When can you issue an invoice in foreign currency?

According to paragraph 7 of Art.

169 of the Tax Code of the Russian Federation, an invoice in foreign currency can be drawn up if the terms of the transaction in the contract are expressed in foreign currency. At the same time, in parallel with this norm of the Tax Code, there is another one in the legislation: sub-clause. "m" clause 1 section. Resolution II of the Government of the Russian Federation “On filling out documents for VAT calculations” dated December 26, 2011 No. 1137 states that if the obligation under the contract is fixed in currency equivalent, but the payment currency is rubles, the invoice should be issued in rubles. Thus, ambiguity arises when applying these rules to transactions between residents of the Russian Federation:

- on the one hand, it seems that it is possible to issue an invoice in foreign currency if the obligation is expressed in foreign currency (conventional units);

- on the other hand, this violates the procedure for issuing invoices according to the rules established for residents of the Russian Federation, which are necessary for their acceptance in tax accounting for VAT.

This point is actively used by tax authorities who check the legality of deducting VAT. The tax accepted for deduction on an invoice issued in foreign currency is not confirmed and an understatement of VAT is registered with all the ensuing consequences. From time to time, the Federal Tax Service reinforces its position with its own explanatory letters. For example, one of the latest - letter No. ED-4-3/12813 dated July 21, 2015 - once again refers to the procedure for issuing VAT documents, approved by Resolution No. 1137 (in rubles), as the only correct one.

NOTE! Buyers have problems with deductions for foreign currency invoices. Tax authorities usually do not try to apply any sanctions to the seller who issued documents in foreign currency. Exceptions occur only in cases where the seller, reflecting data in tax registers, incorrectly recalculated the amount of revenue in rubles on such invoices and thereby underestimated the VAT base.

Purchase of goods under contracts in monetary units: legislation

Accounting and tax accounting

Transactions in foreign currency between Russian organizations are prohibited and are carried out only in Russian rubles (Article 9 of the Federal Law of December 10, 2003 N 173-FZ).

In this case, the price in the contract can be expressed in any currency or conventional units (cu), other than rubles (clause 2 of Article 317 of the Civil Code of the Russian Federation).

Payment under such agreements should be made only in rubles at the rate agreed upon by the parties. As a rule, the agreed rate is equal to the rate of the Central Bank of the Russian Federation established on the day of payment. But often contracts may establish a different rate corresponding to the rate of the Central Bank of the Russian Federation plus 2%, minus 0.5%, etc.

Primary documents under such agreements can be presented in rubles, foreign currency or conventional units.

In such cases, invoices (UPD) are issued only in rubles.

The value of assets (including goods), expressed in monetary units, is subject to conversion into rubles in the accounting system (clause 4 of PBU 3/2006, clause 10 of Article 272 of the Tax Code of the Russian Federation).

What exchange rate should I use to convert the cost of goods into rubles?

The conversion rate depends on how payment for the purchased goods was made.

Option #1. 100% prepayment according to the contract

Goods for which payment was made in the form of 100% prepayment are recognized in the accounting system in ruble valuation at the rate in effect on the date of prepayment (paragraph 2, paragraph 9 of PBU 3/2006, paragraph 10 of Article 272 of the Tax Code of the Russian Federation).

Option #2. 100% post-payment according to the agreement

Goods for which payment is made after they are registered are recognized in ruble valuation at the rate in effect on the date of transfer of ownership (clause 5 of PBU 3/2006, clause 10 of Article 272 of the Tax Code of the Russian Federation).

Option #3. Partial prepayment and postpayment according to the agreement

With a mixed form of payment in the form of partial prepayment and postpayment, goods are invoiced at the total cost:

- the paid part is assessed according to the date of prepayment (paragraph 2, clause 9 of PBU 3/2006);

- the unpaid portion is assessed at the exchange rate on the date the goods were accepted for accounting (clause 5 of PBU 3/2006).

No further recalculation of the cost of goods accepted for accounting under contracts in monetary units is carried out. There is also no recalculation of the amount of advances issued to suppliers (clause 10 of PBU 3/2006).

At the same time, revaluation of accounts payable to suppliers under contracts in monetary units. must be carried out on the earliest date (clause 7 of PBU 3/2006, clause 8 of Article 271 of the Tax Code of the Russian Federation):

- date of repayment of obligations;

- last day of the month.

In this case, exchange rate differences will arise, which are taken into account in account 91 “Other income and expenses”:

- in accounting - as other income or expenses (clause 13 of PBU 3/2006);

- in tax accounting - as non-operating income and expenses (clause 11 of article 250 of the Tax Code of the Russian Federation and clause 5 of clause 1 of article 265 of the Tax Code of the Russian Federation).

Find out more about Exchange Differences .

VAT

The tax base for VAT is determined as of the earliest date (clause 1 of Article 167 of the Tax Code of the Russian Federation):

- day of shipment;

- payment day.

