Features of setting wages for employees

When applying for a job, a citizen must be informed about the rules by which remuneration for work is determined. An employment contract is used to consolidate the main provisions not only verbally, but also in writing. The document describes in detail the system used for the employee and the general formation procedure.

The main elements of wages are:

- incentive payments that make up the bonus system;

- allowances;

- salary or tariff rate.

The main thing is to take into account that equal work is paid equally. This means that employees in the same position should receive the same remuneration. Do not forget about the concept of minimum wage - the minimum wage. The salary cannot be lower than this indicator.

Some regions and industries have the right to increase the minimum wage for employees. It is important that any changes are documented in official documents. If there is no documentation, they are guided by the generally accepted minimum wage.

Relationship with wages

How does salary compare to salary?

Salary is not the entire salary, but only a component of it. You need to understand that at the legislative level, the classic wage structure consists of three main elements:

- Basic pay. In fact, this is the official salary due to the employee or the tariff rate calculated for the period of work. The employer has no right to pay its employees below the basic level of remuneration (minus taxes).

- Compensatory pay level. This category includes all payments due to an employee for additional work, atypical working conditions that differ from normal ones, payment for performing one’s duties in difficult climatic and weather conditions, as well as other payments provided for by legislative and local documents.

- Incentive payments. This includes all the “goodies” with which the employer cajoles its employees, encouraging them to conscientiously fulfill and exceed various planned indicators. Usually these are monthly, quarterly, one-time bonuses, various allowances, additional payments, and other rewards.

As a rule, in order to encourage an employee to effectively perform the functional duties assigned to him, employers try to increase the gap between the base salary and the incentive and compensation payments due to the employee.

Typically, this approach is focused on the final result (for example, in the legal field, when a premium is paid for a won case). In such companies, the official salary can be 20–25% of the final salary level.

At the same time, certain categories of workers are initially highly in demand and highly paid. They don’t need to prove anything, chase somewhere, defeat anyone. The main thing is that everything is done systematically.

Such employees include, for example, programmers and IT workers. In their case, the official salary is about 90% of the total salary.

Remember, specific salaries, rates, remuneration systems, and a variety of incentive payments are usually established by the employer through a collective agreement.

About the procedure for paying salaries

When paying rewards, you must go through the following stages:

- The total amount of earnings is calculated based on the rates and salaries that apply to the enterprise.

- Compensation and incentive payments are added.

- Next, deductions are made from wages.

Typically, income tax is used, referred to as personal income tax. The employer acts as a tax agent. The tax is calculated depending on the rate that is currently in effect. Be sure to take into account the deductions due to a particular employee. A reduction is permissible for the required bonuses, for calculation errors made earlier. The same applies to compensation from an employee if he committed any guilty actions.

What salary calculation formula can be used?

The simplest salary calculation formula includes only 3 points:

- salary size;

- number of days worked;

- income tax.

If we assume that the employee does not have to make any payments and no additional payments are made to him, then the salary is calculated as follows:

1. The salary is divided by the number of working days of the month, then multiplied by the number of days worked.

2. Income tax is subtracted from the amount received (in Russia, personal income tax is 13%).

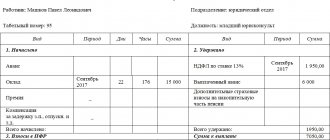

Let's look at an example. The employee's salary is 30,000 rubles. There are 23 working days in a worked month. The employee took 3 days without pay to resolve personal issues, therefore, he worked 20 days in a month. The salary calculation looks like this:

30,000 / 23 × 20 = 26,086.96 rubles (salary before personal income tax);

26,086.96 – 13% = 22,695.65 rubles (take-home salary).

But in practice, such simple calculations almost never happen. Employees are paid bonuses, allowances and compensation. Let’s assume that, in addition to a salary of 30,000 rubles, an employee is paid a bonus of 25% of the salary every month. And he worked only 20 days instead of the required 23 working days per month. Then the calculation will look like this:

Salary + bonus (30,000 + 7,500) = 37,500 rubles (monthly salary);

37,500 / 23 × 20 = 32,608.70 rubles (wages for hours worked excluding personal income tax);

32,608.70 – 13% = 28,369.57 rubles (take-home salary).

Another common case of payments in excess of salary is payment for work on a non-working holiday. A ready-made solution from ConsultantPlus will help you make the calculation correctly. Take advantage of a free trial if you do not yet have access to the system.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

In cases where an employee has the right to a tax deduction, the tax amount is first calculated, and then it is deducted from the salary. For example, the salary is 30,000 rubles. The employee worked all days. He has the right to a tax deduction in the amount of 1,400 rubles. The calculation will look like this:

30,000 – 1,400 = 28,600 × 13% = 3,718 rubles (personal income tax after applying the tax deduction);

30,000 – 3,718 = 26,282 rubles (salary in hand).

