How to set the value of a gift

If the donation has been officially formalized and you have a gift agreement, then everything is simple - the agreement indicates the value of the gift. This amount is used to calculate tax.

Example:

In 2021, the father-in-law gave his son-in-law a room. A gift agreement was drawn up indicating the value of the gift - 900 thousand rubles. Until April 30, 2021, the son-in-law submits a 3-NDFL declaration and pays tax until July 15, 2020: 13% x 900,000 = 117 thousand rubles.

The donation agreement should not artificially reduce the cost of housing.

The tax inspector will take notice of this and force you to pay tax on the market value of the property. Such situations were considered by the Ministry of Finance and described in letters dated October 15, 2015 No. 03-04-05/59154, May 8, 2014 No. 03-04-05/21903, dated April 30, 2014 No. 03-04-05/20685

To determine the market value, tax authorities most often use the cadastral value of housing. If you have reasons to reduce the value of real estate, give compelling arguments in favor of such a discrepancy with the cadastre.

Giving gifts to employees

BOO

The cost of gifts is other expenses (clause 11 of PBU 10/99). Recognized at the time of delivery of gifts to individuals (clause 16 of PBU 10/99).

WELL

The cost of the gift and VAT accrued upon transfer are not recognized as expenses for income tax purposes (clause 1 of Article 252 of the Tax Code of the Russian Federation, clauses 16, 19 of Article 270 of the Tax Code of the Russian Federation).

VAT

The tax is accrued at the time of transfer of the gift, the tax base is the market value (the cost of purchasing the gift) (clause 1, clause 1, article 146 of the Tax Code of the Russian Federation, clause 2, article 154 of the Tax Code of the Russian Federation).

Sales - Sales - Gratuitous transfer.

You can issue one SF for the entire gratuitous transfer.

You should draw up an accounting statement or a summary document containing summary (consolidated) data on gift giving transactions (Letter of the Ministry of Finance of the Russian Federation dated 02/08/2016 N 03-07-09/6171).

Document Invoice issued for sale :

- Transaction type code : “Free transfer of goods, works, services”;

- The lines are marked with dashes: 6 “Buyer”;

- 6a “Address”;

- 6b “Buyer’s INN/KPP”.

The donor does not pay tax

Let's decide once and for all - the donor does not have to pay gift tax. You can safely dispose of your property - donate money, real estate, cars, part of a business - with this procedure you do not have any responsibility to the tax authority, and you are not obliged to notify anyone about your good deed. And this is logical. By making a gift, you do not receive income, and if so, then we cannot talk about income tax.

What about those who received a gift? Let's figure it out.

Online service NDFLka.ru is your assistant in solving tax issues! If you have a question or need to fill out a 3-NDFL declaration, register in your personal account!

Should personal income tax be withheld from a gift to an employee in 2020?

The gift can be given both in cash and in kind:

- Cash incentives mean the issuance of cash or a non-cash payment to an employee’s plastic card.

- Natural form is the actual thing.

Are gifts to company employees subject to personal income tax? Next, let's look at the most interesting points.

The tax base

Article 217 of the Tax Code of the Russian Federation provides a list of income that is not subject to income tax.

Thus, the taxable base is the difference between the price of the gift and 4 thousand rubles.

Rates

Personal income tax on a gift to an employee is charged at standard rates:

- 13% - for recipients who are residents of the Russian Federation;

- 30% - for non-resident donees.

Paperwork

To avoid possible problems with the tax authorities, you should correctly formalize the business transaction in terms of documentation.

If a gift is given as a reward for work, a gift agreement is usually not drawn up, since it is transferred on the basis of an employment agreement.

The order of the head of the company reflects the name of the recipient, his position, the name of the gift and its value.

Example of an order:

Accounting

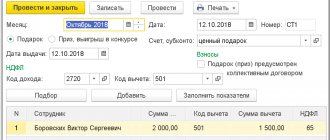

In accounting when issuing gifts, the following entry should be made: D-t 91 subaccount “Other expenses” K-t 41 (10, 43).

Most gifts are given free of charge, so they must be reflected at actual cost.

The withholding of personal income tax on gifts worth more than 4 thousand rubles is reflected by the posting: D-t 70 K-t 68 subaccount “Personal income tax settlements”.

Deadlines

The moment of tax deduction and transfer to the budget depends on the form of the gift:

| Gift form | Deadlines |

| Monetary | The tax amount must be withheld and transferred to the treasury on the day the gift is issued from the cash register or on the day the money is transferred to the employee’s personal account |

| Natural | Tax is paid on the next payday |

Calculation example

Alekseev S.M. has been operating in the Energosbyt company for 20 years. This year the organization celebrates its anniversary - 30 years of activity. Gene. The director decided to give each employee a gift of 5 thousand rubles. Alekseev was also paid a bonus for excellent work and high experience - 10 thousand rubles.

Calculations:

- amount of income tax = (10 thousand + 5 thousand – 4 thousand) * 13% = 14.3 thousand rubles;

- insurance premiums = 10 thousand * 0.3 = 3 thousand rubles.

The accountant must reflect the amount of 13 thousand rubles in expenses.

If it is impossible to hold

If it is not possible within the tax period. period to withhold the amount of the fee, the agent is obliged to inform the taxpayer and the inspectorate about this, as well as the amount of profit from which the fee was not withheld, by March 1 of the next year.

