel records.

On its basis, hiring and dismissal, recording of vacations, sick leave, absenteeism, attendance and everything related to personnel is carried out.

Based on these data, wages, sick leave, benefits, vacation pay and other payments in favor of individuals within the framework of labor law are calculated.

The procedure for maintaining personnel records is monitored by the Federal Labor Service - FST. It has territorial branches of the GIT (state labor inspectorate).

Personnel is a fairly capacious section of an organization’s office work, so small businesses do not pay due attention to this due to the high costs of maintaining personnel services.

We will help you cope with this since we take full responsibility for personnel records within the framework of contracts for accounting services.

If you indicate GPH in the 4 FSS report, how to fill out the example

— — Form 4-FSS and the procedure for filling it out were approved by Order of the FSS of the Russian Federation dated September 26, 2016 No. 381 (hereinafter referred to as the Procedure).

In accordance with clauses 7.1 and 7.2 of the Procedure, table 1, line 1 reflects the amounts of payments and other remuneration accrued in favor of individuals in accordance with Article 20.1 of Law No. 125-FZ. And in line 2, the corresponding columns reflect the amounts that are not subject to insurance premiums in accordance with Article 20.2 of Law No. 125-FZ.

We read Article 20.1 of Law 125-FZ. 1. The object of taxation with insurance premiums is payments and other remuneration accrued by policyholders in favor of the insured within the framework of labor relations and civil contracts, the subject of which is the performance of work and (or) provision of services, author’s order agreements, if in accordance with these agreements the customer is obliged to pay insurance premiums to the insurer.

Those.

Other calculation sheets

The remaining sections are filled out optionally, subject to the conditions specified in the instructions. For example, part 3 is addressed to employers who, in the reporting quarter:

- preventive measures were carried out;

- benefits were paid to employees who were injured at work.

For more information, see

“Table 3 of Form 4-FSS: filling out.”

In turn, the 4th table is intended for companies that have had accidents at work.

For more information about this, see “Filling out Table 4 of Form 4-FSS.”

Compliance with the current procedure for filling out 4-FSS for 2021, set out in the regulations of the Social Insurance Fund, will protect the employer from unnecessary problems and clarifications, and the imposition of penalties.

Also see

In this regard, in addition to the conditions for payment of contributions, the contract must clearly state the amount of payments based on the results of work and the amount of expenses reimbursed to the individual contractor for materials, services, etc.

How to fill out table 6 of section 2 of form 4-FSS correctly?

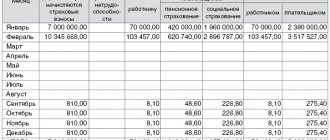

Completing Table 6 in 4-FSS begins with collecting information on all payments made in favor of employees for the reporting period. This information is collected from analytical cards for accounts 70 and 73 (if employers are organizations, individual entrepreneurs) or payroll statements (if employers are individuals). In relation to employees registered under a GPC agreement, information is taken from the cards under account 76 - only in terms of payments for which the employer must pay “traumatic” contributions.

First, all payments to employees displayed under Kt 70, 73, 76 are analyzed and summed up. The results are summed up for each month of the past quarter and for the period being calculated as a whole.

Contributions are calculated regardless of the payment amount.

Contributions are calculated simultaneously with the calculation of payments under the GPA. This is not necessarily the last day of the month. There may be any other date, because payment under a civil contract is made after signing the act. The procedure takes place according to the schedule approved by the contract. Or calculations as work is completed (delivered) or services are provided (accepted). Monitor the primary in a timely manner. The documents must be duly signed. And carry out the accounting operation in a timely manner.

Enter all amounts in the contribution registers. In the case of accidental payments, keeping registers is not required by law. Enough information from analytical accounting accounts. But we recommend unifying accounting. And along with accruals to the Federal Tax Service, record all contributions to the fund.

Fill out reports based on information from the registers. For injury contributions, this is Form 4-FSS to the Social Insurance Fund.

Once you have calculated the amounts, you do not need to pay anything directly to the budget. Wait until the end of the reporting month. Transfer contributions to the budget no later than the 15th of the month in which they were accrued. In a month when the 15th day falls on a weekend or state holiday, the extreme point is moved to the next working day.

Such transfers in 2021 take place in three months: June, September and December. We do not recommend waiting until the last date.

Example 1 on contributions from payments under GPC agreements in 2021

PromoLine LLC cooperates with individuals on GPA.

The agreement provides for insurance of a person in the Social Insurance Fund.

Under the terms of the agreement, the company pays the person a remuneration in the amount of 50,000 rubles within a month after completion of the work.

The work was submitted on January 18, 2021. The full amount of the reward was transferred to the contractor’s card on February 18.