Calculating payroll can seem like a daunting task. But once you understand its algorithm, there will be no more problems with the next calculation.

More examples of salary calculations with allowances are in the article

About different forms of remuneration

Wages are calculated depending on the current agreement and the system that works at a particular enterprise. Economic working conditions and personal preferences of the company owner become the main guidelines when making a decision. The main thing is that the system does not contradict the current Labor Code, otherwise it will be automatically declared invalid.

Time-based and piecework are the key systems that are most often used in practice. The time-based option is used if it is not possible to establish a standardized schedule, or there is no need for it. Then it makes more sense to pay not for the amount of work, but for the time.

This type of salary is most often awarded to representatives of the following professions:

- administrative staff;

- secretaries;

- marketers;

- lawyers.

A day or a month can become reporting periods, although management has the right to choose other options. If the time worked is not complete, then remuneration is paid only for the period during which work duties were performed.

The time-based bonus form is also practiced by many enterprises. A bonus is added to the basic remuneration for those who perform quality work.

In production or in the service sector, preference may be given to piecework payment. In this case, it is more profitable for the manager to pay exactly the amount of work that was performed.

About additional payments and bonuses, allowances

Additional payments and salary supplements are also taken into account when wages are checked for compliance with the minimum wage. If an employee has fulfilled all the norms for a month, his remuneration cannot be lower than this indicator.

The salary, according to current standards, may include the following components:

- basic remuneration for work, depending on tariffs or salaries;

- compensation payments;

- incentive transfers.

There are no other special rules in this regard. The same provisions apply to the regional minimum wage and comparison of wages with this indicator.

The essence of the dispute

The employee demanded that the employer increase her salary, which was only 2,596 rubles. The employer refused, stating that, taking into account all the additional payments, her salary exceeded the minimum wage.

Then the employee went to court, demanding that the employer be obliged to pay a salary (tariff rate) in an amount not lower than the minimum wage, and to pay all compensation and incentive payments in excess of the fixed wage.

In support of her demands, the employee referred to the fact that the amount of the official salary cannot be less than the minimum wage on the basis of Part 3 of Article 133 of the Labor Code of the Russian Federation.

When working part-time, part-time

The minimum wage is guaranteed to those who have worked the full standard for a whole month. Therefore, part-time and part-time employees are allowed to pay remuneration less than this parameter. In this case, remuneration may depend either on the total amount of work or on how much time is actually worked.

The full salary is set for those who work part-time. This procedure complies with the provisions of Article 57 of the Labor Code of the Russian Federation. According to this article, contracts and local acts indicate the full amount of salary at fully established standards.

When working part-time, the monthly quota is not generated. Therefore, only part of the salary specified in the agreement drawn up with employees is subject to payment. The corresponding condition is formed in written documents related to employment.

How to correctly collect source data for payroll calculations

To calculate wages based on salary, initial data is collected:

- about the amount of salary;

- number of working days in the billing month;

- number of days worked in a month;

- payments due to an employee in addition to salary.

Where can I get this data from?

Salary size

Salaries for each position are reflected in the staffing table:

In addition, the salary amount must be specified in the employment contract:

And also reflected in the employment order:

See what a sample T-1 order looks like.

Number of working days in the billing month

The working days for each month are calculated based on the production calendar. This indicator depends on the length of the working week: from Monday to Friday (five-day week) or in another mode (for example, with a working Saturday):

Number of days worked in the billing month

This indicator for calculating wages is taken from a time sheet or other document with which the company records days worked, rest days and other periods (business trips, sickness absence, absenteeism, vacations, etc.).

The following materials will help you organize time tracking in your company:

- “Working time sheet according to form T-12 - form”;

- “Notations used in the time sheet”;

- “What is the shelf life of a time sheet?”

Payments due to an employee in addition to salary

Premiums, additional payments, compensations, bonuses and other payments that an employee can count on in addition to salary are established in employment contracts, agreements, orders or other internal regulations (collective agreement, regulations on remuneration, etc.).

The following articles will introduce you to the nuances of assigning various additional payments and compensations to salary:

- “The procedure for paying bonuses under the Labor Code of the Russian Federation”;

- “Regulations on the provision of financial assistance to employees”;

- “Additional payment for combining positions according to the Labor Code of the Russian Federation.”

We will explain below how to calculate salary based on salary.