As is known, in the personalized information submitted to the Pension Fund under the RSV-1 (approved by Resolution of the Pension Fund Board of January 16, 2014 No. 2p), the policyholder, among other things, indicates information about the length of service of the insured person in subsection 6.8 “Period of work for the last three months of the reporting period " If the employee honestly worked all these three months, then in this subsection it is enough to enter only the start and end dates of work, which will coincide with the start and end dates of the last expired quarter. But if the employee was on leave without pay, parental leave, etc., then the corresponding period of time must be marked in the table with a certain code.

For the purpose of reflecting periods of work in RSV-1, many codes are used (for the correct calculation of length of service) - NEOPL, ACCOUNTING, etc. Let's look at the NEOPL code in personalized accounting.

NEOPL code in the Pension Fund: decoding

The NEOPL code in individual information means that for the specified period of time the employee did not receive money in wages. The reasons for this may be different, so the policyholder must enter the same NEOPL code in the RSV-1 in different situations.

Thus, the code NEOPL is used to denote ():

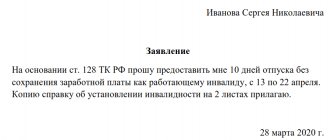

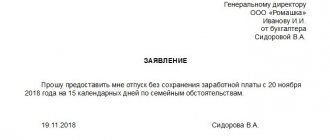

- leaves without pay (Article 128 of the Labor Code of the Russian Federation);

- period of downtime due to the fault of the employee (Article 157 of the Labor Code of the Russian Federation);

- unpaid period of suspension from work / non-admission to work (Article 76 of the Labor Code of the Russian Federation);

- unpaid leave provided to teaching staff (Article 335 of the Labor Code of the Russian Federation);

- an additional day off per month without pay, provided to women working in rural areas (Article 262 of the Labor Code of the Russian Federation);

- unpaid time for participating in a strike (Article 414 of the Labor Code of the Russian Federation);

- other unpaid periods, except for periods with codes DLDETI and Chernobyl NPP.

As you can see, in reporting submitted to the Pension Fund, NEOPL is a frequently encountered code.

Neopldog in personalized accounting

Despite the obvious similarity of the NEOPLDOG codes, it is indicated in individual information in a completely different case: in relation to the period of work performed by the contractor under a civil law contract, in which remuneration was not accrued and will be paid later (Table “Calculation of the insurance period: additional information” of Appendix No. 2 to the Procedure for filling out RSV-1). Let's explain with an example.

Let’s say the GPA for the execution of work was concluded on August 22, 2016. The contract states that the contractor must begin work on September 1, 2021. The certificate of completion of work was signed on October 13, 2021, and at the same time the contractor was awarded remuneration. Then the period from September 1 to September 30 should be marked with the code NEOPLDOG in subsection 6.8 of the RSV-1 for this performer. And the period from October 1 to October 13 - the code is AGREEMENT.

The organization has one employee on staff - the director. Salary is not accrued. The SZV-M report is submitted monthly to the pension fund. Filling out a zero calculation for strass contributions and submitting it to the Federal Tax Service.

Question:

In the LLC, the employment contract is concluded only with the director and he is on unpaid leave (SZV-M is submitted to him monthly). No salary is paid. How can this be reflected in the calculation of insurance premiums? (If you indicate in section 3 only the personal data of the director, and the rest are “0”, then the program generates errors)

Answer:

When calculating the director's insurance premiums, include in lines 010 of subsections 1.1 and 1.2, 010 of Appendix 2. Fill out subsection 3.1. Do not fill out subsection 3.2. In practice, special operator programs show an error if subsection 3.2 is missing. But the inspectorate accepts the calculation with such an “error”.

Rationale

How to prepare and submit a calculation of insurance premiums to the Federal Tax Service

Situation:

Is it necessary to reflect in section 3 of the calculation of insurance premiums to the Federal Tax Service information on the director, the only founder, who does not receive a salary?

