The enterprise balance sheet is the main source of data for analytical activities. The information obtained using its indicators makes it possible to determine the financial stability of the company, the efficiency of its work, and even assess development prospects. This information is needed both by the company’s management itself to develop strategies for the organization’s functioning and identify problems that interfere with maximizing profits, and by counterparties (clients, investors, regulatory authorities, banks) as a guarantor of the solvency and reliability of the partner.

How to assess the financial condition of an enterprise

To begin with, an initial assessment of the company's position is carried out. For this, two main reporting forms are used - Balance Sheet and Profit and Loss Statement.

Take our proprietary course on choosing stocks on the stock market → training course

At this stage, changes in the size of property and its sources that have occurred over the year are simply stated, and relationships between the lines of reporting forms are identified.

The so-called express analysis also involves the calculation of the most indicative values that allow us to draw conclusions about the position of the company, as well as the dynamics of its development. Such indicators, in particular, include:

- The security of the assets on the company's balance sheet with its own property: the difference between the result of the first section of the liability side of the balance sheet (sources of property) and the first section of the asset side of the balance sheet (the actual value of fixed assets and non-current assets);

- The amount of immobilized working capital (in particular, the amount of receivables is considered);

- The provision of actual material property with sources of its formation;

- Solvency of the company (the ability to quickly pay off urgent debts, which is determined by the presence of sufficient amounts in current accounts and the absence of overdue debts to creditors).

Also, when assessing the financial condition, the coefficients of financial stability and liquidity are necessarily studied.

Liquidity is the ability of a company to pay debts to creditors in a fairly short time by selling working capital (in this case, violation of deadlines is acceptable).

Analysts use the following three liquidity measures.

1. Current liquidity (coverage ratio) is a value demonstrating the sufficiency (or lack) of the enterprise’s assets to pay short-term debts during the year. The indicator is calculated using the following formula:

Current assets: Short-term liabilities

2. Quick liquidity (“critical assessment”) - the indicator reflects the ability of the enterprise to repay urgent debts with the liquid part of the property. Those that are not so easy to sell (for example, inventories) are excluded from liquid assets. The formula looks like this:

Liquid assets: Short-term liabilities

3. Absolute liquidity - this indicator provides information about the amount of debt that can be paid immediately with the company’s maximum liquid funds (that is, money). The value is calculated as follows:

(Money in accounts and on hand + short-term financial investments): Short-term liabilities

Financial stability indicators are included in a special group.

In practice, the following are most often calculated:

- Autonomy coefficient (Equity: Total capital) - shows what part of accounts payable can be reimbursed with one’s own funds and should normally exceed 50%;

- Dependency coefficient (Total capital: Equity capital) is the inverse of the autonomy coefficient, showing the participation of borrowed funds in ensuring the functioning of the company;

- Gearing Ratio (Liabilities: Equity);

- Investment coverage ratio ((Equity capital + Long-term liabilities) : Total capital);

- The ratio of coverage of current assets with own working capital, showing what part of these assets is covered by own property (Own property: Current assets);

- The coefficient of provision of the MPZ with its own property, showing the degree of independence of the MPZ from borrowed funds (Own property: MPZ).

Important!

All indicators characterizing the financial condition of the company are calculated at the beginning and end of the year. They are compared both in dynamics and with standard values. Based on the results of such an analysis, conclusions are drawn about the prospects for the company’s development given existing trends, the reasons that caused the changes, and problems are identified that interfere with maximizing profits and increasing the risks of a financial crisis.

The meaning of the word balance

What we are trying to say is that it is impossible to consider the balance sheet in chronological order, say, in this way: in the ancient world the balance sheet was drawn up on papyri, in the Middle Ages on parchment, then one French author mentioned the balance sheet in his early work, then another German author proposed the concept of such - balance, etc.

Alla P. Vitkalova 8a3330c9-eb35-102b-9810-fbae753fdc93 Dina P. Miller 3852d604-eb3a-102b-9810-fbae753fdc93 How to draw up a balance sheet This practical guide outlines two views on the problem of studying the balance sheet: the balance sheet as an element of the accounting method and balance sheet as the main form of accounting (financial) reporting.

When an accountant starts talking about a balance sheet, you can be 100% sure that he doesn’t mean a tightrope walker balancing on a tightrope, or an acid-base balance, or an input balance, or even the results of some calculations, but a standard reporting form .

