Good afternoon, dear readers. The time has come to talk about the use of the UTII (single tax on imputed income) payment, which is very convenient for businessmen and easy to calculate.

Today you will learn:

- Can you apply UTII;

- Restrictions on the use of tax;

- Calculation of UTII.

UTII

This is one of the types of special modes. The tax is classified as “regional”, since it begins to operate only on the basis of decisions of municipalities (as Moscow did and abolished in 14).

A special tax regime, and in particular a single tax, was introduced to simplify the accounting of small and micro enterprises. Since 2013, the choice of UTII occurs at the merchant’s own request. Both companies use UTII.

The use of UTII exempts your business from paying income tax, property tax and VAT; other taxes and contributions are paid without changes.

The tax rate is in no way aligned with your actual income. The exact name of UTII: a single tax on imputed income for certain types of activities (where the key word is “separate”). Therefore, let's figure out what kind of activity a businessman can choose to use UTII.

Conditions for the transition to UTII

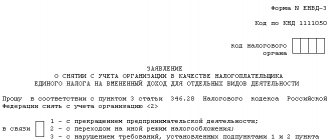

From January 1, 2013, the transition to paying a single tax is carried out voluntarily. Deregistration as a UTII payer is carried out on the basis of an application submitted to the tax authority. Taxpayers have the right to switch to a different tax regime from the beginning of the calendar year (Article 346.28 of the Tax Code of the Russian Federation).

Conditions for the transition to UTII for individual entrepreneurs

A special application for UTII is submitted to the tax office. It is complete, not typical. For individual entrepreneurs in 2021, a special form is established in the application for the transition to UTII. The entrepreneur must fill it out in 2 copies. If a citizen does not switch from the simplified tax system to UTII, but only opens his own business, then this must be done within 5 days from the date of registration. Also find out how much taxes the individual entrepreneur pays in total.

Usually an application is submitted at the place of work of the individual entrepreneur, but some types of activities require the citizen to visit the tax office at the place of residence. These are activities such as:

- retail trade under UTII (distribution, distribution of products);

- placement of advertising materials on transport;

- cargo transportation services.

Conditions for the transition to UTII for legal entities - LLC

To transfer an LLC to UTII, an application is also written. How to switch to UTII? This can be done in winter, as well as in the summer of one year. If a businessman has decided to leave the simplified tax system and switch to UTII, he must inform the tax office about this. And do this no later than January 15 of the year after the transition (or no later than 15 days following the quarter of loss of the right to use the simplified tax system).

You can cancel UTII from 2021 voluntarily, according to Art. 346.28 of the Tax Code of the Russian Federation, as well as by force of law, when an LLC or individual entrepreneur ceased to meet the established rules that previously gave the businessman the right to apply this fee.

Also find out whether UTII for individual entrepreneurs will be completely abolished from 2021 to 2021 and what will happen in return.

The procedure for switching to UTII

Includes writing an application on behalf of the entrepreneur, as well as strict compliance with the deadlines for the transition or the possibility of application during the initial registration of the business.

List of UTII activities

The Tax Code of the Russian Federation contains a register of types of commercial activities that allow the choice of UTII.

Let's list them:

- Provision of household services;

- Veterinary Service;

- Washing, repair and maintenance of vehicles;

- Paid car parking (excluding penalties);

- Road transportation of freight and passenger transport (if this business has no more than 20 units of equipment);

- Stationary retail trade, trading hall 150 sq. m.;

- Retail trade, in which there is no trading floor and mobile retail trade;

- Catering, with a hall for visitors also up to 150 sq. m.;

- Catering service without a hall for visitors;

- Street advertising structures;

- Advertising on transport;

- Hostels, motels, hotels, boarding houses (with a total area of up to 500 sq. m.);

- Leasing of retail outlets for stationary retail (without a sales area), mobile retail outlets and catering facilities (without a service area);

- Leasing of land for retail and catering.

Of course, officially and in more detail, types of commercial activities are listed in the All-Russian Classifier (OKVED 2). But let’s try to decipher the list in our own words:

- This is the so-called KBO (consumer services plant, operating in Soviet times), this includes the repair and production of sewing and knitted products, repair and production of shoes, hairdressers, solarium, beauty salon, repair of all types of household appliances and equipment, saunas and baths, laundry, rentals, jewelry and funeral services. Now I have added to the list (minor repairs in the house “from nail to light bulb”). This category also includes glazing of balconies, installation of doors, windows and metal fences. Another direction: art schools, tutoring, organizing holidays and matinees, various clubs, sections and gyms. And also nannies, nurses, governesses (I repeat, the list is very long);

- Veterinary clinics and pharmacies;

- Points three through seven are probably self-explanatory;

- Catering includes: cafes, restaurants, bars, canteens, snack bars (bistros), cafeterias, culinary shops, including bakery products.

Above we have listed the complete list valid in the Russian Federation. However, at the regional level, certain positions are finally formed (by decision of the municipality); for clarification, you must contact your territorial tax authority (or administration).

Conditions for using UTII

Let's consider the essential conditions for the transition to the UTII regime (the same for both individual entrepreneurs and enterprises):

- The UTII regime is used in this territory;

- The number of employees is no more than one hundred people;

- The type of activity presented is included in the decision of the local government;

- If you do not lease gas stations;

- If you are not working under a simple partnership or trust property management agreement.

