Novice financiers are faced with the problem of correctly distributing positions among sections of the balance sheet. Economists experience particular difficulties when accounting for settlement transactions with personnel.

Let’s figure out how to determine the correct wording: asset or liability, debt to employees for wages or arrears of monthly contributions. In addition, we will clarify the nuances of accounting for the reserve for doubtful debts and settlements with accountable employees.

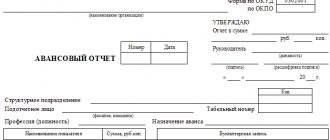

Data source - account 71

The balance sheet includes the debt of employees and the employer for accountable amounts from accounting. All necessary information is accumulated on account 71 “Settlements with accountable persons.

The debit of account 71 reflects the amounts issued to employees:

- for various administrative and economic needs: purchase of stationery, payment for repair services for office equipment, purchase of household chemicals and cleaning products for office cleaning, etc.;

- to pay for travel expenses: purchasing tickets, paying for rented accommodation on a business trip, hotel services, etc.;

- for entertainment and other similar expenses.

Entries on the debit of account 71 are made on the basis of supporting documents: cash receipts orders or bank statements, depending on the source of payment: from the cash register in cash or in non-cash form through a bank account to the accountant’s card.

If an employee spent more than was given to him, the debit of account 71 reflects the amount of repayment by the employer of the overexpenditure to the employee.

Debt on accountable amounts asset or liability

The rest has already been answered correctly. Let me correct you a little Irik:p. 4 Finished products shipped, D 90 K 43, p. 5 The production cost of goods sold is written off D 90 K 43p. 6 settlements with creditors were made at the expense of the loan account D 60 (76) K 55p. 8 - only D 70 K 73 1. Received from the current account to the cash desk: - for payment of wages - for travel expenses D 50 K 512. Issued from the cash desk wages D 70 K 503. Materials received from suppliers D 10 K 60/14.

Finished products have been shipped. In this case, the implementation of D 62/1 K 90/1 is already underway (Irik and Alexey are wrong)5. The production cost of goods sold is written off D 90/2 K 436. Settlements with creditors have been made at the expense of the loan account D 60 (76) or other creditors K 66 (67) 7. An advance payment for products D 51 K 62/28 was received in the bank account. The advance payment issued to the account D 70 K 719 was withheld from the salary.

Filling out the balance: two general rules

If on the date of drawing up the balance sheet for account 71 you have non-zero debit and/or credit balances, the “accountable” debt must be reflected in it. In this case, two important rules should be observed:

This means that the debt of reporting entities is reflected in the balance sheet in expanded form: separately for debit and credit - if the relevant data is available in the records.

The second rule for reflecting settlements with accountables in the balance sheet is related to the period of circulation (repayment) of accountable amounts:

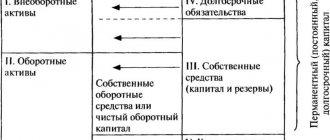

Typically, settlements with accountable persons occur multiple times within a calendar year, that is, they are short-term in nature. Therefore, they are reflected in the assets of the balance sheet in section II “Current assets”, and in the liabilities in section V “Current liabilities”.

If, based on the specifics of the company’s work and the specifics of relationships with accountable persons, certain amounts are repaid within a period exceeding 12 months after the reporting date, these amounts should be shown in the balance sheet based on the general rules - as part of long-term assets.

Assets and liabilities of the balance sheet. Grouping of property and sources of its formation (page 1 of 5)

Ministry of Education and Science of the Russian Federation

State Educational Institution of Higher Professional Education "UFA STATE PETROLEUM TECHNICAL UNIVERSITY"

Department of Accounting and Auditing

in the discipline "Accounting"

Associate Professor, Ph.D. A.M. Nizamutdinova

Task 1. Assets and liabilities of the balance sheet. Grouping of property and sources of its formation.

Based on the data to complete the task, determine which part of the balance sheet (asset or liability) specific types of property and the sources of its formation belong to, and then draw up a balance sheet.