Yes need.

The sole founder director is the insured person. Therefore, regardless of whether his salary was calculated, fill out section 3 for the director and include him in the number of insured employees. These conclusions follow from paragraph 1 of Article 7 of the Law of December 15, 2001 No. 167-FZ, paragraph 1 of Part 1 of Article 2 of the Law of December 29, 2006 No. 255-FZ, paragraph 1 of Article 10 of the Law of November 29, 2010 No. 326-FZ, paragraphs 22.1 -22.36 The procedure approved by order of the Federal Tax Service of Russia dated October 10, 2021 No. ММВ-7-11/551.

The Pension Fund verifies the SZV-M and the calculation of contributions

Information about the founding director

The Pension Fund of Russia will verify the information about the founding director that you indicated in the SZV-M reports and the calculation of contributions. The fact is that the company is obliged to submit a zero calculation for contributions, even if it did not conduct business (letter of the Ministry of Finance of Russia dated March 24, 2017 No. 03-15-07/17273).

In the zero calculation for the first quarter of 2021, you filled out section 3 for the founding director. If there were no accruals in his favor, you filled out only subsection 3.1. Inspectors will pay attention to line 160.* In it you indicated the characteristics of the insured person, depending on whether or not an employment or civil law contract was concluded with the director.

An agreement has been concluded with the founding director.

In this case, the director is classified as an insured person in the compulsory pension insurance system. In line 160 you must indicate attribute 1 (see sample 3 below).

Sample 3. Attribute of the insured person in the calculation of contributions

If, during reconciliation, the Pension Fund discovers that you have not submitted SZV-M reports for January, February and March to the director, the company will be fined 1,500 rubles. (500 rub. ? 3). In addition, the fund will fine the director up to 500 rubles. (Article 15.33.2 of the Code of Administrative Offenses of the Russian Federation).

There is no contract concluded with the founding director.

A director without an employment or civil law contract is not an insured person in the compulsory pension insurance system. In line 160 you must enter the insured person's attribute 2.

Let’s assume that you filled out Section 3 of the contribution calculation with feature 2 for the director, but did not submit SZV-M reports on it. When reconciling reports, the Pension Fund discovered this. No one will ask you for explanations. You have the right not to submit SZV-M reports, because the company does not have insured persons (

What is the procedure for filling out section 3 of the calculation of insurance premiums in 2021, submitted to the Federal Tax Service? How many sections 3 should I fill out? Do I need to fill out 3 for each employee? You will find answers to these and other questions, as well as an example of filling out Section 3, in this consultation.

Question

Based on the text of the question, there were three employees, two employees were laid off in the third quarter. In the calculation of insurance premiums, in column 1 of line 010 of subsection 1.1, indicate “3”, in column 2 of line 010 of subsection 1.1, indicate “1”, in columns 3, 4, 5, also indicate “1”. Similarly, fill out line 010 of subsection 1.2 and line 010 of appendix 2. In section 3, indicate all three employees. For them, fill out only subsection 3.1

Answer

On line 010, indicate the total number of insured persons in the compulsory pension insurance system.* On line 020 - the number of individuals from whose payments you calculated insurance premiums. And on line 021 - the number of individuals from line 020 whose payments exceeded the maximum base for calculating pension contributions.

Download a sample of filling out the RSV. Zero RSV: download example of filling. Letter from the Federal Tax Service from Recommendations on the topic. Articles on the topic. Calculation of insurance premiums for the 2nd quarter of the year form. Deadline for submitting calculations for insurance premiums for the 2nd quarter of the year. Appendix 3 to section 1 of the calculation of insurance premiums for the year.

Tax officials did not have time to change the form of calculation of insurance premiums for reporting for the 1st quarter. But even without the new form there are other changes. Read how to fill out the RSV for the 1st quarter of the year, is there a new form, and what has changed since the year. Tax officials planned to change the form of calculation of insurance premiums. Already in the first quarter of the year, policyholders had to use the new form. But by the beginning of March the draft had not been adopted, which means that the new form was not ready for the DAM for the 1st quarter of the year.