As of January 18, 2021, the organization’s accountant calculated and accrued amounts from the contract to the Social Insurance Fund at the company rate of 1.2% in the amount of 600 rubles.

(50,000 rub.

Unlike payments under employment contracts, in the case of GPA, deductions are not available for all types of insurance. There is no social insurance in the Federal Tax Service in case of temporary disability and in connection with maternity. And as a general rule - to the Social Insurance Fund in case of injury. In this regard, the question arises whether it is necessary to show payments under GPC agreements in the 4-FSS reporting for 2021 and reporting periods. Details are in the article.

Procedure for filling out 4-FSS for the 2nd quarter of 2021

Recommendations for filling out 4-FSS are given in Order of the FSS of the Russian Federation dated September 26, 2016 N 381.

To submit the 4-FSS calculation, all policyholders need to fill out the title page and tables 1, 2, 5. These sheets are submitted even if the company did not have accruals for contributions in the reporting period. If the relevant indicators are available, sheets 1.1, 3 and 4 should also be completed.

To the title page

data about the reporting period and detailed information about the company are entered: TIN, KPP, OGRN (OGRNIP), name, address, average number of employees for the six months (calculated in the usual manner), etc.

Table 1

serves to calculate the base for insurance premiums - cumulatively from the beginning of the year and separately for each of the last three months of the reporting period. Line 9 indicates the amount of the insurance rate, determined taking into account the discount or surcharge.

table 2

shows the status of settlements with the Social Insurance Fund for contributions to injuries for the reporting period. Information is entered according to accounting data: debt on insurance premiums at the beginning and end of the billing period (pages 1, 19), accrued and paid amounts of contributions (pages 2, 16), accident insurance expenses since the beginning of the year (page 15) etc.

If in January-June benefits were paid for work-related injuries or other costs that can be offset against injury contributions, you must fill out Table 3

.

If an accident occurs at work, the information must be entered in table 4

.

Table 5

information is reflected based on the results of a special assessment of working conditions and mandatory medical examinations of employees. The indicators are entered as of the beginning of the year, so this section will be the same in calculations for different periods of the same calendar year.

Recommendations and examples of filling out the 4-FSS calculation - in a free collection

materials from ConsultantPlus “4-FSS. Contributions for injuries calculation, payment.”

Contract with an individual – changes for 2021

A contract, in essence, means that a certain person has contracted to perform a certain set of services or some work within a specified period for a specified amount.

The applied insurance rates are identical: Documents on the basis of which payments are made and insurance premiums are calculated under civil-processing agreements. The civil law relationship between the customer and the contractor is determined by 2 key documents: the civil-processing agreement and the act of acceptance and transfer of work performed.

In 2021, some changes were made to such agreements. A work contract can be concluded in two forms: Distinctive features of such an agreement are: Since the managers of some companies are trying to avoid additional tax burden on employee wages, the practice of concluding work contracts instead of an employment agreement has come into practice.

But since 2021, everything has changed. Previously, the difference between an employment agreement and a work contract was the qualitative approach to the form of payment for an employee and his registration for work.

In rare cases, they are required to provide a military ID or registration certificate if the employee has not reached conscription age, educational documents, and a certificate of health, including from a psychiatrist or narcologist.

Results

Despite the obvious attractiveness of using GPA agreements due to the possibility of charging insurance premiums for the payments they provide for in a smaller amount, their legal component requires accuracy in the wording of the terms of the agreement.

For an accountant, the presence of freelance workers will mean the need to carefully collect and study documents confirming the possibility of non-payment of insurance premiums, as well as work together with a lawyer to exclude language from civil liability agreements that implies negative consequences for the business.

The amounts of remuneration and contributions to Social Insurance under the contract are not displayed in the 4-FSS calculation. Contributions for injuries are accrued only if this condition is fixed in the contract.

It is for this reason that the possibility of reclassifying such a contract into an employment contract should be excluded. Accrual of other insurance premiums (for compulsory health insurance and compulsory medical insurance) is carried out at generally established or reduced (if there is a right to apply them) rates.

Tags: certificate of completion, accountant, Contract, personnel, tax, order, expense, dismissal, Form

Taxes and insurance premiums under a civil contract

The withholding of personal income tax from an employee’s income and the calculation of insurance premiums depend on who is the executor of the contract. If the executor of the contract is an individual who is not an entrepreneur, then the customer will have to independently:

- accrue insurance premiums for the remuneration paid in compulsory health insurance, compulsory medical insurance and insurance against industrial accidents (if this is provided for by the contract itself, in accordance with clause 1 of article 20.1 of law No. 125-FZ);

- withhold personal income tax from his income as a tax agent.

Individual entrepreneurs and companies that have entered into a civil law agreement pay taxes and contributions independently, depending on the applicable tax system.