Balance sheet of OJSC "Stankostroitel" as of 01/01/200.

| Assets | Magnitude. thousand roubles. | |

| Fixed assets | ||

| 1.Fixed assets including: | 120 | |

| 1.1.Buildings: | 120 | |

| Production workshop buildings(8) | 120 | 420 |

| Material warehouse buildings for finished products(9) | 120 | 350 |

| Administration building(10) | 120 | 290 |

| 1.2.Machinery and equipment: | 120 | |

| CNC machines in a finished goods warehouse(2) | 120 | 200 |

| Production equipment in assembly shops(3) | 120 | 850 |

| 2.Intangible assets | 110 | |

| Business reputation of the organization (25) | 110 | 5 |

| Organizational expenses and the account of the founders' contribution to the authorized capital(26) | 110 | 15 |

| Design Rights(27) | 110 | 2 |

| 4. Long-term investments in enterprise securities (14) | 140 | 250 |

| Total for the first section | 2360 | |

| Current assets | ||

| 1.Inventory: | 211 | |

| 1.1.Basic materials: | ||

| Round steel in stock (4) | 211 | 340 |

| Components in stock (6) | 211 | 820 |

| Non-ferrous metals in stock (7) | 211 | 30 |

| 1.2.Other materials: | ||

| Other materials in stock (5) | 211 | 70 |

| Writing paper (11) | 211 | 40 |

| Fax powder (21) | 211 | 5 |

| 2. Work in progress (1) | 213 | 960 |

| Self-made semi-finished products (12) | 213 | 60 |

| 3. Deferred expenses (20) | 216 | 8 |

| 4.Finished products (15) | 214 | 800 |

| 5. Cash: | 260 | |

| Cash in the company's cash register (28) | 261 | 10 |

| Current account (29) | 262 | 380 |

| Currency account (35) | 260 | 30 |

| 6.Short-term investments in enterprise securities (13) | 250 | 25 |

| Short-term loans provided to other enterprises(16) | 250 | 55 |

| 7. Funds in calculations: | ||

| Advances to suppliers for materials (17) | 230 | 120 |

| Total for the second section | 3775 | |

| Balance | 6135 | |

| Passive | ||

| Capital and reserves | ||

| 1. Authorized capital(30) | 410 | 3500 |

| 2.Additional capital(31) | 420 | 90 |

| 3.Reserve capital(32) | 430 | 160 |

| 4.Profit: | ||

| 4.1.Profit of the reporting year (33) | 470 | 170 |

| 5.Targeted financing(34) | 450 | 140 |

| Total for the third section | 4060 | |

| long term duties | ||

| 1.Long-term loans(24) | 510 | 930 |

| Total for the fourth section | 930 | |

| Short-term liabilities | ||

| 1.Short-term loans(23) | 610 | 160 |

| 2. Accounts payable: | 620 | |

| Accounts payable for electricity(22) | 621 | 5 |

| Debt of enterprises to suppliers of materials(18) | 621 | 180 |

| Advances received from buyers(19) | 621 | 170 |

| Debt to employees of the enterprise for wages (36) | 622 | 210 |

| Debt to the budget for personal income tax(37) | 624 | 130 |

| Debt of the enterprise and social insurance authorities(38) | 623 | 290 |

| Total for the fifth section | 1145 | |

| Balance | 6135 |

TASK 2. ACCOUNTS AND DOUBLE ENTRY. REFLECTION OF BUSINESS OPERATIONS ON ACCOUNTS

Purpose of the task

: mastering the procedure for reflecting business transactions in accounting accounts.

Exercise:

Based on data to complete the task: open accounting accounts; reflect business transactions in the accounting accounts using the double entry method; calculate turnover and final balances; draw up a balance sheet based on the final balances.

Data for completing the task Balance sheet of the plant December 1, 200_

| Assets | Amount, thousand rubles | Passive | Amount, thousand rubles |

| Fixed assets including: | 2500 | Authorized capital | 3000 |

| PROFIT 99 | 2400 | ||

| buildings, machines, equipment | 2500 | Short-term loans | 2000 |

| Stocks including: | Accounts payable including: | ||

| raw materials | 1800 | before the budget | 440 |

| unfinished production | 900 | on insurance | 500 |

| finished products | 400 | on wages | 1015 |

| Cash including: | 2815 | other creditors | 60 |

| cash register | 15 | ||

| current accounts | 2800 | ||

| Accounts receivable including: | 1000 | ||

| buyers | 750 | ||

| other debtors | 250 | ||

| BALANCE | 9415 | BALANCE | 9415 |

Business transactions for December (postings)

| 10-Materials | |

| D | TO |

| CH=1800 | |

| 7)250 13)40 | 11)320 |

| Vol.=290 | Vol.=320 |

| Sk=1770 |

Solution

: We will open accounting accounts and post business transactions:

Reportable debts in a simplified balance sheet

Debt on accountable amounts must also be reflected in the simplified balance sheet. The same rules and approaches apply as described above for a regular balance.

