Causes and common types of errors

Payment orders are usually drawn up by an employee of the accounting or financial department. When filling out a document manually, errors are inevitable. Most often, employees make mistakes in the contract number or its date, incorrectly indicate the name of the paid goods or services, and when transferring tax, they make mistakes in the BCC and payment period. In 2021, due to the change in the VAT rate from 18% to 20%, cases of errors in indicating the tax rate and amount have become more frequent. We will tell you how and in what cases to write a sample letter about an error in the purpose of payment.

Some details must be corrected, but in some cases this is not necessary. A clarifying letter must be drawn up if the translation cannot be clearly identified, that is, it cannot be determined for what and on what basis the payment was made. If the error is not critical, a clarification notice need not be drawn up.

What are the dangers of erroneously allocating VAT to a special regime person on a payment slip?

File sample letter about erroneous indication of VAT in a payment order for viruses. Usually, in the event of an erroneously indicated purpose of the payment, an official letter is drawn up informing the recipient about. Download the sample application for clarification of payment. Rubles and kopecks are considered correct as the subsequent purpose of payment. If mistakes were made in the recipient’s kbk, tax identification number or checkpoint, the tax authorities will first send a notice to the treasury.

2018-03-2222.03.2018 18:48

Hello, you are absolutely not obliged to pay such VAT. After all, you did not issue an invoice to the buyer with allocated VAT (clause 5 of Article 173 of the Tax Code of the Russian Federation). However, if you do not correctly justify this VAT in the payment slip to the tax authorities, then rest assured, they will not keep you waiting. They will come by direct message with an on-site inspection. By the way, tax officials firmly believe that if you issue an invoice, you will also be required to file a VAT return.

They are asking you to give an explanation completely legitimately, because they are acting in accordance with paragraph 3 of Art. 88 Tax Code of the Russian Federation. In addition, they have every right to call you to give explanations (clause 4, clause 1, article 31 of the Tax Code of the Russian Federation). Therefore, your task now is to urgently remove VAT from that payment slip. To do this, you first need to notify your customer that he made an error in the payment order. Ask him to draw up and send a letter to his bank stating that they made a mistake in assigning the payment, and he asks to make corrections to it. The bank must put a correction mark on this letter and inform your bank that there was an error in the payment and it needs to be corrected. In turn, your bank will inform you that changes have been made to the payment order. Something like this.

Who and in what cases draws up a notification to clarify the details of the payment order?

A letter of clarification is drawn up and sent by the person who transferred the funds. After all, only the payer has the right to dispose of his funds.

If the recipient of the money believes that there is an error in the payment order, he needs to contact the payer and request a correction. The recipient of the money cannot independently take into account the funds at his own discretion without the permission of the payer.

| Error | Do I need to fix it? | Why |

| Wrong contract | Yes | The supplier may consider the payment as an advance under an erroneous contract and not pay the actual debt for goods and services. In this case:

|

| Incorrect name of product or service | Not necessary | If there are frequent errors or a large transfer amount, the discrepancy between the specified product or service and the recipient’s activity may raise questions from the bank, including blocking the account. It is better to indicate the correct name of the product or service, but in case of widespread errors, they still need to be clarified. |

| VAT rate | No | There are no legal or tax risks. Here, problems may arise for the payer when offsetting VAT from the supplier's advance payment by the Federal Tax Service if the inaccuracy flows into the advance invoice. |

When and how can the inspectorate detect VAT on a payment invoice?

The inspectorate may discover that VAT is included in the payment order much earlier than it comes to you for an on-site inspection. Tax authorities will see this during a desk audit of your declarations for the period in which the payment was made with the erroneously allocated VAT. The fact is that, when checking your declarations, the inspectorate may request from the bank statements from the taxpayer’s bank accounts (Clause 2 of Article 86 of the Tax Code of the Russian Federation). The statement (Appendix 4 to the Order of the Federal Tax Service of Russia dated March 30, 2007 N MM-3-06/ [email protected] ) for each payment indicates, among other things, its purpose, the wording of which the bank transfers from the corresponding field of the payment order. When analyzing statements, tax authorities specifically pay attention to payments including VAT. After all, apart from an on-site inspection, this is the only way to identify cases of VAT filing by those who are not payers of this tax.

