Invoice under simplified tax system

All organizations and individual entrepreneurs using the simplified tax system are not VAT payers, which means they do not need to issue an invoice. However, if certain situations arise, such a document will be needed.

These include situations where “simplified” people pay VAT: (click to expand)

- Import of goods;

- Operations under a simple partnership agreement, or trust management of property and concession agreement;

- When a company performs the duties of a tax agent, for example, rents state or municipal property.

In all of the above situations, organizations are required to issue an invoice (

Invoice of an intermediary under the simplified tax system: an exceptional case

And yet, in some cases, buyers can safely claim a VAT deduction based on an invoice received from a “simplified” company. This applies to situations where the “special regime agent” is an intermediary (commission agent, agent) selling goods on his own behalf. Then the intermediary under the simplified tax system draws up an invoice based on legal norms, and the buyer should not have problems applying the deduction. This conclusion was made by the Ministry of Finance in a letter dated June 25, 2014 No. 03-07-RZ/30534.

This also applies to “simplers” who are participants in a simple partnership agreement or a trustee, since, due to the requirements of the Tax Code, they are required to issue an invoice (clause 2 of article 174.1, clause 2 of article 346.11 and clause 2.1 of art. 346.26 Tax Code of the Russian Federation).

Invoice with o

You are not required to issue an invoice from the company using the simplified tax system. Only companies exempt from VAT put this mark. Organizations that are considered exempt from VAT are recognized in accordance with Article 145 of the Tax Code of the Russian Federation.

Companies that apply the simplified tax system do not qualify as such “exempt” payers, since they are not initially payers of this tax. Accordingly, there is no need to issue a “simplified” invoice marked “without VAT”.

Some counterparties still insist on an invoice. Such companies should keep in mind that they will not receive a deduction for “input” VAT on such an invoice. And why they continue to demand such invoices is not clear.

“Simplers” are not obliged to fulfill such a request. They have the right to explain to their counterparties that in order to post the purchased goods, documents such as an invoice for payment, an invoice and a statement will be sufficient. And if the counterparty continues to insist and it is impossible to convince him, then you can issue the required document. Please indicate that the purchase does not include VAT.

Such registration of an invoice will not entail obligations to pay tax, as well as the preparation and submission of a VAT return, since the tax will not be highlighted in the invoice (

If the counterparty asks to issue an invoice

Why do special regime officers issue invoices with the allocated amount of VAT? The most common reason is the request of the counterparty. The Tax Code does not prohibit this. That is, any entity using the simplified tax system has the right to decide independently whether to issue an invoice with VAT included. However, not every “simplified” person knows that by meeting his customers halfway, he assumes the responsibility of paying this tax.

Meanwhile, the law directly establishes the consequences of such a decision. Subclause 1 of clause 5 of Article 173 of the Tax Code of the Russian Federation states that if a person who is not a VAT payer issues an invoice to the buyer with the allocated amount of tax, he is obliged to pay it to the budget. This is confirmed by clarifications from the Ministry of Finance, for example, letter No. 03-07-14/7897 dated 02/09/2018.

What happens if the simplified taxation system payer ignores this requirement? The Federal Tax Service itself will contact him through a desk audit of his counterparty’s VAT declaration. And then you will have to pay not only VAT, but also fines and penalties. Judicial practice suggests that it will not be possible to challenge these additional charges.

Zero VAT on the invoice

Organizations using the simplified tax system should also not put a real VAT rate of 0% in the invoice. Only companies that are VAT payers can apply this rate. In addition, it must be confirmed by specific documents that organizations submit along with the VAT return to the tax office.

If an accountant decides to meet the buyer halfway and issue a document with zero VAT, the tax authorities have the right to charge it, not at a zero rate, but at a rate of 18%. This will happen because VAT is indicated in the invoice, and it is impossible to confirm that the company’s rate is zero.

Is it possible to issue an invoice without VAT?

In some cases, VAT payers issue invoices without tax. For example, if they received an exemption under Article 145 of the Tax Code of the Russian Federation . In such invoices the entry “Excluding tax (VAT)” is made. Such a document does not entail the obligation to pay tax.