The employee will be required to independently pay the tax that was not withheld.

Other taxes, fees and contributions

If gifts are given free of charge, this is considered a sale, and accordingly VAT is charged in accordance with Part 1 of Art. 146 of the Tax Code of the Russian Federation.

Regardless of the price of gifts, insurance premiums and contributions for injuries are not charged on them, since gifts do not relate to payments under either labor or civil servants contracts.

If the company is under a special tax regime

If a legal entity or individual entrepreneur applies the simplified tax system, income minus expenses incurred, the amount of gifts is not included in expenses if the gifts are not given in connection with the employee’s performance of work duties.

Otherwise, the cost of gifts can be taken into account when calculating expenses under the simplified tax system.

Regulatory regulation

VAT

The operation is subject to VAT (clause 1, clause 1, article 146 of the Tax Code of the Russian Federation, clause 2, article 154 of the Tax Code of the Russian Federation).

Input VAT when purchasing gifts can be deducted (clause 1, clause 2, article 171 of the Tax Code of the Russian Federation, clause 1, article 172 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated August 18, 2017 N 03-07-11/53088).

Income tax

The cost of gifts and VAT accrued on gratuitous transfers are not taken into account in NU expenses

(clause 1 of article 252 of the Tax Code of the Russian Federation, clauses 16, 19 of article 270 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated March 11, 2010 N 03-03-06/1/123).

Gifts can be taken into account for income tax purposes if they are given for achievements in work and are part of the

remuneration

system (paragraph 1, paragraph 2 of Article 255 of the Tax Code of the Russian Federation, Articles 135, 191 of the Labor Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated 22.04. 2010 N 03-03-06/2/79).

Gifts for achievements in work, as an incentive, must be specified in the employment contract (Clause 21, Article 270 of the Tax Code of the Russian Federation).

Personal income tax

From income in the form of a gift to an individual, the donor-tax agent is obliged to withhold personal income tax (clause 1 of Article 210 of the Tax Code of the Russian Federation, clause 1 of Article 226 of the Tax Code of the Russian Federation).

The value of gifts received from organizations and individual entrepreneurs is exempt from taxation up to 4,000 rubles. per year (clause 28 of article 217 of the Tax Code of the Russian Federation).

Organizations are required to keep personalized records of income in the form of gifts received from them by individuals (Letter of the Ministry of Finance of the Russian Federation dated 05/08/2013 N 03-04-06/16327).

Insurance premiums

The cost of a gift is not subject to insurance contributions if it does not relate to incentive payments provided for by the remuneration system (clause 1 of Article 420 of the Tax Code of the Russian Federation).

If a gift is transferred under a gift agreement, then the object of taxation with insurance premiums does not arise (clause 4 of Article 420 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated January 20, 2017 N 03-15-06/2437).

Accountant's Directory

Acting State Advisor of the Russian Federation, 2nd class S.L. BONDARCHUK Expert's commentary The Federal Tax Service of Russia explained how to fill out form 6-NDFL when transferring a gift to an individual, if there were no other payments in his favor, and it is impossible to withhold personal income tax (see also the letter of the Federal Tax Service of Russia dated 08/01/2016 N Example: Reflection of the gift of property in form 6-NDFL.

On June 20, 2016, the organization donated a television worth 10,000 rubles to a former employee, a tax resident of the Russian Federation. In form 6-NDFL for six months... Expert “NA” I.S. Sergeeva Russian organizations, individual entrepreneurs and permanent representative offices of foreign organizations in the Russian Federation, from which or as a result of relations with which the taxpayer received income, are tax agents.

Tax agents are obliged to calculate, withhold from the taxpayer and pay the amount of tax within the established time frame. Calculation of amounts and payment of tax are carried out in relation to all income of the taxpayer, the source of which is the tax agent, with the offset of previously withheld tax amounts.

The exception is income received from tax agents by individual entrepreneurs and other persons engaged in private practice, as well as income on which tax is calculated and paid. Tax agents calculate tax amounts by calculating the cumulative total from the beginning of the annual period based on the results of each month in relation to all income for which a tax rate of 13% is applied to the taxpayer for a given period with the offset of the tax amount withheld in previous months of the current tax period. The tax amount is calculated as a percentage of the tax base corresponding to the tax rate.

In this case, the tax base is defined as the monetary expression of income subject to taxation, reduced by the amount of tax deductions.

The amount of tax in relation to income for which other tax rates are applied is calculated by the tax agent separately for each amount of the specified income accrued to the taxpayer.

The tax amount is calculated as a percentage of the tax base corresponding to the tax rate. In this case, the tax base is determined as the monetary value of such income subject to taxation, and tax deductions are not applied.

The tax amount is calculated without taking into account the income received by the taxpayer from other tax agents and the tax amounts withheld by other tax agents.

The total tax amount is the amount obtained by adding the tax amounts calculated in the manner described above. The tax amount is determined in full rubles.

A tax amount of less than 50 kopecks is discarded, and 50 kopecks or more are rounded up to the full ruble.

Tax agents are required to withhold the accrued tax amount directly from the taxpayer’s income upon actual payment. The tax agent is authorized to withhold from the taxpayer the accrued amount of tax, not exceeding 50% of the payment amount, at the expense of any funds paid by the tax agent to the taxpayer, upon actual payment of these funds to the taxpayer (or on his behalf to third parties).

