Normative base

Letter of the Ministry of Labor of Russia dated 08/05/2013 N 14-4-1702

Letter of the Ministry of Labor of Russia dated 08/10/2017 N 14-1/B-725

Resolution of the State Statistics Committee of the Russian Federation dated January 05, 2004 N 1 “On approval of unified forms of primary accounting documentation for recording labor and its payment”

Letter of Rostrud dated March 18, 2010 N 739-6-1

Federal Law of December 6, 2011 N 402-FZ “On Accounting”

Almost always, in vacancies, instead of the salary that the employee will actually receive, the salary is indicated. And many people don’t even realize that salary and wages are not the same thing. And in order not to delve into the rules of how to calculate salary based on salary, the calculator on our website will help.

What kind of salary is there and when is it supposed to be paid?

An employee's salary is calculated using a time sheet.

When calculating salaries, the accountant is guided by the basic documents and regulations of the organization. The list is as follows:

- internal labor regulations,

- collective agreement,

- provisions on material incentives and remuneration,

- staffing table,

- clauses of the employment agreement,

- local regulations.

Remuneration for labor can be piecework or time-based. With a piece-rate system, earnings directly depend on output: the volume of products produced, the number of services provided. In case of time-based earnings, the employee receives a salary corresponding to his position. The salary for each position is established by the staffing table.

The procedure for calculating salaries may provide for bonuses and additional allowances. For example, for length of service, high results of work or its intensity.

Wages must be paid to the employee at least twice a month. This employer’s obligation is enshrined in Article 136 of the Labor Code of the Russian Federation. Violation of the article entails administrative liability.

There are two established methods of paying salaries 2 times a month:

Advance and payment at the end of the month. In the first half of the month, an advance is issued - part of the official salary. This part is fixed in the monthly tariff schedule. To receive an advance, you need to work for at least two weeks. At the end of the month, the employee receives the remainder. It can be fixed or depend on the hours worked or the amount of work done.

Payment for the 1st and 2nd half of the month. Salaries are calculated twice a month - in the 1st and 2nd halves of the month. The calculation is made based on the actual time worked or the amount of work, in two-week increments. An employee works for two weeks and receives payment the next day of the week. Typically, this payment procedure is established in a collective or employment agreement.

How to use the calculator

To calculate your salary using our service, enter the initial data. The program will do the rest.

Let's say your salary is 30,000 rubles. For a fully worked September, you will be credited 30,000 rubles, but personal income tax will be withdrawn in the amount of 3,900 rubles and only 26,100 rubles will be issued (transferred to the card).

Try calculating your salary based on your salary; the calculator will give you the answer instantly. The only thing is that he does not know how to count overtime, and if the hours are exceeded, the program will not work. But if you worked for less than a full month, let’s say you were hired in the middle of the month, the system will take into account the number of days worked and change the totals.

Nuances and exceptions in calculating the average employee salary

It must be emphasized that to calculate the average daily wage, time and payment for this period are not taken into account if the employee:

- was absent from work, used days (while maintaining salary);

- received benefits from the Social Insurance Fund (sick leave, pregnancy, childbirth, care);

The indicated periods are not taken into account, based on the logical conclusion - they have already been paid with the preservation of the average daily earnings.

If an employee, for example, was on maternity leave, then the average salary is calculated based on the amounts of payments accrued in the period before maternity leave.

Let's consider an example when in one month of the year, an employee was absent for some other reason, at his main workplace, while maintaining his average earnings or receiving benefits. Example of salary calculation (average daily):

Chief Economist, N.P. Kalinina worked in 2015 - 11 months completely, 1 month (November) was absent due to important negotiations and preparation for them. During the negotiations, N.P. Kalinina’s average earnings at her main place of work remained unchanged. The number of days actually worked in November at the main place is 2 days.

The employee's wage fund consists of:

salary – 50,000 rubles;

additional payment (for high qualifications of the employee) – 25% of the salary.

In January 2021, Kalinina N.P. vacation, as scheduled.

The calculation scheme is as follows:

— we determine the amount of payments for the period 2015, they include salary, additional payment for full months and for partial November:

Zaccrued = basic salary for 11 months. + additional salary for 11 months + basic and additional salary in 2 days of November

Z = (50,000*11) + (50,000*25%*11) + (50,000/159*2*8 + (50,000/159*2*8)*25%) =550000 + 137500 + (5031 .56+1257.86) = 693789.42 (rubles).

— we determine the time, for this we multiply the number of fully worked months (11 months) by 29.3, to this number we add 2 days worked in the twelfth month:

11*29.3+2 = 324.3 (days).

