In this article we will look at the reversal method. Corrections of errors in accounting. Let's figure out what a reversal is. Let's learn about the cancellation rules.

The need to adjust accounting data in transactions arises due to the inaccuracy of the initial entry or the need to make changes to the indicators. Deleting accounting entries when it is necessary to make changes to accounting is not performed. Corrections in accounting documents are made using the reversal method. The reversal operation is used to adjust transactions - correspondence or amounts.

Differences in the application of red and black reversal methods

Changes to accounting entries can be made with a plus or minus sign. The black reversal method is a plus operation. The red reversal provides for re-recording the erroneous posting with a minus sign while simultaneously indicating the correct data. Negative entries are made in red ink or in parentheses. When maintaining automated accounting, the entry is highlighted in red.

| Conditions | Red reversal | Black reversal |

| Operation sign | Minus | Plus |

| Purpose | Changing totals with an adjusted entry | Deleting an invalid entry |

| Procedure | Drawing up a reversing entry for the exact amount of incorrect data (repetition with a minus sign) while simultaneously recording the correct entry | Drawing up additional return wiring with a plus sign |

Enterprises that use the red reversal method in everyday turnover, for example, when the planned cost deviates from the actual cost, must secure the right to carry out operations in their accounting policies.

What is a “red storno”?

“Red reversal” is a correction method that is relevant when the amounts indicated in the accounting are overstated. Applicable in the following ways:

- if this is a paper journal for accounting, then the reversed entry can be circled with a red pen;

- If a transaction is entered into a computer database, it must be highlighted in red.

At the end of the reporting year, it is necessary to make a calculation in which the amount of the reversed entry is subtracted from the total amount. The correction method is determined by the enterprise itself. The choice of instrument is not specified by accounting rules.

IMPORTANT! It must be borne in mind that the balance will be similar when using any of the types of reversals. The turnover in the accounting account differs.

Example of a “red reversal”

The company has created a reserve for doubtful debts. This operation is reflected by the entry:

- DT 91.02 “Other expenses”;

- CT 63 “Provisions for doubtful debts.” The amount is 1,200 thousand rubles.

Part of the created reserve is written off. It looks like this:

- DT 63 CT 62. Amount 95,000 rubles;

- DT 91 (subaccount 02) CT 63. Amount 15,000 rubles.

ATTENTION! All adjusting entries must be supported by an accounting statement.

Eligibility of using the black reversal method

A number of accountants, instead of making adjustments by canceling entries while simultaneously recording the correct indicators, use reverse entries using the black reversal method. Recording a reverse entry that does not have a documentary justification is an incorrect accounting operation.

The fundamentals of accounting legislation do not contain the concept of “black reversal”. The concept of reversal in domestic accounting applies only to transactions with a minus sign. The method is typical for Western schools of accounting.

There is no specific prohibition in the legislation on the use of black reversals, with the exception of credit institutions in which solvency is based on reporting indicators. When using reverse entry in accounting, debit and credit turnover unreasonably increases, distorting accounting data. Additional turnover appears in the reporting. Black reversal is used to exclude transaction amounts.

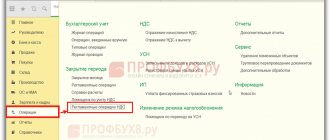

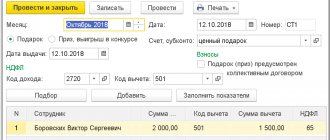

How to make a reversal in 1C 8.3 - the receipt was reflected incorrectly

Let's consider reversing a receipt document in 1C 8.3 Accounting if the accountant entered it incorrectly in the previous period.

On May 18, the accountant discovered that on March 27 he had mistakenly entered the incoming act dated April 7 into the program.

The document Adjustment of receipts will not help in this case. VAT is reflected correctly and there are no errors in the registered invoice. Corrections need to be made only for BU and NU. And also submit an updated income tax return for the first quarter.