The company gave a gift that is exempt from personal income tax

The company gave employees gifts worth up to 4,000 rubles. Such gifts are not subject to personal income tax.

In line 020 of section 1 of the calculation, reflect payments that are only partially exempt from personal income tax. In particular, gifts. Such income is exempt from personal income tax in an amount that does not exceed 4,000 rubles for the tax period (clause 28 of article 217 of the Tax Code of the Russian Federation).

There is an exception to the general rule. If an employee receives only income not subject to personal income tax during the year, it does not need to be shown in line 020. For example, a gift of up to 4 thousand rubles. In relation to such payments, the company is not a tax agent and does not submit income certificates (letter of the Ministry of Finance of Russia dated 05/08/13 No. 03-04-06/16327). If you fill out the payment in the 6-NDFL calculation, the information for the year will not agree with the 2-NDFL certificates (letter of the Federal Tax Service of Russia dated March 10, 2016 No. BS-4-11 / [email protected] ).

For the first half of the year, the company paid salaries to five employees - 700,000 rubles, provided deductions - 10,000 rubles, withheld personal income tax - 89,700 rubles. ((RUB 700,000 - RUB 10,000) × 13%). In the second quarter, the company gave employees gifts worth RUB 3,000. for every. A total of 90,000 rubles. A gift to each employee is not subject to personal income tax, so the company did not reflect the gifts in the half-year calculation. The company filled out Section 1 of the calculation as in sample 54.

If the company gives the employee a gift again, the income may exceed the non-taxable limit. In the period when this happens, reflect in the calculation the cost of all gifts that have been given since the beginning of the year. Write the deduction of 4,000 rubles in line 030 of the calculation.

Sample 54. How to fill out the calculation if the company gave gifts cheaper than 4,000 rubles:

Are gifts worth less than 4,000 rubles reflected in 6-personal income tax? - all about taxes

The donor must independently notify the recipient of the approximate cost of the gift.

Do I have to pay gift tax?

Since personal income tax is collected, the provisions of legislative acts and laws regarding this tax are taken into account. Therefore, information from sources of the Tax Code of the Russian Federation is studied, and a lot of information is contained in Article 226, and the data of Federal Law No. 117, Chapter 23 are also taken into account.

The need to pay personal income tax on a gift received from an employer arises if its value exceeds 4 thousand rubles. Therefore, donors should be aware when preparing a gift that exceeding this limited amount will result in a tax liability.

Important! All gifts received during one period from the employer are taken into account.

If the donor is an individual, then the value of the gift is not important, so tax is paid if the gift is land shares, real estate, shares or cars.

The tax rate depends on residence, therefore:

- for residents of the Russian Federation it is 13%;

- for non-residents – 30%.

Often, employers give their employees significant gifts for birthdays or other significant dates, presented in the form of a one-time remuneration.

Typically, their size depends on the employee’s age, length of service, position and other factors. This is due to the fact that they are not obtained in the process of human activity at work and are not related to the results of performing duties. If the amount of such remuneration does not exceed 4 thousand.

rub. for the tax period, then you are not required to pay personal income tax. For amounts exceeding this limit, 13% is charged.

The specifics of collection depend on who the donor was:

- if the donor is a friend or acquaintance, the recipient must independently calculate the tax and submit a declaration indicating the estimated value of the gift.

- if the gift was given at work, then the employer must independently calculate and pay personal income tax for the employee, and the required amount is withheld from the citizen’s salary;

Important! Tax evasion makes citizens liable and will have to pay fines. It is not allowed to levy a tax if its amount is 50% or more more than a person’s salary

The employer must notify the employee that he has failed to withhold tax.

It is not allowed to levy a tax if its amount is 50% or more more than a person’s salary. The employer must notify the employee that he has failed to withhold tax.

In this case, the taxpayer has an obligation to pay it independently. Do I need to pay gift tax?

Watch the video: Gifts can be given not only at work, but also by various acquaintances or friends.

Important! Tax must be paid on expensive gifts if the donor is not a close relative of the recipient. The need to pay this tax arises if the gift is presented:

The need to pay this tax arises if the gift is presented:

- land share;

- shares;

- real estate;

Certificate as a gift

Currently, so-called gift certificates are becoming increasingly fashionable gifts. Employers give them to employees as a present for a holiday or birthday; trading organizations - to clients who purchased goods for a certain amount; advertising companies - participants of advertising campaigns; construction companies - to purchasers of housing in new buildings, etc. Is the cost of such gifts subject to personal income tax?

The term “ gift certificate ” is usually understood as a document certifying the right of its owner to receive goods (work, services) from the person specified in the certificate (seller), including payment for the goods (work, services) its cost minus that specified in the certificate amount - the nominal value of the certificate (Letter of the Ministry of Finance of Russia dated 04.04.2011 N 03-03-06/1/207). In Letter dated 09/07/2012 N 03-04-06/6-274, the Russian Ministry of Finance qualified the income arising from the recipient of a gift certificate as income in kind in the form of payment for the right to receive services in an organization that sells such certificates. But when does a taxable benefit arise: on the date of receipt of the certificate or at the time of payment for the cost of goods, works, services with this certificate? After all, the owner of the certificate may not use it at all (lose it, forget it, etc.). The Ministry of Finance of Russia in Letter dated September 14, 2012 N 03-04-06/6-279 clearly states: income arises precisely upon receipt of the certificate. And it doesn’t matter whether the citizen presents it for payment or not.