— we determine the average daily salary, to do this we divide the amount of payments by the amount of days:

Z average = 693789.42 / 324.3 = 2139.34 (rubles).

Next, to calculate vacation pay for Kalinina N.P., the accountant will only have to accrue Z average for each day of vacation.

In Kalinina’s example, the additional salary fund is represented by an additional payment for highly qualified work. In the calculation of the average salary, instead of (or together with) additional payments for high qualifications, any additional payments and allowances, bonuses and other payments for this period can be included (according to the same scheme).

Also, during the billing period (year), temporary additional payments and allowances may be accrued or withdrawn (by order), they must also be taken into account in the calculation.

For example, if Kalinina N.P. assigned (by order) an additional payment for part-time work (during the absence, in January 2015, of the head of the personnel department), in the amount of 20% of the official salary (of the chief economist), then the calculation of its average daily salary would change its appearance as follows:

Z = salary basic 11 months. + salary additional 11 months + salary basic and additional. November + salary additional combined January

Z = 550,000 + 137500 + (5031.56+1257.86) + (50,000*20%)=550000 + 137500 + (5031.56+1257.86) + 10,000 = 793789.42 (rubles).

Z average = 793789.42 / 324.3 = 2447.70 (rubles).

Features of manual payroll calculation

Labor legislation defines salary and wages (Article 129 of the Labor Code of the Russian Federation):

- salary - a fixed amount of remuneration for an employee for a calendar month without taking into account compensation, incentives and social payments;

- incentive payments - additional payments and bonuses of an incentive nature (bonuses and incentive payments);

- compensation payments - additional payments and allowances of a compensatory nature (for work in special climatic conditions or in special conditions and other payments);

- wages - remuneration for work, which consists of salary, taking into account compensation and incentive payments. In colloquial speech the concept of “dirty salary”, or gross salary is used;

- take-home salary - the amount of wages to be paid to the employee, or accrued wages minus personal income tax. In colloquial speech it is sometimes referred to as “net pay” or salary net, and a detailed calculation of wages by salary calculator has just helped us do it.

Pay systems

The organization independently develops a system of financial motivation for employees. Different payment systems are established for different categories of employees. The main remuneration systems are:

- official salary;

- tariff rate.

The amount of salary payments depends on the position held. This system is used to reward specialists with a wide range of work. Directors, lawyers, engineers, accountants and other specialists who calculate salaries based on salaries will need a calculator every time they index payments.

Remuneration at the tariff rate is established as the amount of remuneration for fulfilling the norm. This method is used mainly for temporary workers and piece workers (turner, builder, combine operator, etc.).

Deadlines for calculation and payment of wages

The payment date is set in one of the following documents: internal labor regulations, collective agreement or employment contract. Wages are paid at least every half month (Article 136 of the Labor Code of the Russian Federation). The final payment for the month is made no later than the 15th.

In practice, the payment period is set without taking into account how to calculate salary based on salary (calculator), but in the following order:

- advance payment - from the 16th to the 30th (31st) day of the current month;

- final payment for the month is from the 1st to the 15th of the next month.

If the payment day coincides with a weekend or non-working holiday, payment is made on the eve of this day (Article 136 of the Labor Code of the Russian Federation).

IMPORTANT!

In the Letter of the Ministry of Labor of Russia dated 08/05/2013 No. 14-4-1702, when considering the issue of determining the amount of the advance, it was explained that the Labor Code of the Russian Federation does not regulate the size of the advance. In Letter No. 14-1/B-725 dated August 10, 2017, the department reminded that it is unacceptable to reduce the salary advance compared to money actually earned.

In practice, the following methods of calculating the advance are used:

- in proportion to the time worked;

- as a percentage of salary;

- in a fixed amount.

The organization chooses the most convenient payment methods and terms for itself.

How to calculate how much they will give in your hands

The actual amount to be paid is determined using salary calculation, the formula of which is as follows:

ZP = O / Dm × Od,

Where:

- ZP - monthly salary (gross);

- О - official salary according to the staffing table or employment contract;

- Dm - number of days in a month;

- Od - actually worked days in a month.

When the amount of wages is known, we determine the amount of personal income tax:

Personal income tax = salary × 13%,

Where:

- ZP - accrued wages for the month;

- 13% is the personal income tax rate for individuals who are tax residents of the Russian Federation (clause 1 of Article 224 of the Tax Code of the Russian Federation).

Let's determine the amount of wages “on hand” (Net).

Net = salary - personal income tax,

Where:

Net - the amount of wages that will be paid to the employee for the month worked.

Number of working days

The proposed algorithm for calculating salary based on salary is suitable if the employee worked for a whole month, without absences or business trips. Working hours (standard) should not exceed 40 hours per week (Article 91 of the Labor Code of the Russian Federation).