The following additional requirements apply to the company:

- This cannot be an enterprise from the category of the largest tax payers;

- This cannot be an educational, health or social institution. provision;

- The percentage of contribution in the authorized capital of other companies is up to 25 percent.

There is one more restriction: you cannot apply UTII if you pay a single agricultural tax.

To summarize, if your commercial activity fits within this framework, then from January 1 of next year feel free to use the special imputed tax regime. However, remember that you only have five working days (from the date the store opened) to fill out an application for tax registration (after all, you do not want to pay a fine).

If your company combines several types of commercial activities:

- All types of activities require UTII, which means that physical indicators are taken into account separately for one type of activity;

- There are types of commercial activities that are subject to other taxes, which means that you need to maintain separate accounting records for different tax regimes.

If your company “works” under the authority of several tax inspectorates, UTII declarations must be submitted separately for all inspections.

Who cannot apply UTII?

Having talked about what types of activities fall under UTII, it is worth saying a few words about those who cannot apply imputation. These include:

- Individual entrepreneurs and organizations that provide catering services in educational, medical and social institutions.

- Individual entrepreneurs who switched to a patent taxation system and acquired a patent for a type of activity that falls under UTII.

- Individual entrepreneurs and organizations in which the average number of employees for the previous calendar year is more than one hundred people.

- If the share of third-party organizations in the enterprise is more than 25%.

- Individual entrepreneurs or organizations leasing gas stations or gas stations.

- Largest taxpayers.

- Individual entrepreneurs and organizations that have ceased activities that were subject to UTII.

Calculation of UTII

The formula for calculating tax is not difficult: the tax base multiplied by the tax rate. At the same time, the tax base consists of a physical indicator multiplied by the basic (imputed) profitability.

The tax rate is 15%, but in 2015 legislators introduced an amendment, allowing the tariff to be reduced to 7.5% at the local level (to be honest, I have never heard of anyone taking advantage of this right). The basic profitability is determined by the type of your business activity (see “Can you apply UTII?”).

The tax base is also specified by coefficients K1 and K2. The K1 coefficient, called the deflator, is approved at the state level. The K2 coefficient is influenced by the type of services provided, population size, occupied area, seasonality, number of seats, product range, etc., and is established by decision at the local level.

When calculating, it is permissible to reduce the amount of tax by insurance premiums from the payroll of employees directly engaged in commercial activities for which you pay UTII (but only 50% of the tax, even if the amount of contributions is much larger).

The illustrations are clearer and simpler:

Example #1:

- retail sale of alcohol;

- sales area 50 sq. m.;

- Omsk city;

- accrual from payroll RUR 12,500;

- this year.

Let's calculate the amount of tax for the quarter: UTII = (1800*1.915*1*4*50*15%) -12500, the total amount of tax for the reporting period is 90,640 rubles.

Example #2:

- bar;

- sales area 20 sq. m.;

- Achair;

- this year.

Tax calculation: UTII=1000*1.915*0.7*4*20*15%, total 16,086 rub.

So, the reporting period of time for UTII is considered to be a quarter, so declarations are submitted based on the results of the quarter before the 20th day of the month following the reporting period of time. The declaration form is easy to understand.

Contains the following sections:

- “Title page”, it indicates such official data of the enterprise (IP), such as: TIN, KPP, full name of the director or entrepreneur, full name of the company, legal address, contact phone number, reporting period, code of the tax office where the declaration is submitted;

- The second section, it contains basic information on the physical indicators of your divisions (or a single point), from this section we find out the type of activity of the enterprise (OKVED code), the full actual address of the division, its code based on the All-Russian Classifier (OKTMO), as well as the size basic profitability, coefficients K1 and K2, in essence, physical indicators and tax calculation for one specific address;

- The first section contains summary data of the calculated tax for a separate OKTMO; if this is the only point in this area, the data of the first and second sections will coincide;

- The third section is a summary of information on the entire declaration submitted to this Federal Tax Service (if the business is conducted at only one address, the tax amount in sections 1, 2 and 3 is the same), in this section you show the entire amount of calculated tax, the amount of insurance premiums that reduce tax and the final amount of UTII payable.

- The fourth section (which will need to be completed starting from the first quarter of 2021) is entirely devoted to cash registers. The section includes data on the name of the model, its serial and registration number, the date of registration with the tax authorities, and the cost of the device itself.

Payment of the single tax by the 25th day of the month following the reporting quarter.

General procedure for calculating UTII tax

The general procedure for calculating UTII tax is as follows:

UTII = FP x BD x K1 x K2 x 15%, where

FP – physical indicator;

BD – basic profitability;

K1 – deflator coefficient K1 is set annually. It is intended to adjust the tax on changes in prices for consumer goods, works, services;

K2 – coefficient K2, which takes into account the specifics of doing business, including the range of goods (works, services), seasonality, operating hours, etc.

15% – UTII tax rate, set by the federal authorities

The physical indicator and basic profitability are specified in Article 346.29 of the Tax Code of the Russian Federation. The K1 coefficient was established by Order of the Ministry of Economy dated October 30, 2021 No. 595 and in 2021 is equal to 1.915.

The K2 coefficient is set by regional authorities.