Does the payer of the simplified tax system have the right to issue an invoice without VAT? Judicial practice suggests that this will not help him. For example, this is indicated in the resolution of the Supreme Court of the Supreme Soviet of April 12, 2018 No. F02-1385/2018 in case No. A19-13739/2017. The bottom line is that the benefits provided for in Article 145 of the Tax Code of the Russian Federation do not apply to “simplified workers” . As well as other benefits for VAT payers.

Conclusions. There is no point in issuing invoices for a company or individual entrepreneur using the simplified tax system. If this is done, it is usually in order to please a large counterparty. But the benefits from such cooperation seem doubtful. After all, the tax invoiced must be paid to the budget. And at the end of the quarter, submit a VAT return to the Federal Tax Service in electronic form. Failure to fulfill the taxpayer's obligations will entail not only additional tax payment, but also penalties.

If you issue an invoice with VAT

Some organizations, on their own initiative, may issue invoices, highlighting VAT. In this case, they are required to pay tax to the budget and also submit a VAT return to the Federal Tax Service. This must be done before the 25th day of the month following the quarter in which the document was issued. For example, a company issued an invoice using the simplified tax system on February 10, 2021; accordingly, it must submit a VAT return by April 25, 2021.

It is important to understand that issuing an invoice with allocated VAT does not give the simplifier the right to a tax deduction on purchased goods. Only VAT payers have the right to such a deduction, and organizations using the simplified tax system are not such.

Does the simplifier need to issue invoices?

The Tax Code of the Russian Federation provides for the exemption of “simplified” companies from paying VAT, but this right does not apply to all transactions. Therefore, the need to draw up an invoice under the simplified tax system depends on the following circumstances:

- whether the simplifier allocated VAT;

- what operations were performed by the payer on the simplified tax system.

At the same time, the simplifier can issue an invoice without VAT.

What else can be used instead of such invoices is discussed in the article “VAT under the simplified tax system: in what cases should I pay and how to take into account the tax in 2021 - 2020?” .

Answers to common questions

Question: A simplified company, at the request of the buyer, issued an invoice, highlighting VAT. After that, in accordance with the requirements of the law, I paid this tax to the budget and filed a VAT return. When calculating the simplified tax system, will VAT be included in the tax base? (click to expand)

Answer: The tax base for simplifiers is income, which must first of all be economically profitable. Paid VAT is not a benefit for the company, and therefore should not be included in the base for calculating the simplified tax system. Accordingly, when calculating the tax, the simplified tax system does not need to be included in the VAT base.

The taxpayer issues an invoice using the simplified tax system

A taxpayer applying the simplified taxation system (hereinafter referred to as the simplified taxation system) is not a payer of value added tax on the basis of clause 2 of Art. 346.11 Tax Code of the Russian Federation. Accordingly, the taxpayer does not need :

— when selling goods (works, services), in addition to the price (tariff), present the amount of VAT for payment to buyers in accordance with clause 1 of Art. 168 Tax Code of the Russian Federation;

— issue invoices to buyers (clause 3 of Article 169 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated July 24, 2008 No. 3-1-11/239).

However, in cases where the counterparty agrees to work with an organization using the simplified tax system only if it receives invoices from it with the allocated amount of VAT, then the taxpayer using the simplified tax system has the right to issue such an invoice to the buyer. In this case, the taxpayer using the simplified tax system is obliged to pay to the budget the amount of tax indicated in this invoice (clause 5 of article 173 of the Tax Code of the Russian Federation). Tax payment is made at the end of each tax period based on the corresponding sales of goods (work, services) for the expired tax period no later than the 20th day of the month following the expired tax period (clause 4 of Article 174 of the Tax Code of the Russian Federation). The tax period for VAT is a quarter (Article 163 of the Tax Code of the Russian Federation).