Note Of course, the inspection can detect the VAT allocated in the payment during an on-site or desk inspection carried out at the buyer. However, in this case, the buyer will not have your invoice (since you did not issue it), and the inspector will have no reason to suspect you of filing VAT.

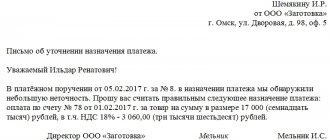

We draw up a correction letter about the purpose of payment in the payment order to the supplier

When it is necessary to change the purpose of payment in a payment order, the letter is drawn up in any form. There is no approved form at the legislative level.

The document must indicate:

- document number and date;

- sender and recipient data;

- details of the payment document in which the error was made;

- correct name of erroneous details;

- signature of the responsible persons (the same ones who signed the payment).

You can send a notification in any convenient way. It is not necessary to receive notification from the counterparty about the receipt of the letter. But it’s better to get it to make sure that the recipient of the money has made accounting corrections.

Sample letter about the correct purpose of payment

Error in payment order. Their correction, types

Whether you are the payer or the recipient of money, you may need to change the purpose of the payment in a payment order already executed by the bank. How to do it? You will not find any specific rules in this regard in the regulations.

But legal disputes about which purpose of payment is considered valid - the original or the changed one - arise constantly. Arbitration practice will tell you how best to act so that no one has any claims against you later.

Note

https://www..com/watch?v=ytcreatorsru

In this article we do not touch upon errors in payment orders for the transfer of taxes and fees. We will only talk about payments between counterparties.

At first, the bank said that they would only accept transfers made on the basis of accounts. We quarreled with half of the organizations, because... they didn't want to give them. Two weeks later, a representative of one of these companies came, which flatly refused to issue accounts, and demanded to call the bank, but it immediately turned out that it was a joke.

They accept payments in any case, as long as the purpose contains a reference to the number of a document.” In general, not everything is as difficult as it seems. The issue can always be resolved in several ways by agreeing with partners or the bank. We are all human, we all make mistakes, so it’s worth meeting each other halfway.

Of course, it makes sense to support your position with relevant documents and knowledge of the law, so that in the future neither the tax office nor the bank will have any questions at the most inopportune moment. Solving the problem after the fact will be much more difficult. However, there is no need to panic, because it is never too late to correct the situation. There would be a desire.

The error may be detected by the payee. Since he cannot independently correct the purpose of the payment, he must make this request to the payer. There are cases when the recipient independently corrects the error and notifies the payer about it. However, in case of disputes, the truth will not be on the recipient’s side, so it is better not to do this.

It is the payer who can send a letter about changing the purpose of payment (we will provide a sample at the end of the article) to the bank. Thus, if the payer himself discovered an error in the payment, he must proceed as follows: agree on a change in the purpose of the payment with the recipient; consent must be asked to be given in writing.

When receiving a written order from a client to transfer funds, the bank is obliged to conduct a comprehensive check of the data specified in it, including the details of the payee (clauses 2.1, 2.7 of the regulation “On the rules for transferring funds”, approved by the Bank of Russia on June 19, 2012 No. 383-P, hereinafter referred to as Regulation No. 383-P).

In this case, the procedure for accepting for execution, recalling and returning client orders is established by the bank itself (clause 2.2 of Regulation No. 383-P). In particular, the credit institution determines the list of payment order details required for verification, which usually include:

- name of the payee;

- his TIN;

- BIC of the recipient's bank.

Failure to indicate or incorrect indication of checkpoint details in a payment order rarely causes negative consequences for both the sender and the recipient of the payment.

If there is an error in the payee's checkpoint, the funds themselves will be transferred to his account, although in some situations the bank may request clarification from the sender of the payment order.

If the funds are sent to the account of a budgetary institution, then they will go to the desired current account, but may remain in the treasury of such an institution as unidentified payments.

How to change the purpose of payment in an executed payment order

Note

https://www..com/watch?v=ytdevru

(or) correct the error. For example, your buyer allocated VAT when sending you a payment for a transaction not subject to this tax, you yourself incorrectly indicated the contract number in the payment, etc.

