When is an inventory report drawn up?

Responsible persons who are directly involved in the inspection draw up all related documents.

The main one is the inventory act. All scan data, its features and results are displayed here. It is worth noting that the type of verification performed determines the type of unified form required for a particular situation. In essence, this document officially confirms what assets are available on the organization’s balance sheet. All assets of the organization are subject to inspection. After all, this is the only way to find out whether the reporting documents correspond to reality. There are situations in which verification must be carried out without fail. For example, it must be carried out before preparing the report at the end of the year. The law also requires that an inventory be taken during the reorganization or complete liquidation of a company. These actions are also carried out in cases where new employees take the position of director or financially responsible employee.

In addition, the act is drawn up in the following situations:

- The company rents or sells property;

- There are suspicions of theft and damage to property;

- After fires, disasters and other force majeure events;

- In any situation where the head of the company deems it necessary to conduct an inspection.

Filling out the document

Form

The title page of the journal inv-23 contains the details of the person responsible for maintaining the journal. After this, the table should contain the following data:

- names of the enterprise, all branches and departments that should be inventoried;

- order number inv-23 and the time of its preparation;

- the names and surnames of everyone present on the inventory commission;

- types of material resources;

- exact date of inspections (planned and actual);

- test results;

- inventory completion date and results.

Instructions

Here are the instructions according to which it is necessary to fill out the INV-23 form:

- The journal must contain the data and details of the enterprise conducting the inventory check.

- Data of all employees who are financially responsible.

- Dates and information regarding all orders.

- Names of committee members.

- The journal must contain the results of the inspection, they must be presented accurately and concisely, the information posted must relate only to material property and its availability.

INV-23 journals, according to regulations, must be signed by those employees who are directly responsible for the truthfulness and correctness of its contents.

Conditions for conducting inventory in 2021

In order for responsible employees to begin carrying out the inventory, a corresponding order must be issued from the director.

The manager also appoints employees who are part of the inspection team. You need to know that the inspection is carried out exclusively in the presence of the financially responsible employee. Next, the commission proceeds directly to the inspection. It includes various actions: taking measurements, counting, weighing. Inspectors make sure that the property is actually in its place. All information is entered into the act, which is then compared with the reports of the accounting department. With simple calculations, you can identify whether there are discrepancies. If there are any, responsible employees find out the reasons.

The last stage of verification is the correct recording of its results. If deficiencies and discrepancies are found, an investigation begins to identify those responsible. As a rule, these are the persons responsible for the property. Responsible employees face administrative punishment.

( Video : “Procedure for carrying out inventory, accounting for surpluses and shortages”)

Objects to be checked

All property that is on the organization’s balance sheet is subject to inventory:

- financial investments;

- fixed assets;

- intangible assets;

- raw materials and finished products;

- inventories held for production;

- various financial assets;

- money, both cash and non-cash.

The financial obligations of the organization are also checked.

These can be credits, debts, loans, etc. Naturally, all this must be accompanied by appropriate agreements, which allow for a correct inventory. There are situations when a check is carried out for a specific department. However, a complete inventory, which is usually carried out at the end of the year, will require maximum effort. Its data is used in the preparation of annual reports. It is this type of check that brings together absolutely everything that may be on the company’s balance sheet.

A complete inventory allows you not only to determine the actual availability of property, but also to check how correctly it is displayed in accounting documents. In addition, the commission makes sure that the equipment is used correctly and the raw materials are stored, and checks how correctly the property is treated. If necessary, certain comments are indicated.

Documentation of inspection results

Naturally, the fact of verification must be documented.

For these purposes, orders, acts, accounting journals, inventories, and collating documents are drawn up. All documents prepared during the inventory process must have at least two copies. There are many standardized forms used for specific situations. They should indicate the following information:

- Company name;

- Title of the document;

- description of objects subject to inventory;

- indication of measurement units, cost and quantity;

- inspectors, their positions and signatures with transcripts.

The legislation does not prohibit adding any new items to the unified form, or changing existing ones. However, you need to remember that the listed points must be left unchanged.

Should an organization keep a journal in Inv 23 form?

Features of the formation of a journal, general information If you are faced with the task of creating a journal of administrative documentation for inventory activities, read the tips below and familiarize yourself with a sample document. Based on our recommendations and example, you can easily fill out the required form.

Before moving on to a detailed examination of the form, we will give some general information. Today, the use of single unified forms of primary documents has been abolished at the legislative level. This means that employees of organizations and enterprises can keep this accounting journal in free form or, if the company has a document template developed and approved in local regulations, by its type.

Many, in the old fashioned way, prefer to use the previously commonly used and mandatory form INV-23.

Read about what forms are intended to reflect deviations identified during the inventory process in the articles: Where you can download the INV-23 log and a sample of its completion. You can download the form corresponding to the INV-23 form approved by the State Statistics Committee on our portal. The document available to you is presented in a convenient Word format. Download form INV-23 At your disposal is also a sample log of inventory orders completed by us in form INV-23.

INV-23 Results An important point in the inventory procedure is the organization of recording orders for its implementation. It allows you not only to compile a list of such documents, but also to monitor the quality and timeliness of various inventory procedures, as well as to effectively plan further inspections.

Info Most often it coincides with point “11”, but not always - the procedure may be delayed.

The procedure for carrying out inventory in the Russian Federation

Before starting the inventory, which will be carried out in anticipation of the annual reporting, it is necessary to take care of the correct execution of all necessary documents. Thus, the verification process can be divided into stages:

- Issuance of an order. The manager must create a written document, which will become the basis for the inspection. A unified form is used for this. Information about the inspectors, property, and inspection deadlines is provided here in detail. The date by which the commission is obliged to carry out all actions related to the inventory is also indicated.

- Typically, the commission includes accounting employees, managers of individual departments, technologists, and economists. It could also be other specialists. As a rule, the head of the department is appointed senior. The inspectors must be accompanied by a financially responsible employee.

- Before the inspection, the responsible employee gives a receipt, which will indicate that all incoming and outgoing documents processed over a certain period are correctly compiled and submitted to the accounting department. The receipt also states that the materials were written off according to the law.

- All measuring instruments that will be used are also checked. The balances that are listed in the accounting department are determined. Specialists record the available documentation before the inspection begins.

- The check itself consists of weighings, recalculations, and measurements. When inspectors take a break, the property must remain secured or locked.

- Preparation of matching statements. This allows discrepancies to be identified. After the inventory, a protocol is drawn up where the commission’s findings are entered.

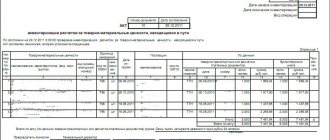

How to draw up an inventory report

The act is drawn up in at least two copies.

It is forbidden to make any edits here. Avoid blots and typos. The corresponding lines indicate the objects being inspected, weight, quantity, etc. When drawing up the report, the signatures of all specialists who are part of the inspection team are required. It must be remembered that if one signature is missing, the document will be considered invalid. After completing the inventory, the employee responsible for these valuables documents the correctness of the commission’s work and indicates that he has no complaints about the inspection.

Download the inventory report in 2021

- Blank form INV-1

If it is necessary to provide information regarding inventory, this form is used. Actual data and accounting information are displayed here.

- Blank form INV-1a

This document provides information about the review related to intangible assets. At the same time, documents are checked that allow the company to use these assets.

- Blank form INV-3

This form is used in cases where inventory items are being checked. As a rule, inventory takes place in warehouses where they are stored. If expired or unusable goods and materials are identified, an additional disposal certificate is issued.

- Blank form INV-10

There are situations when fixed assets are subject to inspection, the repair or construction of which has not yet been completed. This includes machinery, buildings, equipment, and various structures. The audit reveals how actual costs correspond to the costs indicated in accounting documents.

- Form INV-11

The form is designed to verify expenses that relate to future periods. Here, accounting information is compared with actual costs, which are confirmed by primary documents.

- Form INV-15

The form is filled out when taking inventory, which concerns cash. Typically, the check concerns the company's cash register, where actual money, checks, stamps, etc. are checked.

- Form INV-16

Verification regarding strict reporting documents and securities is carried out using this form.

- Form INV-17

Information regarding settlements with suppliers, creditors, buyers and other counterparties is recorded here. The audit allows you to compare accounting data with debts that actually exist.

- Form INV-18

This is exactly the form the matching statement has. It is used when the inventory concerns fixed assets. Here it is recorded how the actual state of affairs differs from the accounting records.