A disturbance in the energy balance cannot remain without consequences - be it the balance of a small unit called a family, or the world balance as a whole.

The modern balance sheet, along with other forms of reporting, is used by external users to assess the property and financial position of the organization, so it is very relevant that the textbook examines the features of creative accounting as a method of regulating balance sheet indicators in accordance with the goals of the balance sheet policy.

Taking too much of any substance over a long period of time can cause a chain reaction that can lead to an imbalance of all elements, which can lead to the development of disease. By eating a balanced diet of whole foods, you can maintain the optimal ratio of minerals in your body. body. Calcium regulates cardiac activity, blood clotting and the overall balance of minerals in the body, ensures the strength of the tissues of teeth and bones.

Only original works explain not the consequences of the adopted method of accounting, like textbooks on balance sheet analysis, and not the procedure for filling out the approved balance sheet form, like practical accounting manuals, but the method of accounting itself... and, accordingly, the balance sheet as the most famous and at the same time controversial reporting form.

An analysis of the nineties gave me the opportunity to do this: the successes of the Clinton administration can be partly attributed to the fact that in some areas the right balance between market and government was found, a balance lost in the Reagan and Thatcher decades; but our failures - some of which only emerged outside the nineties - can be partly attributed to the fact that in other areas we have struck this balance incorrectly.

The most terrible and incomprehensible word for little Vasya was the word “balance”, which he was very afraid of and immediately calmed down if he, being naughty, was threatened with a finger and said: “Hush, dad is doing balance...” This balance seemed to the boy in the form of an invisible monster that often settled in their house, especially at the end of each year, and brought panic to all household members.

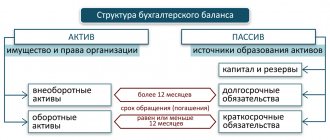

The concept of liabilities on the balance sheet of an enterprise

The liability side of the balance sheet is that part of Form No. 1, which reflects the sources of formation of property. This includes the company's liabilities and its capital.

Passive sections

The passive part of the form includes three sections. They are described below.

| Section number | Name | Content |

| I | Capital and reserves | Here you can find information about the share capital (the initial contribution of the founders), additional and reserve funds (created during the operation of the company), profit (loss). |

| II | long term duties | Fee-based loans provided to the company for a long term (that is, for a period longer than one year). |

| III | Short-term liabilities | Short-term debts to counterparties of various types: the tax office and government funds, own employees, suppliers, credit institutions, etc. Usually, by the end of the year, enterprises try to pay off this type of debt, so often there are no amounts in the annual balance sheet for the corresponding lines. |

Liability accounts

The liabilities side of the balance sheet presents the totals for the following groups of accounts:

- Active-passive: 60, 62, 68, 69, 71, 75, 76, 84, 90, 99;

- Passive: 66, 70, 80, 98.

Composition and structure of capital (liabilities) - diagram

The diagram shows the composition of the liabilities side of the balance sheet. During analytical activities, special attention is paid to the proportions of equity and debt capital.

Having a sufficient amount of own funds ensures the financial stability of the company. At the same time, it is inappropriate to finance activities exclusively from your own sources - this way you can miss out on many benefits. For example, the fee for using borrowed funds may be much lower than the profit that the enterprise will receive from investing in the business.

Therefore, finding the optimal ratio between equity and debt capital (as well as between short-term and long-term liabilities) is an important task for managers and analysts.

What is a liability in accounting?

Liability is a component of the balance sheet. Information from accounting documents will provide the following data:

- objects that are owned by the enterprise;

- financial performance results;

- sources of company funds.

What are the features of filling out the liabilities side of the balance sheet ?

Assets reflect information about the property of the enterprise. Liabilities allow you to determine the sources of available capital. On the right side of the accounting table the following is recorded:

- The enterprise's own funds (include the authorized capital, as well as profits that have not been distributed).

- Loans and credits.

- Funds that were raised.

the sources of property formation grouped in the liabilities side of the balance sheet ?

To simplify things, liabilities are sources of assets. This connection is due to the fact that liability management leads to an increase in assets. Liabilities and assets are inextricably linked. They form a balance. The accounting spreadsheet has this name due to the fact that the liability is equal to the asset. Both indicators balance each other.

IMPORTANT! Asset and liability reflect the main principle of accounting - the principle of double entry.