Cancel a document manually: open the Manual Transactions and create Document Cancellation .

Fill out the document with reversal entries by selecting erroneously entered receipt Reversed document

Please note: the VAT register data submitted is also cancelled.

Next, register the receipt document on the required date.

To correctly reflect VAT, go to the invoice and delete the second, erroneously entered basis document.

The amount on the invoice will be reflected correctly, and the VAT deduction will not be duplicated.

To exclude such situations, Bukhekspert8 recommends closing the period from adjustments. Read more How to protect yourself from accidental adjustments during closed periods.

We have looked at how reversals are processed in 1C 8.3 Accounting.

For more information on how to make a reversal in 1C 8.2, see the video:

The need for reversal methods

When reversing, amounts are deducted from the debit and credit entries and changes are made to the registers and documentation. Red reversal is used in the following cases:

- The need to make adjustments to accounting due to a technical error or inattention of the accountant. The method is used for correct postings in cases of incorrect indication of the amount;

- Bringing the value expression of uninvoiced supplies to the actual value;

- Withdrawal of the amount of trade margin on goods sold or written off according to the act;

- The need to reduce valuation reserves;

- Adjustments for excess costs of actual costs over planned costs;

- Providing retrospective discounts based on the results of previous shipments of goods.

Reversal data affecting business accounting indicators must be communicated to partners in order to avoid discrepancies in indicators.

In what cases is reversal used?

Adjustment entries are relevant under the following circumstances:

- correction of mistakes;

- write-off of the realized trade margin;

- the planned cost of inventories is brought into line with the actual price. This is relevant for those cases when the actual price is less than the accounting price. A similar situation may arise when uninvoiced supplies are recorded;

- the need for correction to reduce the amount of valuation allowances.

Reversal is a common tool in accounting practice.

Using the reversal method in payroll

Reversal of excessively accrued wages is carried out only in the cases specified in Art. 137 Labor Code of the Russian Federation. Withholding is possible if an accountant commits a counting error or recognizes for employees a failure to comply with labor standards established by a labor dispute commission or a judicial body. Overpayments resulting from incorrect information provided by the employee are withheld based on a court decision. Counting errors occur most often in accounting.

The definition of a counting error is not established by law. It is assumed that a counting error is understood as an inaccuracy due to inaccurate calculation, incorrect rounding of amounts, or the accountant performing erroneous arithmetic operations. In other cases, overpaid amounts are not withheld, but can be paid by the employee voluntarily. To withhold an overpayment in the event of a counting error, it is also necessary to have the consent of the employees. The employer must decide to withhold the excess accrued amount within a month.

An example of adjusting salary data when deducting by reversing

Employee K. was paid a salary of 22,700 rubles for October 2021. The amount of personal income tax withheld was 2,951 rubles, the amount of insurance premiums was 6,855 rubles. When accruing, the accountant made an arithmetic error in calculating the allowance. The correct amount of accrued wages was 22,300 rubles. The deduction was made in the statement for November.

| Operation | Wiring | Amount (in rubles) |

| Operations for October 2016 | ||

| Payroll | Dt 20 Kt 70 | 22 700 |

| Calculation of insurance premiums | Dt 20 Kt 69 | 6 855 |

| Personal income tax accrual | Dt 70 Kt 68 | 2 951 |

| Issuing the amount to the employee | Dt 70 Kt 51 | 19 749 |

| Operations for November 2016 | ||

| Reversal of accrued amount | Dt 20 Kt 70 | 22 700 |

| Reversal of contributions | Dt 20 Kt 69 | 6 855 |

| Reversal of personal income tax | Dt 70 Kt 68 | 2 951 |

| Reversal of the issued amount | Dt 70 Kt 51 | 19 749 |

| Payroll calculation | Dt 20 Kt 70 | 22 300 |

| Calculation of contributions | Dt 20 Kt 69 | 2 899 |

| Personal income tax accrual | Dt 70 Kt 68 | 6 735 |

| Issuing the amount to the employee | Dt 70 Kt 51 | 19 401 |

Document confirming the changes

The use of the red reversal method is confirmed by an accounting certificate . The document does not have a unified form and is drawn up in any form. An accounting certificate acts as a primary accounting document with the obligatory indication of details:

- Names of the enterprise, department;

- Dates of the certificate;

- Data of the responsible person;

- Information about the purpose of the operation;

- Incorrect and correct accounting indicators;

- Value expression and posting accounts;

- The reasons that caused the need for reversal;

- Signatures of the employee who carried out the posting.

The form of the accounting certificate is developed by the enterprise independently and approved in the annex to the accounting policy. Persons responsible for maintaining records are allowed to correct records.

What should I do if an error is discovered after accounting approval?

If the error is found for the next accounting year, there is no need to make corrections to the old accounts. The reversal is entered in the new accounting. For example, in February 2021, a mistake was made that was found only in 2021. Adjustments are made to the accounting records for 2021. This rule is due to the fact that no changes are ever made to the reporting of previous years.

So. Accounting documents require strict reporting. They should not contain arbitrary information. All errors found must be corrected immediately. You can do this in two ways:

- reversal,

- making additional entries.

The first method will be relevant if the transaction amounts were inflated. To make an adjustment, it is not enough to simply make an entry, which must be confirmed by an accounting certificate.

Rules for reversing accounts

When making adjustments, a number of rules must be followed. To apply the red reversal method, it is necessary to determine the date of the adjustment. The order of the chronology of corrections is established in PBU 22/2010. The regulation defines the time frame for correcting errors. The adjustment is made in the current or previous accounting periods. Changes to records from the previous period depend on the fact of reporting. No changes are made to the registers after reporting is submitted.

| Period of inaccuracy | Carrying out adjustments |

| Current period error | Month the error was discovered |

| Error of the previous period discovered before reporting | December of the reporting year |

| Error of the previous period identified after reporting | Current period of operations |

In a similar manner, changes are made to accounting if it is necessary to adjust the facts of economic activity when removing the markup, bringing the planned indicators to the actual ones.

REVERSE ACCOUNTING ENTRY is an entry that must be made on the first day of the next accounting period.

[p.507] Reverse accounting entry 507 [p.801] The enterprise prepares an accounting entry with reverse correspondence of accounts [p.201]

Enterprises receive the bulk of their profits from the sale of products, goods, works and services (realization financial result). Such profit is defined as the difference between the proceeds from the sale of products in current prices without value added tax, special tax and excise taxes and the costs of its production and sale, included in the cost of products (works, services), also without VAT, SN and excise taxes. The list of these costs is determined by the provisions on the composition. all costs included in the cost of production, and the procedure. formation of financial results taken into account when taxing profits, approved by the Government of Russia in agreement with the Supreme Council (Appendix 4). The results from the sale of products are written off monthly from account 46 Sales of products (works, services) to account 80. Income from sales is transferred as an accounting entry to the debit of account 46 Sales of products (works, services) and to the credit of account 80. Write-off of losses is recorded as an accounting entry with reverse correspondence accounts. [p.112]

Agricultural organizations that have an annual production cycle close accounts 46 once a year - at the end of the year. The write-off of profit is recorded as an accounting entry, debiting account 46 Sales of products (works, services) and crediting account 80 Profit and loss. Write-off of losses is documented by accounting entry with reverse correspondence of accounts. [p.455]

At the same time, accounting entries provide feedback between accounting objects. With their help, data on the functioning of the controlled system is transferred [p.380]

Reverse entry method - this method is used to correct incorrect entries in accounts. The essence of this method is that it is a way of drawing up additional accounting, but reverse entries. [p.175]

Negative exchange rate differences are recorded as reverse accounting entries in relation to positive exchange rate differences. [p.396]