DAM for half-year 2021: filling features and common errors

If payments in favor of employees are subject to additional pension insurance rates, fill out subsection 1. The necessary codes are indicated in the report form itself. The rest of the sheet is filled out in the same order as the previous two subsections. In the second appendix, provide the calculation of contributions to the Social Insurance Fund in case of disability and maternity.

Hello! Please help me figure it out. Since January, the company has employed 7 people under employment contracts. One employee was on leave at his own expense from September 1 to September 30. In SZV-M for September I showed 7 people. But the number of insured persons does not correspond to line 020 of subsection 1.1 of the calculation of contributions. The employee, who was on leave at his own expense, had no payments, and I did not accrue contributions.

What is section 3 for and who fills it out?

In 2021, a new form of calculation for insurance premiums will be used. The form was approved by order of the Federal Tax Service of Russia dated October 10, 2021 No. ММВ-7-11/551. Cm. " ".

This reporting form includes section 3 “Personalized information about insured persons.” In 2021, section 3 as part of the calculation of contributions must be filled out by all organizations and individual entrepreneurs that have paid income (payments and rewards) to individuals since January 1, 2017. That is, section 3 is a mandatory section.

If an employee is on leave without pay RSV 2021

Answer: and filling out the calculation of insurance premiums (hereinafter referred to as the Procedure) were approved by order of the Federal Tax Service of Russia dated October 10, 2016 No. If the employer (organization or entrepreneur) did not carry out activities during the reporting (calculation) period and did not make payments to individuals, it is necessary to submit “zero” calculation (see letter of the Ministry of Finance of Russia dated March 24, 2020 No. 03-15-07/17273). According to the Procedure, all payers submit as part of the calculation (, ):

RSV-1: reflecting non-standard situations

The vacation schedule establishes the order of provision of paid vacations for the next year. Therefore, all employees of the organization who, at the time of drawing up the schedule, are entitled to annual paid leave in the next year must be included in it.

Column 8 of the SZV-STAZH form is filled out in accordance with the Classifier of territorial conditions codes used when filling out personalized reporting.” The code in column 8 is indicated if the employee has the right to early retirement due to territorial conditions, for example:

Let us remind you that the form can be submitted on paper (without an electronic version of the report) if the company employs 24 or fewer people. Otherwise, providing reports in electronic format is the responsibility of the policyholder.

Conditions for early assignment of an insurance pension, basis (code)

- territorial conditions (code) (column 8);

- special working conditions (code) (column 9);

- calculation of insurance period, basis (code) (column 10);

- calculation of insurance period, additional information (column 11);

- conditions for early assignment of an insurance pension, basis (code) (column 12).

The code “Neopldog” means the period of work of the insured person under contracts that do not provide for his employment, payment for which will be made in the following reporting periods. These include rental agreements, contract agreements, transportation agreements, storage agreements and others. This code takes into account the period of a person’s work, payments and other remuneration.

New reporting to the Russian Pension Fund became mandatory only in 2021. Now insurance companies are required to report annually on all employees and specialists who worked during the reporting period.

Who to include in section 3

Section 3 provides for the inclusion of personalized information for each individual in relation to whom in the last three months of the reporting (calculation) period the organization or individual entrepreneur was the insured. It does not matter whether during this period there were payments and rewards in favor of such individuals. That is, if, for example, in January, February and March 2021, an employee under an employment contract was on leave without pay, then this should also be included in section 3 of the calculation for the 1st quarter of 2021. Since during the designated period of time he was in an employment relationship with the organization and was recognized as an insured person.