Example

The essence of assets or liabilities is easier to understand from an example. The company takes out a loan of 2,000,000 rubles. This operation must be reflected in accounting:

- 2 million are reflected in the accounts. They must be recorded in the list of assets;

- 2 million are indicated in the “Loan debts” account. The indicator must be recorded in the list of liabilities.

That is, information about the receipt of funds can be obtained from assets. From liabilities, the source of money becomes clear - lending.

Analysis of liabilities of the enterprise balance sheet

The main tasks of analyzing the liability side of the balance sheet include:

- Study of the dynamics of the size of equity and debt capital;

- Study of capital structure;

- Analysis of the use of funds;

- Identification of reserves for growth of equity capital;

- Search for the optimal relationship between the structural parts of capital.

By examining the passive part of the balance sheet, you can understand in what amount and from whom the company raised funds in the analyzed year.

The financial stability of the company increases the share of equity capital in the total amount of property. This indicator demonstrates the company's ability to repay debts on its own and makes it attractive and reliable in the eyes of creditors and investors.

The analytical activities themselves are carried out by compiling tables in which the proportions of all structural parts of capital to its total value are calculated (indicators are taken at the beginning and end of the year). Changes in ratios are identified and assessed, conclusions are drawn and recommendations for further action are formulated.

Company Balance Sheet

An organization's balance sheet is the summary of its activities for a specific period of time. This form most clearly demonstrates the principle of double entry accepted in accounting - the results of the active and passive parts of the balance sheet are always equal.

There are many types of balance sheets:

- By moment of filling: introductory and final;

- By degree of consolidation: single or consolidated;

- By period: annual or intermediate;

- According to the filling method: balance or reverse.

For analysis in practice, the annual balance sheet is most often used - form number one, filled out at the end of the year.

Example of analysis of balance sheet liability items

It is most convenient to consider the analysis of passive balance sheet items using an example.

Example. The results of the functioning of CONTINENT LLC are as follows.

| Article title | For the beginning of the year | Specific gravity | At the end of the year | Specific gravity | Change in value | Share change |

| ||||||

| Authorized capital | 9,95 | 0,09 | 10,61 | 0,1 | + 0,66 | + 0,01 |

| retained earnings | 20,92 | 0,2 | 22,39 | 0,22 | + 1,47 | + 0,02 |

| Total for the section | 30,87 | 0,3 | 33 | 0,33 | +2,13 | +0,03 |

| ||||||

| Loans and credits | 2,48 | 0,02 | 5,63 | 0,05 | + 3,15 | + 0,03 |

| Total for the section | 2,48 | 0,02 | 5,63 | 0,05 | + 3,15 | + 0,03 |

| ||||||

| Debt to creditors, including: | 69,83 | 0,68 | 65,21 | 0,63 | – 4,62 | – 0,05 |

| suppliers | 59,07 | 0,57 | 57,33 | 0,55 | – 1,74 | – 0,02 |

| staff | 5,42 | 0,05 | 2,66 | 0,03 | – 2,76 | – 0,02 |

| Tax office and funds | 4 | 0,04 | 3,2 | 0,03 | – 0,8 | – 0,01 |

| Other creditors | 1,34 | 0,01 | 2,02 | 0,01 | – 0,68 | – |

| Total for the section | 69,83 | 0,68 | 65,21 | 0,63 | – 4,62 | – 0,05 |

| Balance | 103,18 | 103,84 |

The table shows that in absolute terms the amount of equity capital has increased. His share in the total property of the company also increased. There was an increase in long-term borrowings in the same proportions.

But the size of short-term liabilities has decreased significantly (mainly due to debt items to suppliers and personnel).

In general, the current situation is assessed positively: the financial stability and independence of the company is growing, borrowed funds with a long repayment period are being attracted into circulation in order to expand the activities of the LLC and maximize profits.

Indicators characterizing the market stability of an enterprise

During the analysis, a number of indicators are calculated that allow one to judge the financial autonomy of the company. Let's take a closer look at them.