Gift or prize

The classification of income received in the form of the value of gift certificates as gifts or other types of income depends on the documentation of the payment (issuance) of income (Letter of the Ministry of Finance of Russia dated September 7, 2012 N 03-04-06/6-274).

Let us recall that clause 28 of Art. 217 of the Tax Code of the Russian Federation provides for an exemption from personal income tax on income received from organizations and entrepreneurs in the form of gifts if their value does not exceed 4,000 rubles. for the tax period. Therefore, if the certificate is issued as a gift, then its value, if it does not exceed 4,000 rubles, is exempt from taxation. The amount of income in excess of the established limit is subject to personal income tax at a rate of 13% (Letters of the Ministry of Finance of Russia dated 04.04.2011 N 03-03-06/1/207, dated 02.07.2012 N 03-04-05/9/809) .

When the issuance of a gift certificate is framed as a win or prize, personal income tax will have to be paid at a much higher rate, but only if the winning amount exceeds 4,000 rubles. from the beginning of the tax period. The fact is that Art. 224 of the Tax Code of the Russian Federation establishes the following: the cost of any winnings and prizes received in competitions, games and other events for the purpose of advertising goods, works and services, in terms of exceeding the amounts specified in clause 28 of Art. 217 of the Tax Code of the Russian Federation, is subject to personal income tax at a rate of 35% (Letter of the Ministry of Finance of Russia dated March 13, 2012 N 03-04-05/3-292).

In turn, the organization (or entrepreneur) from which citizens receive certificates as a gift is recognized as a tax agent (Letter of the Ministry of Finance of Russia dated September 14, 2012 N 03-04-06/6-279). If this organization does not pay these individuals any income in cash from which personal income tax could be withheld, then the provisions of clause 5 of Art. 226 Tax Code of the Russian Federation. If it is impossible to withhold the calculated amount of personal income tax from the taxpayer, the tax agent is obliged, no later than one month from the date of the end of the tax period in which the relevant circumstances arose, to notify the taxpayer and the tax authority at the place of his registration in writing about the impossibility of withholding personal income tax and its amount.

The responsibility for calculating, withholding and paying personal income tax on the taxpayer’s income received in the form of any winnings and prizes in competitions, games and other events for the purpose of advertising goods (works, services) is assigned to the Russian organization from which he received such income, recognized on the basis of Art. 226 of the Tax Code of the Russian Federation as a tax agent. A citizen has an obligation to declare income in the form of winnings and prizes received during promotional events only if personal income tax was not withheld by the tax agent.

helpmsk24.ru

Suppose that the gifts from the previous example were issued on June 25, then income in kind in the 6th personal income tax report for the six months will be reflected as follows: In situations where tax was not withheld at the end of the year, the employer reports this:

- tax inspector;

- employee.

The organization must do this before March 1 of the next year by submitting a 2-NDFL certificate. The certificate is completed as follows:

- field “sign” - enter 2;

- section 5 - indicate the amount of the fee.

The employee, as a reward for his work, can receive income in kind.

Gifts can be given not only at work, but also by various acquaintances or friends

Important! Tax must be paid on expensive gifts if the donor is not a close relative of the recipient. The need to pay this tax arises if the gift is presented:

- shares;

- real estate;

- land share;

- automotive technology.

Important!

Personal income tax is not paid on any gift if it is given by a close relative.

How to register a deed of gift for an apartment with a notary?

Details here. If the donor is not a relative, but at the same time gives cars, shares, land or real estate, then tax will certainly be paid on the assessed value of this gift. You can get information about the cost of a gift in different ways:

- this value is indicated in the gift agreement;

- the value of the property is assessed.

What gifts are taxable? The first option is considered the simplest, but is rare.

The exception is income received from tax agents by individual entrepreneurs and other persons engaged in private practice, as well as income on which tax is calculated and paid.

Tax agents calculate tax amounts by calculating the cumulative total from the beginning of the annual period based on the results of each month in relation to all income for which a tax rate of 13% is applied to the taxpayer for a given period with the offset of the tax amount withheld in previous months of the current tax period. The tax amount is calculated as a percentage of the tax base corresponding to the tax rate. In this case, the tax base is defined as the monetary expression of income subject to taxation, reduced by the amount of tax deductions.

The amount of tax in relation to income for which other tax rates are applied is calculated by the tax agent separately for each amount of the specified income accrued to the taxpayer.

The tax amount is calculated as a percentage of the tax base corresponding to the tax rate. Federal Tax Service of Russia dated August 1, 2016 N Example. Reflection of the donation of property in form 6-NDFL.

On June 20, 2016, the organization donated a television worth 10,000 rubles to a former employee, a tax resident of the Russian Federation. In form 6-NDFL for six months... Expert “NA” I.S. Sergeeva Russian organizations, individual entrepreneurs and permanent representative offices of foreign organizations in the Russian Federation, from which or as a result of relations with which the taxpayer received income, are tax agents.

How are gifts reflected in accounting?

To display a gift in accounting, you do not need to use an account. 70, since it is not related to the performance of official functions. It is advisable to use the account. 73.

The following correspondence must be reflected in accounting:

- Buying a present

Dt 10 Kt 60 - reflection of the purchase price;

Dt 19 Kt 60 - accounting for input VAT;

Dt 68 Kt 19 - application for deduction of input VAT.

The purchase of a gift can also be reflected in another way - the cost is charged directly to the account. 91 excluding account. 10. Accounting for gifts for employees’ children should be reflected on the balance sheet, for example, on the account. 012. This point is due to the fact that acquired values are not considered an asset, because the employer does not plan to receive economic benefit from their use.

- Presentation

If the gift is a valuable property:

Dt 73 Kt 41 (10, 43) - issuance of a gift;

Dt 91 Kt 73 - attribution of cost to costs;

Dt 91 Kt 68 - accrual of VAT on the gratuitous transfer of a gift;

Dt 70 Kt 68 - withholding personal income tax from a gift worth more than 4,000 rubles;

Dt 99 Kt 68 - reflection of a permanent tax liability in the amount of 20% of the value of the gift;

If the gift is in the form of money:

Dt 73 Kt 50 - issuance of funds from the cash register;

Dt 91 Kt 73 - recognition of the cost of the gift as expenses;

Dt 70 Kt 68 - withholding personal income tax from a gift worth more than 4,000 rubles;

Dt 99 Kt 68 - reflection of a permanent tax liability in the amount of 20% of the value of the gift.

How to reflect gifts of less than 4,000 rubles in 6 personal income taxes

The company provided financial assistance of less than 4,000 rubles 6.

The company provided financial assistance of more than 4,000 rubles 7. In addition, there are non-labor bonuses that are timed to coincide with certain events in the life of an employee or the entire enterprise.

In the same way, premiums are also required to pay insurance contributions sent by the company to extra-budgetary funds.

What obligations does an organization have with respect to paying income tax, VAT, and personal income tax? A blog is your new tool to talk about yourself. Publish any content about your company.

In this case, you reflect the payment in section 2 of form 6-NDFL for 9 months, since the last date refers to the third quarter of 2017. It is necessary that he understands in which cases it makes sense to designate an amount as a bonus, and when it should be determined in a different way. In section 2, record the amounts paid to the dismissed employee in a separate block.

They cannot be reflected in the block with wages for other employees. The same rule applies when paying a bonus of this type when an employee leaves the organization.

The exception is for awards, Russian, other states and international, which are given in the decree of the Russian government adopted on February 6, 2001. It mentions prizes that are awarded for significant achievements in various fields, including:

- in education.

- in literature, art, culture, media and tourism;

- in science and technology;

Obviously, gifts are also income received by the taxpayer in kind.

Accordingly, if a company makes certain gifts to individuals, then it is charged with the responsibility for calculating, withholding and paying personal income tax to the budget. The limited liability company form of ownership is the most common among commercial structures.

An organization in the form of an LLC has the right to carry out all types of activities, choose or change forms of taxation depending on business conditions. On this day, the company calculated personal income tax - 390 rubles. ((RUB 7,000 - RUB 4,000) × 13%).

In section 1 of the calculation for the first quarter, the company reflected the gift in line 020, in line 030 it recorded a deduction of 4,000 rubles, and in line 040 it entered the calculated personal income tax.

On May 10, the company gave the employee a salary, from which it was able to withhold personal income tax from the gift.

Therefore, she does not need to show this income in her personal income tax reporting. Officials stated that such income is not subject to personal income tax.

Therefore, there is no need to calculate, withhold and pay tax on this income to the budget. We are talking about gifts whose value during the tax period does not exceed 4,000 rubles.

And it doesn’t matter to whom they are presented - an employee, a former employee or another \"physicist\". On the one hand, there is a certain logic here - such gifts are not subject to tax

This amount does not exceed 50 percent of the salary of each employee to be paid - 11,000 rubles.

Section 1 of 6-NDFL calculation

From a gift less than 4,000 rubles. Personal income tax is not collected (clause 28, article 217 of the Tax Code of the Russian Federation). More expensive gifts are taxed and reflected in the 6-NDFL calculation.

In Section 1, the amounts of income, deductions provided, calculated and withheld tax are entered in an incremental manner from the beginning of the year:

- Income is entered in line 020, taking into account the cost of gifts;

- in line 030 - the deductions provided: for example, standard for a child, deduction for a gift in the amount of 4,000 rubles. and etc.

When receiving a gift in kind, personal income tax is withheld from the next payments to the employee: wages, bonuses, etc. In this case, the withheld tax should not exceed 50% of the amount paid (clause 4 of article 226 of the Tax Code of the Russian Federation).

Personal income tax is transferred to the budget on the day the personal income tax is withheld, or the next day. The amount of tax withheld is entered in line 070.

If the tax was not withheld due to insufficient income of the employee, fill out line 080.

Advance amount in 6-NDFL: types and dates

The concept of “advance” is used everywhere in business. In general, an advance is an amount prepaid (before final income is determined). This can equally apply to:

- “salary” advance paid by force of law to an employee drawn up under an employment contract;

- advance payment under a GPC agreement, the payment of which is determined by the terms of the agreement at the will of its parties;

- fixed advance payments - paid due to the requirements of tax legislation by foreigners working on a patent.