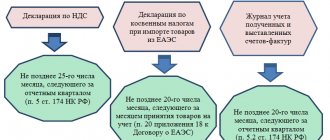

In addition, the taxpayer using the simplified tax system who issued the invoice is obliged to submit a tax return to the tax authority at the place of his registration no later than the 20th day of the month following the expired tax period (Clause 5 of Article 174 of the Tax Code of the Russian Federation). The tax return form and the procedure for filling it out were approved by order of the Ministry of Finance of the Russian Federation dated October 15, 2009 No. 104n. According to clause 3 of this Procedure, when issuing an invoice to the buyer with the allocation of the amount of VAT by organizations using the simplified tax system, such organizations submit a tax return as part of the title page and section 1 of the declaration. The remaining sections of the declaration do not need to be completed or submitted. In this case, in section 1 you only need to fill in lines 010 (OKATO code), 020 (KBK) and 030 (tax amount indicated in invoices issued during the tax period).

If a taxpayer using the simplified tax system has issued an invoice to the buyer with a allocated amount of VAT, then such an invoice is subject to registration in Part 1 of the Logbook of received and issued invoices. The invoice is recorded by the date of issue (that is, the date indicated on the invoice) in Part 1 of the Journal and in the Sales Book. The forms of the Journal of accounting of received and issued invoices and the Sales Book are approved by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

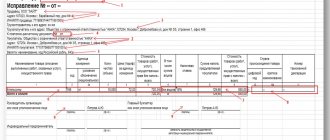

For example, a taxpayer shipped goods worth 500,000 rubles in the 2nd quarter. Of these, goods were shipped with the presentation of invoices in the amount of 118,000 rubles, including VAT of 18,000 rubles. The taxpayer must:

a) register invoices in the Accounting Journal and Sales Book during the quarter according to the date of issue;

b) submit a VAT return for the 2nd quarter no later than July 20. In the tax return on line 030 of section 1, you must indicate the amount of 18,000 rubles;

c) pay a tax of 18,000 rubles to the budget no later than July 20.

Note!

1. In accordance with paragraph 1 of Art. 167 of the Tax Code of the Russian Federation, the moment of determining the tax base for VAT is the day of shipment (transfer) of goods (work, services), property rights. In this regard, the taxpayer under the simplified tax system has an obligation to calculate and pay tax in the tax period (quarter) in which he issued an invoice to the buyer, regardless of the receipt or non-receipt of payment from the buyer for the shipped goods (work, services).

2. A taxpayer using the simplified tax system who has issued an invoice with an allocated VAT amount does not have the right to tax deductions for purchased goods (works, services), since only VAT taxpayers who are such in accordance with the norms of tax legislation have the right to tax deductions. The payer of the simplified tax system is not a taxpayer of value added tax due to clause 2 of Art. 346.11 Tax Code of the Russian Federation. The VAT amounts presented by sellers of goods (work, services), the taxpayer on the simplified tax system includes the cost of purchased goods (work, services) on the basis of paragraphs. 3 p. 2 art. 170 Tax Code of the Russian Federation.

In the situation described above, another question arises: when issuing invoices, is it necessary to take into account the amount of VAT payable to the budget as part of income on the simplified tax system?

According to paragraph 1 of Art. 346.15 of the Tax Code of the Russian Federation, taxpayers using the simplified tax system when determining the object of taxation take into account the following income:

- income from sales, determined in accordance with Art. 249 Tax Code of the Russian Federation;

- non-operating income determined in accordance with Art. 250 Tax Code of the Russian Federation.

According to Art. 249 of the Tax Code of the Russian Federation, income from sales is recognized as proceeds from the sale of goods (work, services), property rights, which is determined on the basis of all receipts associated with payments for sold goods (work, services) or property rights. At the same time, the general procedure for determining income referred to in Art. Art. 249 and 250 of the Tax Code of the Russian Federation, established by Article 248 of the Tax Code of the Russian Federation. According to paragraph 1 of Art. 248 of the Tax Code of the Russian Federation, when determining income for tax purposes, the amounts of taxes presented in accordance with the Tax Code by the taxpayer to the buyer (acquirer) of goods (work, services, property rights) are excluded from them.

Based on the foregoing, we can conclude that a taxpayer using the simplified tax system has the right not to include in income VAT amounts received from buyers and subject to payment to the budget. VAT, subject to payment to the budget on the basis of a VAT tax return, by its economic essence is not the taxpayer’s income under the simplified tax system and is not subject to inclusion in the tax base for the single tax paid in connection with the application of the simplified tax system.