Financial autonomy coefficient (share of equity capital in total capital)

The autonomy coefficient shows what part of the debts can be repaid with one’s own funds. Normally, this figure should exceed 50%. It is calculated like this:

Equity: Total capital

Financial dependence ratio (share of borrowed capital)

The dependence coefficient is the inverse value of the autonomy indicator, showing the participation of borrowed funds in ensuring the functioning of the company. The indicator is calculated as follows:

Total capital: Own capital

Leverage of financial leverage (financial risk ratio)

This coefficient reads as follows:

Debt capital / Equity capital

Obviously, the lower the level of financial leverage, the greater the financial stability of the company.

Financial position of the enterprise

Any retail company must always maintain a very accurate balance sheet. A business owner needs to know the financial health of the business before making plans for the next year or considering expansion. The banker needs the company's balance sheet to make a decision on extending the loan or providing new services. If a business owner is looking for investors or partners, he must take into account that they will look at the current balance sheet of the enterprise. If liabilities exceed assets, questions may arise about the prospects of the enterprise. The company may have too much debt or too many accounts payable and receivable. An enterprise with a negative balance is a warning to banks and other counterparties. It is also a warning to the owner that the business is under financial stress and that although the company appears to be doing well, it needs to make adjustments to make a profit in the long term.

In-depth structural analysis of the enterprise’s capital (stages, tasks)

A deeper structural study of the passive part of the balance sheet involves studying the relationship between borrowed and own sources of financing activities, a detailed assessment of changes in their levels with a study of the reasons for these changes, and searching for the optimal relationship between long-term and short-term debts.

Assessment of short-term and long-term sources of borrowed capital

When examining the structure of long-term and short-term debts, it is the growth of long-term liabilities that is positively assessed, since they have a number of advantages:

- Providing the company with prolonged financial sources necessary for investing in capital transformations;

- Increasing current solvency;

- Increased financial stability.

As for short-term accounts payable, the proportions between bank loans and debts to personnel, counterparties, tax and funds, etc. are examined here.

Bank loans are considered more expensive sources of financing compared to cheap (and sometimes free) other short-term obligations. However, you need to be careful here: sometimes penalties for late payment of taxes or late payment under an agreement can be quite significant.

Assessing the balance for signs of “good” balance

The final stage of the analysis is to evaluate the balance sheet for signs of a “good” report. It is considered that the position of the company is favorable and stable if:

- The amounts in the balance sheet totals are growing, and the rate of their increase exceeds the rate of inflation;

- The size of current assets increases faster than the amount of non-current assets;

- Current assets exceed short-term liabilities in value terms by at least 1.5 times (this also applies to their growth rate);

- In the active half of form No. 1 there is the minimum required amount of maximum liquid assets (that is, cash);

- The size, growth rate and shares of receivables and payables are approximately the same;

- The size and growth of long-term sources are greater than similar indicators for non-current property;

- The share of equity capital in the sum of all sources is at least 50%;

- There is no item in the balance sheet that directly indicates the financial ill health of the company - an uncovered loss.

In the dictionary Dictionary of foreign words

I

a, pl. No m.

1. The ratio of mutually related indicators of some activity or process. B. production and consumption. a Trade balance is the ratio of imports and exports. Heat balance (physical, technical) - 1) the relationship between available heat resources and their consumption, including losses in furnaces, engines, steam boilers, etc.; 2) the arrival and consumption of heat in the atmosphere, on the earth’s surface. Water balance is the inflow and flow of water (from precipitation, snow melting, evaporation and water runoff).

2. Finnish Comparative total of income and expenses. Annual b. Let down b. and Active balance (fin.) - the excess of income over expenses or the export of goods over their import. Passive balance (fin.) - the excess of expenses over receipts or the import of goods over their export.||Cf. BALANCE" title='BALANCE, BALANCE is, what is BALANCE, BALANCE interpretation'>BALANCE.

3. Finnish A summary statement reflecting in monetary terms the state of the enterprise’s funds by their composition and placement, sources, purposes, payment terms, etc. and To be (have) on the balance sheet (fin.) - about some kind of thing. material object: to be, be under the financial control of an enterprise, institution, which provides for the costs of maintaining this object and income from its functioning. Take (take) something onto (your) balance sheet (fin.) - include (include) some object in the balance sheet. Transfer (transfer) something to the balance sheet (fin.) - transfer (transfer) to another enterprise, institution the right to include some object in its balance sheet. Balance - related to balance. II

a, m.

A part of a clock mechanism in the form of a ring with a crossbar, serving as a speed regulator; same as balancer.

Share the meaning of the word: