Advance report and general rules for its preparation

So, the organization issues money on account. To begin with, it should be said that the issuance rules have changed a lot recently. However, one thing remains unchanged - the mechanism for working with accountable amounts must be spelled out in the company’s internal documents.

In order for the employee to receive the required amount, the director issues an order . With this order, the accountable person goes to the accounting department and receives money. Currently, it is possible to receive another amount without reporting the previously received amount.

After the funds have been spent, the employee must provide an advance report on them no later than 3 days later, relative to the date established in the order. All supporting documents must be attached to the advance report. It should be remembered that since online cash registers are now widespread, the check can arrive electronically, but it must be printed and attached to the expense report. If the document is lost or not on hand, written explanations must be attached to the report. In this case, only the director (in accordance with the established internal procedure) decides whether to accept expenses without documents as part of the report or not.

If an employee often takes out funds on account and always has a certain amount left on hand, then the tax office may oblige such amounts to be equated to the employee’s income with all the ensuing consequences. In such cases, the courts make decisions in favor of the tax authorities.

Accountability and online cash register: is it necessary to issue receipts?

The issuance of funds on account is an indirect form of payment for goods (work, services) between the buyer and the seller through a person authorized by the buyer (through an accountable person). And in this case, the question arises: does the organization that issued the money on account and accepts back the unspent balance need to carry out these operations through an online cash register (punch cash receipts)?

What is a “sub-report”

To issue money on account means providing funds to cover expenses associated with the activities of a legal entity or individual entrepreneur. This definition is given in clause 6.3 of Bank of Russia Directive No. 3210-U dated March 11, 2014 (LINK). Such issuance of funds is formalized by an expense cash order, which, in turn, is drawn up on the basis of one of the options:

- an administrative document on the issuance of accountable funds (most often a special order);

- written statement of the accountable person.

In addition, it would not be superfluous (but the law does not oblige you to do so) if the enterprise issues an administrative document that defines the list of persons to whom funds can be issued on account. An example of such an order:

The accountant’s application is written in any form, but with the obligatory indication of the requested amount of cash, the direction of its expenditure and the period for which these funds are issued.

The expenditure of funds or its absence is confirmed by drawing up an advance report by the accountable person. This document according to the wording of clause 6.

3 of Instructions No. 3210-U serves as a reflection of the status of the amounts issued to the employee on account, including unspent ones.

In fact, accountable funds are a form of realization of expenses by an enterprise necessary for the implementation of its activities. And these funds can be spent on anything: to cover debts to suppliers, to purchase materials, etc.

And the company entrusts the execution of such payments to its employee, who, after receiving the money on account, is both an accountable person (from the point of view of the origin of the funds) and an authorized person (from the point of view of the order of their expenditure). Those.

the accountable during procurement activities and when paying bills acts on behalf and at the expense of his employer and usually within the limits of the amount issued to him.

To understand who can issue money on account, you should refer to Banking Directive No. 3210-U. It says that the accountable person can be an employee of an entrepreneur or a legal entity with whom an employment or civil law contract has been concluded.

This is directly stated in paragraph 5 of Directive No. 3210-U and the letter from the Bank of Russia dated 02.10.

2014 No. 29-R-R-6/7859 (LINK), which, for the purposes of registering and conducting cash transactions, recognizes as an employee of the organization the person with whom the enterprise has a civil law agreement.

In this case, the duration of such an agreement does not matter. Moreover, the job title of the accountable person is not important. Therefore, the director of the company can also receive money against the report.

Are settlements on accountable amounts subject to Law No. 54-FZ

Accountable amounts can be issued either in cash or by transferring them to the employee’s corporate or even personal card marked “Accountable money”.

It is worth recalling that a bank card in accordance with paragraph 19 of Art.

3 of Law No. 161-FZ (on the national payment system) refers to electronic means of payment, which, based on Bank of Russia Regulation No. 383-P, are a non-cash form of payment.

And the July version of Law No. 54-FZ of 2021 states that the online cash register is used for cash and almost any non-cash forms of payment. However, settlements for accountable amounts in any form in the event of their return and issue are not settlements within the meaning of Law No. 54-FZ, since they do not include:

- to the receipt and payment of money directly for goods, works, services (i.e. to the monetary relations that arise between the buyer and the seller);

- to accept bets, interactive bets and pay out winnings on them;

- to accepting money during the sale of lottery tickets (including electronic ones);

- to accept lottery bets;

- for the payment of lottery winnings.

All these types of operations are recognized by Art. 1.

1 of Law No. 54-FZ for payments in which an online cash register is used, except for those cases in which the law itself provides for the possibility of not working with cash registers.