If the initial moment of determining the tax base under the agreement in c.u. is the day of shipment, it should be determined based on the exchange rate of the Central Bank of the Russian Federation on the day of shipment.

In accounting and tax accounting, the ruble valuation of assets is determined at the exchange rate of the Central Bank of the Russian Federation on the day of transfer of ownership. Therefore, if the date of shipment and the date of transfer of ownership do not coincide, a difference will arise between the estimated value in accounting/tax accounting and the tax base for VAT.

When subsequently paying for goods, VAT deductions are not adjusted. Differences in the amount of tax as a result of postpayment from the buyer are taken into account as part of non-operating income or expenses (paragraph 5, paragraph 1, article 172 of the Tax Code of the Russian Federation).

When purchasing goods, VAT is deductible (clause 2 of Article 171 of the Tax Code of the Russian Federation) if the following conditions are met:

- the goods must be used in activities subject to VAT;

- a correctly executed SF (UPD) is available;

- goods are accepted for registration (clause 1 of article 172 of the Tax Code of the Russian Federation).

In what amount are we entitled to deduct VAT under the contract in cu?

The buyer has the right to deduct the amount of VAT indicated on the invoice. But you need to be careful and check the amounts of VAT in the Federation Council indicated by the supplier.

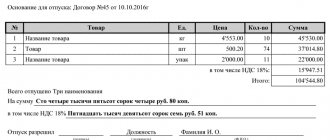

Invoices (UPD) for contracts in cu. are billed only in rubles. The ruble amount in the invoice for shipment depends on the payment procedure under the contract in cu.

Option #1. 100% prepayment according to the contract

The supplier is obliged to issue the shipping SF in ruble valuation at the rate of the Central Bank of the Russian Federation in effect on the date of prepayment (clause 14 of Article 167 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated December 23, 2015 N 03-07-11/75467).

If an advance invoice was previously received from the supplier, then according to this invoice we also have the right to deduct VAT. But at the time of receipt of goods, VAT on the advance SF must be restored.

Read more about Accepting VAT for deduction on advances issued to suppliers, as well as about Restoring VAT when offsetting an advance

Option #2. 100% post-payment according to the agreement

The supplier is obliged to set the shipping invoice in rubles at the rate of the Central Bank of the Russian Federation in effect on the date of shipment (clause 4 of article 153 of the Tax Code of the Russian Federation).

Option #3. Partial prepayment and postpayment according to the agreement

The supplier is obliged to set the shipping invoice in rubles at a cost consisting of:

- the paid part, assessed at the exchange rate on the date of prepayment (clause 14 of article 167 of the Tax Code of the Russian Federation);

- the unpaid portion, assessed at the exchange rate on the date of shipment (clause 4 of Article 153 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated December 23, 2015 N 03-07-11/75467).

If an advance invoice for partial prepayment was previously received from the supplier, then according to this SF VAT we also have the right to deduct. But at the time of receipt of goods, VAT on the advance SF must be restored.

Who should issue an invoice in foreign currency?

If you look at the lawsuits in which VAT on foreign currency invoices was ultimately accepted for deduction, you can note that the peak occurred in 2011–2013. Then, by 2016–2017, the consideration of such cases practically disappeared.

Most likely, this is due to the fact that residents simply stopped filing VAT documents in foreign currency under agreements under which they are calculated in rubles.

Thus, the answer to the question “In general, is it possible for a resident of the Russian Federation to issue an invoice in foreign currency to a counterparty resident of the Russian Federation?” like this: theoretically possible, but not necessary. Unless, of course, the goal is to make it difficult for the resident partner to deduct VAT on such documents.

To whom exactly can VAT documents be issued in foreign currency?

1. To a counterparty (including a resident), with whom settlements are also carried out in foreign currency. This option is limited by the currency legislation of the Russian Federation. The list of transactions between residents of the Russian Federation that qualify for this option is listed in clause 1 of Art. 9 of the Law “On Currency Regulation” dated December 10, 2003 No. 173-FZ.

2. To yourself. For export transactions (for which the rate is 0%), the resident exporter is not exempt from the obligation to keep VAT records. The exporter must issue an invoice (with zero VAT) and register it in the sales ledger.

Opening a foreign currency account

To receive foreign currency, you will need a foreign currency account.

To open it, you need to prepare a package of documents almost the same as when opening a regular current account. Each bank has its own requirements for the required set of documents, so check this information in advance. If you open a foreign currency account in the same bank where you already have a ruble account, the procedure will be much simpler. Along with a foreign currency account, the bank will open a transit account for you - a kind of transfer point for funds. It is needed so that receipts pass exchange control. While the money is in the transit account, you will not be able to use it. Once the legitimacy of your transactions is confirmed, you can withdraw funds to a foreign exchange account or immediately sell the currency. Otherwise, the amount of money will be returned back to your client.