Despite the unambiguous interpretation of the term “advance”, the reflection of the tax date on advance payments in 6-NDFL in these cases has its own characteristics.

Date of UN when paying a “salary” advance

When setting the UL date for a “salary” advance, you must proceed from the following:

- advance payment is part of earnings;

- for the purpose of calculating personal income tax, a salary is considered income, the date of receipt of which falls on the last day of the month for which the salary is accrued (clause 2 of Article 223 of the Tax Code of the Russian Federation).

In this regard:

- the advance is not yet considered income;

- The Tax Code of the Russian Federation does not require withholding personal income tax from advance amounts.

Consequently, the fact of payment of an advance is not reflected separately in 6-NDFL and is included in this report only as part of the accrued salary, that is, on the last day of the month. The UN date for income in the form of salary (including “salary” advance) is the day of payment of earnings at the end of the month worked.

Date of UN for GPC advance

An advance paid by the customer to a contractor - an individual, is regarded by tax legislation differently than “salary”. The fact is that a GPC agreement may provide for various payment schemes:

- step by step (based on completed work completion certificates);

- after the full scope of work provided for in the contract has been completed (with or without advances).

Phased acceptance and payment means the contractor receives payment for part of the work performed accepted by the customer, i.e., income actually received. The same approach applies to advances - officials of the Ministry of Finance insist on this (letter dated May 26, 2014 No. 03-04-06/24982), based on the Tax Code of the Russian Federation (subclause 1, clause 1, article 223).

The analogy with a “salary” advance is inappropriate here, since the nature of the income received differs.

Thus, the UN date in 6-NDFL occurs every time an advance is issued to the contractor - this is the day the money is transferred to his card or cash is received at the cash desk.

For more information on reflecting advances under a GPC agreement in 6-NDFL, see.

UN date and fixed advances

The UN date in 6-NDFL has features in one more case - if the company paid income to a foreigner working on the basis of a patent (subject to certain conditions).

In this case, the fixed advance payments paid by the employee are reflected in line 050 of the 6-NDFL report and reduce the personal income tax calculated from the earnings of “patent” foreigners.

The “Date UN” parameter in 6-NDFL will appear if the “foreign” advances turned out to be less than the personal income tax calculated from the foreigner’s salary. Until the advance payment is exhausted, “0” is placed in the line with the date of the UN.

“Nuances of filling out 6-NDFL for

“patent” foreigners” will help in filling out the lines of the personal income tax report on “foreign” advances .

Tax officials answered questions about filling out 6-NDFL

1. As part of the promotion, the organization pays lottery participants cash prizes in the amount of no more than 4,000 rubles. Is it necessary to indicate such amounts in the calculation of 6-NDFL?

No no need. Income not exceeding 4 thousand rubles received in the form of winnings and prizes is not subject to personal income tax (clause 28 of article 217 of the Tax Code of the Russian Federation). In this regard, the tax agent has the right not to indicate the payment of a cash prize in the 6-NDFL calculation if its amount does not exceed 4 thousand rubles.

2. Is income in the form of financial assistance paid to an employee at the birth of a child in the amount of 50,000 rubles reflected in 6-NDFL?

A similar approach applies to the payment of financial assistance at the birth of a child. A one-time payment at the birth of a child is not subject to personal income tax up to 50 thousand rubles for each child (clause 8 of article 217 of the Tax Code of the Russian Federation). Accordingly, the employer has the right not to reflect the payment of financial assistance in the calculation of 6-NDFL if it does not exceed 50 thousand rubles.

Let us recall that the same explanations are contained in the letter of the Federal Tax Service dated December 15, 2016 No. BS-4-11 / [email protected] (see “The Federal Tax Service reported in which case financial assistance paid at the birth of a child is not reflected in the calculation of 6-NDFL” ).

3. When is an income payment transaction considered completed in order to be reflected in the calculation using Form 6-NDFL?

In section 2 of the calculation for the corresponding reporting period, you need to reflect only those transactions that were made during the last three months of this period. If an operation is started in one reporting period and completed in another reporting period, then it is reflected in the completion period. In this case, the operation is considered completed in the submission period, in which the deadline for tax transfer occurs in accordance with paragraph 6 of Article 226 and paragraph 9 of Article 226.1 of the Tax Code of the Russian Federation.

For example, when paying salaries for June on the last day of the month (06/30/2017), the deadline for transferring personal income tax falls on the next period (July 3, since July 1 and 2 are weekends). This means that this operation should be reflected in section 2 of the calculation for the nine months of 2017.

Also see “The Federal Tax Service explained how to fill out 6-NDFL if the tax payment deadline occurs in another period.”

4. The acceptance certificate for works (services) under a civil contract was signed in March 2021, and the remuneration to the individual was paid in April 2021. In what period should this income be reported?

The date of actual receipt of income in the form of remuneration for the performance of work (services) under a civil contract is the day of payment of income, including the transfer of income to the taxpayer’s bank accounts or, on his behalf, to the accounts of third parties (subclause 1, clause 1, art. 223 of the Tax Code of the Russian Federation). Thus, this payment is indicated in the calculation of 6-NDFL in the period when the contractor received it.

Since the act was signed in March 2021, and the remuneration for the provision of services under this agreement was paid in April 2021, this operation is reflected in sections 1 and 2 of the 6-NDFL calculation for the first half of 2021.