Of course, it is necessary to formulate section 3 for persons in whose favor in the last three months of the reporting period there were payments and remunerations under employment or civil law contracts (clause 22.1 of the Procedure for filling out calculations for insurance premiums, approved by order of the Federal Tax Service of Russia dated October 10, 2021 No. MMV -7-11/551).

Let us assume that during the reporting period a civil contract (for example, a contract) was concluded with an individual, but the person did not receive any payments under this contract, since the services (work) have not yet been provided (performed). In this case, is it necessary to include it in section 3 of the calculation of insurance premiums? In our opinion, yes, it is necessary. The fact is that those employed under civil contracts are also recognized as insured persons by virtue of paragraph 2 of clause 1 of Article 7 of the Federal Law of December 15, 2001 No. 167-FZ “On Compulsory Pension Insurance”.

We also believe that section 3 should be formed for the general director, the only founder with whom the employment contract has been concluded. After all, such persons are also named in paragraph 2 of paragraph 1 of Article 7 of the Federal Law of December 15, 2001 No. 167-FZ “On Compulsory Pension Insurance”. Therefore, they should fall under section 3. Even if they did not receive any payments from their own organization in the last three months of the reporting period.

Subsection 6.6

Fill out subsection 6.6 in forms with the “original” information type if in the last three months of the reporting period the data presented in previous reporting periods were adjusted.

If there is data in subsection 6.6, then it is mandatory to submit corrective (cancelling) sections 6 of the calculation and (or) forms SZV-6-1, SZV-6-2, SZV-6-4.

In this case, submit corrective (cancelling) information using the individual (personalized) accounting forms that were in force in the period for which errors were identified.

When correcting information about the amounts of recalculation of insurance premiums, please indicate:

- for reporting periods starting from the first quarter of 2014 - in column 3 of subsection 6.6;

- for the reporting periods 2010–2013 - in columns 4 and 5 of subsection 6.6.

How to fill out section 3: detailed analysis

Initial part

If you are filling out personalized information for a person for the first time, then enter “0–” on line 010. If you are submitting an updated calculation for the corresponding billing (reporting) period, then show the adjustment number (for example, “1–,” “2–,” etc.). In field 020, reflect the code of the billing (reporting) period, for example:

- code 21 – for the first quarter;

- code 31 – for half a year;

- code 33 – for nine months;

- code 34 – per year.

In field 030, indicate the year for the billing (reporting) period of which personalized information is provided.

Check

The value of field 020 of section 3 must correspond to the indicator of the field “Calculation (reporting period (code)”) of the title page of the calculation, and field 030 of section 3 - the value of the field “Calendar year” of the title page.

In field 040, reflect the serial number of the information. And in field 050 – the date of submission of information. As a result, the initial part of section 3 should look like this:

Subsection 3.1

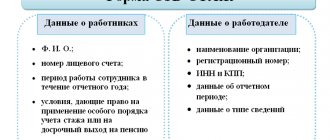

In subsection 3.1 of the calculation, indicate the personal data of the individual for whom section 3 is being filled out. We will explain what personal data to indicate and provide a sample:

| Line | Filling |

| 060 | TIN (if available) |

| 070 | SNILS |

| 080, 090 and 100 | FULL NAME. |

| 110 | Date of Birth |

| 120 | Code of the country of which the individual is a citizen from the Classifier approved on December 14, 2001 No. 529-st, OK (MK (ISO 3166) 004-97) 025-2001 |

| 130 | digital gender code: “1” – male, “2” – female |

| 140 | Identity document type code |

| 150 | Details of the identity document (series and document number) |

| 160, 170 and 180 | Sign of an insured person in the system of compulsory pension, medical and social insurance: “1” – is an insured person, “2” – is not an insured person |

Subsection 3.2

Subsection 3.2 contains information about the amounts:

- payments to employees;

- accrued insurance contributions for compulsory pension insurance.

However, if you are filling out section 3 for a person who has not received any payments in the last 3 months of the reporting (settlement) period, then this subsection does not need to be filled out. This is stated in paragraph 22.2 of the Procedure for filling out calculations for insurance premiums, approved by order of the Federal Tax Service of Russia dated October 10, 2021 No. ММВ-7-11/551. If the fact of payments took place, then fill out the following fields:

| Count | Filling |

| 190 | |

| 200 | Category code of the insured person (according to Appendix 8 to the Procedure for filling out the calculation). Enter the code in capital letters of the Russian alphabet. For example - HP. |

| 210 | The total amount of payments in favor of an individual for the first, second and third months of the last three months of the billing (reporting) period, respectively. |

| 220 | The basis for calculating pension contributions, not exceeding the maximum value. In 2021, this value is 876,000 rubles. |

| 230 | The amount of payments under civil contracts (allocated from the database). |

| 240 | Amount of pension insurance contributions. |

| 250 | The total amount of payments in favor of the employee, not exceeding the maximum base amount for all three months of the reporting (billing) period. |

Let's give an example.

Example

Lobzik and Company LLC is preparing calculations for insurance premiums for the 1st quarter of 2021. In section 3, the accountant needs to include data on mechanic O.V. Romashkin. In January, February and March 2021, he received 30,000 rubles monthly. The accountant included the entire amount in the base for calculating insurance premiums. The accountant filled out subsection 3.2 as follows:

If you apply different insurance premium rates, fill out the required number of lines.

Subsection 3.2.2

In subsection 3.2.2, reflect the payments from which pension contributions were calculated at additional tariffs. The transcript of this section is as follows:

| Count | Filling |

| 260 | The serial number of the month in the calendar year (“01”, “02”, “03”, “04”, “05”, etc.) for the first, second and third month of the last three months of the billing (reporting) period, respectively. |

| 270 | Tariff code. |

| 280 | Amounts of payments from which contributions at additional tariffs were calculated. |

| 290 | Amount of insurance premiums at additional rates. |

| 300 | The total amount of payments and insurance premiums. |

What general principles should be used to formulate section 3 of the unified calculation of insurance premiums in 2021? Who exactly should provide this part of the report put into effect by Order No. ММВ-7-11/ dated 10.10.16? And is it possible to submit a blank section 3 of the calculation of insurance premiums? Current answers to these and other questions follow.

Filling out the zero DAM for the 1st quarter of 2021

The delivery of a zero RSV also follows the usual rules. It must be sent to the tax authority on time (for the 1st quarter of 2021 it expires on 04/30/2020). Late submission results in a fine, which in its minimum possible amount (RUB 1,000) will be charged even in the absence of digital indicators in the main sections of the report (clause 1 of Article 119 of the Tax Code of the Russian Federation).

Where to download a sample of filling out the zero RSV for the 1st quarter of 2020

The report (during the year compiled on an accrual basis) will be completely zero (that is, with zeros in all fields corresponding to the digital indicators of accruals) only when there is no activity at the beginning of the year. Because of this, the most often created with zero data is the DAM generated for the 1st quarter. The appearance of data in later periods of the year automatically transfers the report to the non-zero category.

In line 220 (the basis for calculating contributions), do not include income that is not subject to insurance contributions. The general list of non-taxable income is given in Art. 422 of the Tax Code of the Russian Federation. Also take into account the explanations of officials and courts. We have collected some of them in a table:

- Russian companies (LLC, JSC), as well as their branches;

- foreign enterprises operating in the Russian Federation;

- entrepreneurs and heads of peasant farms-employers;

- individuals who are not registered as individual entrepreneurs, but pay income to hired employees.

Fill out Appendix 2 to Section 1

In the finished calculation, put the number of each page in the “Page” field. Calculation pages have continuous numbering, starting with the title page. And it doesn’t matter how many sections you filled out, which ones you included, and which ones you skipped. The number for the first page is “001”. This is stated in clauses 2.1-2.21 of the Procedure approved by Order of the Federal Tax Service dated October 10, 2016 No. ММВ-7-11/551.