In addition, settlements that are subject to the obligation to use cash registers or the right not to use them also include the following transactions aimed at paying for goods, works, and services:

- acceptance and payment of money in the form of prepayment and (or) advances;

- offset and return of prepayment and (or) advances;

- issuance and repayment of loans (including lending by pawnshops);

- providing or receiving counter provision for payments for goods, works, services.

And the issuance and return of accountable amounts also does not apply to these operations, since this money is only a cash transaction, which is aimed at future expenditure, and does not reflect the very fact of payment for goods (work, services). And the accountable person is not a buyer in relation to his employer.

Therefore, when issuing to its employee or receiving from him the balance or the entire amount of unused accountable money, the company should not use an online cash register, but must comply with the requirements of Bank Instructions No. 3210-U on the preparation of cash documents (advance reports, cash orders, Cash Book).

Is it necessary to use an online cash register when an accountable person makes a purchase from another organization or entrepreneur?

In this situation, the accountable person acts as a buyer, acting on behalf and at the expense of his employer. This means that the seller is subject to all the requirements of Law No. 54-FZ for the use of an online cash register and for issuing (providing) a cash document to such a buyer. Such clarifications are given in paragraph 2 of the letter of the Federal Tax Service of Russia dated August 10, 2018 No. AS-4-20 / [email protected] - LINK.

The exception is those types of non-cash payments between legal entities and (or) entrepreneurs, including through accountable persons, in which an (for example, a bank card) is not presented

In this case, the seller does not use CCT (clause 9 of Article 2 of Law No. 54-FZ - LINK).

If on the contrary, and an electronic means of payment is presented for such settlements, then the seller must use cash register equipment to complete the settlement transaction.

conclusions

- The issuance and return of accountable money at an enterprise that provided these funds to its employee is not a settlement transaction within the meaning of Law No. 54-FZ. Therefore, the online cash register should not be used for this calculation.

- If the accountable person has paid with the money given to him for goods, work, or service, then the seller must issue a cash document (check, BSO or other document) to the specified person.

Moreover, the form of payment does not matter - cash or non-cash with the buyer presenting an electronic means of payment (ESP). - If payments for goods (work, services) between organizations and (or) entrepreneurs took place in a non-cash manner without presentation of an ESP, then the seller does not use the online cash register for such payments.

We advise you to look at a SELECTION OF USEFUL ONLINE SERVICES and SOFTWARE that will be useful to many entrepreneurs.

Call us by phone (we work in all regions of the Russian Federation) if you want to find out prices for cash registers, register a cash register with the Federal Tax Service, issue a cash register, connect an online cash register to the OFD.

What to pay attention to from July 1, 2021

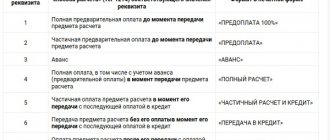

The Law on Online Cash Registers has also made adjustments to the procedure for confirming the legality of using accountable funds. Here you need to pay attention to two main innovations that relate to the use of strict reporting forms and the content of cash receipts .

| Form of strict accountability | Cash receipt |

| Until July 1, 2021, strict reporting forms can be filled out manually. However, starting July 1, 2021, hand-filled forms will be outlawed. From now on, strict reporting forms should be generated automatically, using special devices | Since the new law regarding cash transactions, checks have also changed a lot. They have a huge number of new mandatory details, without which the check will be considered invalid. One of the most striking new details is the QR code. In addition, the check contains general information about the company, the tax system used, and the website of the tax office. The check can be checked through the tax inspection service. It should also be remembered that, for example, entrepreneurs using a simplified system may not print the name of goods on receipts until February 1, 2021 |

Loss of documents

Situations are possible when an employee purchases the necessary goods (work, services), transfers them to the organization, but for some reason cannot document the expenses. This may also be the employee’s forgetfulness, which will result in the fact that he simply did not take the documents, or their loss - the reasons for the loss can be different, and the lack of documents is not a reason for not reporting on the amounts spent.

Whether to reimburse the employee for expenses or not in this situation entirely depends on the manager’s decision, therefore, even in the absence of supporting documents, the company’s accounting department, on the basis of a written order from the manager, accepts an advance report from the employee, where the supporting document may be an explanatory note indicating the circumstances and reasons for the lack of papers.

If the employee does not provide a receipt

An employee usually does not provide a receipt in two cases: he lost it or the seller works without a cash register.

It happens that the accountable person simply inadvertently loses the check or the check is damaged. Usually in such cases, a memo is attached to the expense report, where the employee explains where, when and for what reason he lost a specific check. If the director considers it necessary to reimburse such expenses, then the employee will receive the money spent, but it is better not to include such an amount in expenses, especially when applying the simplified tax system. After all, all expenses must be documented.