Also see “The Federal Tax Service reported how to reflect income paid to the contractor under a civil contract in the calculation of 6-NDFL.”

5. The employee went on vacation from June 1, 2021, and vacation pay was paid to him on May 25. How to reflect the amount of vacation pay in 6-NDFL?

The date of actual receipt of income in the form of vacation pay is considered the day the income is paid (subclause 1, clause 1, article 223 of the Tax Code of the Russian Federation). Tax agents are required to withhold the accrued amount of tax directly from the taxpayer’s income upon actual payment (Clause 4 of Article 226 of the Tax Code of the Russian Federation). When paying an employee income in the form of vacation pay, personal income tax is transferred no later than the last day of the month in which such payments were made.

Taking into account the above, in the described situation, the payment of vacation pay is reflected in sections 1 and 2 of the 6-NDFL calculation for the first half of 2021. When filling out section 2 of the half-year calculation, the payment of vacation pay must be reflected as follows:

- on line 100 “Date of actual receipt of income” - 05/25/2017;

- on line 110 “Date of tax withholding” - 05.25.2017;

- on line 120 “Tax payment deadline” - 05/31/2017;

- on lines 130 “Amount of income actually received” and 140 “Amount of tax withheld” - the corresponding total indicators.

Also see “The Federal Tax Service has clarified how to fill out 6-NDFL if the payment of vacation pay and the start of vacation fall on different reporting periods.”

6. What date in the calculation of 6-NDFL on line 100 of section 2 should be indicated in relation to the average earnings accrued to the employee while on a business trip?

While on a business trip, the employee performs job duties. Average earnings for days on a business trip are part of the salary. Accordingly, the amount of average earnings, like wages, is recognized as income on the last day of the month for which this income was accrued (clause 2 of Article 223 of the Tax Code of the Russian Federation). It is this date that is reflected in line 100 “Date of actual receipt of income” of section 2 of the 6-NDFL calculation.

7. After submitting the 6-NDFL calculation for the first half of 2021 to the inspectorate, the organization discovered that an error was made in the calculation for the first quarter. This miscalculation led to an underestimation of the amount of income, and, accordingly, to an underestimation of the calculated and withheld amount of personal income tax. Is it necessary to submit an updated calculation of 6-NDFL for each submission period (for the first quarter and half of the year)?

Yes need. Since section 1 of the calculation of form 6-NDFL is compiled on an accrual basis, in the described situation, “clarifications” should be presented for the first quarter and for the first half of 2021. When submitting an updated calculation, the corresponding adjustment number is indicated on the title page: “001”, “002”, etc.

Also see:

- “Federal Tax Service: in case of recalculation of personal income tax for the first quarter, it is necessary to submit “clarifications” for 6-personal income tax for this and subsequent reporting periods”;

- “The Federal Tax Service has explained what to do if errors are detected in 6-NDFL.”

8. The tax agent made an arithmetic error when calculating personal income tax on wages for December 2021, paid in January. In February 2021, he recalculated. How to reflect the recalculation of wages in the calculation of 6-NDFL?

In this case, the total amounts, taking into account the recalculation made, are reflected in section 1 of the calculation for 2021 and in section 2 of the calculation for the first quarter of 2021.

In addition, the amount of personal income tax from the December salary, taking into account the recalculation made, must be indicated in the 2-NDFL certificate for 2016.

Also see “The Federal Tax Service reported how to fill out 6-NDFL in case of recalculation of wages for December.”

How to withhold tax under a GPC agreement in 2021 and fill in the withholding date in 6-NDFL?

Payment of income to an individual under a civil law agreement (GPC) is also a reason for calculating and withholding personal income tax, as in the situation with “salary” income.

It should be noted that for the purposes of personal income tax in general and the calculation of 6-personal income tax in particular, the accrual dates for the specified types of income (p. 100) differ:

- for salary (income received by an employee for performing a job function within the framework of an employment contract), this is the last day of the month for which it is accrued;

- for income under a GPC agreement (payment for work performed) - the day it is received.

Despite the indicated differences in the date of tax calculation, the date of withholding in the situation of payment of income under a civil process agreement is determined similarly to the date of taxation under an employment contract, as the day of payment of remuneration. This means that when filling out the calculation regarding income from GPC, the dates in lines 100 and 110 will coincide.

Meanwhile, the GPC agreement has one feature that affects the reflection of the tax date in 6-NDFL.

If the contractor receives advances from the customer during the period of performance of work (provision of services), they are equated to income and are subject to personal income tax, regardless of their amount, payment period and other conditions.

We will discuss how GPC advances affect the UN date filled out in 6-NDFL in the next section.

Section 2 of form 6-NDFL

In Section 2, the calculations show information for the last quarter:

- Line 100 shows the actual date of receipt of income in the form of a gift. If an item is donated, the number when it was given is entered here. If money is donated, the day it is paid to the employee (clause 1 of Article 223 of the Tax Code of the Russian Federation).

- Lines 110 and 120 show the dates of tax withholding and transfer to the budget.

- In line 130, actual income is entered without taking into account the required deductions and before personal income tax is collected. The tax withheld from this amount is reflected in line 140.

An example of filling out 6-NDFL with a gift over 4,000 rubles.