If the policyholder submits the report later than the due date, he will be fined. The fine is equal to 5% of the contributions reflected in the report. It is charged for each full and partial month of delay. At the same time, you will not be able to pay a fine of less than 1,000 rubles, but you will not be punished for more than 30% of the contributions.

This is interesting: Comparative table of kvr and kosgu from 2021 latest news

What is section 3 of the unified calculation of insurance premiums intended for?

Detailed section 3 of the new calculation of insurance premiums is compiled in order to provide personalized information for all insured individuals. The frequency of submission of this report is quarterly, therefore all business entities that have entered into employment contracts with staff must include section 3 in the current calculation of insurance premiums - a sample is given below. At the same time, the fact of issuing money in this case is not of key importance.

When exactly is it necessary to fill out section 3 of the calculation of insurance premiums:

- If settlements are made with employees within the framework of labor or civil relations (clause 22.1).

- When specialists are on vacation without saving their earnings.

- When employees go on maternity leave, in the calculation of insurance premiums, section 3 for the maternity leave is drawn up without the formation of a subordinate. 3.2 about payments.

- If the company has only one employee, he is also the director, who is the founder.

- If settlements were made with dismissed persons in the current quarter.

Important! If the policyholder submits to the regulatory government agencies a calculation of insurance premiums without section 3, such a report will be considered incomplete, which will entail a refusal to accept the document.

Filling out section 3 of the calculation of insurance premiums in 2017

Full instructions for entering information into section 3 of the calculation of insurance premiums are in the Procedure for filling out the report regulated by order MMV-7-11 / Separate recommendations are given by the Federal Tax Service in letter No. BS-4-11/4859 dated March 17, 2017. Coding algorithm for line 040 Section 3 of the calculation of insurance premiums is explained in detail in letter No. BS-4-11/ dated January 10, 2017.

Rules for filling out section 3 of calculation of insurance premiums:

- Information is entered separately for each insured individual.

- At the top, initial data is formed - by corrective number (in case of clarifications), reporting period, reporting number and date.

- It is mandatory to reflect personal personalized information in other information. 3.1 – TIN, SNILS of a person, his full name, citizenship, exact date of birth, identity document number, attribute code in the insurance system.

- Other 3.2.1 is formed only if there are various payments to citizens in the reporting period - for example, section 3 of the calculation of insurance premiums for the employee’s maternity leave is provided without this part (subclause 22.2).

- Other 3.2.2 is formed when calculating contributions for compulsory pension insurance in terms of additional tariffs.

Important! If the zero section 3 of the calculation of insurance premiums is presented, “0” is entered in the corresponding lines with monetary indicators, and dashes in the rest. If payments were made on sick leave, the benefits in section 3 in the calculation of insurance premiums must be entered in page 210 sub. 3.2.

How to fill out section 3 of calculating insurance premiums - example

Using the initial data, we will analyze exactly how to form section 3 for 1 sq.m. 2021 Let’s assume that an LLC under the general tax regime is engaged in the wholesale trade of electrical equipment. There is 1 employee on staff, whose salary is 45,000 rubles. per month. There are no contract workers. In Sect. 3, data is entered for one specialist; accordingly, if there is more staff, information for each individual should be filled out separately.

Sample of filling out section 3 of the calculation of insurance premiums

Attention! Often when filling in for employees who were on unpaid leave in the current quarter ,

Section 3 of calculation of insurance premiums in 1C is not formed correctly, because the program automatically indicates empty values for all lines. To rectify the situation, experts recommend accountants to enter monthly indicators in subdivisions. 3.2.1 with zero amounts. After this, the program skips the report and it can be promptly sent to the Federal Tax Service.

“Neopl” in personalized accounting is one of the codes whose inclusion in reporting documents based on length of service is mandatory. Let's look at how these codes are used in 2019.