It is interesting to note that in some countries, for example in the USA, the preparation of a balance sheet is treated in the same way as the closure of accounts and is formalized by the corresponding entries, with the help of which the General Ledger accounts are posted among the balance sheet items; material, monetary and partially settlement accounts are transferred to the balance sheet asset, and stock and partially current accounts - in liabilities. As a result of this operation, all accounts are closed. The new reporting period begins with reverse postings. A similar approach, in a veiled form, was also proposed by individual representatives of the Russian school of accounting. In particular, Professor N. S. Pomazkov (1889-1969) recommended writing the final account balance not on the strong side, as is traditionally done by accountants, but on the weak side [p.200]

The assessment of currency and currency values and other property contributed as contributions to the authorized capital may differ from their assessment in the constituent documents. The difference arising in this case is written off to account 87 “Additional capital”. A positive difference in estimates is reflected in the debit of the property, currency and currency valuables accounts and the credit of account 87, and a negative difference is reflected in the reverse accounting entry. This procedure for writing off differences in prices and exchange rate valuation allows you not to change the share of the founders in the authorized capital specified in the constituent documents. [p.57]

At the end of the month, the difference between the actual cost of the materials consumed and their cost at fixed accounting prices is determined. The difference is written off to the same cost accounts to which materials were written off at fixed accounting prices (accounts 20, 23, 25, 26, etc.). Moreover, if the actual cost is higher than the fixed accounting price, then the difference between them is written off with an additional accounting entry, while the reverse difference (which is possible when using the planned cost of materials as a firm accounting price) is written off using the “red reversal” method, i.e. negative numbers. [p.127]

Profit from previous years, identified in the reporting year, is reflected in the debit of account 51 “Current account” and the credit of account 80 “Profits and losses”; losses are recorded using a reverse accounting entry. [p.317]

The fact of theft of materials from a warehouse is recorded in accounting in the form of a redistribution of material assets from one active account 10 “Materials” to another active account 84 “Shortages and losses from damage to valuables.” The balance currency does not change. If the culprit of the theft is found and the materials are returned, a posting will appear that is the opposite of what was done. [p.50]

Profits of previous years identified in the reporting year are reflected in the debit of account 81 Use of profit and the credit of account 80 Profits and losses. Losses are recorded using a reverse accounting entry. [p.113]

If, according to the processing conditions, corrections cannot be made in this way, then erroneous entries are corrected by reversing (reversing) the erroneous entry and posting a new correct entry. The reversed entry in the registers is marked with a distinctive sign. For the wire, two orders are drawn up on the current day - reversed and correct. Orders are signed, in addition to the accounting employee, by a supervisory employee. [p.224]

At the same time, the amount of depreciation of the IBP, taken into account at the time of revaluation of property on account 13, is credited to the depreciation of fixed assets (d-t account 13, set account 02) within the amount of depreciation subject to accrual at the current rates for fixed assets transferred from the IBP, additional accrual of the amount of depreciation of fixed assets is reflected by entries in the accounting accounts of the account. 87-1 - for production facilities of fixed assets and accounts. 88-4 - for non-production, set of accounts. 02 the decrease in the amount of depreciation of fixed assets for the above operation is taken into account by reverse accounting entries. [p.14]

A reverse accounting entry is made for the amount of fulfilled obligations secured by the pledge. [p.59]

When the loan is repaid, a reverse accounting entry is made for the value of the returned shares. [p.60]

Capitalized to the central instrumental warehouse of the head enterprise of the IBP at on-farm planned prices, manufactured and handed over by a specialized enterprise or other specialized divisions for internal consumption during intra-balance sheet calculations (a decentralized form of organizing accounting (financial) accounting; these divisions make up reverse accounting entries) 79-2 [ p.143]