- Form INV-19

This comparison sheet records data relating to inventory items, during the recalculation of which the inspection team identified deviations.

- Blank form INV-22

Before starting the inspection, the head of the company must issue an appropriate order. It is for these purposes that the INV-22 form is used. The deadlines, the composition of the commission, the procedure for carrying out the inventory and its volume are displayed here. Once signed by the director, the document is handed over to a senior member of the inspection team.

- Blank form INV-23

In essence, this form is a journal in which the correctness of the inventory is entered. All orders issued by management before the inspection are recorded here.

- Blank form INV-24

This act includes the results of inventory control checks.

- Blank form INV-25

The results of all control checks, which are intended to determine the correctness of the work of specialists, are entered not only in a special act, but also in a journal in the INV-25 form.

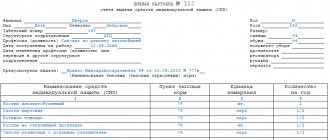

Filling out the tabular part of the INV-23 journal

Direct registration of orders is performed in a journal table containing 22 columns. One order may contain an order to conduct an inventory of various types of property and liabilities, while in order to correctly reflect the results of the audit, it is reasonable to distribute the inspected objects into separate lines depending on the type.

Filling out the INV-23 form:

| Column number | Information to be filled in |

| 1 | The serial number of the line to be filled in; sequential line numbering is used. |

| 2 | Enter the name of the unit, department, site to which the property or liabilities being inspected belongs. If the object being inspected does not belong to a specific division, and the inventory in relation to it is carried out for the entire enterprise, then it is written “as a whole for the organization” - for example, deferred expenses, accounts payable or receivable, financial investments. |

| 3 | The list of persons financially responsible for the objects for which the inventory is being carried out - the full names of the persons responsible for specific objects are listed; the presence of the MOL during the inventory is mandatory. |

| 4 | The date of issue of the order INV-22 is indicated in the header part of the order to conduct an inventory. |

| 5 | Order number - may contain numbers, letters, as well as signs, and is placed on the order form next to the date. |

| 6 | The members of the inventory commission are listed sequentially, including the chairman - full name. |

| 7 | Signature of the person who received the INV-22 order. As a rule, the order is issued to the chairman of the commission. By signing this column, the chairman confirms that he has received the manager’s assignment, is familiar with it and is ready for execution. |

| 8 | Property or liabilities subject to inventory in accordance with the contents of the order - information is taken from the INV-22 form. Each individual type of inventory item is entered on a separate line. |

| 9 | The start date of the inventory procedure is taken from the registered order INV-22. |

| 10 | The actual start date of the inventory, this date may not coincide with the planned one. |

| 11 | The planned completion date of the inspection is taken from order INV-22. |

| 12 | The day on which the inventory procedure is completed. |

| 13, 14, 15 | Preliminary inventory results - the date and amount of identified shortages or surpluses are indicated. Filled out on the basis of inventory documentation. |

| 16, 17, 18 | Final results - filled in after the accountant has summed up the results of the audit based on the documentation received from the commission. The inventory results are shown in a comparison sheet, which is signed by the accountant and approved by the manager, and a decision is made on whether to accept surpluses for accounting and the method of covering shortages. |

| 19 | The date when the manager confirmed the final results obtained with his signature. |

| 20 | The date corresponding to the moment of taking measures to cover the shortage - write-off, compensation for damage at the expense of the guilty parties, if guilt is established. |

| 21 | The date of transfer of the case to the investigative authorities is indicated if it is not possible to resolve the issue of the shortage in any other way. |

| 22 | Explanatory additional information related to the inventory performed. The reason for the inspection may be indicated - replacement of the financially responsible person, indicating the full name of the new MOL and the date of commencement of his functions. Explanations may be given regarding the identified inventory results - the method of writing off or compensating for shortages, capitalizing surpluses. |

The information entered into the INV-23 accounting journal allows you to track the degree of implementation of management’s instructions and orders regarding the inventory of certain types of property and obligations, monitor deadlines, and analyze the results.

The magazine summarizes information about inventories carried out during the calendar year, which greatly speeds up the process of collecting the necessary information. First of all, this is important for medium and large enterprises that conduct a large number of scheduled and unscheduled inspections throughout the year.