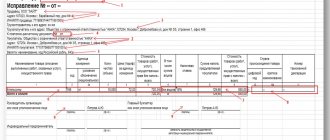

How to issue a foreign currency invoice in 2020-2021

Let's consider the nuances of drawing up a foreign currency invoice from the seller:

- line 7 - enter the name and currency code of the account (according to OKV - the All-Russian Classifier of Currencies);

- then the “standard” lines of the document are filled in in the specified currency.

As you can see, it is not so difficult for the seller to issue an invoice. Questions usually arise at the stage of deciding whether the document will be in foreign currency or in rubles.

IMPORTANT! You can enter additional information into the currency invoice. This is allowed to be done between line 7 and the rest of the tabular part to be filled in, as well as in the tabular part itself, provided that the form of the invoice is preserved and the sequence of filling out its columns is not disrupted. This rule is enshrined in Federal Tax Service letter No. SD-4-3/ [email protected] and is especially relevant for those who work with counterparties in the EAEU. This letter was issued before additional line 8 “Government contract identifier (if any)” was introduced into the invoice form, therefore we believe that additional information must be indicated without violating the structure of the invoice between line 8 and the tabular part.

Let us remind you that from July 1, 2016, it is mandatory to indicate the product code in invoices to a counterparty in the EAEU in accordance with the unified product nomenclature of the EAEU. The product code is indicated in column 1a “Product type code” of the tabular part of the invoice, applicable from 10/01/2017. Until October 2021, the code of the type of goods when exported to the EAEU was indicated in the invoice in a self-entered column.

For more details, see: “Export to the EAEU: where to indicate the code of non-taxable goods in the invoice?” .

ConsultantPlus experts explained which codes to indicate on the invoice. To avoid mistakes, get trial access to the system and go to the Ready-made solution.

An invoice for payment

An invoice is a document in which the seller sets the price for his services or goods.

The buyer agrees to the supplier's terms and conditions at the time of payment. The legislator does not establish the form of the invoice, so each company draws it up in its own way. The invoice specifies the terms of the transaction, terms, payment and delivery procedures, etc.

The signature of the director or chief accountant on this document is not required (Article 9 No. 402-FZ). But to avoid any questions from the tax authorities or counterparties, it is better not to neglect them. An invoice for payment does not provide an opportunity to present demands to the supplier - it only records the purchase price. The buyer retains the right to demand a refund in case of violation of the terms of the contract or illegal enrichment of the supplier.

How to generate invoices in foreign currency in 1C

First of all, it is necessary that the “Currencies” directory be filled out in “1C”. You can select the desired currency or add it manually.

NOTE! If the terms of the agreement provide for a “special” conversion into rubles (a currency clause has been made), for example, “payment at the rate of 1 euro plus 3%,” then you can enter the following new position into the directory:

- create a “new currency”;

- link to the euro exchange rate (check the box in the form that opens);

- set the required “surcharge”;

- save with a name that will allow you to quickly find the position if necessary.

Read about the nuances of currency clauses in the article “Sample of a currency clause in a contract and its types .

Then you need to correctly enter information about the contract into the database. In the “Calculations” section of the contract being drawn up, you need to select the desired currency from the directory. Save changes.

When entering a document (for example, a sale) under an agreement, the required currency will be automatically selected and converted into rubles at a given rate for accounting purposes.

The easiest way to issue an invoice is through the “Create based on” option, which is available in all accounts receivable documents. The invoice created on the basis of the source document (sale or payment) will automatically take into account all the nuances of the reflected transaction, including the currency of the contract.

Primary documents are divided by business stage

All transactions of the company can be divided into three stages:

The first stage is an agreement on the terms of the transaction . The result will be an agreement and an invoice for payment.

The second stage is payment for the transaction . Primary documents confirming payment:

- Cash payments - cash receipt, receipt for cash receipt order, strict reporting form. Organizations rarely pay each other in cash, since the amount of payments through the cash register is limited to 100 thousand rubles. Employees usually receive advances or accountable money in cash.

- Electronic payments, including acquiring, payment systems or transfers from a current account - bank account statement.

The third stage is receiving products . Confirmation is required that the buyer has received the product or service, and the seller has received payment. Without supporting documents, the tax office will not allow you to include the funds spent in expenses. Receipt is confirmed:

- waybill;

- sales receipt;

- act of work performed or services rendered.

What is an invoice?

An invoice, sometimes called an invoice, is a document sent by the supplier of a product or service to the buyer. An invoice establishes an obligation on the part of the buyer to pay for a product or service, creating a receivable. In short, an invoice is a written confirmation of the agreement between the buyer and seller.

An orderly invoice speeds up the payment process. When a customer looks at an invoice, they should understand exactly what is being charged, the amount, and when it is due.