At the same time, the depreciation of fixed assets transferred to the IBP is written off, with the transfer of this balance to the depreciation of the IBP d-t account. 02-1, set count. 13 - within the amount of depreciation of the IBP subject to accrual on the cost of objects included in the IBP from fixed assets, while the additional accrued amount of depreciation of the IBP is taken into account by the accounting entry d-t. 88-3, 96, set of accounts. 13 - for property of the intended purpose and dt account. 88-4, 96 - for social sector property, and the decrease in the amount of depreciation of the IBP in comparison with the balance of depreciation of fixed assets transferred to the IBP is taken into account by reverse accounting entries. [p.145]

If operations to form the authorized (share) capital are carried out in foreign currency, then the amount of the exchange rate difference between the assessment of the deposit on the date of its registration and the assessment of the actual deposit, expressed in foreign currency at the rate of the Central Bank of the Russian Federation, is sent to regulate the organization’s additional capital in the amount of positive differences d-sch. 01, 04, 06, 10, 50, 51, 62, 76, other property and settlement accounts (the value of the contribution increases in the assessment as of the date it was registered), set of accounts. 87-2, a reverse or reversal accounting entry records the amount of the negative exchange rate difference (you can also capitalize the deposit on the date of the actual contribution at the foreign exchange rate announced by the Central Bank of the Russian Federation from the credit of account 75-1 and for the exchange rate difference d-t account 75-1 (87 -2), count 87-2(75-1). [p.455]

The return of the deposit is reflected by a reverse accounting entry (account 51 is debited and account 76 is credited). [p.389]

Profit from previous years identified in the reporting year is reflected in the debit of account 51 Current account and the credit of account 91. Other income and expenses, losses are recorded using a reverse accounting entry. In the same way, receipts for compensation and compensation for losses caused to the organization are taken into account. [p.522]

As a rule, such posting negates the results of the adjustment. Reverse accounting entries can only be made for corrections that increase assets or liabilities, or when using computer programs. [p.507]

The financial result from the sale of products, identified in the Sales account, is recorded in the Profit and Loss account at the end of the reporting year. For the amount of accounting (calculated) profit from the sale, the accounting entry D-t of the Sales account, K-t of the Profit and Loss account is drawn up. When selling products at a loss, a reverse accounting entry is drawn up D-t account Profit and loss, K-t account Sales. [p.313]

Accounting for transactions for the return (repayment) of funds in the balance sheet of the creditor bank is carried out by entries reverse to the above. [p.185]

Accounting for the return of previously provided funds in the balance sheet of the borrowing bank is made by entries that are the opposite of those stated above. [p.190]

To reflect permanent tax assets in accounting, it is necessary to make a reverse entry. [p.990]

The write-off of profits is made out by an accounting entry, debiting account 46 “Sales of products (work, Profit and loss.” The write-off of losses is made out by an accounting entry with reverse correspondence of accounts. [p.314]

In active accounts, debit shows the initial balance (balance) and its increase, and credit shows its decrease. In passive accounts, entries are made in reverse order. Each business transaction affects two accounts. Equal amounts are recorded in the debit of one account and the credit of another account. This method of recording business transactions is called double entry. > The indication of the debited and credited account and the amount reflected in the accounting of a business transaction is called an accounting entry, and the relationship of accounts is called correspondence of accounts. [p.286]

The reasons for the emergence, logic of formation and prospects for the development of these areas are quite obvious. First, at the business entity level, finance and accounting are closely intertwined. We hardly dispute the thesis that it is impossible to become a competent financier without proper and, we note, very decent knowledge of the conceptual foundations of accounting, its logic and technology. The opposite is also true, an accountant who limits the scope of his activity to following standard transactions, who does not want to delve into the specifics of financial planning, budgeting and financial simulation, will never be able to rise above the level of an ordinary clerk. It is no coincidence that in developed countries, in particular in countries professing the Anglo-American accounting model, a distinction is made between an accountant and a bookkeeper. The fact is that financial decisions at the enterprise level are essentially reduced to (a) to optimize its balance sheet, which, as is known, is the best financial model of the enterprise, and (b) initialization and optimization of cash flows. Such decisions, on the one hand, are based on a thorough understanding of the principles of the movement of funds through accounting accounts, and, with on the other hand, they involve the use of a variety of financial models, taking into account, among other things, the stochastic nature of the parameters of many operations and the time value of the transaction [p.283]