The number of days worked in a month is determined by the working time sheet.

In the case of working for less than a full month, wages and salaries are calculated differently. For example: hiring or dismissal in the middle of the month. Payment is made based on the days actually worked in the month.

Average earnings

When on a business trip, during layoffs and in other cases provided for in Art. 139 of the Labor Code of the Russian Federation, payment is based on average earnings.

The calculation of average wages is determined by the formula:

SZP = (ZP + SV) / D,

Where:

- SWP - average salary;

- Salary - actual accrued salary for the 12 months preceding the date of payment;

- SV - accrued incentive payments provided for by the remuneration system for the period, with the exception of amounts of financial assistance;

- D - the number of days actually worked in the 12 months preceding the date of payment.

IMPORTANT!

One average earnings is not included in another, i.e., when calculating average earnings, the time during which the employee maintained the average earnings is excluded from the calculation period, in accordance with the legislation of the Russian Federation.

Salary remuneration: features

The most common and simple payment for labor is salary. With this system, the main indicator of successful work is compliance with the workday schedule: working out the planned number of working days (hours) in the billing period (month) guarantees receipt of the full salary determined by the employment contract.

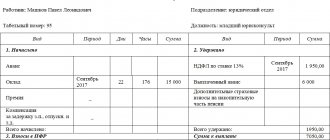

Official salary is a fixed amount of remuneration for the performance of official duties in a calendar month. At the same time, you need to understand that the salary is not the amount “on hand” (received after withholding personal income tax), but the amount accrued for work in a particular month (before deducting personal income tax and other deductions at the request of the employee).

Documents reflecting the calculation, accrual and payment of wages

When hiring an employee, a hiring order is issued. The order is issued in any form or using forms No. T-1 or T-1a.

The employee's salary is indicated in the employment contract and/or staffing table (form No. T-3).

To calculate wages and record actual time worked, the following forms are used:

- timesheet for recording working hours and calculating wages (form No. T-12);

- time sheet (form No. T-13).

To fill out timesheets, HR employees use a production calendar.

The following forms are used to document payroll calculations:

- payroll statement, form T-49;

- pay slip, form T-51;

- payroll, form T-53.

Accounting and registration of payrolls for payments made to employees of the organization is reflected in the payroll register (Form No. T-53a).

All these forms are approved by Resolution of the State Statistics Committee dated January 5, 2004 No. 1 “On approval of unified forms of primary accounting documentation for recording labor and its payment.”

When paying wages, the employer is obliged to notify each employee in writing about the amount of wages (Article 136 of the Labor Code of the Russian Federation and Letter No. 739-6-1 of March 18, 2010).

The approved unified forms do not contain a payslip form. The organization has the right to independently develop the form.

When an employee is dismissed, an order is issued to terminate the employment contract with the employee. The order is issued in any form or the unified form No. T-8 is used.

The employee must be familiarized with all orders in writing.

The organization has the right to independently develop forms and forms reflecting the calculation, accrual and payment of wages. The developed forms are approved as part of the accounting policy (Article 9 of Law No. 402-FZ of December 6, 2011).

Payroll statement (form T-49)

Payroll (form T-51)

Payroll (form T-53)

Payroll register (form No. T-53a)

Order on approval of the pay slip and the procedure for issuing it to the employee

Calculation of the average monthly salary of an employee in 2017

Basic payroll operations, for which you will need to calculate the average monthly salary of an employee, in the current mode:

- calculation of vacation payments, as well as payments of unused vacation in case of dismissal;

- calculation of payments, maintaining the average monthly salary at the main place of work;

- calculation of wages during technological (and other types of) downtime, due to the fault of the employer, or natural disasters and other force majeure;

- calculation of severance (and other types) benefits for termination of an employment contract, staff reduction, etc.;

- for calculating disability benefits (in accordance with sick leave);

- to calculate payments for working hours on business trips;

- provision of information on the average monthly salary and other data (contracts, orders), at the request of the employee, in person;

- others.

Salary for January 2021

Despite the fact that January is a short month in terms of working hours, wages for January are accrued and paid in full (of course, if the employee has worked all working days). Reducing wages for January due to low working hours is a violation of the law.

Calculate wages for the first half of the month based on the number of days worked in the period from January 1 to January 15. Do not withhold personal income tax from the advance payment for January.

Example

The company has a 5-day work week. The official salary of accountant A. S. Komarova is 60 thousand rubles. The advance for the first half of January will be equal to: 20 thousand rubles. (60 thousand rubles / 15 working days * 5 days worked).

The cost of a working day in January is the highest of the year. Absence from work for an employee will have a significant impact on his income.