The courts do not see any obstacles to correcting such technical errors in the purpose of payment {amp}lt;1{amp}gt; and they even believe that this can be done without the consent of the counterparty {amp}lt;2{amp}gt; and without notifying the bank {amp}lt;3{amp}gt;.

Legal meaning of changing the purpose of payment

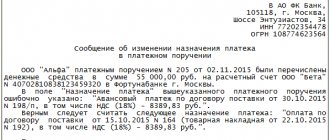

There is no unified form of the letter, so drafting it is often difficult, especially when the company encounters this for the first time. How to change the purpose of payment in a payment order, how to correctly compose a message to the bank?

The message is written in free form.

The letter must include the following information: the number of the payment order, the date on which it was drawn up, the amount of the transfer, the payer, the recipient of the funds and his current account.

In addition, in the text of the message it is necessary to indicate the purpose of the payment, which must be considered incorrect, and the purpose that the payer asks to be considered correct.

A message about changing the purpose of payment must be sent to the bank in two copies. The message must be signed by the same persons who signed the initial payment order with an incorrect payment purpose. The message can be sent to the bank by a valuable letter with a description of the attachment or delivered during a personal visit.

If you decide to send a message by letter, it would be a good idea to attach to the letter a copy of the payment order being corrected and the recipient’s written consent to make the corrections. If you are sending a message to the bank in person, ask to put a mark indicating receipt of the message on your copy of the letter.

Typically, banks do not refuse requests to correct the purpose of an executed payment. However, the bank may ignore the payer’s request or refuse.

In this case, it is important that the payer has confirmation of sending the message in the form of a copy with a bank mark on receipt or a post office mark on sending the letter.

In case of disputes, this will be proof that the payer contacted the bank with a request.

It is worth considering one more point: despite the fact that there is no deadline during which you can clarify the change in payment, you should not put it off for a long time.

In case of disputes, the court may declare the change in the purpose of payment invalid due to the long period of time that has passed from the moment of transfer of money to the date when the payer requested to change the purpose of payment.

Errors in payments occur not only when paying with the Federal Tax Service and extra-budgetary funds, they can also arise when working with counterparties. The following situations may occur:

- The TIN is entered incorrectly. The bank will not be able to demand clarification from the taxpayer if the remaining points of the payment document are filled out correctly;

- The basis for the payment is entered incorrectly. Since the funds will find the right recipient, it is not difficult to correct the situation. You just need to contact him and then attach a letter with his response to the payment order. Despite the harmlessness of the error, it needs to be corrected so as not to confuse accountants and tax authorities;

- Allocation of VAT in payment orders to companies under a special tax regime. If an enterprise that, due to paying taxes under a special tax regime (USNO, for example), does not pay VAT, is sent a payment slip with the allocated amount of this tax, the company will be forced to transfer this amount to the budget. When a company paying VAT at a reduced rate (0% or 10%) receives a payment with VAT at a rate of 18%, it will have to pay tax at a high rate. If such errors occur, the sender is required to send a clarifying letter to the bank, which in turn will notify the banking institution of the payment recipient;

- Incorrect purpose of sending money. The money was transferred for one purpose, but the statement indicated other reasons for sending it, for example, an advance payment was made for services, but the payment statement indicated a loan. If the situation is not corrected by notifying banking institutions, the tax service will not allow a tax deduction for the advance payment;

- Incorrect indication of the counterparty's details. Sometimes companies forget to inform their partners about a change in payment details, and the funds remain in the bank until the circumstances are clarified. Over the next 5 days, a bank employee will make inquiries about who the payment was intended for. There are two options here. Either notify the bank about the error, or receive the money returned on the 6th day and reissue the payment document).

It is necessary to note some positions of the courts on the possibility of correcting such an error in a payment order:

- In itself, changing the purpose of payment on the basis of a letter sent to the counterparty does not contradict the law (resolution of the North-Western District Court dated June 13, 2021 in case No. A56-33705/2015). The parties can resolve the issue of changing the said details through mutual agreement, without then contacting the bank.

Source: https://kupit-krohe.ru/obrazets/oshibka-naznachenii-platezha/

How to correct a tax payment

There are rules for clarifying tax payments:

- No more than three years have passed since the date of transfer.