How to fill out the RSV for the 1st quarter of 2021

- “08” - payers of insurance premiums who apply the simplified tax system, and whose main type of economic activity is specified in subparagraph 5 of paragraph 1 of Article 427 of the Tax Code;

- “09” - payers of insurance premiums who pay UTII and have a license for pharmaceutical activities - in relation to payments and remunerations made to individuals who have the right to engage in pharmaceutical activities or are allowed to engage in it;

- “12” - payers of insurance premiums - individual entrepreneurs on the PSN in relation to payments and rewards accrued in favor of individuals engaged in the type of economic activity specified in the patent, with the exception of individual entrepreneurs carrying out the types of business activities specified in subparagraphs 19, 45 - 47 of paragraph 2 articles 346.43 Tax Code.

This is interesting: Sample of filling out 3 personal income tax for 2021 for dental treatment for a child

DAM and beneficiaries

4. Appendix 6 “Calculation of compliance with the conditions for applying a reduced rate of insurance premiums by payers specified in subparagraph 5 of paragraph 1 of Article 427 of the Tax Code of the Russian Federation” to section 1 of the DAM is not completed.

- availability of time for a subordinate to resolve personal matters;

- during such leave, the employee’s workplace is maintained without making any adjustments to the employment agreement;

- the amount of wages does not change.

Personalized accounting

Personalized accounting is intended to summarize the data on the personal account of each employee (from the moment of his employment) for the insurance and funded parts of the pension. Data on his work experience is recorded on the same account.

The main regulatory documents for such accounting are:

- Law “On individual (personalized) accounting in the compulsory pension insurance system” dated April 1, 1996 No. 27-FZ;

- Resolution of the Pension Fund of the Russian Federation “On the forms of individual (personalized) accounting documents in the compulsory pension insurance system and Instructions for filling them out” dated July 31, 2006 No. 192p.

The source of data for personalized accounting is information submitted by employers.

Features of personalized reporting in 2021

Starting from 2021, reporting regarding the calculation of insurance premiums (including those intended for the Pension Fund of Russia) is submitted to the tax authorities. The calculation of contributions, which combines information on all types of contributions transferred under the control of the Federal Tax Service, contains a section devoted to personalized data. However, these data only include information on accrued income for the period and related contributions. There is no information about experience in them.

Reporting on length of service is submitted at the end of the year directly to the Pension Fund of the Russian Federation before March 1 (clause 2 of Article 11 of Law No. 27-FZ of April 1, 1996). For it, by resolution of the Board of the Pension Fund of December 6, 2018 No. 507p, a new form SZV-STAZH was approved, in which for information about length of service a table is provided, similar to that included in the expired form RSV-1.

IMPORTANT!

From 01/01/2019 it is necessary to use the new forms SZV-STAZH and EDV-1, approved.

Resolution of the Board of the Pension Fund of December 6, 2018 No. 507p. Resolution of the Pension Fund Board of January 11, 2018 No. 3p, according to which personal reporting has been submitted until now, has lost force. You can download the updated forms. By the way, before the end of the year, the liquidating organization and the individual entrepreneur deregistering must submit the SZV-STAZH.

Resolution No. 507p approved the rules for filling out the new form and the formats for submitting it to the Pension Fund. The text of the rules contains a reference to the same codes that were used when filling out personalized information in the RSV-1.

Vacation code in SZV-STAZH

The provisions approved by the Resolution of the Board of the Pension Fund of December 6, 2020 No. 507p apply from January 1, 2021. They must be followed when filling out information about experience for 2021. The deadline for submitting the SZV-STAZH reporting form for 2021 is March 1, 2021. Changes are also taken into account by policyholders who submit a report to the Pension Fund for 2021 on persons retiring this year. If errors are discovered in a report that has already been submitted, it is better for the policyholder to clarify the data independently by submitting an adjustment before the Fund discovers the false information.

kod_otpuska_v_szv-stazh.jpg

According to the table of codes “Calculation of insurance experience: additional information” given in the appendix to the Filling Out Procedure, DLOTPUSK means being on annual paid leave (main or additional). That is, the encoding is used for rest time provided on the basis of Articles 114-116 of the Labor Code of the Russian Federation. In SZV-STAZH for 2021, this code designated such vacations for all employees.