The only clarification is that in the simplified balance sheet, the lines where accountable debt falls are called slightly differently:

Let us remind you that clause 4 of Art. 6 of the Law of December 6, 2011 No. 402-FZ “On Accounting”. Small enterprises, non-profit organizations, and participants in the Skolkovo project have the right to draw up a simplified balance sheet using the form from Appendix 5 to Order No. 66n of the Ministry of Finance of Russia dated July 2, 2010.

Penalty for errors in reporting

If you show the final balance of payments in the balance sheet (the difference between accounts receivable and accounts payable on account 71), the indicators on line 1230 “Accounts receivable” of the asset and line 1520 “Accounts payable” on the liability side of the balance sheet will be unreliable. And this is fraught with negative consequences: a distortion of any balance sheet indicator by 10% or more is considered a gross violation of accounting rules.

The punishment for this violation is a fine on company officials from 5,000 to 10,000 rubles. (Article 15.11 of the Code of Administrative Offenses of the Russian Federation). If the violation is committed and detected again, the fine will double. And the top officials of the company may be disqualified for a period of 1 to 2 years.

Contents of terminology issues

The balance sheet of an enterprise consists of two sections that balance each other - assets and liabilities.

Let's start the conversation by clarifying key definitions. The accounting book is a table where financiers make entries about the ownership of the enterprise and the sources of obtaining this capital in special columns.

In addition, accounts payable are also recorded here. Thus, the company’s accounting consists of two sections - assets and liabilities.

Note that the correct definition of positions is a key criterion for the correct reflection of information.

Consider, based on such records, the organization’s management or potential creditors are analyzing the liquidity and solvency of this enterprise. Moreover, the accounting structure is determined by the conditional formula:

“Property + Liabilities = Assets = Liabilities.”

Note! Economists say that the source of an asset becomes a liability - after all, the use of such instruments contributes to the company’s profit. When it comes to the supply of goods in advance, accountants classify customer debt as assets

When it comes to the supply of goods in advance, accountants classify customer debt as assets

However, let’s return to the main topic of discussion and find out whether customer debt is an asset or liability on the balance sheet. Since this position relates to debtors' debts, economists say that the correct solution here is to record a line in the liquid fund section.

After all, these funds become the working capital of the enterprise, which guarantees profit in the future.

True, transactions related to settlements are considered transitional, because here the posting is determined by the time of transfer of funds and delivery of products. In cases of prepayment of delivered goods by counterparties, the company enters such transactions into the liability side of the balance sheet.

Accordingly, experienced accountants call such things active-passive transactions.

Documentation

So that in the future there are no questions about how a specific figure appears, the transaction between the enterprise and buyers is recorded and documented.

Moreover, in this situation, the fact of services performed or goods delivered is supported by both parties. The lender retains the initial cooperation agreement, which sets out the key terms and conditions of interaction.

The basis for reflecting a specific transaction in the balance sheet is primary documentation

In addition, an invoice for payment is attached to the list of required papers. True, this document will be required in situations of concluding long-term agreements. When completing a one-time transaction for a specific batch of products, this paper is not used. However, an indispensable attribute of the company’s primary documentation is the act of completion of work or the invoice.

Note! To avoid misunderstandings and disputes later, the buyer signs and stamps such forms, confirming the actual receipt of the service or product. When a company is considered a VAT payer, an invoice also becomes a necessary basis for recording in the balance sheet

This paper contributes to the correct distribution of the amount transferred to the budget from the amount of funds sold. As for the papers on the buyer’s side, the main document here is considered to be a bank statement about the money transferred to the lender’s accounts. If payment is made through the cash register, the statement is replaced by a receipt

When a company is considered a VAT payer, an invoice also becomes a necessary basis for entry into the balance sheet. This paper contributes to the correct distribution of the amount transferred to the budget from the amount of funds sold. As for the papers on the buyer’s side, the main document here is considered to be a bank statement about the money transferred to the lender’s accounts. If payment is made through the cash register, the statement is replaced by a receipt.

Nuances

Keep in mind that the employee who maintains the organization’s accounting, in such circumstances, cooperates with the person responsible for product accounting. In these situations, a product inventory is periodically carried out, which is verified with actual balance sheet indicators based on primary documentation.

If there is a discrepancy between the number of goods in the warehouse and the transactions reflected in the accounting department, an inventory will be required and the records adjusted

Please note that when discrepancies are identified, both employees study the reasons for such situations. Then there will be an accounting adjustment, which is confirmed by the relevant papers. Please note that the documentation is signed by the reviewing parties with a date stamp for the audit.