- Clarification will not lead to arrears.

- The payment went to the budget.

It is impossible to clarify the payment if the payer made a mistake in the Federal Treasury account number or bank details. It is considered not to have been received by the budget, and can only be returned.

To correct an error in a payment order, you must compose a letter in any form and also attach a copy of the incorrect payment order to it.

The payment slip indicated VAT by mistake, what should I do?

Then the buyer will take it and indicate the amount of tax in the payment order. It will turn out that the previous accountant wrote out invoices for some reason... Anything, as they say, can happen. In this article we offer you an overview of VAT errors and possible methods for eliminating them.

Error No. 1. The buyer accidentally allocated the VAT amount in the payment order

If the buyer is a VAT payer, transferring money to you, he can allocate VAT, as they say, “automatically”. Despite the fact that the contract does not provide for VAT and you also do not highlight it in the primary documents, you do not issue an invoice.

And the buyer can indicate in the “Purpose of payment” field: “Including VAT - 18%” or even calculate the exact amount of tax by calculation.

We immediately hasten to reassure you: due to this mistake on the part of the buyer, you do not have the obligation to pay tax to the budget.

And you don’t need to submit a VAT return either, since you didn’t allocate or charge VAT yourself. However, this does not mean that nothing needs to be corrected.

An important point. If you did not charge VAT on sales and did not issue an invoice, you do not have an obligation to pay tax to the budget, even if the buyer allocates VAT in the payment order.

What to do. Send a message to the counterparty that the VAT amount was allocated erroneously in the corresponding payment order. Since the price does not include tax, and your company applies the simplified tax system. This letter, along with the primary transaction documents, will confirm the accuracy of your accounting.

Sample letter about incorrect purpose of payment to the Federal Tax Service

When composing a notice, it must indicate:

- sender's details (name, address, TIN, OGRN);

- tax office details;

- data of the payment document in which there was an inaccuracy;

- details that need to be corrected with their correct values.

Sample letter about the correct purpose of payment to the tax office

You can send a notification:

- in writing in person to the Federal Tax Service or by mail;

- in electronic form through an EDF operator.

Is it possible to challenge a payment change?

Sometimes the recipient of the money does not agree with the changes made by the payer. Unfortunately, it is quite difficult to challenge a letter of clarification. This must be done in court. It is advisable to resolve the problem through negotiations.

When making changes to the purpose of payment, you must remember that such transactions are carefully reviewed by regulatory authorities. If the Federal Tax Service sees signs of tax evasion in such letters, then claims may be made: additional taxes and penalties will be assessed. The most common issue that arises is prepayment under a supply agreement, which is later reclassified as a transfer under a loan agreement. This clearly shows a way to avoid paying VAT on the buyer's advance payment, and questions from the tax inspectorate are inevitable.

Letter to counterparty

How to write a letter to clarify the purpose of payment

A letter about changing the purpose of payment is a notification to the counterparty, which indicates the need to correct an error when processing a money transfer. The documentation must be drawn up correctly so that it is clear where the problem occurred. The document storage time must be observed.

Instructions are usually issued by an employee of the finance or accounting department. If document fields are filled in manually, there is a risk of errors. Often, blots are associated with incorrect indication of the contract number, date, name of goods; when transferring value added tax, the BCC or payment period is entered incorrectly.

A letter with clarification is issued by the person who transferred the funds. This is due to the fact that only the payer can manage his money. If the recipient is sure that the order was drawn up incorrectly, it is necessary to contact the payer and make a request for adjustments.

It is mandatory to correct shortcomings related to the indication of the contract. This is due to the fact that the supplier may consider the payment as an advance under an erroneous contract. The supplier will then need to pay VAT on the advance payment.

If it is necessary to make changes to the purpose of payment, the letter can be drawn up in any format, since there is no approved form. The documentation must include the date of preparation and document number, information about the sender and recipient, data on the payment document with a blot, and the name of the details where adjustments need to be made.

There are some features of clarifying tax payments. To correct the error, you need to compose a letter and attach a copy of the incorrect payment to it. When drawing up a notification, you should display the details of the sender and tax authorities, information about the payment document with inaccuracies, and details with correct data.