In the event that the seller does not issue a check due to the absence of a new cash register, you need to request a letter from the seller confirming the legality of the absence of cash registers or a copy of a document confirming that you are in special mode.

It is possible to receive a sales receipt or receipt without a cash receipt.

The accountant presented a cash receipt with a list of goods; is it necessary to request a sales receipt?

At the same time, in the letter of the Federal Tax Service of Russia dated June 25, 2013 N ED-4-3/ [email protected] “On documentary evidence of expenses for tax purposes,” attention is drawn to the fact that the List of required details of a cash register receipt of a cash register does not contain all the details of the primary accounting document in accordance with accounting legislation. In particular, the KKM cash receipt does not contain such details as “position name” and “signature” of the persons who performed the business transaction (the letter referred to the period of validity of the Regulations on the use of cash registers when making cash settlements with the population, approved by the Decree of the Government of the Russian Federation dated July 30, 1993 N 745). The basis for recognizing expenses for the acquisition of goods by an accountable person in this case will be an advance report approved by the head of the organization with a cash receipt attached to it containing a list of goods. In this case, the sales receipt may not be attached.

Please note => How ownership of an apartment in a new building is registered

Purchasing goods using imprest amounts

Probably the most common way to spend accountable funds is to purchase goods.

In most cases of purchase, a cash receipt is issued immediately at the checkout. This is an ideal option when a check is taken, an advance report is drawn up and transferred to the company’s accounting department for reporting.

With the commissioning of online cash registers, there is another opportunity to receive a check. The seller sends all information regarding the check via SMS or email link . It is printed and attached to the expense report.

It happens that the accountable person receives money in cash, and payment is made by card. In this case, you must provide a receipt for payment using the card. If payment is made from the card of another person, for example, a relative, then it is necessary to explain in writing why the goods were paid for by someone else, as well as a receipt that the money was transferred to the person who paid with the card.

Free legal assistance

On the use of cash registers" dated May 22, 2003 No. 54-FZ) are required to issue a cash register or BSO check to the buyer (clause 2, article 1.2 of law 54-FZ). Cash register receipt (BSO) is a primary accounting document printed using specially designed automated technology or generated in electronic form at the time of settlement between the seller and the client. Moreover, after a year of storage, you can even make copies of them and put them with the originals, since over time the clarity of the image on the receipts may be lost and it will no longer be possible to rely on them one hundred percent. How can you be left without a receipt, and what to do about it? A very unpleasant situation can happen if you lose your payment receipt before the debt is fully repaid. Sometimes you can be left without a receipt due to the fault of the terminal that has run out of paper.

Confirmation of accountable amounts for travel expenses

When confirming business expenses, you must keep in mind the following nuances:

- There may not be a receipt for accommodation, since hotels do not use cash registers until July 1 of the current year. In this case, only an invoice for payment can be provided

- If the employee went on a business trip in his own car, then fuel receipts and a voucher for the trip route are attached to the report

- If the employee traveled to the destination by train or plane, then it is necessary to provide not only a ticket, but also a document that will confirm that the trip actually took place. If you used an electronic ticket, you must provide a printout of it, as well as your boarding pass. If there is no coupon, then you can request from the carrier, for example, a certificate that will confirm that the employee was actually on the road. It is necessary to explain to employees that the boarding pass must be printed and this point must be fixed in the company’s internal documents that relate to travel expenses.

- If an employee travels by taxi while on a business trip, then you need to have a receipt for such transportation and attach it to the advance report

We accept a cash receipt from an accountable person

To confirm the expenses incurred, an individual provides the organization with a receipt as a document confirming payment for the goods, as well as a sales receipt, if there is no decoding of the purchased goods in the cash register receipt. In addition, an advance report must be prepared.

This is interesting: Decree on transfer to the reserve 2020

The accountable person purchases goods under a supply agreement

Thus, taking into account expenses a cash receipt that does not indicate the mandatory details listed in paragraph 6.1 of Article 4.7 of Federal Law No. 54-FZ of May 22, 2003, provided that the other necessary conditions are met, is a possible option.

In 2021, several amendments came into force that relate to documents confirming the expenditure of accountable funds - checks - paper and electronic. Although the list of documents required from accountants in the second half of the year has not changed so that the company can take into account costs when taxing, it is important that the evidence provided meets the new requirements.

This data is important if the employee purchases goods or services on behalf of a company or individual entrepreneur. If he spends money on a taxi, car wash or car repair, he must be given a receipt, not a BSO; such a replacement of a cash receipt remains in exceptional cases.