When an association or other large enterprise uses internal balance sheet calculations, as well as divisions of the enterprise allocated to a separate (independent) balance sheet, in addition to the indicated, an accounting entry is drawn up for the amount of recorded balance sheet profit, transferred monthly to the balance sheet of the association (in the general balance sheet) d-account . 80, set count. 79-2 (a combination of the same amount constitutes a reverse accounting entry). [p.308]

Under operation 1.3, in a situation where the property, in accordance with a short-term loan agreement, is provided to the borrower at its book value (accounting) value, the lender writes off the property with an accounting entry d-ac. 58-3, set of accounts. 01, 04, 12 (at residual value), 07, 08, 10, 11, 20, 23, 29, 40, 41 for the amount of depreciation recorded on the date of transfer of property (operations 1.3, 1.4) d-account. 02, 05, 13, count. 01, 04, 12-2 (respectively) for operation 1.4, if the balance sheet (for depreciable property - residual) value of the property contribution is higher than the contractual value, the resulting difference is credited to additional capital d-t. 58-3, set of accounts. 87-3 (with inclusion in taxable profit), otherwise the difference is written off from the net profit of the account. 88-1, 88-2, 88-3, set of accounts. 58-3. [p.386]

Reversal method. Correcting Accounting Errors: Examples of Using Reversals

One of the mistakes is when an incorrect entry may be made when reflecting accounts. Cashier M. of the enterprise gave employee S. an accountable amount of 5,200 rubles for business needs. At the time of the transaction, the cashier applied the amount to the payroll account. The error was discovered in the current period when summing up monthly results. In the accounting of an enterprise, the accountant makes entries:

- Adjustment of postings using the reversal method: Dt 70 Kt 50 in the amount of 5,200 rubles;

- The amount given to the employee is reflected: Dt 71 Kt 50 in the amount of 5,200 rubles.

Conclusion: the red reversal adjustment did not affect the results of the month. Another common mistake is recording the transaction amount in a larger amount.

Cashier N. carries out payroll calculations in the branch using a cashier authorized to issue amounts in the branch. The amount of the payroll for the payment of wages for March amounted to 87,250 rubles. Cashier N. indicated to the cash register and issued the amount of 97,250 rubles. The error was discovered when the settlement with employees was completed and the statement was submitted to the cashier. The following entries are made in the company's accounting:

- Reversing an incorrect transaction amount: Dt 70 Kt 50 in the amount of 97,250 rubles;

- Entering the correct entry: Dt 70 Kt 50 in the amount of 87,250 rubles.

Conclusion: the error, which arose due to the carelessness of the cashier and the distributor, was eliminated this month.

Reversal rules

Proper reversal solves several problems at once. A correctly compiled report helps you quickly understand the trading operations carried out. It is also important to ensure the company's protection during tax audits. Let's look at the basic rules for making a reversal:

- If an incorrectly entered entry was identified in the current period before the delivery was made, then the corrections are indicated under the date of the day ending the quarter.

- The reversal can be made on the discovery date, but this is subject to certain conditions. In particular, this is relevant when identifying an error in the delivery period, which has already passed.

- Each of the adjusting entries must be confirmed by an accounting certificate. This document states the reason for making the corrections, as well as the amount of the new entry.

- All accounting entries must match the primary documentation. Entries are always supported by associated papers. If the information does not match, the company will have problems when passing tax audits.

Making a reversal is a relatively simple procedure. However, in practice, this wiring raises many questions.