For example, if you submit reports with incorrect codes, charges and payments in the inspection database will appear on different personal cards. Moreover, on the front card with the BCC for old deductions, the company will have an arrears, for which the inspectorate will automatically begin to charge penalties. And at the desired KBK there will be an overpayment. To correct the situation, you will have to submit a clarification with the correct BCC.

In the “Submitted to the tax authority (code)” field, indicate the code of the tax office to which you are submitting the calculation. In the “Location (accounting)” field, enter the code, which depends on where you submit your reports. Check the table below.

Example of filling out section 1

The Ministry of Finance believes that companies must submit payments for contributions, even if they do not operate or do not pay remuneration to employees. Payers of insurance premiums are required to submit calculations to the DAM. If an organization has at least one employee, for example, the general director is the only founder, it is required to submit reporting on contributions. It’s just that the accruals in favor of individuals in this case are zero.

The Federal Tax Service has approved a new form for calculating insurance premiums, which must be submitted starting with reporting for the 1st quarter of 2021. An example of filling out a calculation for the 2nd quarter of 2021 for organizations using the general taxation system is presented in this article.

If the amount of contributions turned out to be positive, i.e. for payment, then in line 090 the line attribute code “1” is indicated. However, if the amount of expenses incurred was greater than the accrued contributions, then the attribute code “2” is indicated in line 90. The amount in line 090 is always reflected only in a positive value, the minus sign is not placed.

This is interesting: Is there a danger of receiving dividends from the chief accountant’s cash desk?

Section 1 Summary data on the obligations of the payer of insurance premiums

In the third month of the quarter, the employee was on sick leave for 4 days, and he was paid sick leave in the amount of 7,200 rubles. The employer paid for the first 3 days of illness, which amounted to 5,400 rubles, and the remaining 1,800 rubles. – paid at the expense of the Social Insurance Fund.

Changes in the procedure for filling out the DAM for 9 months of 2021 are related to the abolition of benefits on insurance premiums for some categories of policyholders. Now companies in special regimes with preferential types of activities apply not reduced, but regular tariffs. The Federal Tax Service letter No. BS-4-11/ [email protected] lists the following changes:

Where are the types of codes indicated?

Grouped by sections, the codes of the parameters required to fill out information about the length of service are contained in clause 2.3.26 to the Pension Fund Resolution No. 507 p dated December 6, 2018:

- insured persons by category;

- taking into account working conditions in the territories of the Far North and those exposed to radiation contamination;

- for special working conditions;

- on the basis for calculating the insurance period;

- according to additional information for calculating the insurance period;

- for periods that are not included in the insurance period when calculating the length of service;

- on the grounds for assigning a labor pension early;

- for a special assessment of working conditions.

The parameter classifier is intended to identify employees and the conditions of their work when considering personalized data in the Pension Fund. It allows you to ensure the assignment of a pension taking into account all factors (earnings, length of service, working conditions, etc.).

The classifier also includes codes for such categories of insured persons as foreign citizens temporarily residing in the territory of the Russian Federation.

“Neopl” and “Agreement” in personalized accounting

The “Neople” code is used if there were periods during which no work was carried out. Such periods are:

- leave without pay;

- downtime due to the employee’s fault;

- suspension from work in case of violations of labor regulations (for example, state of intoxication);

- unpaid leave of up to one year provided to teachers;

- other unpaid periods.

The “Contract” code is entered if work under the contract began in the previous reporting period and continues in the current one. It is used for contracts, transportation and others.