Registration of cash documents in electronic form

Thanks to the decisions of the Central Bank, it has become easier to conduct settlements with accountable persons in 2021, taking into account the latest changes: now cash documents when issuing and returning money can be executed electronically (clauses 5.1 and 6.2 of the Directive of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U). Thus, when registering cash receipt order 0310002 in electronic form, the recipient of the money has the right to put an electronic signature. And when registering a cash receipt order 0310001 (when returning unspent money to the cash desk), the depositor of the money is allowed to send a receipt to his email address, without paper registration.

This position is also reflected in the letter of the Ministry of Finance of Russia dated June 25, 2007 No. 03-03-06/1/392. Officials indicated that the consignment note (form No. TORG-12) is the primary accounting document confirming the costs. Papers that indirectly justify the expenses incurred (in particular, invoices) can only serve as an addition to the already existing “primary document”. Thus, expenses for the purchase of goods received without a delivery note from the supplier are considered undocumented.

And don’t forget that according to the Ministry of Finance today, a correctly executed cash document can only serve as confirmation of payment. To take into account, for example, paid materials, you need a delivery note or UPD.

Receipt without decryption of goods

The new BSO is almost no different from a regular online check. It must contain all the details, as in a cash receipt, including a QR code. The only difference is that it is called a strict reporting form (clauses 2 and 4 of Article 1.2 of Law No. 54-FZ).

We also note that until July 1, 2021, business entities named in paragraph 4 of Article 4 of Law dated July 3, 2020 No. 192-FZ (including participants in legal relations) may not use cash registers - if they have the right not to issue a document alternative to a cash receipt in the field of housing and communal services, major repairs, some areas of consumer lending) - LINK.

This is interesting: Register with the employment center in 2021

The employee spent his own funds – is this accountable or not?

Sometimes this situation happens - an accountable person travels on work matters, and the organization urgently needs a particular product. Often in such cases, the employee spends his personal funds on the purchase, and does not specifically return to the office for money. He buys the necessary goods, takes a check or other document confirming the fact of the transaction, and then, together with the expense report, provides all the documents to the company’s accounting department.

If the director agrees with such expenses, then the employee is returned the purchase amount without any problems.

It must be borne in mind that in such a situation we are not talking about accountable funds, since the organization did not issue funds to the employee in advance for specific purposes. Accordingly, the rules that apply to imprest amounts do not apply here. Refunds are made at the request of the employee. It is also not necessary to prepare an advance report; you can simply provide supporting documents.

If the accountant does not have documents confirming expenses

As for the taxation of accountable amounts with insurance premiums, this topic was not touched upon in the court decision. But by analogy, we can conclude that unconfirmed expenses of an accountable person must also be subject to contributions (Part 1, Article 7 of Federal Law No. 212-FZ of July 24, 2009). After all, in essence, accountable money must be considered as remuneration to an employee, and the opposite it will not be possible to prove due to lack of documents. In the case under consideration, the company decided not to demand from the employee the money paid for the product or service. And accept an advance report without documents confirming expenses. However, according to the court, since these expenses were not supported by documents, the employee must withhold personal income tax at a rate of 13% from the money that was issued for reporting. The servants of Themis explain this by saying that the base for personal income tax must take into account all the taxpayer’s income received by him both in cash and in kind, or the right to dispose of which he has acquired (Article 210 of the Tax Code of the Russian Federation).

Please note => Check arrests on a car by state number

Issuing a report when the cash register limit is exceeded

Another reason why organizations like to issue money on account is if the limit at the cash register is exceeded. The excess amount is simply given to the responsible person, thereby regulating the balance. Such amounts are spent and confirmed in the general manner.

By the way, if necessary, the accountable person can return the funds back to the cash desk as excess accountable amounts.

The accountant is a financially responsible person. He receives funds from the accounting department's cash desk, or directly to the employee's bank card and spends them on the needs of the organization. For all amounts spent, you must provide an advance report, to which all supporting documents are attached. The Law on Online Cash Registers makes its own adjustments to this procedure. Now it is very carefully necessary to check whether all the necessary details are contained in the check and whether strict reporting forms are issued correctly.

Sales receipt without cash register

• amounts issued to the employee on account and correctly used by him can be accepted by the employer company to reduce the tax base (if they are available in the completeness required by law, papers are needed confirming both the fact of payment for goods or services and their receipt); So from tomorrow they have to punch checks using new cash registers. The only thing in which the Federal Tax Service promised to meet entrepreneurs halfway was that at first it would not impose fines on those of them who, due to a shortage of devices on the market, were unable to acquire them.

24 Dec 2021 marketur 168

Share this post

- Related Posts

- Calculator for calculating penalties at the refinancing rate

- Family composition certificate free or paid

- Benefits for pensioners in the Lipetsk region in 2021

- What happens if you flee the scene of an accident?