Invoice under a simplified taxation system

4.2. According to Art. 421 of the Civil Code of the Russian Federation - each owner bears the burden of maintaining his property independently. An energy supply contract is concluded with the subscriber if he has a power receiving device that meets the established technical requirements, connected to the networks of the energy supply organization, and other necessary equipment, as well as providing metering of energy consumption. If other owners have the appropriate device, equipment and the ability to ensure energy consumption metering, they must enter into independent agreements with energy supply organizations and make independent payments to them. Accordingly, re-imposition by the owner who pays the costs of energy supply to other owners regarding their real estate is unacceptable. The only exception is the past period of time, for which payment for all real estate was made by this owner. If other owners do not have the appropriate device, equipment and the ability to provide metering of energy consumption, it is necessary to conclude subscription energy supply agreements between the owner making the payment and other owners, which must be agreed upon with energy supply organizations. Under these agreements, it will be possible to “re-invoice” energy supply costs. If other owners have the appropriate device, equipment and the ability to provide metering of energy consumption, “re-billing” the costs of paying for energy supply for the past period of time is possible in the form of recovery of unjust enrichment and interest for the use of other people’s money in pre-trial (filing a claim) or in court ok. After concluding independent contracts, other owners will make payments themselves. If other owners do not have the appropriate device, equipment and the ability to provide metering of energy consumption, “re-billing” the costs of paying for energy supply for the past period of time is also possible in the form of recovery of unjust enrichment and interest for the use of other people’s money in pre-trial (filing a claim) or in judicial procedure. In the future, “re-invoicing” will be carried out within the framework of subscription contracts.

Do I need to register?

Considering that an organization that uses the simplified tax system is not subject to VAT, it does not need to maintain a Book of Purchases and Sales, or a Journal of Received and Issued Documents. This frees the company from logging invoices without VAT and declaring them to the tax authority.

An organization that is not a taxpayer under a special tax system has VAT benefits to the tax authorities, in accordance with the legislation of the Russian Federation.

Whether to issue an invoice or not remains the right of the manager . But in order not to waste time and paper, it is better to justify to the counterparty the uselessness of this document and complete the transaction.

VAT invoice = obligation to pay VAT

An invoice must be issued within 5 calendar days from the date of shipment of goods (performance of work, provision of services) or from the date of receipt of payment. Draw it up in two copies, sign and give one copy to the counterparty.

Sometimes a customer asks to issue an invoice without VAT because his accounting department has the following procedure: for each purchase there is an invoice. In this case, you can issue an invoice, there will be no risk. Despite the VAT exemption, there are cases when the special regime must issue invoices.

In what cases are you required to issue an invoice:

- you are a VAT tax agent;

- work under a contract as an agent on your own behalf: purchase goods or services with VAT for a client on OSNO or sell goods or services to another company that works with VAT;

- participate in a simple partnership agreement, trust management of property or a concession agreement.

There is another case when you need to pay VAT - when importing goods from abroad, but then the tax is a customs payment.

In other cases, issuing an invoice is your voluntary matter. Please note: when issuing an invoice, you are obligated to pay VAT to the tax office and submit a VAT report. The income of the simplified tax system takes into account the amount of payment from the client excluding VAT.

Submit reports in three clicks

Elba - online accounting for individual entrepreneurs and LLCs. She will help you issue invoices, generate a VAT return and reporting according to the simplified tax system.

Try 30 days free Gift for new entrepreneurs A year on “Premium” for individual entrepreneurs under 3 months

Is it exhibited on “simplified”?

In an organization that operates under a simplified taxation system, it is optional according to the norms of the Tax Code of the Russian Federation, Federal Law No. 117, Article 346.11, clause 2. A company that operates under a simplified taxation system is not required to issue invoices , since the tax is imposed on a general monthly basis.

Considering its purpose, it is absolutely useless both for tax authorities and for companies with the simplified tax system. It is also useless for the counterparty, but sometimes the client needs this document for certain reasons.

The Tax Code of the Russian Federation implies the absence of an invoice for organizations with the simplified tax system.