Let's consider line-by-line filling out the 6-NDFL calculation for income in the form of gifts more than 4,000 rubles.

Example

Salaries accrued to 10 company employees:

- for December 2021 (paid in January) - 405,000 rubles;

- for January 2021 (paid in February) - 350,000 rubles,

- for February 2021 (paid in March) - 420,000 rubles,

- for March 2021 (payment in April) - 410,000 rubles.

These employees have a total of 12 children, for whom deductions are provided monthly: 12 * 1,400 = 16,800.

For an anniversary, one of the employees was presented with a gift worth 10,000 rubles, and personal income tax was calculated: (10,000 - 4,000) * 13% = 780 rubles. The gift was presented on February 25, and personal income tax was withheld on March 5 - when paying salaries for February. The tax was transferred to the budget the next day after the withholding, March 6.

Let’s fill out the 6-personal income tax calculation for the 1st quarter of 2021 using these data.

The personal income tax withheld from income in the form of salary for each month was:

- in January0) * 13% = 50,466 rubles.

- in February: (350,000 - 16,800) * 13% = 43,316 rubles.

- in March0) * 13% = 52,416 rubles.

- in April0) * 13% = 51,116 rubles.

Line 020 will include all income accrued for the period from January to March 2021, including the amount of the gift: 350,000 + 420,000 + 10,000 + 410,000 = 1,190,000 rubles. However, the salary for December is not included here, since it was accrued in 2021.

In line 030, reflect deductions - for children and from gifts: (16,800 * 3) + 4,000 = 54,400 rubles.

In line 040, show the total amount of calculated personal income tax: (1,190,000 - 54,400) * 13% = 147,628 rubles.

Indicate the tax withheld in the 1st quarter, including from a gift, in line 070: this will also include personal income tax for December 2021, withheld in January 2021. But the tax for March was withheld in April, so it is calculated for the 1st quarter no need to include: 50,466 + 43,316 + 780 + 52,416 = 146,978 rub.

Lines 040 and 070 may not be equal to each other. They will be the same only if personal income tax was accrued and withheld in the same reporting period.

Section 1 of form 6-NDFL is as follows:

6-NDFL: gifts up to 4000

In section 1, the value of the gift is reflected on line 020, but if during the year the employee received gifts with a total value of no more than 4,000 rubles. – such gifts may not be reflected at all in the 6-NDFL declaration. This is stated in the Letter of the Federal Tax Service dated July 21, 2017 No. BS-4-11/

If the cost of gifts given to an employee during the year exceeds 4,000 rubles, then the amount of gifts and the deduction must be shown in the corresponding lines of form 6-NDFL (lines 020 and 030).

For the 1st quarter, Location LLC accrued income to its employees in the amount of 210,000 rubles. (70,000 rubles per month). The amount of standard deductions for the quarter was 4,200 rubles. (1400 rubles per month). The salary payment date is the 7th.

Personal income tax in each month of the quarter was: (70,000 -1,400) x 13% = 8,918 rubles.

The amount of calculated personal income tax for 3 months is equal to: (210,000 – 4,200) x 13% = 26,754 rubles.

The withholding tax (p. 070) does not include the amount for March, because March's salary was paid in April.

In addition, in February, an employee was given a gift worth 3,500 rubles, and by March 8, an employee was given 4,000 rubles. Since these amounts did not exceed the established limit, the gifts were not reflected in 6-NDFL. Sections 1 and 2 were completed as follows:

If during this year the same employees receive more gifts from the company, then in the quarter when this happens, it will be necessary to reflect the total value of all gifts and show a deduction of 8000 (4000 x 2 employees) on line 030.

Let's continue our example:

Let’s assume that in the second quarter the monthly salary of employees remained the same as in the 1st quarter – 70,000 rubles. Also on April 15, employees received another gift in connection with the company’s anniversary - 5,000 rubles. every. The total cost of gifts for the six months was 17,500 rubles. (4000 + 3500 + 5000 + 5000). Then the following should be indicated in the Half-Year Calculation:

According to page 020, the amount of income is 437,500 rubles. (210,000 for 1 quarter + 210,000 for 2 quarters + 17500).

On page 030, taking into account the deduction for gifts, the amount will be 16,400 rubles. (1400 x 6 months + 4000 + 4000).

The total calculated amount of personal income tax (line 040) is 54,743 rubles. ((437500 – 16400) x 13%).

At the same time, personal income tax should be withheld from the above-limit value of gifts - 1235 rubles. ((17500 – 8000) x13%).

In the 1st quarter in 6-personal income tax, gifts up to 4000 were not shown. Tax on gifts received in April was withheld when paying salaries for April and reflected in the semi-annual Calculation.

Filling out form 6-NDFL for the six months:

What you need to know about financial assistance

Financial assistance is not only money paid to an employee in order to support him in a difficult life situation or in connection with a special date (anniversary, wedding, death of a close relative). Also, financial assistance can be provided in the form of work, services or goods (food, personal hygiene products, clothing, etc.).

However, the key characteristic of MP is its one-time and one-time nature. That is, the material is not part of the specialist’s salary and does not apply to incentive or compensation payments. The main goal of the MP is to support the citizen in connection with the current circumstances.

We discussed the basic concepts, as well as the key principles of taxation of this payment, in a separate article “Is financial assistance subject to personal income tax?”